false

N-2

0001754836

Eagle Point Income Co Inc.

0001754836

2023-01-01

2023-12-31

0001754836

2023-12-31

0001754836

2023-12-31

2023-12-31

0001754836

2024-01-31

0001754836

2024-01-31

2024-01-31

0001754836

eic:RisksOfInvestingInClosAndOtherStructuredDebtSecuritiesMember

2023-01-01

2023-12-31

0001754836

eic:SubordinatedSecuritiesRiskMember

2023-01-01

2023-12-31

0001754836

eic:HighYieldInvestmentRiskMember

2023-01-01

2023-12-31

0001754836

eic:LeverageRiskMember

2023-01-01

2023-12-31

0001754836

eic:CreditRisksMember

2023-01-01

2023-12-31

0001754836

eic:KeyPersonnelRiskMember

2023-01-01

2023-12-31

0001754836

eic:ConflictsOfInterestRiskMember

2023-01-01

2023-12-31

0001754836

eic:PrepaymentRisksMember

2023-01-01

2023-12-31

0001754836

eic:LiquidityRiskMember

2023-01-01

2023-12-31

0001754836

eic:ManagementFeeRiskMember

2023-01-01

2023-12-31

0001754836

eic:FairValuationOfTheCompanysPortfolioInvestmentsMember

2023-01-01

2023-12-31

0001754836

eic:LimitedInvestmentOpportunitiesRiskMember

2023-01-01

2023-12-31

0001754836

eic:MarketRiskMember

2023-01-01

2023-12-31

0001754836

eic:LoanAccumulationFacilitiesRiskMember

2023-01-01

2023-12-31

0001754836

eic:SyntheticInvestmentsRiskMember

2023-01-01

2023-12-31

0001754836

eic:CurrencyRiskMember

2023-01-01

2023-12-31

0001754836

eic:HedgingRiskMember

2023-01-01

2023-12-31

0001754836

eic:ReinvestmentRiskMember

2023-01-01

2023-12-31

0001754836

us-gaap:InterestRateRiskMember

2023-01-01

2023-12-31

0001754836

eic:RefinancingRiskMember

2023-01-01

2023-12-31

0001754836

eic:TaxRiskMember

2023-01-01

2023-12-31

0001754836

eic:CounterpartyRiskMember

2023-01-01

2023-12-31

0001754836

eic:PriceRiskMember

2023-01-01

2023-12-31

0001754836

eic:GlobalRisksMember

2023-01-01

2023-12-31

0001754836

eic:BankingRiskMember

2023-01-01

2023-12-31

0001754836

eic:CommonSharesMember

2023-01-01

2023-12-31

0001754836

eic:PreferredSharesMember

2023-01-01

2023-12-31

0001754836

eic:PreferredSharesMember

2023-12-31

0001754836

eic:RevolvingCreditFacilityBNPParibasMember

2023-12-31

0001754836

eic:PreferredSharesMember

2022-12-31

0001754836

eic:PreferredSharesMember

2022-01-01

2022-12-31

0001754836

eic:RevolvingCreditFacilityBNPParibasMember

2022-12-31

0001754836

eic:PreferredSharesMember

2021-12-31

0001754836

eic:PreferredSharesMember

2021-01-01

2021-12-31

0001754836

eic:RevolvingCreditFacilityBNPParibasMember

2021-12-31

0001754836

eic:RevolvingCreditFacilitySocieteGeneraleMember

2020-12-31

0001754836

eic:RevolvingCreditFacilitySocieteGeneraleMember

2019-12-31

0001754836

2022-03-31

0001754836

2022-01-01

2022-03-31

0001754836

2022-06-30

0001754836

2022-04-01

2022-06-30

0001754836

2022-09-30

0001754836

2022-07-01

2022-09-30

0001754836

2022-12-31

0001754836

2022-10-01

2022-12-31

0001754836

2023-03-31

0001754836

2023-01-01

2023-03-31

0001754836

2023-06-30

0001754836

2023-04-01

2023-06-30

0001754836

2023-09-30

0001754836

2023-07-01

2023-09-30

0001754836

2023-10-01

2023-12-31

0001754836

eic:SeriesATermPreferredStockMember

2023-01-01

2023-12-31

0001754836

eic:SeriesBTermPreferredStockMember

2023-01-01

2023-12-31

0001754836

eic:CommonSharesMember

2023-12-31

2023-12-31

0001754836

eic:PreferredSharesMember

2023-12-31

2023-12-31

0001754836

eic:SeriesATermPreferredStockMember

2023-12-31

2023-12-31

0001754836

eic:SeriesBTermPreferredStockMember

2023-12-31

2023-12-31

0001754836

2024-02-15

iso4217:USD

xbrli:shares

iso4217:USD

xbrli:shares

xbrli:pure

UNITED

STATES

SECURITIES

AND EXCHANGE COMMISSION

Washington,

D.C. 20549

FORM

N-CSR

CERTIFIED

SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT

INVESTMENT COMPANIES

Investment

Company Act File Number: 811-23384

Eagle

Point Income Company Inc.

(Exact

name of registrant as specified in charter)

600

Steamboat Road, Suite 202

Greenwich,

CT 06830

(Address

of principal executive offices) (Zip code)

Thomas

P. Majewski

c/o

Eagle Point Income Company Inc.

600

Steamboat Road, Suite 202

Greenwich,

CT 06830

(Name

and address of agent for service)

Copies

to

Thomas

J. Friedmann

Philip

Hinkle

Dechert LLP

One International Place, 40th Floor

100

Oliver Street

Boston,

MA 02110

(617) 728-7120

Registrant’s

telephone number, including area code: (203) 340-8500

Date

of fiscal year end: December 31

Date

of reporting period: December 31, 2023

Form

N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission

to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of

1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection,

and policymaking roles.

A

registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant

is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office

of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection

burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 100 F Street, NE, Washington,

DC 20549. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

| Item 1. |

Report to Stockholders |

The

Annual Report to stockholders of Eagle Point Income Company Inc. (the “Company”) for the year ended December 31, 2023 is

filed herewith.

Eagle

Point Income Company Inc.

Annual

Report – December 31, 2023

Table of Contents

LETTER TO STOCKHOLDERS

AND MANAGEMENT DISCUSSION OF COMPANY PERFORMANCE

February 22,

2024

Dear Fellow

Stockholders:

We are pleased

to provide you with the enclosed report of Eagle Point Income Company Inc. (“we,” “us,” “our”

or the “Company”) for the fiscal year ended December 31, 2023.

The primary

investment objective of the Company is to generate high current income, with a secondary objective to generate capital appreciation.

We seek to achieve these objectives by investing primarily in junior debt tranches of collateralized loan obligations (“CLOs”)

rated BB – including those rated BB+, BB or BB- – or their equivalent. In addition, the Company may invest up to 35%

of its total assets in CLO equity securities and other securities and instruments that are consistent with our investment objectives.

The Company

benefits from the specialized investment experience of Eagle Point Income Management LLC (“Eagle Point” or the “Adviser”),

which applies its proprietary, private markets-style investment process to CLO investing. This process seeks to maximize returns

while mitigating risks. We believe the scale and experience of our Adviser and its affiliates in CLO investing provides the Company

with meaningful advantages.

The Company

had an excellent 2023. The rising interest rate environment during the year was materially positive for our portfolio of mostly

floating-rate CLO junior debt securities. For the year ended December 31, 2023, the Company had an increase in net assets resulting

from operations (inclusive of unrealized mark-to-market gains) of $29.3 million, or $3.21 per weighted average common share.1

This represents a GAAP ROE of 25.93% during the year.2 From December 31, 2022 through December 31, 2023, the Company’s

net asset value (“NAV”) per common share increased by 11% to $14.39 from $12.91.

As a result

of our strong 2023 performance, the Company increased its monthly common distribution from $0.14 per share at the end of 2022 to

$0.18 per share at the end of 2023. Additionally, the Company was pleased to increase its monthly common distribution again to

$0.20 per share beginning in January 2024.

