false

2023

FY

0001793895

0001793895

2023-01-01

2023-12-31

0001793895

dei:BusinessContactMember

2023-01-01

2023-12-31

0001793895

2023-12-31

0001793895

2022-12-31

0001793895

2022-01-01

2022-12-31

0001793895

2021-01-01

2021-12-31

0001793895

CDTG:SewageTreatmentSystemsMember

2023-01-01

2023-12-31

0001793895

CDTG:SewageTreatmentSystemsMember

2022-01-01

2022-12-31

0001793895

CDTG:SewageTreatmentSystemsMember

2021-01-01

2021-12-31

0001793895

CDTG:SewageTreatmentServicesAndOthersMember

2023-01-01

2023-12-31

0001793895

CDTG:SewageTreatmentServicesAndOthersMember

2022-01-01

2022-12-31

0001793895

CDTG:SewageTreatmentServicesAndOthersMember

2021-01-01

2021-12-31

0001793895

us-gaap:CommonStockMember

2020-12-31

0001793895

us-gaap:AdditionalPaidInCapitalMember

2020-12-31

0001793895

CDTG:RetainedEarningsStatutoryReservesMember

2020-12-31

0001793895

CDTG:RetainedEarningsUnrestrictedMember

2020-12-31

0001793895

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2020-12-31

0001793895

us-gaap:NoncontrollingInterestMember

2020-12-31

0001793895

2020-12-31

0001793895

us-gaap:CommonStockMember

2021-12-31

0001793895

us-gaap:AdditionalPaidInCapitalMember

2021-12-31

0001793895

CDTG:RetainedEarningsStatutoryReservesMember

2021-12-31

0001793895

CDTG:RetainedEarningsUnrestrictedMember

2021-12-31

0001793895

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2021-12-31

0001793895

us-gaap:NoncontrollingInterestMember

2021-12-31

0001793895

2021-12-31

0001793895

us-gaap:CommonStockMember

2022-12-31

0001793895

us-gaap:AdditionalPaidInCapitalMember

2022-12-31

0001793895

CDTG:RetainedEarningsStatutoryReservesMember

2022-12-31

0001793895

CDTG:RetainedEarningsUnrestrictedMember

2022-12-31

0001793895

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2022-12-31

0001793895

us-gaap:NoncontrollingInterestMember

2022-12-31

0001793895

us-gaap:CommonStockMember

2021-01-01

2021-12-31

0001793895

us-gaap:AdditionalPaidInCapitalMember

2021-01-01

2021-12-31

0001793895

CDTG:RetainedEarningsStatutoryReservesMember

2021-01-01

2021-12-31

0001793895

CDTG:RetainedEarningsUnrestrictedMember

2021-01-01

2021-12-31

0001793895

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2021-01-01

2021-12-31

0001793895

us-gaap:NoncontrollingInterestMember

2021-01-01

2021-12-31

0001793895

us-gaap:CommonStockMember

2022-01-01

2022-12-31

0001793895

us-gaap:AdditionalPaidInCapitalMember

2022-01-01

2022-12-31

0001793895

CDTG:RetainedEarningsStatutoryReservesMember

2022-01-01

2022-12-31

0001793895

CDTG:RetainedEarningsUnrestrictedMember

2022-01-01

2022-12-31

0001793895

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2022-01-01

2022-12-31

0001793895

us-gaap:NoncontrollingInterestMember

2022-01-01

2022-12-31

0001793895

us-gaap:CommonStockMember

2023-01-01

2023-12-31

0001793895

us-gaap:AdditionalPaidInCapitalMember

2023-01-01

2023-12-31

0001793895

CDTG:RetainedEarningsStatutoryReservesMember

2023-01-01

2023-12-31

0001793895

CDTG:RetainedEarningsUnrestrictedMember

2023-01-01

2023-12-31

0001793895

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2023-01-01

2023-12-31

0001793895

us-gaap:NoncontrollingInterestMember

2023-01-01

2023-12-31

0001793895

us-gaap:CommonStockMember

2023-12-31

0001793895

us-gaap:AdditionalPaidInCapitalMember

2023-12-31

0001793895

CDTG:RetainedEarningsStatutoryReservesMember

2023-12-31

0001793895

CDTG:RetainedEarningsUnrestrictedMember

2023-12-31

0001793895

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2023-12-31

0001793895

us-gaap:NoncontrollingInterestMember

2023-12-31

0001793895

CDTG:CQBVIMember

2023-01-01

2023-12-31

0001793895

CDTG:CDTBVIMember

2023-01-01

2023-12-31

0001793895

CDTG:UltraHKMember

2023-01-01

2023-12-31

0001793895

CDTG:CDTHKMember

2023-01-01

2023-12-31

0001793895

CDTG:ShenzhenCDTMember

2023-01-01

2023-12-31

0001793895

CDTG:BJCDTMember

2023-01-01

2023-12-31

0001793895

CDTG:FJLSYMember

2023-01-01

2023-12-31

0001793895

CDTG:TJCDTMember

2023-01-01

2023-12-31

0001793895

CDTG:CDCDTMember

2023-01-01

2023-12-31

0001793895

CDTG:BJCXCDTMember

2023-01-01

2023-12-31

0001793895

CDTG:BDCDTMember

2023-01-01

2023-12-31

0001793895

CDTG:HSCDTMember

2023-01-01

2023-12-31

0001793895

CDTG:GXCDTMember

2023-01-01

2023-12-31

0001793895

CDTG:HZCDTMember

2023-01-01

2023-12-31

0001793895

CDTG:HHHTCDTMember

2023-01-01

2023-12-31

0001793895

CDTG:TYCDTMember

2023-01-01

2023-12-31

0001793895

CDTG:XMYDTMember

2023-01-01

2023-12-31

0001793895

us-gaap:IPOMember

us-gaap:SubsequentEventMember

2024-04-22

0001793895

us-gaap:IPOMember

us-gaap:SubsequentEventMember

2024-04-21

2024-04-22

0001793895

currency:CNY

2023-12-31

0001793895

currency:CNY

2022-12-31

0001793895

currency:HKD

2023-12-31

0001793895

currency:HKD

2022-12-31

0001793895

currency:CNY

2023-01-01

2023-12-31

0001793895

currency:CNY

2022-01-01

2022-12-31

0001793895

currency:CNY

2021-01-01

2021-12-31

0001793895

currency:HKD

2023-01-01

2023-12-31

0001793895

currency:HKD

2022-01-01

2022-12-31

0001793895

currency:HKD

2021-01-01

2021-12-31

0001793895

CDTG:SewageTreatmentServicesMember

2023-12-31

0001793895

CDTG:SewageTreatmentServices1Member

2023-12-31

0001793895

2022-01-02

0001793895

us-gaap:BuildingMember

2023-12-31

0001793895

us-gaap:EquipmentMember

srt:MinimumMember

2023-12-31

0001793895

us-gaap:EquipmentMember

srt:MaximumMember

2023-12-31

0001793895

us-gaap:FurnitureAndFixturesMember

srt:MinimumMember

2023-12-31

0001793895

us-gaap:FurnitureAndFixturesMember

srt:MaximumMember

2023-12-31

0001793895

us-gaap:AutomobilesMember

srt:MinimumMember

2023-12-31

0001793895

us-gaap:AutomobilesMember

srt:MaximumMember

2023-12-31

0001793895

