UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

(Rule 14a-101)

Information Required in Proxy Statement

Schedule 14A Information

Proxy Statement Pursuant to Section 14(a) of the Securities Exchange Act of 1934

(Amendment No. )

Filed by the Registrant ý

Filed by a Party other than the Registrant ☐

Check the appropriate box:

| | | | | |

| ☐ | Preliminary Proxy Statement |

| ☐ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

| ☐ | Definitive Proxy Statement |

| ý | Definitive Additional Materials |

| ☐ | Soliciting Material Pursuant to §240.14a-12 |

EVERTEC, Inc.

(Name of Registrant as Specified In Its Charter)

(Name of Person(s) Filing Proxy Statement, if other than the Registrant)

Payment of Filing Fee (Check the appropriate box):

| | | | | |

| ý | No fee required. |

| ☐ | Fee paid previously with preliminary materials. |

| ☐ | Fee computed on table in exhibit required per Item 25(b) per Exchange Act Rules 14a-6(i)(1) and 0-11. |

EVERTEC, INC.

SUPPLEMENT TO THE DEFINITIVE PROXY STATEMENT

FOR THE ANNUAL MEETING OF STOCKHOLDERS TO BE HELD ON MAY 23, 2024

May 13, 2024

Dear Evertec Stockholders:

On behalf of the Board of Directors of Evertec, Inc. (“Evertec”, the “Company”, “we”, “us”, or “our”) we are writing to encourage you to vote “FOR” Proposal 2 – Advisory vote on executive compensation for our named executive officers (also known as the Say-on-Pay (“SOP”) Proposal), at the Company’s 2024 Annual Meeting of Stockholders, which will be held virtually on Thursday, May 23, 2024.

It has come to our attention that concerns have been expressed by certain proxy advisory firms regarding our 2023 compensation program. Evertec is committed to strong governance and pay-for-performance results as evidenced by our 97.55% average SOP support level over a 9-year period since 2015, the first year we were subject to a SOP vote since becoming a public company.

In an effort to provide you with a complete picture, context, and thorough understanding of the decisions and rationale employed by our Board and Compensation Committee (the “Committee”) regarding the Company’s compensation program during 2023 we will address the following items:

•The special long-term retention grant to Mr. Schuessler, our Chief Executive Officer (“CEO”), and commitment to not grant additional special retention or one-time awards to Mr. Schuessler for the duration of the existing retention grant (i.e., approximately 4 years)

•Further context regarding Evertec’s incentive goal-setting process for fiscal year 2023 and historic approach to a robust performance evaluation process

•Institutional Shareholder Services (“ISS”) peer group selection and corresponding CEO pay levels for the current and past ISS peer groups, which drive the ISS Pay-for-Performance quantitative test results

•Rationale for the long-term incentive design at Evertec which has been in place for the last eight years

1. Special Long-Term Retention Grant for Our CEO

The Committee approved a one-time special long-term retention grant of RSUs valued at $6,000,000 for Mr. Schuessler in December 2023, which was a critical juncture for our Company, having just announced the largest acquisition in our Company’s history, Sinqia S.A. Successful integration of this business is essential to the future growth and expansion of our footprint in Latin America. The RSUs will cliff vest on the fourth anniversary of grant, subject to continued service.

During this time period, the Board discussed the existing holding power associated with outstanding awards currently held by Mr. Schuessler in the context of an extremely active marketplace for high caliber executive talent in our industry. Understanding the importance of a cohesive and intact leadership team for the foreseeable future, the Committee determined that a special one-time award to the CEO would help protect the Company and its shareholders and properly incentivize Mr. Schuessler to remain as the Company’s CEO and ensure his continued leadership of the Company.

In structuring the size and design of the award, the Committee discussed adding performance conditions to the award such as deal synergies and other strategic initiatives. Ultimately, the Committee felt deal-related metrics would be more subjective, resulting in potentially greater scrutiny and questions around the awards construct when the primary goal was Mr. Schuessler’s retention for at least the next four years. To bolster the Company’s retention efforts, the Committee placed stringent cliff vesting conditions on the award, well outside vesting associated with Evertec’s normal annual equity grant practices and those found among the Company’s peers. The size of the award was designed to be roughly equal to 1x Mr. Schuessler’s annual Long-Term Incentive (“LTI”) opportunity which represented a meaningful increase in his holding power and is generally aligned with market data for such awards as provided by the Committee’s independent outside compensation consultant.

The Committee did not take this decision lightly as governance remains at the forefront of its decision-making process. Evertec has exhibited a strong commitment to compensation “best practices” and has only granted one-time or special

awards in extraordinary circumstances, the last coming in November 2017 in response to the devastation caused by Hurricane Maria.

