false

0001984060

0001984060

2025-01-27

2025-01-27

iso4217:USD

xbrli:shares

iso4217:USD

xbrli:shares

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 8-K

CURRENT REPORT

PURSUANT TO SECTION 13 OR 15(D)

OF THE SECURITIES EXCHANGE ACT OF 1934

Date of report (Date of earliest event reported):

January 27, 2025

ATLAS ENERGY SOLUTIONS INC.

(Exact Name of Registrant as Specified in Charter)

| Delaware |

|

001-41828 |

|

93-2154509 |

(State or other jurisdiction

of incorporation) |

|

(Commission

File Number) |

|

(I.R.S. Employer

Identification Number) |

5918 W. Courtyard Drive, Suite 500

Austin, Texas 78730

(Address of Principal Executive Offices) (Zip

Code)

(512) 220-1200

(Registrant’s Telephone Number, Including Area Code)

Check the appropriate box below if the Form 8-K filing is intended

to simultaneously satisfy the filing obligation of the registrant under any of the following provisions:

| ¨ |

Written communication pursuant to Rule 425 under the Securities Act (17 CFR 230.425) |

| ¨ |

Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) |

| ¨ |

Pre-commencement communication pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) |

| ¨ |

Pre-commencement communication pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) |

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class |

|

Trading

Symbol(s) |

|

Name of each exchange

on which registered |

| Common Stock |

|

AESI |

|

NYSE |

Indicate by check mark whether the registrant is an emerging growth

company as defined in Rule 405 of the Securities Act of 1933 (§ 230.405 of this chapter) or Rule 12b-2 of the Securities

Exchange Act of 1934 (§ 240.12b-2 of this chapter).

Emerging growth company ¨

If an emerging growth company, indicate

by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial

accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

| Item 2.02. | Results of Operations and Financial Condition. |

To the extent the information included or incorporated into Item 7.01

below with respect to the results of operations or financial condition of Atlas Energy Solutions Inc. (“Atlas” or the “Company”)

relates to or is presented as of or for a completed fiscal period, such information is incorporated into this Item 2.02 by reference herein.

| Item 7.01. | Regulation FD Disclosure. |

On January 27, 2025, the Company issued a press release

announcing entry into a Stock Purchase Agreement by and among Wyatt Holdings, LLC, a Delaware limited liability company and

wholly-owned subsidiary of the Company (the “Purchaser”), Moser Holdings, LLC, a Delaware limited liability company (the

“Seller”), and for the limited purposes set forth therein, the Company (together with the Purchaser and the Seller, the

“Parties”), pursuant to which the Purchaser will acquire (i) 100% of the authorized, issued and outstanding equity

ownership interests in Moser Acquisition, Inc., a Delaware corporation and wholly-owned subsidiary of the Seller (“Moser

AcquisitionCo”), and (ii) Moser Engine Service, Inc. (d/b/a Moser Energy Systems), a Wyoming corporation and a

wholly-owned subsidiary of Moser AcquisitionCo (such transaction, the “Moser Acquisition”).

Also on January 27, 2025, the Company made available an investor

presentation related to the Moser Acquisition. Copies of the press release and the investor presentation are attached hereto as Exhibit 99.1

and Exhibit 99.2, respectively, and incorporated into this Item 7.01 by reference.

The information in this Item 7.01, including Exhibit 99.1 and

Exhibit 99.2, is being “furnished” pursuant to General Instruction B.2 of Form 8-K and shall not be deemed to be

“filed” for purposes of Section 18 of the Securities Exchange Act of 1934, as amended (the “Exchange Act”)

or otherwise subject to the liabilities of that section, nor shall it be deemed incorporated by reference into any filing under the Securities

Act, except as shall be expressly set forth in such filing.