us-gaap:BuildingMember

2022-12-31

0001793895

us-gaap:EquipmentMember

2023-12-31

0001793895

us-gaap:EquipmentMember

2022-12-31

0001793895

us-gaap:FurnitureAndFixturesMember

2023-12-31

0001793895

us-gaap:FurnitureAndFixturesMember

2022-12-31

0001793895

us-gaap:AutomobilesMember

2023-12-31

0001793895

us-gaap:AutomobilesMember

2022-12-31

0001793895

CDTG:FujianMingzhengConstructionDevelopmentLtdMember

2023-01-01

2023-12-31

0001793895

CDTG:FujianMingzhengConstructionDevelopmentLtdMember

2023-12-31

0001793895

CDTG:FujianMingzhengConstructionDevelopmentLtdMember

2022-12-31

0001793895

CDTG:JinhuoChenMember

2023-01-01

2023-12-31

0001793895

CDTG:JinhuoChenMember

2023-12-31

0001793895

CDTG:JinhuoChenMember

2022-12-31

0001793895

CDTG:ShenzhenLedoufuInformationTechnologyLtdMember

2023-01-01

2023-12-31

0001793895

CDTG:ShenzhenLedoufuInformationTechnologyLtdMember

2023-12-31

0001793895

CDTG:ShenzhenLedoufuInformationTechnologyLtdMember

2022-12-31

0001793895

CDTG:FujianTantanTechnologyCoLtdMember

2023-01-01

2023-12-31

0001793895

CDTG:FujianTantanTechnologyCoLtdMember

2023-12-31

0001793895

CDTG:FujianTantanTechnologyCoLtdMember

2022-12-31

0001793895

CDTG:FuzhouJinhuiEnvironmentalServiceCoLtdMember

2023-01-01

2023-12-31

0001793895

CDTG:FuzhouJinhuiEnvironmentalServiceCoLtdMember

2023-12-31

0001793895

CDTG:FuzhouJinhuiEnvironmentalServiceCoLtdMember

2022-12-31

0001793895

CDTG:WanqiangLinMember

2023-01-01

2023-12-31

0001793895

CDTG:WanqiangLinMember

2023-12-31

0001793895

CDTG:WanqiangLinMember

2022-12-31

0001793895

CDTG:BeijingMinhongyunEnergySupplyCoLtdMember

2023-01-01

2023-12-31

0001793895

CDTG:BeijingMinhongyunEnergySupplyCoLtdMember

2023-12-31

0001793895

CDTG:BeijingMinhongyunEnergySupplyCoLtdMember

2022-12-31

0001793895

CDTG:ShenzhenLiYaxinIndustrialCoLtdMember

2023-01-01

2023-12-31

0001793895

CDTG:ShenzhenLiYaxinIndustrialCoLtdMember

2023-12-31

0001793895

CDTG:ShenzhenLiYaxinIndustrialCoLtdMember

2022-12-31

0001793895

CDTG:YunwuLiMember

2023-01-01

2023-12-31

0001793895

CDTG:YunwuLiMember

2023-12-31

0001793895

CDTG:YunwuLiMember

2022-12-31

0001793895

CDTG:JianzhongZhaoMember

2023-01-01

2023-12-31

0001793895

CDTG:JianzhongZhaoMember

2023-12-31

0001793895

CDTG:JianzhongZhaoMember

2022-12-31

0001793895

CDTG:JianshanMaMember

2023-01-01

2023-12-31

0001793895

CDTG:JianshanMaMember

2023-12-31

0001793895

CDTG:JianshanMaMember

2022-12-31

0001793895

CDTG:YanWangMember

2023-01-01

2023-12-31

0001793895

CDTG:YanWangMember

2023-12-31

0001793895

CDTG:YanWangMember

2022-12-31

0001793895

CDTG:ZhaozhaoXuMember

2023-01-01

2023-12-31

0001793895

CDTG:ZhaozhaoXuMember

2023-12-31

0001793895

CDTG:ZhaozhaoXuMember

2022-12-31

0001793895

CDTG:YaoyuZhouMember

2023-01-01

2023-12-31

0001793895

CDTG:YaoyuZhouMember

2023-12-31

0001793895

CDTG:YaoyuZhouMember

2022-12-31

0001793895

CDTG:GuangxiJingxingmingEletricalLtdMember

2023-01-01

2023-12-31

0001793895

CDTG:GuangxiJingxingmingEletricalLtdMember

2023-12-31

0001793895

CDTG:GuangxiJingxingmingEletricalLtdMember

2022-12-31

0001793895

CDTG:XingshengPanMember

2023-01-01

2023-12-31

0001793895

CDTG:XingshengPanMember

2023-12-31

0001793895

CDTG:XingshengPanMember

2022-12-31

0001793895

CDTG:YunfangLiMember

2023-01-01

2023-12-31

0001793895

CDTG:YunfangLiMember

2023-12-31

0001793895

CDTG:YunfangLiMember

2022-12-31

0001793895

CDTG:GuangqingShiMember

2023-01-01

2023-12-31

0001793895

CDTG:GuangqingShiMember

2023-12-31

0001793895

CDTG:GuangqingShiMember

2022-12-31

0001793895

CDTG:ZhaozhaoXuOneMember

2023-01-01

2023-12-31

0001793895

CDTG:ZhaozhaoXuOneMember

2023-12-31

0001793895

CDTG:ZhaozhaoXuOneMember

2022-12-31

0001793895

CDTG:ChinaConstructionBankMember

2023-01-01

2023-12-31

0001793895

CDTG:ChinaConstructionBankMember

2022-12-31

0001793895

CDTG:ChinaConstructionBankOneMember

2023-01-01

2023-12-31

0001793895

CDTG:ChinaConstructionBankOneMember

2022-12-31

0001793895

CDTG:ChinaBankofCommunicationMember

2023-01-01

2023-12-31

0001793895

CDTG:ChinaBankofCommunicationMember

srt:MaximumMember

2023-01-01

2023-12-31

0001793895

CDTG:ChinaBankofCommunicationMember

srt:MinimumMember

2023-01-01

2023-12-31

0001793895

CDTG:ChinaBankofCommunicationMember

2023-12-31

0001793895

CDTG:ChinaBankofCommunicationMember

2022-12-31

0001793895

CDTG:ChinaBankofCommunicationOneMember

2023-01-01

2023-12-31

0001793895

CDTG:ChinaBankofCommunicationOneMember

2023-12-31

0001793895

CDTG:IndustrialAndCommercialBankOfChinaMember

2023-01-01

2023-12-31

0001793895

CDTG:IndustrialAndCommercialBankOfChinaMember

2022-12-31

0001793895

CDTG:WeizhongBankMember

2023-01-01

2023-12-31

0001793895

CDTG:WeizhongBankMember

2022-12-31

0001793895

CDTG:WeizhongBankOneMember

2023-01-01

2023-12-31

0001793895

CDTG:WeizhongBankOneMember

2022-12-31

0001793895

CDTG:ChinaResourceBankMember

2023-01-01

2023-12-31

0001793895

CDTG:ChinaResourceBankMember

2023-12-31

0001793895

CDTG:PostalSavingBankOfChinaMember

2023-01-01

2023-12-31

0001793895

CDTG:PostalSavingBankOfChinaMember

2023-12-31

0001793895

CDTG:BankOfChinaMember

2023-01-01

2023-12-31

0001793895

CDTG:BankOfChinaMember

2023-12-31

0001793895

CDTG:ChinaConstructionBankTwoMember

2023-01-01

2023-12-31

0001793895

CDTG:ChinaConstructionBankTwoMember

2023-12-31

0001793895

CDTG:WeizhongBankTwoMember

2023-01-01

2023-12-31

0001793895

CDTG:WeizhongBankTwoMember

srt:MaximumMember

2023-01-01

2023-12-31

0001793895

CDTG:WeizhongBankTwoMember

srt:MinimumMember

2023-01-01

2023-12-31

0001793895

CDTG:WeizhongBankTwoMember

2023-12-31

0001793895

CDTG:WeizhongBankMember

srt:MaximumMember

2023-01-01

2023-12-31

0001793895

CDTG:WeizhongBankMember

srt:MinimumMember

2023-01-01