During 2023,

we:

| ● | Generated strong GAAP net

investment income (“NII”) less realized capital losses of $1.90 per weighted average common share in 2023. Excluding

non-recurring items related to securities offerings and incurring Federal excise tax on our spillover income, our income of $2.08

per weighted average common share would have been above the $1.98 per share in regular monthly common distributions paid during the

year. |

| ● | Increased our common

distribution twice during the year to $0.18 per share. In addition, the Company declared an additional increase in our monthly

common |

Past

performance is not indicative of, or a guarantee of, future performance.

Please

see page 11 for endnotes.

| | | distribution

to $0.20 per share beginning in January 2024. Our current monthly distribution rate is

equal to 250% of what was paid during the first quarter of 2021. |

| ● | Significantly increased

recurring cash flows for the year to $29.0 million, or $3.17 per weighted average common share. This compares to recurring cash

flows of $21.0 million, or $2.97 per weighted average common share, collected during 2022. Recurring cash flows received in 2023

exceeded our total expenses and regular common distributions by $0.17 per weighted average common share. |

| ● | Strengthened our balance

sheet by issuing $34.3 million of 7.75% Series B Term Preferred Stock due in 2028 (the “Series B Term Preferred Stock”),

with proceeds deployed opportunistically into new CLO debt and equity investments, as well as raising $42.5 million of additional

common equity through our at-the-market (“ATM”) program and committed equity finance arrangement at a premium to NAV. |

While CLO junior

debt remains a significant majority of the Company’s portfolio, the CLO equity exposure continued to help enhance the Company’s

earnings ability. We believe CLOs, with their strong structural protections and self-correcting mechanisms, are well-positioned

to weather periods of market volatility. In our view, the performance of our portfolio through volatility has demonstrated the

resilience of the Company’s investment strategy.

Our portfolio’s

strong performance in 2023 allowed the Company to pay cash distributions to shareholders of $1.98 per share, or 14.01% of our average

stock price.

As of January

31, 2024, management’s unaudited estimate of the range of the Company’s NAV per common share was between $14.94 and

$15.04. The midpoint of this range represents an increase of 4.2% compared to the NAV per common share as of December 31, 2023.

As of February 15, 2024, we have $26.6 million in cash and available borrowing capacity on our balance sheet.

Company

Overview

Common Stock

The Company’s

common stock trades on the New York Stock Exchange (“NYSE”) under the symbol “EIC.” As of December 31,

2023, the NAV per share of the Company’s common stock was $14.39. The trading price of our common stock may, and often does,

differ from NAV per share. The closing price per share of our common stock was $14.57 on December 29, 2023, representing a 1.25%

premium to NAV per share as of year end.3

In connection

with our at-the-market offering program and committed equity financing arrangement, the Company sold 3.1 million shares of common

stock during the year for total net proceeds to the Company of approximately $42.5 million. The common stock issuance resulted in

NAV accretion of $0.13 per share.

Past

performance is not indicative of, or a guarantee of, future performance.

Please

see page 11 for endnotes.

During 2023,

through our usage of the ATM and committed equity financing programs, as well as the growth of our portfolio, we saw a significant

enhancement in the liquidity of the Company’s common stock as the year progressed. This was evidenced by the increased average

daily trading volume during the fourth quarter of 2023, which was nearly double the fourth quarter of 2022. With approximately

11 million outstanding common shares as of the end of 2023, the Company’s market cap as of December 31, 2023 of approximately

$160 million was more than 40% greater than where it stood at the end of 2022.

The Company

declared and paid nine monthly distributions of $0.16 per share of common stock from January 2023 through September 2023, and three

monthly distributions of $0.18 per share of common stock from October 2023 through December 2023. The Company paid a total of $1.98

per common share of monthly distributions during 2023. Please note that the actual frequency, components and amount of such distributions

are subject to variation over time.

At year-end,

a shareholder who purchased common stock as part of our initial public offering (“IPO”) in July 2019 has received total

cash distributions of $7.02 per share, over 35% of the IPO price. A portion of these distributions was comprised of a return of

capital.4

As of January

31, 2024, the closing price per share of common stock was $15.42, reflecting a premium of 2.87% compared to the midpoint of management’s

unaudited and estimated NAV range of $14.94 to $15.04 as of January month-end.

We also highlight

the Company’s dividend reinvestment plan (“DRIP”) for common stockholders. This plan allows common stockholders

to have their distributions automatically reinvested into new shares of common stock. If the prevailing market price of our common

stock exceeds our NAV per share, such reinvestment is at a discount (up to 5%) to the prevailing market price. If the prevailing

market price of our common stock is less than our NAV per share, such reinvestment is at the prevailing market price, subject to

the terms in the DRIP. We encourage all common stockholders to carefully review the terms of the plan. See “Dividend

Reinvestment Plan” in the enclosed report.

Past

performance is not indicative of, or a guarantee of, future performance.

Please

see page 11 for endnotes.

Financing Solutions

In addition

to our common stock, the Company has two preferred equity securities which trade on the NYSE, summarized below:

| Security |

NYSE

Symbol |

Par

Amount

Outstanding |

Rate |

Payment

Frequency |

Callable |

Maturity |

| 5.00%

Series A Term Preferred Stock due 2026 |

EICA |

$38.0

million |

5.00% |

Monthly |

Callable |

October

2026 |

| 7.75%

Series B Term Preferred Stock due 2028 |

EICB |

$34.3

million |

7.75% |

Monthly |

July

2025 |

July

2028 |

The weighted

average maturity on our preferred stock as of December 31, 2023 was approximately 3.7 years. In addition, all of our preferred

stock financing is fixed rate, providing us with certainty in a dynamic rate environment.

As of December

31, 2023, we had $14.5 million in outstanding borrowings from the Company’s $25 million revolving credit facility. This,

coupled with our preferred stock, represented leverage of 36% of total assets (less current liabilities). Over the long term, management

expects the Company to operate under normal market conditions generally with leverage of between 25% and 35% of total assets (less

current liabilities). Based on applicable market conditions at any given time, or should significant opportunities present themselves,

the Company may incur leverage in excess of this amount, subject to applicable regulatory and contractual limits.

Past

performance is not indicative of, or a guarantee of, future performance.

Please

see page 11 for endnotes.

Portfolio

Overview

2023 Portfolio

Update

The secondary

market was a key focus for our Adviser throughout 2023, as CLO secondary levels offered material discounts compared to most CLO

primary opportunities. The Company benefited from an elevated rate environment as the base rates for floating rate CLO debt investments

reached the highest levels observed in well over 15 years. As CLO prices appreciated throughout the year, the convexity in our

CLO debt portfolio contributed significantly to the appreciation of the Company’s investments.

For the year

ended December 31, 2023, the Company deployed $83.5 million in gross capital into CLO debt, CLO equity and other investments. The

CLO debt had a weighted average expected yield (to maturity) of 12.47% at the time of purchase, while the CLO equity had a weighted

average expected yield of 23.83% at the time of purchase.5 With essentially all of our CLO debt purchased at discounts,

and due to the callable nature of most CLO debt tranches, there is potential for higher returns than the yield to maturity for

most of those investments.

As of December

31, 2023, we had 91 CLO investments in our portfolio, the large majority of which are BB-rated (or the equivalent) CLO junior debt.

At year-end, the weighted average effective yield on the aggregate portfolio of CLO debt and equity investments was 13.29%, based

on amortized cost. This compares to 12.82% as of December 31, 2022.

During 2023,

the Company received recurring cash flows of $29.0 million, or $3.17 per weighted average common share. This was a significant

increase compared to our 2022 recurring cash flows, which totaled $21.0 million, or $2.97 per weighted average common share. Recurring

cash flows received in 2023 exceeded total expenses and our regular common distribution by $0.17 per weighted average common share.

Included within

the enclosed report, you will find detailed portfolio information, including certain look-through information related to the underlying

collateral characteristics of the CLO investments that we held as of December 31, 2023.

Past

performance is not indicative of, or a guarantee of, future performance.

Please

see page 11 for endnotes.

Market

Overview6

Loan Market

Despite a few

periods of considerable volatility in 2023, the broadly syndicated loans (“BSL”) market capped off its strongest year

since 2009. The Credit Suisse Leverage Loan Index7 (“CSLLI”) recorded a total return of 13.04% in 2023.