In connection with the Moser

Acquisition, the Company is filing certain updated risk factors disclosure, attached hereto as Exhibit 99.3, applicable to its business

for the purpose of supplementing and updating disclosures contained in the Company’s prior public filings, including those discussed

under the heading “Item 1A. Risk Factors” in the Company’s Annual Report on Form 10-K for the year ended December 31, 2023, filed with the U.S. Securities and Exchange Commission (the “SEC”) on February 27, 2024, which is incorporated

by reference herein.

Forward-Looking Statements

This Current Report contains

forward-looking statements within the meaning of Section 27A of the Securities Act, and Section 21E of the Exchange Act. Statements

that are predictive or prospective in nature, that depend upon or refer to future events or conditions or that include the words “may,”

“assume,” “forecast,” “position,” “strategy,” “potential,” “continue,”

“could,” “will,” “plan,” “project,” “budget,” “predict,” “pursue,”

“target,” “seek,” “objective,” “believe,” “expect,” “anticipate,”

“intend,” “estimate” and other expressions that are predictions of or indicate future events and trends and that

do not relate to historical matters identify forward-looking statements. Examples of forward-looking statements include, but are not limited

to, statements about the anticipated financial performance of Atlas following the Moser Acquisition; the expected synergies and efficiencies

to be achieved as a result of the Moser Acquisition; expected accretion to Adjusted EBITDA; expected production volumes; expectations

regarding the leverage and dividend profile of Atlas following the Moser Acquisition; expansion and growth of Atlas’s business;

Atlas’s plans to finance the Moser Acquisition; and the receipt of all necessary approvals to close the Moser Acquisition and the

timing associated therewith; our business strategy, our industry, our future operations and profitability, expected capital expenditures

and the impact of such expenditures on our performance, statements about our financial position, production, revenues and losses, our

capital programs, management changes, current and potential future long-term contracts and our future business and financial performance.

Although forward-looking statements

reflect our good faith beliefs at the time they are made, we caution you that these forward-looking statements are subject to a number

of risks and uncertainties, most of which are difficult to predict and many of which are beyond our control. These risks include but are

not limited to: the completion of the Moser Acquisition on anticipated terms and timing or at all, including obtaining any required governmental

or regulatory approval and satisfying other conditions to the completion of the Moser Acquisition; uncertainties as to whether the Moser

Acquisition, if consummated, will achieve its anticipated benefits and projected synergies within the expected time period or at all;

Atlas’s ability to integrate Moser’s operations in a successful manner and in the expected time period; the occurrence of

any event, change, or other circumstance that could give rise to the termination of the Moser Acquisition; risks that the anticipated

tax treatment of the Moser Acquisition is not obtained; potential litigation relating to the Moser Acquisition; the possibility that the

Moser Acquisition may be more expensive to complete than anticipated, including as a result of unexpected factors or events; the effect

of the announcement, pendency, or completion of the Moser Acquisition on the Parties’ business relationships and business generally;

risks that the Moser Acquisition disrupts current plans and operations of Atlas or Moser and their respective management teams and potential

difficulties in retaining employees as a result of the Moser Acquisition; the risks related to Atlas’s financing of the Moser Acquisition;

potential negative effects of this announcement and the pendency or completion of the Moser Acquisition on the market price of Atlas’s

common stock or operating results; uncertainty regarding the ultimate cost and time needed to execute the desired process improvements

at our production facilities; unexpected future capital expenditures; unforeseen or unknown liabilities; our ability to successfully execute

our stock repurchase program or implement future stock repurchase programs; commodity price volatility, including volatility stemming

from the ongoing armed conflicts between Russia and Ukraine and Israel and Hamas; increasing hostilities and instability in the Middle

East; adverse developments affecting the financial services industry; our ability to complete growth projects on time and on budget; the

risk that stockholder litigation in connection with our recent corporate reorganization may result in significant costs of defense, indemnification

and liability; changes in general economic, business and political conditions, including changes in the financial markets; transaction

costs; actions of OPEC+ to set and maintain oil production levels; the level of production of crude oil, natural gas and other hydrocarbons

and the resultant market prices of crude oil; inflation; environmental risks; operating risks; regulatory changes; lack of demand; market

share growth; the uncertainty inherent in projecting future rates of reserves; production; cash flow; access to capital; the timing of

development expenditures; the ability of our customers to meet their obligations to us; our ability to maintain effective internal controls;

and other factors discussed or referenced in our filings made from time to time with the SEC, including those discussed under the heading