2023-12-31

0001793895

CDTG:WeizhongBankMember

2023-12-31

0001793895

CDTG:DeyunZhouMember

2023-01-01

2023-12-31

0001793895

CDTG:DeyunZhouMember

2022-12-31

0001793895

CDTG:LingyuYeMember

2023-01-01

2023-12-31

0001793895

CDTG:LingyuYeMember

2023-12-31

0001793895

CDTG:LingyuYeMember

2022-12-31

0001793895

CDTG:RunzeLiMember

2023-01-01

2023-12-31

0001793895

CDTG:RunzeLiMember

2023-12-31

0001793895

CDTG:RunzeLiMember

2022-12-31

0001793895

CDTG:ShanghaiXinjingConstructionLaborServiceCenterMember

2023-01-01

2023-12-31

0001793895

CDTG:ShanghaiXinjingConstructionLaborServiceCenterMember

2023-12-31

0001793895

CDTG:ShanghaiXinjingConstructionLaborServiceCenterMember

2022-12-31

0001793895

CDTG:XiamenHaoshengInvestingCoLtdMember

2023-01-01

2023-12-31

0001793895

CDTG:XiamenHaoshengInvestingCoLtdMember

2023-12-31

0001793895

CDTG:XiamenHaoshengInvestingCoLtdMember

2022-12-31

0001793895

CDTG:PRCSubsidiariesMember

2023-12-31

0001793895

CDTG:PRCSubsidiariesMember

2022-12-31

0001793895

CDTG:HongKongSubsidiariesMember

2023-12-31

0001793895

CDTG:HongKongSubsidiariesMember

2022-12-31

0001793895

CDTG:PRCSubsidiariesOtherThanShenzhenCDTMember

2023-12-31

0001793895

CDTG:PRCSubsidiariesOtherThanShenzhenCDTMember

2022-12-31

0001793895

us-gaap:CreditRiskMember

2023-12-31

0001793895

us-gaap:CreditRiskMember

2022-12-31

0001793895

us-gaap:CreditRiskMember

country:CN

2023-12-31

0001793895

currency:CNY

us-gaap:CreditRiskMember

2023-12-31

0001793895

us-gaap:CreditRiskMember

country:HK

2023-12-31

0001793895

us-gaap:CreditRiskMember

country:HK

2022-12-31

0001793895

CDTG:Customer1Member

us-gaap:SalesRevenueNetMember

us-gaap:CustomerConcentrationRiskMember

2023-01-01

2023-12-31

0001793895

CDTG:Customer2Member

us-gaap:SalesRevenueNetMember

us-gaap:CustomerConcentrationRiskMember

2023-01-01

2023-12-31

0001793895

CDTG:Customer1Member

us-gaap:SalesRevenueNetMember

us-gaap:CustomerConcentrationRiskMember

2022-01-01

2022-12-31

0001793895

CDTG:Customer2Member

us-gaap:SalesRevenueNetMember

us-gaap:CustomerConcentrationRiskMember

2022-01-01

2022-12-31

0001793895

CDTG:Customer3Member

us-gaap:SalesRevenueNetMember

us-gaap:CustomerConcentrationRiskMember

2022-01-01

2022-12-31

0001793895

CDTG:Customer1Member

us-gaap:SalesRevenueNetMember

us-gaap:CustomerConcentrationRiskMember

2021-01-01

2021-12-31

0001793895

CDTG:Customer2Member

us-gaap:SalesRevenueNetMember

us-gaap:CustomerConcentrationRiskMember

2021-01-01

2021-12-31

0001793895

CDTG:Customer1Member

us-gaap:AccountsReceivableMember

us-gaap:CustomerConcentrationRiskMember

2023-01-01

2023-12-31

0001793895

CDTG:Customer2Member

us-gaap:AccountsReceivableMember

us-gaap:CustomerConcentrationRiskMember

2023-01-01

2023-12-31

0001793895

CDTG:Customer1Member

us-gaap:AccountsReceivableMember

us-gaap:CustomerConcentrationRiskMember

2022-01-01

2022-12-31

0001793895

CDTG:Customer2Member

us-gaap:AccountsReceivableMember

us-gaap:CustomerConcentrationRiskMember

2022-01-01

2022-12-31

0001793895

CDTG:Customer3Member

us-gaap:AccountsReceivableMember

us-gaap:CustomerConcentrationRiskMember

2022-01-01

2022-12-31

0001793895

CDTG:Customer4Member

us-gaap:AccountsReceivableMember

us-gaap:CustomerConcentrationRiskMember

2022-01-01

2022-12-31

0001793895

CDTG:Vendor1Member

CDTG:PurchaseMember

us-gaap:CustomerConcentrationRiskMember

2023-01-01

2023-12-31

0001793895

CDTG:Vendor1Member

CDTG:PurchaseMember

us-gaap:CustomerConcentrationRiskMember

2022-01-01

2022-12-31

0001793895

CDTG:Vendor2Member

CDTG:PurchaseMember

us-gaap:CustomerConcentrationRiskMember

2022-01-01

2022-12-31

0001793895

CDTG:Vendor1Member

CDTG:PurchaseMember

us-gaap:CustomerConcentrationRiskMember

2021-01-01

2021-12-31

0001793895

CDTG:Vendor2Member

CDTG:PurchaseMember

us-gaap:CustomerConcentrationRiskMember

2021-01-01

2021-12-31

0001793895

CDTG:Vendor3Member

CDTG:PurchaseMember

us-gaap:CustomerConcentrationRiskMember

2021-01-01

2021-12-31

0001793895

CDTG:Vendor4Member

CDTG:PurchaseMember

us-gaap:CustomerConcentrationRiskMember

2021-01-01

2021-12-31

0001793895

CDTG:VendorMember

us-gaap:AccountsPayableMember

us-gaap:CustomerConcentrationRiskMember

2023-01-01

2023-12-31

0001793895

CDTG:OneVendorMember

us-gaap:AccountsPayableMember

us-gaap:CustomerConcentrationRiskMember

2022-01-01

2022-12-31

0001793895

CDTG:TwoVendorMember

us-gaap:AccountsPayableMember

us-gaap:CustomerConcentrationRiskMember

2022-01-01

2022-12-31

0001793895

2019-10-15

0001793895

2020-12-30

0001793895

srt:ManagementMember

2023-12-31

0001793895

us-gaap:SubsequentEventMember

2024-01-10

0001793895

us-gaap:SubsequentEventMember

2024-01-09

2024-01-10

0001793895

us-gaap:SubsequentEventMember

2024-04-21

2024-04-22

0001793895

srt:ParentCompanyMember

2023-12-31

0001793895

srt:ParentCompanyMember

2022-12-31

0001793895

srt:ParentCompanyMember

2023-01-01

2023-12-31

0001793895

srt:ParentCompanyMember

2022-01-01

2022-12-31

0001793895

srt:ParentCompanyMember

2021-01-01

2021-12-31

0001793895

srt:ParentCompanyMember

2021-12-31

0001793895

srt:ParentCompanyMember

2020-12-31

iso4217:USD

xbrli:shares

iso4217:USD

xbrli:shares

xbrli:pure

iso4217:HKD

UNITED

STATES

SECURITIES

AND EXCHANGE COMMISSION

Washington,

D.C. 20549

FORM

20-F

(Mark One)

| ☐ |

|

REGISTRATION

STATEMENT PURSUANT TO SECTION 12(b) OR 12(g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| ☒ |

|

ANNUAL REPORT PURSUANT

TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2023

OR

| ☐ |

|

TRANSITION REPORT PURSUANT

TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

OR

| ☐ |

|

SHELL COMPANY REPORT PURSUANT

TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Date of event requiring this shell company report _____________