Firming BSL prices, higher floating rate coupons, and below average loan default levels drove performance through most of the year,

as demand from investors seeking yields amidst the higher-for-longer environment overshadowed intermittent risk-off periods during

the year. From November into year-end, economic data pointed investors towards a “soft landing” – or even “no

landing” – scenario, igniting a broad rally across debt markets, including broadly syndicated loans and CLOs.

Average BSL

prices finished 2023 at 95.32. This is an increase from 91.89 at the beginning of the year, but still below pre-Ukraine war levels.

As such, with a significant share of high-quality issuers still trading at discounted prices, we believe this represents a path

to further upside. Additionally, markets like these allow CLO collateral managers to improve underlying loan portfolios through

relative value swaps.

The trailing 12-month average default rate ended 2023 at 1.53%. This compares to 0.72% for 2022 but remains comfortably below the long-term

average of 2.70%.8 The Fund’s underlying portfolio has a materially lower default exposure

at only 0.55%. According to JP Morgan, default activity for December 2023 was the lowest since October 2022, highlighting that

while higher costs are impacting many BSL issuers, their fundamentals are holding up well. Indeed, third quarter earnings show

continued growth in issuers’ revenue and EBITDA, helping to offset the effects of rising rates.

Refinancing

activity by BSL issuers increased on a year-over-year basis, accounting for over 58% of 2023’s new supply volume, compared

to 26% in 2022. The 12-month trailing loan repayment rate increased to nearly 17.6% in December, its highest monthly level for

the year. With only 7% of the outstanding loan market at year-end set to mature prior to 2026, the often-feared maturity wall has

been pushed out: debt coming due in 2025 was cut down by 58% in 2023 to $83.1 billion, and 2026 maturities were reduced by 26%

to $175 billion. Only 7.7% of the loan portfolios underlying our CLO equity positions mature prior to 2026.

For 2023, mutual

funds and ETFs investing in U.S. leveraged loans experienced net outflows of $17 billion, compared to net outflows of $13 billion

in 2022.9 The high-yield mutual fund/ETF market, by comparison, recorded $7 billion of net outflows in 2023 after recording

$49 billion of net outflows in 2022. While these are significant sums of money, they represent a small fraction of the overall

$1.4 trillion BSL market.

A notable dynamic

that picked up steam during the second half of the year was the trend of stressed BSLs being prepaid and refinanced into new facilities

from private credit funds and business development companies (“BDCs”). Due to the sheer amount of capital raised for

private credit, we even saw CCC-rated loans getting paid off at par as companies refinanced their BSL debt in the private credit

market. The prepayment of CCC-rated loans allows reinvesting CLOs

Past

performance is not indicative of, or a guarantee of, future performance.

Please

see page 11 for endnotes.

to redeploy capital into higher quality discounted loan issues.

This has been a good trend for CLOs and if it continues into 2024, as we expect, the potential reduction of tail risk is net positive

for CLOs. Overall, private credit managers refinanced around $16 billion of BSLs in 2023, according to LCD Pitchbook.

CLO Market

The CLO market

saw $116 billion of new CLO issuance in 2023, according to LCD Pitchbook. Wide liability spreads and a generally unattractive CLO

equity arbitrage did little to deter the less economically sensitive captive CLO funds from issuing CLOs. We believe due to the

misalignment of incentive, many CLO issuers with captive CLO funds are willing to accept suboptimal CLO equity returns in order

to generate new fee streams for themselves. Of the 208 new BSL CLOs issued during the year, we estimate over 80% were supported

by captive CLO funds, while economically sensitive investors like our Adviser focused on the attractive opportunities in the secondary

market.

CLO refinancing

and reset volumes declined in 2023. Of the $24.6 billion in refinancings and resets across 57 transactions in 2023, $14.7 billion

occurred in the last three months of the year, per LCD Pitchbook data, as CLO debt spreads tightened with the year-end rally.

By the end of

2023, CLO BB discount margins averaged approximately 783 basis points over the secured overnight financing rate (“SOFR”),

a tightening of 148 basis points since the end of 2022. With average CLO BB prices at 92.5 points, we believe there continues to

be further upside to the Company’s portfolio.

Additional

Information

In addition

to the Company’s regulatory requirement to file certain quarterly and annual portfolio information as described further in

the enclosed report, the Company makes certain unaudited portfolio information available each month on its website in addition

to making certain other unaudited financial information available on its website (www.eaglepointincome.com). This information includes

(1) an estimated range of the Company’s NII and realized capital gains or losses per share of common stock for each calendar

quarter end, generally made available within the first fifteen days after the applicable calendar month end, (2) an estimated range

of the Company’s NAV per share of common stock for the prior month end and certain additional portfolio-level information,

generally made available within the first fifteen days after the applicable calendar month end, and (3) during the latter part

of each month, an updated estimate of the Company’s NAV per share of common stock, if applicable, and, with respect to each

calendar quarter end, an updated estimate of the Company’s NII and realized capital gains or losses per share for the applicable

quarter, if available.

Subsequent

Developments

Management’s

unaudited estimate of the range of the Company’s NAV per share of common stock was between $14.94 and $15.04 as of January

31, 2024. The midpoint of this range

Past

performance is not indicative of, or a guarantee of, future performance.

Please

see page 11 for endnotes.

represents an increase of 4.2% compared to the NAV per common share as of December 31, 2023.

On January 31,

2024, the Company paid a monthly distribution of $0.20 per common share to stockholders of record on January 11, 2024. Additionally,

and as previously announced, the Company declared distributions of $0.20 per share of common stock payable on each of February

29, 2024 and March 28, 2024 to holders of record on February 9, 2024 and March 8, 2024, respectively. Additionally, on February

13, 2024, the Company declared three separate distributions of $0.20 per share on its common stock. The distributions are payable

on each of April 30, 2024, May 31, 2024 and June 28, 2024 to holders of record as of April 10, 2024, May 13, 2024 and June 10,

2024, respectively.

On January 31,

2024, the Company paid a monthly distribution of $0.104167 per share of the Company’s 5.00% Series A Term Preferred Stock

due 2026 (the “Series A Term Preferred Stock”) to holders of record on January 11, 2024. Additionally, and as previously

announced, the Company declared distributions of $0.104167 per share on Series A Term Preferred Stock, payable on each of February

29, 2024 and March 28, 2024 to holders of record on February 9, 2024 and March 8, 2024, respectively. Additionally, on February

13, 2024, the Company declared three separate distributions of $0.104167 per share on its Series A Preferred Stock. The distributions

are payable on each of April 30, 2024, May 31, 2024 and June 28, 2024 to holders of record as of April 10, 2024, May 13, 2024 and

June 10, 2024, respectively.

On January 31,

2024, the Company paid a monthly distribution of $0.161459 per share of the Company’s Series B Term Preferred Stock to holders

of record on January 11, 2024. Additionally, and as previously announced, the Company declared distributions of $0.161459 per share

on Series B Term Preferred Stock, payable on each of February 29, 2024 and March 28, 2024 to holders of record on February 9, 2024

and March 8, 2024, respectively. Additionally, on February 13, 2024, the Company declared three separate distributions of $0.161459

per share on its Series B Preferred Stock. The distributions are payable on each of April 30, 2024, May 31, 2024 and June 28, 2024

to holders of record as of April 10, 2024, May 13, 2024 and June 10, 2024, respectively.

In the period

from January 1, 2024 through February 15, 2024, the Company received cash distributions on its investment portfolio of $10.3 million.

During that same period, the Company made net new investments totaling $8.9 million. As of February 15, 2024, the Company had $26.6

million of cash available for investment, inclusive of undrawn amounts on our revolving credit facility.

*

* * * *

Management remains

keenly focused on continuing to create value for our stockholders. We appreciate the trust and confidence our fellow stockholders

have placed in the Company.

Past

performance is not indicative of, or a guarantee of, future performance.

Please

see page 11 for endnotes.