“Risk Factors” in our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K

and those disclosed in Exhibit 99.3 filed herewith. Readers are cautioned not to place undue reliance on forward-looking statements,

which speak only as of the date hereof. Factors or events that could cause our actual results to differ may emerge from time to time,

and it is not possible for us to predict all of them. We undertake no obligation to publicly update or revise any forward-looking statement,

whether as a result of new information, future developments or otherwise, except as may be required by law. Atlas’s SEC filings

are or will be available publicly on the SEC’s website at www.sec.gov.

| Item 9.01. | Financial Statements and Exhibits. |

(d) Exhibits

SIGNATURE

Pursuant to the requirements

of the Securities Exchange Act of 1934, the Company has duly caused this report to be signed on its behalf by the undersigned hereunto

duly authorized.

Date: January 27, 2025

| |

ATLAS ENERGY SOLUTIONS INC. |

| |

|

|

| |

By: |

/s/ John Turner |

| |

Name: |

John Turner |

| |

Title: |

President and Chief Executive Officer |

Exhibit 99.1

Atlas Energy Solutions Inc. Announces Agreement to Acquire Moser

Energy Systems

and Provides Preliminary Fourth Quarter and

Year-End 2024 Results

Austin, TX – January 27, 2025 –

Atlas Energy Solutions Inc. (NYSE: AESI) (“Atlas” or the “Company”) today announced that it has entered into

a definitive agreement to acquire all of the outstanding capital stock of Moser Acquisition, Inc. (“Moser Energy Systems”

or “Moser”), a leading provider of distributed power solutions, in a transaction valued at $220 million (the “Moser

Acquisition”).

The transaction consideration includes $180 million

of cash and approximately 1.7 million shares (the “Stock Consideration”) of the Company’s common stock, par value $0.01

per share, which are valued at $40.0 million based on the 20-day trailing volume-weighted average price ending at the close of trading

on Friday, January 24, 2025. Atlas has the ability to elect to pay the aggregate transaction consideration in cash in lieu of Atlas’s

issuance of the Stock Consideration (the “Cash Option”). The final consideration mix will be determined at closing and the

Stock Consideration is subject to revision for customary post-closing adjustments. Following closing, if the Cash Option has not been

exercised, all or any portion of the Stock Consideration will be subject to redemption at the option of Atlas, with any such redemption

to be paid in cash.

Acquisition Highlights

| · | The combination of Atlas’s completion platform

and Moser’s distributed power platform creates an innovative, diversified energy solutions provider with a leading portfolio of

proppant, logistics (including the Dune Express) and distributed power solutions. |

| · | Dynamic fleet of natural gas-powered assets (~212MWs)

expands Atlas’s current operations into production and distributed power end markets supported by strong macro tailwinds expected

to reduce through-cycle volatility associated with completions operations. |

| · | Moser’s

strong EBITDA(1) margin profile of 50%+ and robust cash flow generation is expected to

enhance Atlas’s pro forma cash flow generation and shareholder returns. |

| · | Adds

critical, differentiated in-house manufacturing and remanufacturing capabilities driving best-in-class quality and reliability while

reducing through-cycle maintenance and equipment replacement costs. |

| · | Increases Atlas’s customer reach with a

vital power service offering in Atlas’s core geography, the Permian Basin, while providing geographic diversity with operating locations

in key oil and gas basins across the central United States. |

| · | Estimated to be immediately accretive. |

| · | Assuming 10-months of contribution, we expect

the acquired assets to generate $40-45 million in Adjusted EBITDA(1) in 2025, which implies on a full run-rate basis

a valuation of approximately 4.3x 2025 Adjusted EBITDA(1). |

| · | The transaction is expected to close before the

end of the first quarter of 2025. |

1 EBITDA and Adjusted EBITDA are non-GAAP financial

measures. See Non-GAAP Financial Measures for a discussion of these measures and a reconciliation of estimated 2024 Adjusted EBITDA to

our most directly comparable financial measures calculated and presented in accordance with GAAP.