Commission file number: 001-42007

| CDT Environmental Technology Investment Holdings Limited |

| (Exact Name of Registrant as Specified in Its Charter) |

| |

| N/A |

| (Translation of Registrant’s Name Into English) |

| |

| Cayman Islands |

| (Jurisdiction of Incorporation or Organization) |

| |

|

C1, 4th Floor, Building 1, Financial Base, No. 8 Kefa Road

Nanshan District, Shenzhen, China 518057 |

| (Address of Principal Executive Offices) |

| |

|

Yunwu Li

Chief Executive Officer

C1, 4th Floor, Building 1, Financial Base, No. 8 Kefa Road

Nanshan District, Shenzhen, China 518057

E-mail: liyunwu@cdthb.cn

Telephone: + 86-0755-86667996 |

| (Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person) |

Securities registered or to be registered pursuant

to Section 12(b) of the Act:

| Title of each class |

|

Trading symbol(s) |

|

Name of each exchange on which registered |

| Ordinary Shares, par value $0.0025 per share |

|

CDTG |

|

Nasdaq Capital Market |

Securities registered or to be registered pursuant to Section 12(g) of

the Act:

Securities for which there is a reporting obligation pursuant to Section

15(d) of the Act:

Indicate the number of outstanding shares of each

of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report:

As of December 31, 2023, there were 9,200,000 ordinary

shares issued and outstanding, par value $0.0025 per ordinary share.

Indicate by check mark if the registrant is a well-known

seasoned issuer, as defined in Rule 405 of the Securities Act.

☐

Yes ☒ No

If this report is an annual or transition report,

indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act

of 1934.

☐

Yes ☒ No

Note - Checking the box above will not relieve any

registrant required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 from their obligations under

those Sections.

Indicate by check mark whether the registrant (1)

has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months

(or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements

for the past 90 days.

☒

Yes ☐ No

Indicate by check mark whether the registrant has

submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of

this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

☒

Yes ☐ No

Indicate by check mark whether the registrant is a

large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See definition of “large

accelerated filer,” “accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ☐ |

|

Accelerated filer ☐ |

|

Non-accelerated filer ☒ |

|

Emerging growth company ☒ |

If an emerging growth company that prepares its financial

statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period

for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act.

† The term “new or revised financial

accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification

after April 5, 2012.

Indicate by check mark whether the registrant has

filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting

under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its

audit report. ☐

If securities are registered pursuant to Section 12(b)

of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of

an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error

corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s

executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark which basis of accounting the

registrant has used to prepare the financial statements included in this filing:

| U.S. GAAP ☒ |

|

International Financial Reporting Standards as issued

by the International Accounting Standards Board ☐ |

|

Other ☐ |

If “Other” has been checked in response

to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

☐

Item 17 ☐ Item 18

If this is an annual report, indicate by check mark

whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

☐

Yes ☒ No

(APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY

PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate by check mark whether the registrant has

filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to

the distribution of securities under a plan confirmed by a court.

☐

Yes ☐ No

TABLE OF CONTENTS

INTRODUCTION

Unless otherwise indicated

or the context otherwise requires, all references in this annual report to:

| ● | “CDT

Cayman,” the “Company,” “we,” “us” and “our”

refer to CDT Environmental Technology Investment Holdings Limited, a Cayman Islands holding

company, and its subsidiaries: CQ BVI, CDT BVI, Ultra HK, Shenzhen CDT and CDT HK. See “Item

4. Information on the Company—History and Development of the Company” for additional

details. |

| ● | “CQ

BVI” refers to Chao Qiang Holdings Limited, a holding company established under the

laws of the British Virgin Islands and a wholly-owned subsidiary of CDT Cayman. |

| ● | “CDT

BVI” refers to CDT Environmental Technology Group Limited, a holding company established

under the laws of the British Virgin Islands and a wholly-owned subsidiary of CDT Cayman. |

| ● | “Ultra

HK” refers to Ultra Leader Investments Limited, a holding company established under

the laws of Hong Kong and a wholly-owned subsidiary of CQ BVI. |

| ● | “Shenzhen

CDT” refers to Shenzhen CDT Environmental Technology Co., Ltd., a company established

under the laws of the PRC and a 15% subsidiary of Ultra HK and 85% subsidiary of CDT HK. |

| ● | “PRC”

or “China” refers to the People’s Republic of China, excluding, for the

purpose of this annual report, Taiwan. “RMB” or “Renminbi” refers

to the legal currency of China. “HKD” or “HK$” refers to the legal

currency of Hong Kong. “$” or “U.S. dollars” refers to the legal

currency of the United States. |

We have made rounding adjustments to some of the figures

included in this annual report. Accordingly, numerical figures shown as totals in some tables may not be an arithmetic aggregation of

the figures that preceded them.

Unless the context indicates otherwise, all information

in this annual report assumes no exercise by the underwriters of their over-allotment option and no exercise of the representative’s

warrants.

Our functional currency is RMB. Our consolidated financial

statements are presented in U.S. dollars. We use U.S. dollars as the reporting currency in our consolidated financial statements and in

this annual report. Assets and liabilities are translated into U.S. dollars at the unified exchange rates as quoted by the People’s

Bank of China as of the balance sheet dates, the statements of income are translated using the average rate of exchange in effect during

the reporting periods, and the equity accounts are translated at historical exchange rates. Translation adjustments resulting from this

process are included in accumulated other comprehensive income (loss). Transaction gains and losses that arise from exchange rate fluctuations

on transactions denominated in a currency other than the functional currency are included in the results of operations as incurred. Translation

adjustments included in accumulated other comprehensive income (loss) amounted to $2,009,421, $1,490,621 and $559,752 as of December 31,

2023, December 31, 2022 and December 31, 2021, respectively. The balance sheet amounts, with the exception of shareholders’ equity

at December 31, 2023 and 2022 were translated at 7.08 RMB and 6.96 RMB to $1.00, respectively, and at 7.81 HKD and 7.80 HKD to $1.00,

respectively. The shareholders’ equity accounts are stated at their historical exchange rates. The average translation rates applied

to the statements of income accounts for the years ended December 31, 2023, 2022 and 2021 were 7.05 RMB, 6.73 RMB and 6.45 RMB to $1.00,

respectively, and were 7.83 HKD, 7.83 HKD and 7.77 HKD to $1.00, respectively. Cash flows are also translated at average translation rates

for the periods, therefore, amounts reported on the statements of cash flows will not necessarily agree with changes in the corresponding

balances on the consolidated balance sheets.

With respect to amounts not recorded in our consolidated

financial statements included elsewhere in this annual report, unless otherwise stated, all translations from RMB to U.S. dollars were

made at RMB 7.0999 to $1.00, the noon buying rate on December 29, 2023, as set forth in the H.10 statistical release of the Board of Governors

of the Federal Reserve System. We make no representation that the RMB or U.S. dollar amounts referred to in this annual report could have

been or could be converted into U.S. dollars or RMB, as the case may be, at any particular rate or at all.