Thomas Majewski

Chairman and

Chief Executive Officer

This

letter is intended to assist stockholders in understanding the Company’s performance during the twelve months ended December

31, 2023. The views and opinions in this letter were current as of February 15, 2024. Statements other than those of historical

facts included herein may constitute forward-looking statements and are not guarantees of future performance or results and involve

a number of risks and uncertainties. Actual results may differ materially from those in the forward-looking statements as a result

of a number of factors. The Company undertakes no duty to update any forward-looking statement made herein. Information contained

on our website is not incorporated by reference into this stockholder letter and you should not consider information contained

on our website to be part of this stockholder letter or any other report we file with the Securities and Exchange Commission.

Past

performance is not indicative of, or a guarantee of, future performance.

Please

see page 11 for endnotes.

ABOUT

OUR ADVISER

Eagle Point

Income Management LLC is a specialist asset manager focused exclusively on investing in CLO securities and related investments.

As of December 31, 2023, our Adviser has approximately $9.1 billion of assets under management (inclusive of undrawn capital commitments).10

Notes

| 1 | “Weighted average common share”

is calculated based on the average daily number of shares of common stock outstanding during the period and “per common share”

refers to per share of the Company’s common stock. |

| 2 | Return on our common equity reflects the Company’s

cumulative monthly performance net of applicable expenses and fees measured against beginning capital adjusted for any common equity

issued during the period. |

| 3 | An investment company trades at a premium when the market price at

which its common shares trade is more than its net asset value per common share. Alternatively, an investment company trades at

a discount when the market price at which its common shares trade is less than its net asset value per common share. |

| 4 | To date, a portion of common stock distributions has been estimated to be a return of capital as

noted under the Tax Information section on the Company’s website. The actual components of the Company's distributions for

U.S. tax reporting purposes can only be finally determined as of the end of each fiscal year of the Company and are thereafter

reported on Form 1099-DIV. A distribution comprised in whole or in part by a return of capital does not necessarily reflect the

Company’s investment performance and should not be confused with “yield” or “income”. Future distributions

may consist of a return of capital. Not a guarantee of future distributions or yield. |

| 5 | Weighted average effective yield is based on an investment’s amortized cost and expected

future cash flows whereas weighted average expected yield is based on an investment’s fair market value and expected future

cash flows as of the applicable period end as disclosed in the Company’s financial statements, which is subject to change

from period to period. |

| 6 | JPMorgan Chase & Co.; S&P Capital IQ; Pitchbook LCD; Credit Suisse |

| 7 | The CSLLI tracks the investable universe of the US

dollar-denominated leveraged loan market. The performance of an index is not an exact representation of any particular investment,

as you cannot invest directly in an index. |

| 8 | “Par-weighted default rate” represents the rate of obligors who fail to remain current on their loans based on

the par amount. |

| 9 | JPMorgan Chase & Co. North American Credit Research – JPM High Yield and Leveraged Loan

Research (cumulative 2023 reports). |

| 10 | Calculated in the aggregate with its affiliate Eagle Point Credit Management LLC and certain other

affiliated advisers. |

Past

performance is not indicative of, or a guarantee of, future performance.

Page Intentionally Left

Blank

Important Information about this Report and

Eagle Point Income Company Inc.

This report is transmitted

to the stockholders of Eagle Point Income Company Inc. (“we”, “us”, “our” or the “Company”)

and is furnished pursuant to certain regulatory requirements. This report and the information and views herein do not constitute

investment advice, or a recommendation or an offer to enter into any transaction with the Company or any of its affiliates. This

report is provided for informational purposes only, does not constitute an offer to sell securities of the Company and is not a

prospectus. From time to time, the Company may have a registration statement relating to one or more of its securities on file

with the US Securities and Exchange Commission (“SEC”). Any registration statement that has not yet been declared effective

by the SEC, and any prospectus relating thereto, is not complete and may be changed. Any securities that are the subject of such

a registration statement may not be sold until the registration statement filed with the SEC is effective.

The information and its

contents are the property of Eagle Point Income Management LLC (the “Adviser”) and/or the Company. Any unauthorized

dissemination, copying or use of this presentation is strictly prohibited and may be in violation of law. This presentation is

being provided for informational purposes only.

Investors

should read the Company’s prospectus and SEC filings (which are publicly available on the EDGAR Database on the SEC website

at http://www.sec.gov) carefully and consider their investment

goals, time horizons and risk tolerance before investing in the Company. Investors should consider the Company’s investment

objectives, risks, charges and expenses carefully before investing in securities of the Company. There is no guarantee that any

of the goals, targets or objectives described in this report will be achieved.

An investment in the Company

is not appropriate for all investors. The investment program of the Company is speculative, entails substantial risk and includes

investment techniques not employed by traditional mutual funds. An investment in the Company is not intended to be a complete investment

program. Shares of closed-end investment companies, such as the Company, frequently trade at a discount from their net asset value

(“NAV”), which may increase investors’ risk of loss. Past performance is not indicative of, or a guarantee of,

future performance. The performance and certain other portfolio information quoted herein represents information as of December

31, 2023. Nothing herein should be relied upon as a representation as to the future performance or portfolio holdings of the Company.

Investment return and principal value of an investment will fluctuate, and shares, when sold, may be worth more or less than their

original cost. The Company’s performance is subject to change since the end of the period noted in this report and may be

lower or higher than the performance data shown herein.

Neither the Adviser nor

the Company provide legal, accounting or tax advice. Any statement regarding such matters is explanatory and may not be relied

upon as definitive advice. Investors should consult with their legal, accounting and tax advisors regarding any potential investment.

The information presented herein is as of the dates noted herein and is derived from financial and other information of the Company,

and, in certain cases, from third party sources and reports (including reports of third party custodians, CLO managers and trustees)

that have not been independently verified by the Company. As noted herein, certain of this information is estimated and unaudited,

and therefore subject to change. We do not represent that such information is accurate or complete, and it should not be relied

upon as such.

Eagle Point Income Company

Inc.

The following information

in this annual report is a summary of certain changes during the fiscal year ended December 31, 2023. This information may not

reflect all of the changes that have occurred since you purchased shares of our common stock.

During the applicable period,

there have been: (i) no material changes to the Company’s investment objectives and policies that have not been approved

by shareholders, (ii) no material changes to the Company’s principal risks, (iii) no changes to the persons primarily responsible

for day-to-day management of the Company; and (iv) no changes to the Company’s charter or bylaws that would delay or prevent

a change of control of the Company.

Investment Objectives

and Strategies

We are an externally managed,

diversified closed-end management investment company that has registered as an investment company under the Investment Company

Act of 1940, as amended (the “1940 Act”). We have elected to be treated, and intend to qualify annually, as a regulated

investment company, or “RIC,” under Subchapter M of the Internal Revenue Code of 1986, as amended, or the “Code,”

beginning with our tax year ended December 31, 2018. We were formed on September 28, 2018

as EP Income Company LLC, a Delaware

limited liability company, and converted into a Delaware corporation on October 16, 2018.

Our primary investment

objective is to generate high current income, with a secondary objective to generate capital appreciation. We seek to achieve our

investment objectives by investing primarily in junior debt tranches of CLOs, that are collateralized by a portfolio consisting

primarily of below investment grade U.S. senior secured loans with a large number of distinct underlying borrowers across various

industry sectors. We focus on CLO debt tranches rated “BB” (e.g., BB+, BB or BB-, or their equivalent) by Moody’s

Investors Service, Inc., or “Moody’s,” Standard & Poor’s, or “S&P,” or Fitch Ratings,

Inc., or “Fitch,” and/or other applicable nationally recognized statistical rating organizations. We may also invest

in other junior debt tranches of CLOs, loan accumulation facilities, senior debt tranches of CLOs and other related securities

and instruments, including synthetic investments, such as significant risk transfer securities and credit risk transfer securities

issued by banks or other financial institutions. In addition, we may invest up to 35% of our total assets (at the time of investment)

in CLO equity securities. We expect our investments in CLO equity securities to primarily reflect minority ownership positions.