John Turner, President and Chief Executive Officer

of Atlas, commented, “Today marks yet another exciting milestone for Atlas. This acquisition diversifies the Company into attractive

high-growth end markets in both production and distributed power while strengthening Atlas’s current market position as a leading

provider of energy solutions within the oil and gas sector across North America. This transaction highlights our continued commitment

to evolve our organization by deploying innovative and differentiated solutions to return value to our shareholders. We are looking forward

to continuing to invest in our current operations and expand the capabilities of our distributed power platform.”

“When we made our original investment in Moser, we saw a company

with tremendous potential and a rich legacy of customer service and excellence that Randy Moser and his family had built over the previous

40 years. We have worked hard to be good caretakers of that legacy as we have grown the business, and we view Atlas Energy as the perfect

company to further build upon that legacy,” said Mark Plunkett, Managing Partner of Hilltop Opportunity Partners. “We have

greatly valued the partnership we have had with the Moser team over the last several years and look forward to watching them thrive as

they lead Moser into this next chapter with Atlas.”

Transaction Financing

At closing, Atlas will fund $180 million of cash

and 1.7 million shares of Atlas common stock, subject to the Cash Option, to Moser’s sole shareholder. Atlas has secured funding for the cash portion of the consideration,

including the Cash Option, if exercised, through an upsizing amendment to its existing delayed draw term loan facility.

Transaction Timing and Approvals

Atlas’s Board of Directors has approved

the Moser Acquisition. The transaction is subject to customary closing conditions and the Company expects the transaction to close by

the end of the first quarter of 2025.

Preliminary Fourth Quarter and Year-End 2024

Results

Set forth below are certain estimated preliminary

unaudited financial results and other data for the fourth quarter ended December 31, 2024 and the corresponding period of the prior

fiscal year, as well as fiscal year ended December 31, 2024 and the corresponding period of the prior fiscal year. Our unaudited

interim consolidated financial statements for the fourth quarter ended December 31, 2024 and fiscal year ended December 31,

2024 are not yet available. These ranges are based on the information available to us as of the date of this release. These are forward-looking

statements and may differ from actual results. We have provided ranges, rather than specific amounts, because these results are preliminary

and subject to change. Our actual results may vary from the estimated preliminary results presented below due to the completion of our

financial closing and other operational procedures, final adjustments and other developments that may arise between now and the time the

financial results for the fourth quarter ended December 31, 2024 and fiscal year ended December 31, 2024 are finalized.

These estimates should not be viewed as a

substitute for our full interim or annual audited financial statements prepared in accordance with U.S. generally accepted

accounting principles (“GAAP”). Accordingly, you should not place undue reliance on this preliminary data. See

“Cautionary Statement Regarding Forward-Looking Statements” below for additional information regarding factors that

could result in differences between the preliminary estimated ranges of our financial and other data presented below and the actual

financial and other data we will report for the fourth quarter ended December 31, 2024 and fiscal year ended December 31,

2024.

The estimated preliminary financial results for

the fourth quarter ended December 31, 2024 and fiscal year ended December 31, 2024 have been prepared by, and are the responsibility

of, management. Our independent registered public accounting firm, Ernst & Young LLP, has not audited, reviewed, compiled or

performed any procedures with respect to the estimated preliminary financial results. Accordingly, Ernst & Young LLP does not

express an opinion or any other form of assurance with respect thereto.