FORWARD-LOOKING STATEMENTS

This annual report on Form 20-F contains forward-looking

statements that involve substantial risks and uncertainties. In some cases, you can identify forward-looking statements by the words

“may,” “might,” “will,” “could,” “would,” “should,” “expect,”

“intend,” “plan,” “goal,” “objective,” “anticipate,” “believe,”

“estimate,” “predict,” “potential,” “continue” and “ongoing,” or the negative

of these terms, or other comparable terminology intended to identify statements about the future. These statements involve known and

unknown risks, uncertainties and other important factors that may cause our actual results, levels of activity, performance or achievements

to be materially different from the information expressed or implied by these forward-looking statements. The forward-looking statements

and opinions contained in this annual report are based upon information available to us as of the date of this annual report and, while

we believe such information forms a reasonable basis for such statements, such information may be limited or incomplete, and our statements

should not be read to indicate that we have conducted an exhaustive

inquiry into, or review of, all potentially available relevant information. Forward-looking statements include statements about:

| ● | timing

of the development of future business; |

| ● | capabilities

of our business operations; |

| ● | expected

future economic performance; |

| ● | the

impact of COVID-19 on the Company; |

| ● | competition

in our markets; |

| ● | continued

market acceptance of our products; |

| ● | exposure

to product liability and defect claims; |

| ● | protection

of our intellectual property rights; |

| ● | changes

in the laws that affect our operations; |

| ● | inflation

and fluctuations in foreign currency exchange rates; |

| ● | our

ability to obtain and maintain all necessary government certifications, approvals, and/or

licenses to conduct our business; |

| ● | continued

development of a public trading market for our securities; |

| ● | the

cost of complying with current and future governmental regulations and the impact of any

changes in the regulations on our operations; |

| ● | managing

our growth effectively; |

| ● | projections

of revenue, earnings, capital structure and other financial items; |

| ● | fluctuations

in operating results; |

| ● | dependence

on our senior management and key employees; and |

| ● | other

factors set forth under “Item 3. Key Information—D. Risk Factors.” |

You

should refer to the section titled “Item 3. Key Information—D. Risk Factors” for a discussion of important factors

that may cause our actual results to differ materially from those expressed or implied by our forward-looking statements. As a result

of these factors, we cannot assure you that the forward-looking statements in this annual report will prove to be accurate. Furthermore,

if our forward-looking statements prove to be inaccurate, the inaccuracy may be material. In light of the significant uncertainties in

these forward-looking statements, you should not regard these statements as a representation or warranty by us or any other person that

we will achieve our objectives and plans in any specified time frame, or at all. We undertake no obligation to publicly update any forward-looking

statements, whether as a result of new information, future events or otherwise, except as required by law.

You should read this annual report and the documents that we reference

in this annual report and have filed as exhibits to this annual completely and with the understanding that our actual future results

may be materially different from what we expect. We qualify all of our forward-looking statements by these cautionary statements.

PART I

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not applicable.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not applicable.

ITEM 3. KEY INFORMATION

A. [Reserved]

B. Capitalization and Indebtedness

Not applicable.

C. Reasons for the Offer and Use of Proceeds

Not applicable.

D. Risk Factors

Risks Related to Our Business

We have a limited operating

history. There is no assurance that our future operations will be profitable operations. If we cannot generate sufficient revenues to

operate profitably, we may suspend or cease operations.

Given our limited operating history,

there can be no assurance that we can build our business such that we can earn a significant profit or any profit at all. The future of

our business will depend upon our ability to obtain and retain customers and when needed, obtain sufficient financing and support from

creditors, while we strive to achieve and maintain profitable operations. The likelihood of success must be considered in light of the

problems, expenses, difficulties, complications and delays encountered in connection with the operations that we undertake. There is no

history upon which to base any assumption that our business will prove to be successful, and there is significant risk that we will not

be able to generate the sales volumes and revenues necessary to achieve profitable operations. To the extent that we cannot achieve our

plans and generate revenues which exceed expenses on a consistent basis, our business, results of operations, financial condition and

prospects will be materially adversely affected.

Our management team has limited

public company experience. We have not previously operated as a public company in the United States and several of our senior management

positions are currently held by employees who have been with us for a short period of time. Our entire management team, as well as other

Company personnel, will need to devote substantial time to compliance, and may not effectively or efficiently manage our transition into

a public company. If we are unable to effectively comply with the regulations applicable to public companies or if we are unable to produce

accurate and timely financial statements, which may result in material misstatements in our financial statements or possible restatement

of financial results, our stock price may be materially adversely affected, and we may be unable to maintain compliance with the listing

requirements of Nasdaq. Any such failures could also result in litigation or regulatory actions by the SEC or other regulatory authorities,

loss of investor confidence, delisting of our securities, harm to our reputation and diversion of financial and management resources from

the operation of our business, any of which could materially adversely affect our business, financial condition, results of operations

and growth prospects. Additionally, the failure of a key employee to perform in his or her current position could result in our inability

to continue to grow our business or to implement our business strategy.

We face risks related to

natural disasters, health epidemics and other outbreaks, particularly the coronavirus, which could significantly disrupt our operations.

In recent years, there have been

outbreaks of epidemics in various countries, including China and the United States. In December 2019, a novel strain of coronavirus, or

COVID-19 or the coronavirus, surfaced and it has spread rapidly to many parts of China and

other parts of the world, including the United States. COVID-19 has resulted in quarantines, travel restrictions, and the

temporary closure of stores and business facilities throughout China and several other parts of the world, including the United States.

In March 2020, the World Health Organization declared COVID-19 a pandemic. All of our revenue is concentrated in China through our subsidiaries.

Consequently, our revenues were impacted by COVID-19 and were significantly lower in 2020 as compared to the same period of 2019. We had

to comply with the temporary closure of facilities, or the ‘shelter in place’ order, in China in the first quarter of 2020.

As a result, we closed our facilities in January 2020 and re-opened them in late March 2020. The COVID-19 outbreak materially adversely

affected our business operations, financial condition and operating results for 2020 and 2021, including but not limited to material negative

impact on our total revenues, slower collection of accounts receivable and additional allowances for doubtful accounts and could continue

to adversely affect our business operations, financial condition and operating results. Despite the ongoing COVID-19 pandemic, we resumed

relatively normal business operations after March 2020. However, the resurgence of COVID-19, particularly the Omicron variant, has resulted

in government restrictions in quarantines, travel and the temporary closures of stores and business facilities in parts of China and the

world during the first few months of 2022. As of date of this annual report, the PRC government has lifted the above mentioned restrictions.

In December 2022, the Chinese government unveiled a series of new COVID-related policies to loosen its zero-COVID policy, and uplifted

the existing prevention and control measures that were in place for the COVID-19 pandemic. On December 26, 2022, China’s National

Health Commission announced that the COVID-19 infections will not be subject to the prevention and control measures of a Class A infectious

disease, which means that COVID-19 infections will no longer be included in the administration of quarantinable infectious diseases. Starting

from January 8, 2023, among other changes, China no longer conducts nucleic acid tests or centralized quarantine for all inbound travelers,

and measures to control the number of international passenger flights have been lifted. We expect our business operations, financial condition

and operating results to continue to recover from the negative impact of the COVID-19 pandemic. However, due to the significant uncertainties

surrounding the COVID-19 pandemic, the extent of the business disruption and the related financial impact cannot be reasonably estimated

at this time.

In general, our business could

be materially and adversely affected by natural disasters, health epidemics or other public safety concerns affecting China and the world,

particularly the coronavirus. Natural disasters may give rise to server interruptions, breakdowns, system failures, technology platform

failures or internet failures, which could cause the loss or corruption of data or malfunctions of software or hardware as well as adversely

affect our ability to operate our business and provide services and solutions. In recent years, there have been outbreaks of epidemics

in China and globally, such as the coronavirus, H1N1 flu, and avian flu. Our business operations could be disrupted by any of these

epidemics, in addition to any other epidemics. In addition, our results of operations could be adversely affected to the extent that any

health epidemic harms the Chinese economy in general. A prolonged outbreak of any of these illnesses or other adverse public health developments

in China or elsewhere in the world could have a material adverse effect on our business operations. Such outbreaks could significantly

impact our industry, which could severely disrupt our operations and adversely affect our business, financial condition and results of

operations. Our headquarters and factory are located in Shenzhen and Nanping, China. Consequently, if any natural disasters, health epidemics

or other public safety concerns were to affect Shenzhen or Nanping, our business may experience material disruptions, which may materially

and adversely affect our business, financial condition and results of operations.

We operate in highly competitive

markets and the size and resources of many of our competitors may allow them to compete more effectively than we can, preventing us from

achieving profitability.