We may also invest in other securities and instruments that the Adviser believes are consistent with our investment objectives

such as securities issued by other securitization vehicles, such as collateralized bond obligations or “CBOs”. The

amount that we will invest in other securities and instruments, which may include investments in debt and other securities issued

by CLOs collateralized by non-U.S. loans or securities of other collective investment vehicles, will vary from time to time and,

as such, may constitute a material part of our portfolio on any given date, all as based on the Adviser’s assessment of prevailing

market conditions. The CLO securities in which we primarily seek to invest are rated below investment grade or, in the case of

CLO equity securities, are unrated and are considered speculative with respect to timely payment of interest and repayment of principal.

Below investment grade and unrated securities are also sometimes referred to as “junk” securities.

These investment objectives

are not fundamental policies of ours and may be changed by our board of directors without prior approval of our stockholders.

Investment Restrictions

Our investment objectives

and our investment policies and strategies, except for the eight investment restrictions designated as fundamental policies under

this caption, are not fundamental and may be changed by the board of directors without stockholder approval.

The following eight investment

restrictions are designated as fundamental policies and, as such, cannot be changed without the approval of the holders of a majority

of our outstanding voting securities:

| 1. | We may not borrow money, except as permitted by (i) the 1940 Act,

or interpretations or modifications by the SEC, SEC staff or other authority with appropriate jurisdiction, or (ii) exemptive or

other relief or permission from the SEC, SEC staff or other authority with appropriate jurisdiction; |

| 2. | We may not engage in the business of underwriting securities issued

by others, except to the extent that we may be deemed to be an underwriter in connection with the disposition of portfolio securities; |

| 3. | We may not purchase or sell physical commodities or contracts

for the purchase or sale of physical commodities. Physical commodities do not include futures contracts with respect to securities,

securities indices, currency or other financial instruments; |

| 4. | We may not purchase or sell real estate, which term does not

include securities of companies which deal in real estate or mortgages or investments secured by real estate or interests therein,

except that we reserve freedom of action to hold and to sell real estate acquired as a result of our ownership of securities; |

| 5. | We may not make loans, except to the extent permitted by (i)

the 1940 Act, or interpretations or modifications by the SEC, SEC staff or other authority with appropriate jurisdiction, or (ii)

exemptive or other relief or permission from the SEC, SEC staff or other authority with appropriate jurisdiction. For purposes

of this investment restriction, the purchase of debt obligations (including acquisitions of loans, loan participations or other

forms of debt instruments) shall not constitute loans by us; |

| 6. | We may not issue senior securities, except to the extent permitted

by (i) the 1940 Act, or interpretations or modifications by the SEC, the SEC staff or other authority with appropriate jurisdiction,

or (ii) exemptive or other relief or permission from the SEC, SEC staff or other authority with appropriate jurisdiction; |

| 7. | We may not invest in any security if as a result of such investment,

25% or more of the value of our total assets, taken at market value at the time of each investment, are in the securities of issuers

in any particular industry or group of |

| | | industries

except (a) securities issued or guaranteed by the U.S. government and its agencies and

instrumentalities or tax-exempt securities of state and municipal governments or their

political subdivisions (however, not including private purpose industrial development

bonds issued on behalf of non-government issuers), or (b) as otherwise provided by the

1940 Act, as amended from time to time, and as modified or supplemented from time to

time by (i) the rules and regulations promulgated by the SEC under the 1940 Act, as amended

from time to time, and (ii) any exemption or other relief applicable to us from the provisions

of the 1940 Act, as amended from time to time. For purposes of this restriction, in the

case of investments in loan participations between us and a bank or other lending institution

participating out the loan, we will treat both the lending bank or other lending institution

and the borrower as “issuers.” For purposes of this restriction, an investment

in a CLO, collateralized bond obligation, collateralized debt obligation or a swap or

other derivative will be considered to be an investment in the industry or group of industries

(if any) of the underlying or reference security, instrument or asset; and |

| 8. | We may not engage in short sales, purchases on margin, or

the writing of put or call options, except as permitted by (i) the 1940 Act, or interpretations or modifications by the SEC, SEC

staff or other authority with appropriate jurisdiction or (ii) exemptive or other relief or permission from the SEC, SEC staff

or other authority with appropriate jurisdiction. |

The latter part of certain

of our fundamental investment restrictions (i.e., the references to “except to the extent permitted by (i) the 1940

Act, or interpretations or modifications by the SEC, the SEC staff or other authority with appropriate jurisdiction, or (ii) exemptive

or other relief or permission from the SEC, SEC staff or other authority with appropriate jurisdiction”) provides us with

flexibility to change our limitations in connection with changes in applicable law, rules, regulations or exemptive relief. The

language used in these restrictions provides the necessary flexibility to allow our board of directors to respond efficiently to

these kinds of developments without the delay and expense of a stockholder meeting.

Whenever an investment

policy or investment restriction set forth in this report or in our prospectus states a maximum percentage of assets that may be

invested in any security or other asset, or describes a policy regarding quality standards, such percentage limitation or standard

shall be determined immediately after and as a result of our acquisition of such security or asset. Accordingly, any later increase

or decrease resulting from a change in values, assets or other circumstances or any subsequent rating change made by a rating agency

(or as determined by the Adviser if the security is not rated by a rating agency) will not compel us to dispose of such security

or other asset. Notwithstanding the foregoing, we must always be in compliance with the borrowing policies set forth above.

Use of Leverage and

Leverage Risks

The use of leverage, whether

directly through borrowing under a revolving credit facility with BNP Paribas (the “Credit Facility”) or the issuance

of the Series A Term Preferred Stock and Series B Term Preferred Stock, or indirectly through investments such as CLO junior debt

and equity securities that inherently involve leverage, may magnify our risk of loss. CLO junior debt and equity securities are

very highly leveraged (with CLO equity securities typically being leveraged ten times), and therefore the CLO securities in which

we invest are subject to a higher degree of loss since the use of leverage magnifies losses.

We have incurred leverage

by issuing preferred stock and incurring indebtedness for borrowed money. We may incur additional leverage, directly or indirectly,

through one or more special purpose vehicles, indebtedness for borrowed money, as well as leverage in the form of derivative transactions,

additional shares of preferred stock, debt securities and other structures and instruments, in significant amounts and on terms

that the Adviser and our board of directors deem appropriate, subject to applicable limitations under the 1940 Act. Such leverage

may be used for the acquisition and financing of our investments, to pay fees and expenses and for other purposes. Such leverage

may be secured and/or unsecured. The more leverage we employ, the more likely a substantial change will occur in our NAV. Accordingly,

any event that adversely affects the value of an investment would be magnified to the extent leverage is utilized. The cumulative

effect of the use of leverage with respect to any investments in a market that moves adversely to such investments could result

in a substantial loss that would be greater than if our investments were not leveraged.

The following table is

intended to illustrate the effect of the use of direct leverage on returns from an investment in our common stock assuming various

annual returns, net of expenses. The calculations in the table below are hypothetical and actual returns may be higher or lower

than those appearing in the table below.

| Assumed Return on Our Portfolio (Net of Expenses) |

-10% |

-5% |

0% |

5% |

10% |

| Corresponding return to common stockholder(1) |

-19.24% |

-11.49% |

-3.74% |

4.01% |

11.76% |

Based on our assumed leverage

described above, our investment portfolio would have been required to experience an annual return of at least 2.41% to cover annual

interest payments on our outstanding indebtedness and preferred equity.

Principal Risk Factors

For a description of the

principal risk factors associated with an investment in the Company, please refer to Note 3 to the Financial Statements, “Investments

– Investment Risk Factors”).

Additional

Information

The Company makes certain

unaudited portfolio information available each month on its website in addition to making certain other unaudited financial information

available on its website (www.eaglepointincome.com). This information includes (1) an estimated range of the Company’s net

investment income (“NII”) and realized capital gains or losses per weighted average share of common stock for each

calendar quarter end, generally made available within the first fifteen days after the applicable calendar month end, (2) an estimated

range of the Company’s NAV per share of common stock for the prior month end and certain additional portfolio-level information,

generally made available within the first fifteen days after the applicable calendar month end, and (3) during the latter part

of each month, an updated estimate of NAV, if applicable, and, with respect to each calendar quarter end, an updated estimate of

the Company’s NII and realized capital gains or losses for the applicable quarter, if available.