For the fourth quarter ended December 31,

2024, we expect:

| · | Revenue to be between $270.0 million and $272.0

million, as compared to revenue of approximately $141.1 million for the fourth quarter ended December 31, 2023, an increase of approximately

92% at the midpoint. |

| · | Gross profit to be between $49.0 million and

$51.0 million, as compared to gross profit of $62.9 million for the fourth quarter

ended December 31, 2023, a decrease of approximately 21% at the midpoint. |

| · | Adjusted EBITDA(1) to be between

$62.2 million and $64.2 million, as compared to Adjusted EBITDA(1) of $68.7 million for the fourth quarter ended December 31,

2023, a decrease of approximately 8% at the midpoint. |

For the fiscal year ended December 31, 2024,

we expect:

| · | Revenue to be between $1,055.0 million and $1,057.0

million, as compared to revenue of $614.0 million for the fiscal year ended

December 31, 2023, an increase of approximately 72% at the midpoint. |

| · | Gross profit to be between $231.0 million and

$233.0 million, as compared to gross profit of $313.8 million for the fiscal year ended

December 31, 2023, a decrease of approximately 26% at the midpoint. |

| · | Adjusted EBITDA(1) to be between

$287.9 million and $289.9 million, as compared to Adjusted EBITDA(1) of $329.7 million for the fiscal year ended December 31,

2023, a decrease of approximately 12% at the midpoint. |

| · | Cash and cash equivalents to total approximately

$71.7 million, as compared to cash and cash equivalents of $210.2 million at December 31, 2023, a decrease of approximately 66%. |

Advisors

Piper Sandler & Co. is serving as

exclusive financial advisor to Atlas. Vinson & Elkins L.L.P. is serving as legal advisor to Atlas in association with the

transaction.

TPH&Co., the energy business of Perella Weinberg Partners, is serving as exclusive financial advisor to Moser. Katten Muchin Rosenman LLP is serving as legal advisor in association with the transaction.

Conference Call

The Company will

host a conference call to discuss the transaction on January 27, 2025 at 9:00am Central Time (10:00am Eastern Time). Individuals

wishing to participate in the conference call should dial (877) 407-4133. A live webcast will be available at https://ir.atlas.energy/.

Please access the webcast or dial in for the call at least 10 minutes ahead of the start time to ensure a proper connection. An archived

version of the conference call will be available on the Company’s website shortly after the conclusion of the call.

The Company will also post an updated

investor presentation titled “Moser Acquisition Presentation” at https://ir.atlas.energy/ in the “Presentations”

section under “News & Events” tab on the Company’s Investor Relations webpage prior to the conference

call.

About Atlas Energy Solutions

Atlas Energy Solutions Inc. is a leading proppant

producer and proppant logistics provider, serving primarily the Permian Basin of West Texas and New Mexico. We operate 14 proppant production

facilities across the Permian Basin with a combined annual production capacity of 29 million tons, including both large-scale in-basin

facilities and smaller distributed mining units. We manage a portfolio of leading-edge logistics assets, which includes our 42-mile Dune

Express conveyor system. In addition to our conveyor infrastructure, we manage a fleet of over 120 trucks, which are capable of delivering

expanded payloads due to our custom-manufactured trailers and patented drop-depot process. Our approach to managing both our proppant

production and proppant logistics operations is intently focused on leveraging technology, automation and remote operations to drive efficiencies.

We are a low-cost producer of various high-quality,

locally sourced proppants used during the well completion process. We offer both dry and damp sand, and carry various mesh sizes including

100 mesh and 40/70 mesh. Proppant is a key component necessary to facilitate the recovery of hydrocarbons from oil and natural gas wells.

Our logistics platform is designed to increase

the efficiency, safety and sustainability of the oil and natural gas industry within the Permian Basin. Proppant logistics is increasingly

a differentiating factor affecting customer choice among proppant producers. The cost of delivering sand, even short distances, can be

a significant component of customer spending on their well completions given the substantial volumes that are utilized in modern well

designs.

We continue to invest in and pursue leading-edge

technologies, including autonomous trucking, digital infrastructure, and artificial intelligence, to support opportunities to gain efficiencies

in our operations. These technology-focused investments aim to improve our cost structure and also combine to produce beneficial environmental

and community impacts.