The markets we compete in are highly

competitive. Competition may result in pricing pressures, reduced profit margins or lost market share, or a failure to grow our market

share, any of which could substantially harm our business and results of operations. We compete for customers primarily on the basis of

our brand name, price and the range of products and services that we offer. Across our business, we face competitors who are constantly

seeking ideas which will appeal to customers and introducing new products that compete with our products. Many of our competitors have

significant competitive advantages, including longer operating histories, larger and broader customer bases, less-costly production, more

established relationships with a broader set of suppliers and customers, greater brand recognition and greater financial, research and

development, marketing, distribution and other resources than we do. We cannot assure that we will be able to successfully compete against

new or existing competitors. If we fail to maintain our reputation and competitiveness, customers demand for our products and projects

could decline.

In addition to existing competitors,

new participants with a popular product idea could gain access to customers and become a significant source of competition in a short

period of time. These existing and new competitors may be able to respond more rapidly than us to changes in customer preferences. Our

competitors’ products may achieve greater market acceptance than our products and potentially reduce demand for our products, lower

our revenues and lower our profitability.

Any decline in the availability

or increase in the cost of raw materials could materially impact our earnings.

Our products and project installation

operations depend heavily on the ready availability of various raw materials. The availability of raw materials may decline, and their

prices may fluctuate greatly. If our suppliers are unable or unwilling to provide us with raw materials on terms favorable to us, we may

be unable to produce certain products. The inability to produce certain products or installation projects for customers could result in

a decrease in profit and damage to our reputation. In the event our raw material costs increase, we may not be able to pass these higher

costs on to our customers in full or at all.

Our revenue will decrease

if the industries in which we and our customers operate experience a protracted slowdown.

We are subject to general changes

in economic conditions impacting the economy. If the industries in which we and our customers operate do not grow or if there is a contraction

in these industries, including if government spending is affected, demand for our business will decrease. Demand for our business is typically

affected by a number of overarching economic factors, including interest rates, environmental laws and regulations, government spending,

including the availability and magnitude of private and governmental investment in infrastructure projects and the health of the overall

economy. If there is a decline in economic activity in China and the markets in which we operate or a protracted slowdown in industries

upon which we rely for our sales, demand for our projects, products and our revenue will likewise decrease which would have a materially

adverse effect on our business.

Our business depends in large

part on the success of our vendors and outsourcers, and our brand and reputation may be harmed by actions taken by third parties that

are outside of our control. In addition, any material failure, inadequacy, or interruption resulting from such vendors or outsourcers

could harm our ability to effectively operate our business.

We rely on vendor and outsourcing

relationships with third parties for services and systems including manufacturing and logistics. We outsource manufacturing of our integrated

rural sewage treatment system primarily to three vendors in the Jiangsu and Fujian provinces. Any shortcoming of a vendor or an outsourcer,

particularly an issue affecting the quality of these services or systems, may be attributed by customers to us, thus damaging our reputation

and brand value, and potentially affecting our results of operations. In addition, problems with transitioning these services and systems

to or operating failures with these vendors and outsourcers could cause delays in product sales, and reduce efficiency of our operations,

and significant capital investments could be required to remediate the problem.

We primarily rely on a limited

number of vendors, and the loss of any such vendor could harm our business.

For the year ended December 31,

2023, one vendor accounted for 27.3%, respectively, of our total purchases, and no vendors accounted for more than 10.0% of our accounts

payable. For the year ended December 31, 2022, two vendors accounted for 19.7% and 10.0%, respectively, of our total purchases, and two

vendors accounted for 12.6% and 10.9%, respectively, of our accounts payable. For the year ended December 31, 2021, four vendors accounted

for 40.7%, 23.6%, 11.7% and 10.0%, respectively, of our total purchases, and five vendors accounted for 15.3%, 14.5%, 13.2%, 11.3% and

10.3%, respectively, of our accounts payable. We generally do not have long term agreements or arrangements with our vendors. Our decision

in choosing vendors is typically based on the compressive consideration of multiple factors including, among others, pricing, location,

delivery terms and line of credit. Our vendors generally provide us with standard parts used in sewage treatment and integrated sewage

treatment equipment. Any difficulty in replacing such vendors could negatively affect our performance. If we are prevented or delayed

in obtaining products, or components for products, due to political, civil, labor or other factors beyond our control that affect our

vendors, including natural disasters or pandemics, our operations may be substantially disrupted, potentially for a significant period

of time. Such delays could significantly reduce our revenues and profitability and harm our business while alternative sources of supply

are secured.

Our dependence on a limited

number of customers could adversely affect our business and results of operations.

One or a few customers have in

the past, and may in the future, represent a substantial portion of our total revenues in any one year or over a period of several years.

For example, for the year ended December 31, 2023, two customers accounted for 23.4% and 10.2%, respectively, of our total revenues ,

and two customers accounted for 13.0%, 12.3%, respectively, of our accounts receivable. For the year ended December 31, 2022, three customers

accounted for 48.5%, 15.2%, and 14.6%, respectively, of our total revenues, and four customers accounted for 18.2%, 15.1%, 12.9% and 11.2%,

respectively, of our accounts receivable. For the year ended December 31, 2021, two customers accounted for 48.9% and 20.8%, respectively,

of our total revenues, and four customers accounted for 16.1%, 13.1%, 11.6% and 10.2%, respectively, of our accounts receivable.

The customer that accounted for

23.4% of our total revenues for the year ended December 31, 2023 was attributable to the Lianjiang Project. We expect the percentage of

revenue attributable to the Lianjiang Project will decrease once such project is completed. We secured the agreement to undertake

the Lianjiang Project in January 2023. The total contracted amount of this project is tentatively fixed at RMB 140 million (approximately

$19.1 million). We commenced early-stage construction and material acquisition in January 2023 and expect to complete the entire Lianjiang

Project by July 2024. Key terms of our agreement for the Lianjiang Project include the project name and location, duration, price

and payment terms, quality, safety and construction requirements, and breach of contract terms.

The customer that accounted for

less than 10% of our total revenues for the year ended December 31, 2023 and 15.2% of our total revenues for the year ended December

31, 2022 was attributable to the Wuyishan Project. We expect the percentage of revenue attributable to the Wuyishan Project will decrease

once such project is completed. We secured the agreement to undertake the Wuyishan Project in September 2022. The total contracted amount

of this project is tentatively fixed at RMB 37 million (approximately $5.1 million). We commenced early-stage construction and material

acquisition in September 2022 and completed the entire Wuyishan Project in August 2023 according to verbal discussions with such customer.

Key terms of our agreement for the Wuyishan Project include the project name and location, duration, price and payment terms, quality,

safety and construction requirements, and breach of contract terms. Additionally, we entered into a separate agreement with this customer

for extended scope of work in July 2023, which we refer to as the Wuyishan Project – Phase 2. The total contracted amount of Wuyishan

Project – Phase 2 is tentatively fixed at RMB 30 million (approximately $4.1 million). We expect to complete the entire Wuyishan

Project – Phase 2 by May 2024 . Key terms of our agreement for the Wuyishan Project – Phase 2 project include the project

name and location, duration, price and payment terms, quality, safety and construction requirements, and breach of contract terms.

The customer that accounted for

14.6% of our total revenues for the year ended December 31, 2022 and 48.9% of our total revenues for the year ended December 31, 2021

was attributable to the Zhongshan Project. The Zhongshan Project accounted for less than 10% of our total revenues for the year ended

December 31, 2023. We expect the percentage of revenue attributable to the Zhongshan Project will decrease once such project is completed.

We secured the agreement to undertake the Zhongshan Project in April 2021. The total contracted amount of this project is tentatively

fixed at RMB 180 million (approximately $26.9 million), and is subject to the actual construction quantity settlement, per the agreement.