To further alleviate concerns regarding pay opportunities for Mr. Schuessler, the Committee is committed to not issuing any additional special awards to Mr. Schuessler for the duration of the existing retention award (i.e., no special awards over the next four years – December 6, 2027).

2. Fiscal Year 2023 Incentive Plan Goal Setting

In their report, ISS raised goal rigor concerns because the adjusted net income (“ANI”) target for the 2023 short-term incentive plan was set below the prior year’s target and actual results and were earned above target, and similarly the adjusted EBITDA target for the 2023 LTI performance based RSUs was set below the prior year’s actual performance.

Some historical (and future) perspective is of value when analyzing the Company’s commitment to rigorous goal setting. The Committee and the Board undertake a comprehensive budget process at the start of each year that is driven by a multitude of factors including real-time economic conditions and business circumstances. This robust process helps shape the Company’s annual budget, incentive goals, and external guidance to investors.

To fully understand the basis for the goals set in 2023 and how they compare to the previous year’s actual performance, it is key to consider the transaction with Popular, Inc. (“Popular”) that was completed in 2022 and the financial impacts of this transaction to the second half of 2022 and full year 2023. For context, Popular is our largest customer and before July 2022 represented approximately 40% of our total revenues and was our largest shareholder. Popular engages with Evertec through three main agreements with original end dates of September 2025. In July 2022, we completed a transaction with Popular that meaningfully extended all three of these agreements and included a revenue share component that created better alignment with our biggest customer. The transaction also included provisions for Popular to ensure the Company was no longer deemed a “subsidiary” of Popular for purposes of the Bank Holding Company Act, allowing for greater flexibility to execute on our diversification strategy through M&A. Additionally, we sold certain technology assets to Popular in exchange for approximately 4.6 million shares of the Company that were owned by Popular and subsequently retired by the Company.

The outcome of this key transaction was considered a success given the importance of this relationship for the future of the Company, but it came with specific financial effects that negatively impacted our 2023 results and goals when compared to 2022. The technology assets sold to Popular generated approximately $30 million in annualized revenues at above average margins for Evertec and the inclusion of the revenue share translates into an incremental expense to Evertec that negatively impacted margins. These impacts were clearly communicated to our shareholders and expected as part of our 2023 financial performance. Thus, it was under this context and these business circumstances that the Board adopted the corporate performance targets to be used for the annual cash incentive and the long-term incentive grant for compensation year 2023.

Below is a table that illustrates the relationship between target financial goals within the Company’s incentive plans and actual achievement for each of the past four years. As illustrated below, the Company’s targets for all metrics (revenues, ANI, adjusted EBITDA) have consistently been higher than the previous year’s target and actual performance except for the years 2022 and 2023 where the financial considerations of the transaction with Popular mentioned previously were considered.

Of note, Evertec’s one-year Total Shareholder Return (“TSR”) for 2023 was 27.15%, significantly outperforming our four digit GICS code 4020 of 19.99% and ahead of the broader market Russell 3000 of 25.96%. We are proud of our performance in 2023 and believe our compensation for 2023 is well aligned with the performance and value delivered to our shareholders.

To further mitigate concerns about goal rigor, the Company can affirm that current FY 24 targets under both our annual incentive plan and long-term incentive plan (as approved by the Committee in February 2024) are at levels that exceed our prior FY 23 target and actual performance. Full disclosure of these goals and ultimate earnouts will be provided in next year’s proxy statement. Taking into account the current FY 24 targets, the Company has set current year revenue goals above prior actuals in each of the last six years, and for adjusted net income and adjusted EBITDA in four of the last six years, due to the impact described above for FY 22 and FY 23.

3. Peer Group Selection

The Committee allocates considerable time and effort each year to reviewing and approving the Company’s compensation peer group. Please see the CD&A at page 26 of the Proxy Statement for a detailed discussion of the factors considered and list of companies used to make NEO compensation decisions in 2023.

Evertec understands that proxy advisory firms may have varying approaches to determining compensation peer groups and we respect their process. However, a core tenet of well-established benchmarking practices is stability in a peer group, as significant changes to peer constituents can result in disproportionate and potentially misleading swings in compensation statistics year-over-year.