While our core business is fundamentally aligned

with a lower emissions economy, our core obligation has been, and will always be, to our stockholders. We recognize that maximizing value

for our stockholders requires that we optimize the outcomes for our broader stakeholders, including our employees and the communities

in which we operate. We are proud of the fact that our approach to innovation in the hydrocarbon industry while operating in an environmentally

responsible manner creates immense value. Since our founding in 2017, our core mission has been to improve human beings’ access

to the hydrocarbons that power our lives while also delivering differentiated social and environmental progress. Our Atlas team has driven

innovation and has produced industry-leading environmental benefits by reducing energy consumption, emissions, and our aerial footprint.

We call this Sustainable Environmental and Social Progress.

We were founded in 2017 by Ben M. “Bud”

Brigham, our Executive Chairman, and are led by an entrepreneurial team with a history of constructive disruption bringing significant

and complementary experience to this enterprise, including the perspective of longtime E&P operators, which provides for an elevated

understanding of the end users of our products and services. Our executive management team has a proven track record with a history of

generating positive returns and value creation. Our experience as E&P operators was instrumental to our understanding of the opportunity

created by in-basin sand production and supply in the Permian Basin, which we view as North America’s premier shale resource and

which we believe will remain its most active through economic cycles.

About Moser Energy Systems

Moser Energy Systems is a world-class provider

of innovative, low-emission, grid interactive distributed energy solutions for Oilfield Services, Commercial, Industrial, and Military

applications.

Since 1973, Moser has been at the forefront of

advances in distributed energy solutions. Moser’s cutting-edge technologies include industry-leading development of proprietary

oilfield generator systems utilizing raw wellhead gas. These innovations substantially reduce flaring and offer customers significant

reductions in operating expenses. The company’s products and commitment to customers are recognized throughout the industry as the

gold standard for low-emissions, reliable, and durable natural gas generators and hybrid generator systems.

Moser continues to build on its commitment

to excellence and its legacy of industry-leading innovation in pursuit of a lower emissions future powered by flexible, smart energy

applications with integrated grid services and active load management. With a dynamic vision, dedication to responsible business

practices, and cleaner, more efficient products, Moser is transforming power for the future.

Cautionary Statement Regarding Forward-Looking

Statements

This press release contains forward-looking statements

within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E

of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). Statements that are predictive or prospective in

nature, that depend upon or refer to future events or conditions or that include the words “may,” “assume,” “forecast,”

“position,” “strategy,” “potential,” “continue,” “could,” “will,”

“plan,” “project,” “budget,” “predict,” “pursue,” “target,” “seek,”

“objective,” “believe,” “expect,” “anticipate,” “intend,” “estimate”

and other expressions that are predictions of or indicate future events and trends and that do not relate to historical matters identify

forward-looking statements. Examples of forward-looking statements include, but are not limited to, statements regarding Atlas’s

plans to finance the Moser Acquisition; the anticipated financial performance of Atlas following the Moser Acquisition; expected accretion

to Adjusted EBITDA; expectations regarding the leverage and dividend profile

of Atlas following the Moser Acquisition; the expected synergies and efficiencies to be achieved as a result of the Moser Acquisition;

expansion and growth of Atlas’s business; Atlas’s plans to finance the Moser Acquisition; the receipt of all necessary approvals

to close the Moser Acquisition and the timing associated therewith; our business strategy, industry, future operations and profitability,

expected capital expenditures and the impact of such expenditures on our performance, statements about our financial position, production,

revenues and losses, our capital programs, management changes, current and potential future long-term contracts and our future business

and financial performance.