We commenced early-stage construction and material acquisition in June 2021 and expect to complete the entire Zhongshan Project by the

end of August 2024 according to verbal discussions with such customer. Key terms of our agreement for the Zhongshan Project include

the project name and location, duration, price and payment terms, quality, safety and construction requirements, and breach of contract

terms. Pursuant to the agreement for the Zhongshan Project, liquidated damages equal to: (i) 0.1% of the total contract amount each day

must be paid by Shenzhen CDT if it fails to complete a task within the time specified in the contract, and (ii) 10% of the total contract

amount may be required to be paid by Shenzhen CDT if a task is not completed within 45 days of delay and if the customer chooses to terminate

the contract and request Shenzhen CDT to pay such liquidated damages. Therefore, if such circumstances occur, Shenzhen CDT may be required

to pay such liquidated damages, which could result in significant cash expenditures.

The customer that accounted for

10.2% of our total revenues for the year ended December 31, 2023, attributable to four different stages of such project, 48.5% of our

total revenues for the year ended December 31, 2022, attributable to two different stages of such project, and 20.8% of our total revenues

for the year ended December 31, 2021 was attributable to the Guankou Project. We do not have long term agreements or arrangements with

such customer. We expect the percentage of revenue attributable to the Guankou Project will decrease as such project has been completed.

We secured the agreement to undertake the Guankou Project in September 2021. The total contracted amount of this project is tentatively

fixed at RMB 95 million (approximately $14.2 million),

and is subject to the actual construction quantity settlement, per the agreement.

We commenced early-stage construction and material acquisition in October 2021 and completed the entire Guankou Project in March 2023

according to verbal discussions with such customer. Key terms of our agreement for the Guankou Project include the project name and location,

duration, price and payment terms, quality, safety and construction requirements, and breach of contract terms. Therefore, the loss of

business from any one of such customers could have a material adverse effect on our business or results of operations. In addition, a

default or delay in payment on a significant scale by a customer could materially adversely affect our business, results of operations,

cash flows and financial condition.

We face substantial inventory

risk, which if such risk is not addressed could have a material adverse effect on our business.

We must order materials for our

products and projects and build inventory in advance of production. We typically acquire materials through a combination of purchase orders,

supplier contracts and open orders, in each case based on projected demand.

As our markets are competitive

and subject to technology and price changes, there is a risk that we will forecast incorrectly and order or produce incorrect amounts

of products or not fully utilize purchase commitments. If we were unsuccessful in accurately quantifying appropriate levels of inventory,

our business, financial condition and results of operation may be materially and adversely affected.

Any disruption in the supply

chain of raw materials and our products could adversely impact our ability to produce and deliver products which could have a material

adverse effect on our business.

In order to optimize our product

manufacturing, we must manage our supply chain for raw materials and delivery of our products. Supply chain fragmentation and local protectionism

within China further complicates supply chain disruption risks. Local administrative bodies and physical infrastructure built to protect

local interests may pose transportation challenges for raw material transportation as well as product delivery. In addition, profitability

and volume could be negatively impacted by limitations inherent within the supply chain, including competitive, governmental, legal, natural

disasters, and other events that could impact both supply and price. Any of these occurrences could cause significant disruptions to our

supply chain, manufacturing capability and distribution system that could adversely impact our ability to produce and deliver products.

If we were unsuccessful in maintaining efficient operation of our supply chain, our business, financial condition and results of operation

may be materially and adversely affected.

Our return on investment

in client projects may be different from our projections.

Our return on investment in client

projects typically takes some time to materialize. At the initial stages of project investment and construction, the depreciation of fixed

assets may negatively affect our operating results. In addition, the projects may be subject to changes in market conditions during the

installation and implementation phases. Changes in industry policy, the progress of the projects, project management, raw materials supply,

market conditions and other variables may affect the profitability and the time in which we profit on projects, which may be different

from our initial forecast, thus affecting the actual return on investment of the projects.

Issues or defects with products

may lead to product liability, personal injury or property damage claims, recalls, withdrawals, replacements of products, or regulatory

actions by governmental authorities that could divert resources, affect business operations, decrease sales, increase costs, and put us

at a competitive disadvantage, any of which could have a significant adverse effect on our financial condition.

We may experience issues or defects

with products that may lead to product liability, personal injury or property damage claims, recalls, withdrawals, replacements of products,

or regulatory actions by governmental authorities. Any of these activities could result in increased governmental scrutiny, harm to our

reputation, reduced demand by customers for our products, decreased willingness by our service providers to provide support for those

products, absence or increased cost of insurance if insurance is available, or additional safety and testing requirements. Such results

could divert development and management resources, adversely affect our business operations, decrease sales, increase legal fees and other

costs, and put us at a competitive disadvantage compared to other companies not affected by similar issues with products, any of which

could have a significant adverse effect on our financial condition and results of operations.

Our future growth depends

in part on new products and new technology innovation, and failure to invent and innovate could adversely impact our business prospects.

Our future growth depends in part

on maintaining our current products in new and existing markets, as well as our ability to develop new products and technologies to serve

such markets. To the extent that competitors develop competitive products and technologies, or new products or technologies that achieve

higher customer satisfaction, our business prospects could be adversely impacted. In addition, regulatory approvals for new products or

technologies may be required, these approvals may not be obtained in a timely or cost effective manner, adversely impacting our business

prospects.

Changes in demand for our

products and business relationships with key customers and vendors may negatively affect operating results.

To achieve our objectives, we must

develop and sell products that are subject to the demands of our customers. This is dependent on several factors, including managing and

maintaining relationships with key customers, responding to the rapid pace of technological change and obsolescence, which may require

increased investment by us or result in greater pressure to commercialize developments rapidly or at prices that may not fully recover

the associated investment, and the effect on demand resulting from customers’ research and development, capital expenditure plans

and capacity utilization. If we are unable to keep up with our customers’ demands, our sales, earnings and operating results may

be negatively affected.

We may be unable to deliver

our backlog on time, which could affect future sales and profitability and our relationships with customers.

Our ability to meet customer delivery

schedules for backlog is dependent on a number of factors including sufficient manufacturing capacity, adequate supply channel access

to raw materials and other inventory required for production, an adequately trained and capable workforce, engineering expertise for certain

projects and appropriate planning and scheduling of manufacturing resources. Failure to deliver in accordance with customer expectations

could subject us to contract cancellations and financial penalties, and may result in damage to existing customer relationships and could

have a material adverse effect on our business, financial condition and results of operations.

Our future success depends

in part on our ability to retain key executives and to attract, retain and motivate qualified personnel.

We are highly dependent on the

principal members of our executive team listed in “Item 6. Directors, Senior Management and Employees” located elsewhere in

this annual report, the loss of whose services may adversely impact the achievement of our objectives. Recruiting and retaining other

qualified employees for our business, including technical personnel, will also be critical to our success. Competition for skilled personnel

is intense and the turnover rate can be high. We may not be able to attract and retain personnel on acceptable terms given the competition

among numerous companies for individuals with similar skill sets. The inability to recruit or loss of the services of any executive or

key employee could adversely affect our business.

We will need to expand our

organization, and we may experience difficulties in managing this growth, which could disrupt our operations.

As of December 31, 2023, we had

114 employees, of whom 107 were full-time employees, 7 were part-time employees and all were located in China. As our Company matures,

we expect to expand our employee base. In addition, we intend to grow by expanding our business, increasing market penetration of our

existing products, developing new products and increasing our targeting of certain markets in China. Future growth would impose significant

additional responsibilities on our management, including the need to develop and improve our existing administrative and operational systems

and our financial and management controls and to identify, recruit, maintain, motivate, train, manage and integrate additional employees,

consultants and contractors. Also, our management may need to divert a disproportionate amount of its attention away from our day-to-day

activities and devote a substantial amount of time to managing these growth activities. We may not be able to effectively manage the expansion

of our operations,

which may result in weaknesses in our infrastructure, give rise to operational mistakes, loss of business opportunities,

loss of employees and reduced productivity among remaining employees. Future growth could require significant capital expenditures and

may divert financial resources from other projects, such as the development of our existing or future product candidates. If our management

is unable to effectively manage our growth, our expenses may increase more than expected, our ability to generate and grow revenue could

be reduced, and we may not be able to implement our business strategy. Our future financial performance and our ability to compete effectively

will depend, in part, on our ability to effectively manage any future growth.