Information contained on

our website is not incorporated by reference into this Annual Report and you should not consider information contained on our website

to be part of this Annual Report or any other report we file with the SEC.

Forward-Looking Statements

This report may contain

“forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Statements

other than statements of historical facts included in this report may constitute forward-looking statements and are not guarantees

of future performance or results and involve a number of risks and uncertainties. Actual results may differ materially from those

in the forward-looking statements as a result of a number of factors, including those described in the Company’s filings

with the SEC. The Company undertakes no duty to update any forward-looking statement made herein. All forward-looking statements

speak only as of the date of this report.

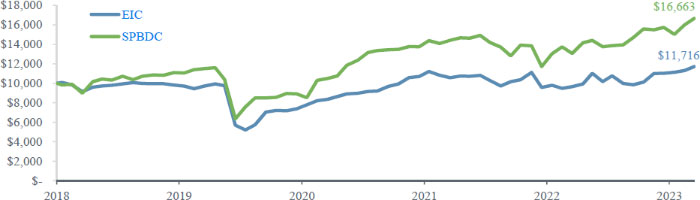

Performance

Data1,2

The

following graph shows the market price performance of a $10,000 investment in the Company’s common shares for the period

from October 16, 2018 (inception) through December 31, 2023. The performance calculation assumes the purchase of Company shares

at net asset value for the beginning of the period (prior to the Company’s public listing) and the sale of Company shares

at the market price at the end of the period. Ending value for each year are as of December 31 of the applicable year. As the

Company’s IPO occurred in July 2019, the value used for the Company’s performance as of December 31, 2018 reflects

the Company’s then-current net asset value per share. For comparative purposes, the performance of a relevant third-party

securities market index, the S&P BDC Index, is shown. Distributions are assumed, for purposes of this calculation, to be reinvested

at prices obtained under the Company’s dividend reinvestment plan. The performance does not reflect brokerage commissions

in connection with the purchase or sale of Company shares, which if included would lower the performance shown. Returns do not

reflect the deduction of taxes that a shareholder would pay on Company distributions or the sale of Company shares.

Past

performance is not indicative of, or a guarantee of, future performance. Future results may vary and may be higher or lower than

the data shown.

| Value

of $10,000 Invested |

| |

Average

Annualized Total Return |

Cumulative

Returns |

| |

1

year |

5

year |

Since

Inception |

Since

Inception |

| EIC |

21.37% |

5.09% |

3.09% |

17.16% |

| S&P

BDC Index |

27.58% |

13.16% |

10.31% |

66.63% |

Summary

of Certain Unaudited Portfolio Characteristics

The

information presented below is on a look–through basis to the collateralized loan obligation, or “CLO”, investments held by the Company as of December 31, 2023 (except as otherwise noted) and reflects the aggregate underlying

exposure of the Company based on the portfolios of those investments. The data is estimated and unaudited and is derived from

CLO trustee reports received by the Company relating to December 2023 and from custody statements and/or other information received

from CLO collateral managers, or other third party sources.

| Summary

of Portfolio Investments (as of 12/31/2023)3 |

| |

|

Cash

and Borrowing Capacity: $11.4 million3 |

| |

| Summary

of Underlying Portfolio Characteristics (as of 12/31/2023)4 |

| Number

of Unique Underlying Loan Obligors |

1,419 |

| Largest

Exposure to an Individual Obligor |

0.73% |

| Average

Individual Loan Obligor Exposure |

0.07% |

| Top

10 Loan Obligors Exposure |

5.57% |

| Currency:

USD Exposure |

100.00% |

| Indirect

Exposure to Senior Secured Loans5 |

97.59% |

| Weighted

Average OC Cushion Senior to the Security6 |

4.34% |

| Weighted

Average Market Value of Loan Collateral |

96.25% |

| Weighted

Average Stated Loan Spread |

3.76% |

| Weighted

Average Loan Rating7 |

B+/B |

| Weighted

Average Loan Maturity |

4.2

years |

| Weighted

Average Remaining CLO Reinvestment Period |

1.2

years |

| Top

10 Underlying Obligors4 |

| Obligor |

%

of Total |

| Asurion |

0.7% |

| Numericable |

0.6% |

| Cablevision |

0.6% |

| Ineos |

0.6% |

| Medline

Industries |

0.6% |

| Virgin

Media |

0.5% |

| Athenahealth |

0.5% |

| Centurylink |

0.5% |

| Transdigm |

0.5% |

| Ultimate

Software Group |

0.5% |

| Total |

5.6% |

| Top

10 Industries of Underlying Obligors4,8,9 |

| Industry |

%

of Total |

| Technology:

Software & Services |

11.1% |

| Media |

6.5% |

| Health

Care Providers & Services |

5.6% |

| Hotels,

Restaurants & Leisure |

4.3% |

| Diversified

Telecommunications Services |

4.0% |

| Commercial

Services & Supplies |

3.9% |

| Diversified

Financial Services |

3.8% |

| Insurance |

3.4% |

| Chemicals |

3.2% |

| Technology:

Hardware & Equipment |

3.0% |

| Total |

48.8% |

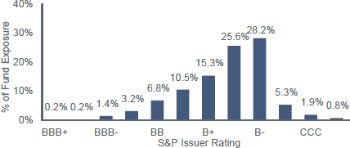

| Rating

Distribution of Underlying Obligors4,7 |

|

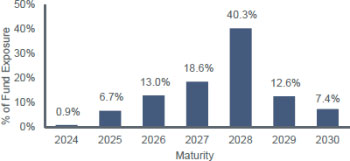

| Maturity

Distribution of Underlying Obligors4 |

|

Notes

| 1 | Based

on the market price. Prices for October 16, 2018 (inception date) and December 31, 2018

represent the Net Asset Value (“NAV”) per share. |

| 2 | The

performance of an index is not an exact representation of any particular investment,

as you cannot invest directly in an index. The indices shown herein have not been selected

to represent a benchmark for a strategy’s performance, but are instead disclosed

to allow for comparison of the Company’s returns to that of known, recognized and/or

similar indices. The S&P

BDC Index is intended to measure the performance of all Business Development Companies

(BDCs) that are listed on the NYSE or NASDAQ and satisfy market capitalization and other

eligibility requirements. Although EIC is not a BDC, BDCs generally invest in high yielding

credit investments, as does EIC. In addition, similar to EIC, BDCs generally elect to

be classified as a regulated investment company under the U.S. Internal Revenue Code

of 1986, as amended, which generally requires an investment company to distribute its

taxable income to shareholders. |

| 3 | The

summary of portfolio investments shown is based on the estimated fair value of the underlying

positions as of December 31, 2023. Cash and borrowing capacity represents cash net of

pending trade settlements and includes available capacity on the Company’s credit

facility as of December 31, 2023. Borrowings under the credit facility are subject to

applicable regulatory and contractual limits. |

| 4 | The

information presented herein is on a look-through basis to the collateralized loan obligation,

or “CLO,” and other related investments held by the Company as of December

31, 2023 (except as otherwise noted) and reflects the aggregate underlying exposure of

the Company based on the portfolios of those investments. The data is estimated and unaudited

and is derived from CLO trustee reports received by the Company relating to December

2023 and from custody statements and/or other information received from CLO collateral

managers and other third-party sources. Information relating to the market price of underlying

collateral is as of month end; however, with respect to other information shown, depending

on when such information was received, the data may reflect a lag in the information

reported. As such, while this information was obtained from third party data sources,

December 2023 trustee reports and similar reports, other than market price, it does not

reflect actual underlying portfolio characteristics as of December 31, 2023 and this

data may not be representative of current or future holdings. The Weighted Average Remaining

Reinvestment Period information is based on the fair value of CLO equity and debt investments

held by the Company at the end of the reporting period. |

| 5 | Data

represents aggregate indirect exposure. We obtain exposure in underlying senior secured

loans indirectly through our CLO and related investments. |

| 6 | The

weighted average OC cushion senior to the security is calculated using the BBB OC cushion

for all BB-rated CLO debt securities in the portfolio and the BB OC cushion for all other

securities in the portfolio, in each case as held on December 31, 2023. |

| 7 | Credit

ratings shown are based on those assigned by Standard & Poor’s Rating Group,

or “S&P,” or, for comparison and informational purposes, if S&P does

not assign a rating to a particular obligor, the weighted average rating shown reflects

the S&P equivalent rating of a rating agency that rated the obligor provided that

such other rating is available with respect to a CLO or related investment held by us.