Although forward-looking statements reflect

our good faith beliefs at the time they are made, we caution you that these forward-looking statements are subject to a number of

risks and uncertainties, most of which are difficult to predict and many of which are beyond our control. These risks include but

are not limited to: the completion of the Moser Acquisition on anticipated terms and timing or at all, including obtaining any

required governmental or regulatory approval and satisfying other conditions to the completion of the Moser Acquisition;

uncertainties as to whether the Moser Acquisition, if consummated, will achieve its anticipated benefits and projected synergies

within the expected time period or at all; Atlas’s ability to integrate Moser’s operations in a successful manner and in

the expected time period; the occurrence of any event, change, or other circumstance that could give rise to the termination of the

Moser Acquisition; risks that the anticipated tax treatment of the Moser Acquisition is not obtained; unforeseen or unknown

liabilities; potential litigation relating to the Moser Acquisition; the possibility that the Moser Acquisition may be more

expensive to complete than anticipated, including as a result of unexpected factors or events; the effect of the announcement,

pendency or completion of the Moser Acquisition on the parties’ business relationships and business generally; risks that the

Moser Acquisition disrupts current plans and operations of Atlas or Moser and their respective management teams and potential

difficulties in retaining employees as a result of the Moser Acquisition; the risks related to Atlas’s financing of the Moser

Acquisition; potential negative effects of this announcement and the pendency or completion of the Moser Acquisition on the market

price of Atlas’s common stock or operating results; unexpected future capital expenditures; our ability to successfully

execute our stock repurchase program or implement future stock repurchase programs; commodity price volatility, including volatility

stemming from the ongoing armed conflicts between Russia and Ukraine and Israel and Hamas; increasing hostilities and instability in

the Middle East; adverse developments affecting the financial services industry; our ability to complete growth projects on time and

on budget; the risk that stockholder litigation in connection with our recent corporate reorganization may result in significant

costs of defense, indemnification and liability; changes in general economic, business and political conditions, including changes

in the financial markets; transaction costs; actions of OPEC+ to set and maintain oil production levels; the level of production of

crude oil, natural gas and other hydrocarbons and the resultant market prices of crude oil; inflation; environmental risks;

operating risks; regulatory changes; lack of demand; market share growth; the uncertainty inherent in projecting future rates of

reserves; production; cash flow; access to capital; the timing of development expenditures; the ability of our customers to meet

their obligations to us; our ability to maintain effective internal controls; and other factors discussed or referenced in our

filings made from time to time with the U.S. Securities and Exchange Commission (“SEC”), including those discussed under

the heading “Risk Factors” in our Annual Report on Form 10-K, filed with the SEC on February 27, 2024, and any

subsequently filed Quarterly Reports on Form 10-Q and Current Reports on Form 8-K. Readers are cautioned not to place

undue reliance on forward-looking statements, which speak only as of the date hereof. Factors or events that could cause our actual

results to differ may emerge from time to time, and it is not possible for us to predict all of them. We undertake no obligation to

publicly update or revise any forward-looking statement, whether as a result of new information, future developments or otherwise,

except as may be required by law.

Non-GAAP Financial Measures

This press release includes or

references certain forward-looking financial measures not prepared in conformity with generally accepted accounting principles (“GAAP”),

including EBITDA and Adjusted EBITDA. Because Atlas provides certain of these

measures on a forward-looking basis, it cannot reliably or reasonably predict certain of the necessary components of the most directly

comparable forward-looking GAAP financial measures, such as Gross Profit, Net Income, Operating Income, or any other measure derived in

accordance with GAAP. Accordingly, Atlas is unable to present a quantitative reconciliation of such forward-looking, non-GAAP financial

measures to the respective most directly comparable forward-looking GAAP financial measures. Atlas believes that these forward-looking,

non-GAAP measures may be a useful tool for the investment community in comparing Atlas’s forecasted financial performance to the

forecasted financial performance of other companies in the industry.