Failure of beneficial owners

of our shares who are PRC residents to comply with certain PRC foreign exchange regulations could restrict our ability to distribute profits,

restrict our overseas and cross-border investment activities and subject us to liability under PRC law.

SAFE has promulgated regulations,

including the Notice on Relevant Issues Relating to Foreign Exchange Control on Domestic Residents’ Investment and Financing and

Round-Trip Investment through Special Purpose Vehicles, or SAFE Circular 37, and its appendices. These regulations require PRC residents,

including PRC institutions and individuals, to register with local branches of SAFE in connection with their direct establishment or indirect

control of an offshore entity, for the purpose of overseas investment and financing, with such PRC residents’ legally owned assets

or equity interests in domestic enterprises or offshore assets or interests, referred to in SAFE Circular 37 as a “special purpose

vehicle”, or SPV. The term “control” under SAFE Circular 37 is broadly defined as the operation rights, beneficiary

rights or decision-making rights acquired by the PRC residents in the offshore SPVs by such means as acquisition, trust, proxy, voting

rights, repurchase, convertible bonds or other arrangements. SAFE Circular 37 further requires amendment to the registration in the event

of any significant changes with respect to the SPV, such as increase or decrease of capital contributed by PRC individuals, share transfer

or exchange, merger, division or other material event. In the event that a PRC shareholder holding interests in a SPV fails to fulfill

the required SAFE registration, the PRC subsidiaries of that SPV may be prohibited from making profit distributions to the offshore parent

and from carrying out subsequent cross-border foreign exchange activities, and the SPV may be restricted in its ability to contribute

additional capital into its PRC subsidiaries. Further, failure to comply with the various SAFE registration requirements described above

could result in liability under PRC law for foreign exchange evasion.

These regulations apply to our

direct and indirect shareholders who are PRC residents and may apply to any offshore acquisitions or share transfers that we make in the

future if our shares are issued to PRC residents. However, in practice, different local SAFE branches may have different views and procedures

on the application and implementation of SAFE regulations, and there remains uncertainty with respect to its implementation. We cannot

assure you that these direct or indirect shareholders of our company who are PRC residents will be able to successfully update the registration

of their direct and indirect equity interest as required in the future. If they fail to update the registration, our PRC subsidiaries

could be subject to fines and legal penalties, and SAFE could restrict our cross-border investment activities and our foreign exchange

activities, including restricting our PRC subsidiaries’ ability to distribute dividends to, or obtain loans denominated in foreign

currencies from, our company, or prevent us from contributing additional capital into our PRC subsidiaries. As a result, our business

operations and our ability to make distributions to you could be materially and adversely affected. In addition, non-U.S. shareholders

may experience unfavorable tax consequences if such non-U.S. shareholders are determined to be a resident enterprise for PRC tax purposes.

See “Item 4. Information on the Company—Regulation—Legal Regulations on Tax in the PRC” and “Item 10. Additional

Information—E. Taxation— PRC Taxation” for further information.

Failure to make adequate

contributions to various employee benefits plans as required by PRC regulations may subject us to penalties.

Companies operating in China are

required to participate in various government sponsored employee benefit plans, including certain social insurance, housing funds and

other welfare-oriented payment obligations, and contribute to the plans in amounts equal to certain percentages of salaries, including

bonuses and allowances, of employees up to a maximum amount specified by the local government from time to time at locations where they

operate their businesses. The requirement of employee benefit plans has not been implemented consistently by the local governments in

China given the different levels of economic development in different locations. If we fail to make contributions to various employee

benefit plans and to comply with applicable PRC labor-related laws in the future, we may be subject to late payment penalties. We may

be required to make up the contributions for these plans as well as to pay late fees and fines. If we are subject to late fees or fines

in relation to the underpaid employee benefits, our financial condition and results of operations may be adversely affected.

We do not have business insurance

coverage. Any future business liability, disruption or litigation we experience might divert management focus from our business and could

significantly impact our financial results.

Availability of business insurance

products and coverage in China is limited, and most such products are expensive in relation to the coverage offered. We have determined

that the risks of disruption, cost of such insurance and the difficulties associated with acquiring such insurance on commercially reasonable

terms make it impractical for us to maintain such insurance. As a result, we do not have any business liability, disruption or litigation

insurance coverage for our operations in China. Accordingly, a business disruption, litigation or natural disaster may result in substantial

costs and divert management’s attention from our business, which would have an adverse effect on our results of operations and financial

condition.

We may require additional

financing in the future and our operations could be curtailed if we are unable to obtain required additional financing when needed.

In addition to the net proceeds

raised in our initial public offering, we may need to obtain additional debt or equity financing to fund future capital expenditures.

While we do not anticipate seeking additional financing in the immediate future, any additional equity financing may result in dilution

to the holders of our outstanding ordinary shares. Additional debt financing may impose affirmative and negative covenants that restrict

our freedom to operate our business. We cannot guaranty that we will be able to obtain additional financing on terms that are acceptable

to us, or any financing at all, and the failure to obtain sufficient financing could adversely affect our business operations.

Risks Related to Intellectual

Property

If we are not able to adequately

protect our proprietary intellectual property and information, and protect against third party claims that we are infringing on their

intellectual property rights, our results of operations could be adversely affected.

The value of our business depends

in part on our ability to protect our intellectual property and information, including our patents, trade secrets, and rights under agreements

with third parties, in China and around the world, as well as our customer, employee, and customer data. Third parties may try to challenge

our ownership of our intellectual property in China and around the world. In addition, intellectual property rights and protections in

China may be insufficient to protect material intellectual property rights in China. Further, our business is subject to the risk of third

parties counterfeiting our products or infringing on our intellectual property rights. The steps we have taken may not prevent unauthorized

use of our intellectual property. We may need to resort to litigation to protect our intellectual property rights, which could result

in substantial costs and diversion of resources. If we fail to protect our proprietary intellectual property and information, including

with respect to any successful challenge to our ownership of intellectual property or material infringements of our intellectual property,

this failure could have a significant adverse effect on our business, financial condition, and results of operations.

If we are unable to adequately

protect our intellectual property rights, or if we are accused of infringing on the intellectual property rights of others, our competitive

position could be harmed or we could be required to incur significant expenses to enforce or defend our rights.

Our commercial success will depend

in part on our success in obtaining and maintaining issued patents, and other intellectual property rights in China and elsewhere and

protecting our proprietary technology. If we do not adequately protect our intellectual property and proprietary technology, competitors

may be able to use our technologies or the goodwill we have acquired in the marketplace and erode or negate any competitive advantage

we may have, which could harm our business and ability to achieve profitability. The core of our business is our proprietary systems and

technology, together with our experience and expertise in waste treatment services, particularly in rural sewage treatment and septic

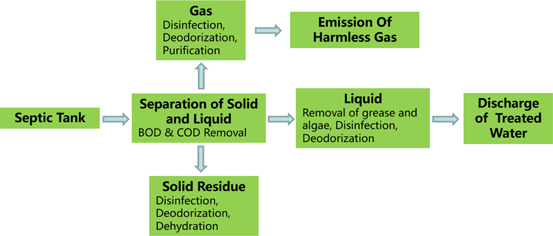

tank treatment. As of December 31, 2023, we had 2 invention patents, 38 utility model patents, 3 trademarks and 2 computer software copyrights.

We are continually working to upgrade our quick separation technology and septic tank treatment systems through independent research and