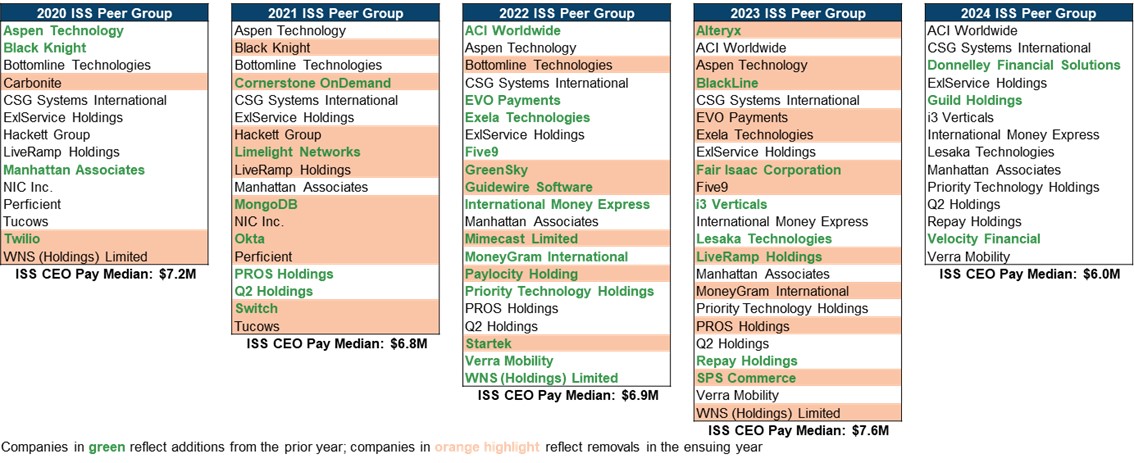

The following table provides the list of compensation peers used by ISS in its research reports issued for Evertec over the past five years and the corresponding level of median CEO pay that ISS disclosed. In particular, we are concerned by the significant adjustments to the peer group in the most recent year with ISS shrinking the peer size from 23 companies to 14 companies (40% reduction in peer group size) through the removal of more than half of the existing ISS peers (12) and the addition of three new companies. This material change in the peer construct resulted in a greater than 30% reduction in CEO peer compensation year-over-year. Such an extreme movement in CEO compensation does not align with any recent publicly available trend data or our direct experiences with the labor markets in which we compete for talent.

It is important for investors to understand that the preliminary conclusions reached by the major advisory firms are driven largely by quantitative tests tied to these self-selected peer groups that evaluate CEO pay (primarily) and Company performance as defined by TSR over multiple time periods. For the last five years, we have scored “Low Concern” on ISS’s three core quantitative tests and believe we would have done so again if not for the material changes to the peer group which materially disadvantaged the Company.

4. 2023 Long-Term Incentive Design

The Committee believes the compensation packages provided to our executives, including our CEO, should include both cash and equity-based incentives that reward performance against established business goals and that discourage management from taking unnecessary and/or excessive risks that may harm the Company. The Committee has consciously structured compensation opportunities such that the weighting of long-term incentives increases as an executive moves up in level within the organization. This philosophy is also true of the weighting within the long-term incentive component allocated to performance-based awards versus time-based awards as shown below:

The Committee strongly believes our CEO, Mr. Schuessler, should have a compensation package that is closely tied to the Company’s long-term performance, with performance-based awards comprising a significant majority of that value (65%).

Some concerns have been expressed regarding the structure of our performance-based awards. Our performance-based RSU design, which has remained unchanged since 2017, is linked to both an absolute financial metric and a relative stock-based metric. We believe this balance provides an appropriate forum to evaluate management’s performance on a core

earnings-based metric that is followed closely by our investors (Adjusted EBITDA) while also calibrating to the experiences of our shareholders during the performance period through the use of a relative TSR modifier. The Adjusted EBITDA goal is tied to one-year performance (with a two-year service requirement after the performance period) while the TSR modifier is tied to three-year performance relative to the constituents of the Russell 2000 Index.

Given the dynamic nature of our industry and associated challenges with setting multi-year financial goals, we believe the above approach with a combination of a 1-year financial goal and 3-year relative TSR goal allows for appropriate goal setting and aligns pay and performance. Below is a summary of the last four completed performance-based RSU awards and the corresponding TSR delivered during those periods which further proves that our program is working as entitled (i.e., rewarding management and shareholders for periods of outperformance and holding management accountable for periods of underperformance).

In summary, we strongly encourage our shareholders to vote “FOR” the advisory vote on executive compensation and all other agenda items in accordance with the recommendation of our Board of Directors.

On behalf of the Board and the Evertec team, we thank you for your continued investment in Evertec and support. We look forward to continuing to build on the strength of our leadership team and growth initiatives as we expand our product portfolio throughout the Americas.

Sincerely,

Frank D’Angelo

Independent Chairman of the Board

Chairman of the Compensation Committee

Evertec (NYSE:EVTC)

과거 데이터 주식 차트

부터 4월(4) 2024 으로 5월(5) 2024

Evertec (NYSE:EVTC)

과거 데이터 주식 차트

부터 5월(5) 2023 으로 5월(5) 2024