In the event multiple ratings are available, the lowest S&P rating, or if there is

no S&P rating, the lowest equivalent rating, is used. The ratings of specific borrowings

by an obligor may differ from the rating assigned to the obligor and may differ among

rating agencies. For certain obligors, no rating is available in the reports received

by the Company. Such obligors are not shown in the graphs and, accordingly, the sum of

the percentages in the graphs may not equal 100%. Ratings below BBB- are below investment

grade. Further information regarding S&P’s rating methodology and definitions

may be found on its website (www.standardandpoors.com). |

| 8 | Industry

categories are based on the S&P industry categorization of each obligor as reported

in CLO trustee reports to the extent so reported. Certain CLO trustee reports do not

report the industry category of all of the underlying obligors and where such information

is not reported, it is not included in the summary look-through industry information

shown. As such, the Company’s exposure to a particular industry may be higher than

that shown if industry categories were available for all underlying obligors. In addition,

certain underlying obligors may be re-classified from time to time based on developments

in their respective businesses and/or market practices. Accordingly, certain underlying

borrowers that are currently, or were previously, summarized as a single borrower in

a particular industry may in current or future periods be reflected as multiple borrowers

or in a different industry, as applicable. |

| 9 | Certain

CLO trustee reports do not provide the industry classification for certain underlying

obligors. These obligors are not summarized in the look-through industry data shown;

if they were reflected, they would represent 7.2%. |

Fees

and Expenses (unaudited)

The

following table is intended to assist you in understanding the costs and expenses that an investor in shares of the Company’s

common stock will bear directly or indirectly. The expenses shown in the table under “Annual Expenses” are estimated

based on historical fees and expenses incurred by the Company, as appropriate. In addition, such amounts are based on the

Company’s pro forma assets as of December 31, 2023, which have been adjusted to reflect (i) the issuance in the

Company’s “at-the-market” offering of 1.1 million shares of our common stock and 45,322 shares of our Series B

Preferred Stock from January 1, 2024 through February 15, 2024, yielding net proceeds to the Company of approximately $16.9 million;

(ii) the hypothetical borrowings of the full $25,000,000 available under the BNP Credit Facility, which would mean that the

Company’s adjusted total assets are assumed to equal approximately $269.6 million. As of December 31, 2023, and pro forma for

the issuances and assumed borrowings described above (excluding any regular monthly distributions paid after December 31, 2023), the

Company’s leverage represented approximately 36.7% of the Company’s total assets (less current liabilities). Such

expenses, and actual leverage incurred by the Company, may vary in the future. Whenever this report (or other Company disclosures,

including the Company’s prospectus) contain a reference to fees or expenses paid by the Company, the Company’s common

stockholders will indirectly bear such fees or expenses.

| Stockholder

Transaction Expenses (as a percentage of the offering price): |

|

|

| Sales

load |

|

—%(1) |

| Offering

expenses borne by the Company |

|

—%(2) |

| Dividend

reinvestment plan expenses |

|

Up

to $15(3) |

| Total

stockholder transaction expenses |

|

—% |

| Annual

Expenses (as a percentage of net assets attributable to common stock): |

|

|

| Management

fee |

|

1.94%(4) |

| Interest

payments on borrowed funds |

|

3.74%(5) |

| Other

expenses |

|

1.49%(6) |

| Total

annual expenses |

|

7.17% |

| (5) | “Interest

payments on borrowed funds” represents the Company’s annualized interest

expense and includes dividends payable on the Series A Term Preferred Stock and Series

B Term Preferred Stock, outstanding on December 31, 2023, and includes the pro forma

effect of the Series B Preferred Stock issuance and assumed borrowings under the BNP Credit Facility described above, which,

in the aggregate, have a weighted average interest rate of 6.60% per annum. The Company

may issue additional shares of preferred stock. In the event that the Company were to

issue additional shares of preferred stock, the Company’s borrowing costs, and

correspondingly its total annual expenses, including, |

| in the case of such preferred stock,

the base management fee as a percentage of the Company’s managed assets attributable

to common stock, would increase. |

| (6) | “Other

expenses” includes the Company’s overhead expenses, including payments under

the Administration Agreement based on the Company’s allocable portion of overhead

and other expenses incurred by Eagle Point Administration LLC (“Eagle Point Administration”),

the administrator to the Company and an affiliate of the Adviser, and payment of fees

in connection with outsourced administrative functions, and are based on the actual amounts

for the 2023 fiscal year. See “Related Party Transactions —

Administrator” in the Notes to the Financial Statements. “Other expenses”

also includes the ongoing administrative expenses to the independent accountants and

legal counsel of the Company, compensation of independent directors, and cost and expenses

relating to rating agencies. |

Example

The

following example is furnished in response to the requirements of the SEC and illustrates the various costs and expenses that

you would pay, directly or indirectly, on a $1,000 investment in shares of the Company’s common stock for the time periods

indicated, assuming (1) total annual expenses of 7.17% of net assets attributable to the Company’s common stock and (2) a

5% annual return*:

| |

|

1 year |

|

3 years |

|

5 years |

|

10 years |

|

| You

would pay the following expenses on a $1,000 investment, assuming a 5% annual return |

|

|

$72 |

|

|

$210 |

|

$343 |

|

$651 |

|

*

The example should not be considered a representation of future returns or expenses, and actual returns and expenses may be

greater or less than those shown. The example assumes that the estimated “other expenses” set forth in the

Annual Expenses table are accurate, and that all dividends and distributions are reinvested at NAV. The Company’s actual

rate of return may be greater or less than the hypothetical 5% return shown in the example.

Consolidated

Financial Statements for the Year Ended

December 31, 2023 (Audited)

Eagle

Point Income Company Inc. and Subsidiaries

Consolidated

Statement of Assets and Liabilities

As

of December 31, 2023

(expressed

in U.S. dollars)

| ASSETS | |

| |

| Investments, at fair value (cost $254,810,654) | |

$ | 234,917,292 | |

| Cash and cash equivalents | |

| 944,060 | |

| Interest receivable | |

| 6,895,878 | |

| Receivable for shares of common stock issued pursuant to the Company's dividend reinvestment plan | |

| 144,528 | |

| Excise tax refund receivable | |

| 55,413 | |

| Prepaid expenses | |

| 770,872 | |

| Total Assets | |

| 243,728,043 | |

| | |

| | |

| | |

| | |

| LIABILITIES | |

| | |

| 5.00% Series A Term Preferred Stock due 2026, at fair value under the fair value option (1,521,649 shares outstanding) (Note 6) | |

| 35,241,087 | |

| | |

| | |

| 7.75% Series B Term Preferred Stock due 2028, at fair value under the fair value option (1,372,482 shares outstanding) (Note 6) | |

| 34,243,289 | |

| Unamortized share issuance premium associated with 7.75% Series B Term Preferred Stock due 2028 | |

| 2,932 | |

| 7.75% Series B Term Preferred Stock due 2028, at fair value, plus associated unamortized share issuance premium | |

| 34,246,221 | |

| | |

| | |

| Borrowings under credit facility (less unamortized deferred financing costs of $33,333 (Note 9)) | |

| 14,486,667 | |

| Management fees payable | |

| 706,349 | |

| Tax expense payable | |

| 228,480 | |

| Professional fees payable | |

| 149,039 | |

| Interest expense payable | |

| 143,803 | |

| Directors' fees payable | |

| 127,500 | |

| Administration fees payable | |

| 127,072 | |

| Due to affiliates | |

| 28,072 | |

| Payable for securities purchased | |

| 28,000 | |

| Other expenses payable | |

| 8,333 | |

| Total Liabilities | |

| 85,520,623 | |

| | |

| | |

| COMMITMENTS AND CONTINGENCIES (Note 7) | |

| | |

| | |

| | |

| NET ASSETS applicable to 10,997,398 shares of $0.001 par value common stock outstanding | |

$ | 158,207,420 | |

| | |

| | |

| NET ASSETS consist of: | |

| | |

| Paid-in capital (Note 5) | |

$ | 191,377,889 | |

| Aggregate distributable earnings (losses) | |

| (33,604,689 | ) |

| Accumulated other comprehensive income (loss) | |

| 434,220 | |

| Total Net Assets | |

$ | 158,207,420 | |

| Net asset value per share of common stock | |

$ | 14.39 | |

See accompanying notes to the consolidated financial statements

Eagle

Point Income Company Inc. and Subsidiaries

Consolidated

Schedule of Investments

As

of December 31, 2023

(expressed

in U.S. dollars)

| Issuer

⁽¹⁾ | |

Investment

Description ⁽²⁾ ⁽³⁾ | |

Acquisition

Date ⁽⁴⁾ | |

|

Principal

Amount | |

Cost | | |

Fair

Value ⁽⁵⁾ | | |

%

of Net Assets | |

| Investments, at fair

value | |

| |

| |

|

| |

| | |

| | |

| |

| CLO Debt ⁽⁶⁾ | |

| |

| |

|

| |

| | | |

| | | |

| | |

| Structured Finance | |

| |

| |

|

| |

| | | |

| | | |

| | |

| AGL CLO 12 Ltd. | |

Secured Note - Class E, 11.83%,

(3M SOFR + 6.41%, due 07/20/2034) | |

08/18/2023 | |

$ |

1,500,000 | |

$ | 1,430,634 | | |

$ | 1,444,800 | | |

| 0.91 | % |

| AMMC CLO 24, Limitted | |

Secured Note - Class E, 12.25%, (3M SOFR

+ 6.83%, due 01/20/2035) | |

07/26/2023 | |

|

5,000,000 | |

| 4,664,684 | | |

| 4,788,000 | | |

| 3.03 | % |

| AMMC CLO 25, Limitted | |

Secured Note - Class E, 12.98%, (3M SOFR

+ 7.59%, due 04/15/2035) | |

08/08/2023 | |

|

5,000,000 | |

| 4,735,950 | | |

| 4,885,500 | | |

| 3.09 | % |

| Ares XXXIV CLO Ltd. | |

Secured Note - Class E-R, 12.51%, (3M SOFR

+ 7.11%, due 04/17/2033) | |

08/08/2023 | |

|

1,517,600 | |

| 1,370,691 | | |

| 1,411,368 | | |

| 0.89 | % |

| Ares XLV CLO Ltd. | |

Secured Note - Class E, 11.76%, (3M SOFR

+ 6.36%, due 10/15/2030) | |

05/30/2019 | |

|

800,000 | |

| 790,180 | | |

| 752,960 | | |

| 0.48 | % |

| Barings CLO Ltd. 2018-IV | |

Secured Note - Class E, 11.48%, (3M SOFR

+ 6.08%, due 10/15/2030) | |

10/26/2018 | |

|

840,000 | |

| 836,476 | | |

| 772,296 | | |

| 0.49 | % |

| Battalion CLO XII Ltd. | |

Secured Note - Class E, 11.72%, (3M SOFR

+ 6.35%, due 05/17/2031) | |

10/04/2018 | |

|

5,060,000 | |

| 4,921,180 | | |

| 4,460,896 | | |

| 2.82 | % |

| Battalion CLO XXI Ltd. | |

Secured Note - Class E, 12.12%, (3M SOFR

+ 6.72%, due 07/15/2034) | |

06/08/2022 | |

|

5,000,000 | |

| 4,680,842 | | |

| 4,247,000 | | |

| 2.68 | % |

| Black Diamond CLO 2016-1, Ltd. | |

Secured Note - Class D-R, 11.24%, (3M SOFR

+ 5.86%, due 04/26/2031) | |

10/04/2018 | |

|

1,050,000 | |

| 1,002,793 | | |

| 900,165 | | |

| 0.57 | % |

| Black Diamond CLO 2017-1, Ltd. | |

Secured Note - Class D, 12.26%, (3M SOFR

+ 6.86%, due 04/24/2029) | |

10/04/2018 | |

|

3,600,000 | |

| 3,593,415 | | |

| 3,495,960 | | |

| 2.21 | % |

| Carlyle US CLO 2017-1, Ltd. | |

Secured Note - Class D, 11.68%, (3M SOFR

+ 6.26%, due 04/20/2031) | |

09/15/2020 | |

|

2,000,000 | |

| 1,720,927 | | |

| 1,744,200 | | |

| 1.10 | % |

| Carlyle US CLO 2018-1, Ltd. | |

Secured Note - Class D, 11.43%, (3M SOFR

+ 6.01%, due 04/20/2031) | |

10/04/2018 | |

|

665,000 | |

| 660,021 | | |

| 602,091 | | |

| 0.38 | % |

| Carlyle US CLO 2018-2, Ltd. | |

Secured Note - Class D, 10.91%, (3M SOFR

+ 5.51%, due 10/15/2031) | |

10/04/2018 | |

|

5,500,000 | |

| 5,337,175 | | |

| 4,985,750 | | |

| 3.15 | % |

| Carlyle US CLO 2019-1, Ltd. | |

Secured Note - Class D, 12.38%, (3M SOFR

+ 6.96%, due 04/20/2031) | |

08/19/2019 | |

|

3,125,000 | |

| 2,984,784 | | |

| 2,944,375 | | |

| 1.86 | % |

| CIFC Funding 2015-I, Ltd. | |

Secured Note - Class E-RR, 11.67%, (3M SOFR

+ 6.26%, due 01/22/2031) | |

10/04/2018 | |

|

5,000,000 | |

| 4,769,385 | | |

| 4,754,000 | | |

| 3.00 | % |

| CIFC Funding 2018-II, Ltd. | |

Secured Note - Class D, 11.53%, (3M SOFR

+ 6.11%, due 04/20/2031) | |

10/04/2018 | |

|

1,225,000 | |

| 1,196,576 | | |

| 1,181,880 | | |

| 0.75 | % |

| CIFC Funding 2018-III, Ltd. | |

Secured Note - Class E, 11.16%, (3M SOFR

+ 5.76%, due 07/18/2031) | |

08/16/2023 | |

|

4,750,000 | |

| 4,418,098 | | |

| 4,539,100 | | |

| 2.87 | % |

| CIFC Funding 2018-IV, Ltd. | |

Secured Note - Class E, 13.36%, (3M SOFR

+ 7.96%, due 10/17/2031) | |

05/22/2019 | |

|

2,000,000 | |

| 1,885,116 | | |

| 1,662,600 | | |

| 1.05 | % |

| CIFC Funding 2019-II, Ltd. | |

Secured Note - Class E-R, 12.25%, (3M SOFR

+ 6.85%, due 04/17/2034) | |

08/03/2023 | |

|

2,650,000 | |

| 2,603,625 | | |

| 2,650,000 | | |

| 1.68 | % |

| CIFC Funding 2019-V, Ltd. | |

Secured Note - Class D-R, 12.44%, (3M SOFR

+ 7.04%, due 01/15/2035) | |

08/03/2023 | |

|

950,000 | |

| 933,817 | | |

| 942,020 | | |

| 0.60 | % |

| CIFC Funding 2021-III, Ltd. | |

Secured Note - Class E-1, 12.06%, (3M SOFR

+ 6.66%, due 07/15/2036) | |

08/18/2023 | |

|

3,750,000 | |

| 3,651,563 | | |

| 3,704,250 | | |

| 2.34 | % |

| Cook Park CLO, Ltd. | |

Secured Note - Class E, 11.06%, (3M SOFR

+ 5.66%, due 04/17/2030) | |

10/04/2018 | |

|

1,250,000 | |

| 1,203,574 | | |

| 1,068,125 | | |

| 0.68 | % |

| Dryden 37 Senior Loan Fund, Ltd. | |

Secured Note - Class E-R, 10.81%, (3M SOFR

+ 5.41%, due 01/15/2031) | |

10/04/2018 | |

|

500,000 | |

| 486,553 | | |

| 408,100 | | |

| 0.26 | % |