Atlas Energy Solutions – Reconciliation

of Adjusted EBITDA to Net Income

(unaudited, in thousands)

| | |

Fourth Quarter Ended December 31, | |

| | |

| | |

2024 Estimated | |

| (In thousands) | |

2023 Actual | | |

Low | | |

High | |

| Net Income | |

$ | 36,050 | | |

$ | 12,850 | | |

$ | 14,250 | |

| Depreciation, depletion and accretion expense | |

| 12,266 | | |

| 31,012 | | |

| 31,612 | |

| Amortization expense of acquired intangible assets | |

| — | | |

| 3,943 | | |

| 3,543 | |

| Interest expense | |

| 4,731 | | |

| 12,357 | | |

| 12,157 | |

| Income tax expense | |

| 11,010 | | |

| 4,766 | | |

| 5,766 | |

| EBITDA | |

$ | 64,057 | | |

$ | 64,928 | | |

$ | 67,328 | |

| Stock and unit-based compensation | |

| 3,749 | | |

| 6,520 | | |

| 6,320 | |

| Insurance recovery (gain) | |

| — | | |

| (10,098 | ) | |

| (10,098 | ) |

| Other non-recurring costs | |

| 441 | | |

| — | | |

| — | |

| Other acquisition related costs | |

| 451 | | |

| 850 | | |

| 650 | |

| Adjusted EBITDA | |

$ | 68,698 | | |

$ | 62,200 | | |

$ | 64,200 | |

| | |

Fiscal Year Ended December 31, | |

| | |

| | |

2024 Estimated | |

| (In thousands) | |

2023 Actual | | |

Low | | |

High | |

| Net Income | |

$ | 226,493 | | |

$ | 58,392 | | |

| 59,792 | |

| Depreciation, depletion and accretion expense | |

| 41,634 | | |

| 101,877 | | |

| 102,477 | |

| Amortization expense of acquired intangible assets | |

| — | | |

| 12,516 | | |

| 12,116 | |

| Interest expense | |

| 17,452 | | |

| 43,178 | | |

| 42,978 | |

| Income tax expense | |

| 31,378 | | |

| 16,182 | | |

| 17,182 | |

| EBITDA | |

$ | 316,957 | | |

$ | 232,145 | | |

$ | 234,545 | |

| Stock and unit-based compensation | |

| 7,409 | | |

| 22,481 | | |

| 22,281 | |

| Loss on disposal of assets | |

| — | | |

| 19,672 | | |

| 19,672 | |

| Insurance recovery (gain) | |

| — | | |

| (20,098 | ) | |

| (20,098 | ) |

| Other non-recurring costs | |

| 4,838 | | |

| 14,335 | | |

| 14,335 | |

| Other acquisition related costs | |

| 451 | | |

| 19,331 | | |

| 19,131 | |

| Adjusted EBITDA | |

$ | 329,655 | | |

$ | 287,866 | | |

$ | 289,866 | |

Non-GAAP Measure Definitions

We define Adjusted EBITDA as net income before

depreciation, depletion and accretion, amortization expense of acquired intangible assets, interest expense, income tax expense, stock

and unit-based compensation, loss on extinguishment of debt, loss on disposal of assets, insurance recovery (gain), unrealized commodity

derivative gain (loss), other acquisition related costs, and other non-recurring costs. Management believes Adjusted EBITDA is useful

because it allows management to more effectively evaluate the Company’s operating performance and compare the results of its operations

from period to period and against our peers without regard to financing method or capital structure. We exclude the items listed above

from net income in arriving at Adjusted EBITDA because these amounts can vary substantially from company to company within our industry

depending upon accounting methods and book values of assets, capital structures and the method by which the assets were acquired.

We define EBITDA as net income before depreciation,

depletion and accretion expense, amortization expense of acquired intangible assets, interest expense, and income tax expense.

No Offer or Solicitation

This press release is for informational purposes

only and does not constitute an offer to sell or the solicitation of an offer to buy any securities, or a solicitation of any vote or

approval, nor shall there be any sale of securities in any jurisdiction in which such offer, solicitation or sale would be unlawful prior

to registration or qualification under the securities laws of any such jurisdiction.

Investor Contact

Kyle Turlington

5918

W Courtyard Drive, Suite #500

Austin, Texas 78730

United States

T: 512-220-1200

IR@atlas.energy

Exhibit 99.2

| Atlas Energy Solutions (NYSE: AESI) | January 2025 NYSE: AESI

Acquisition of

Moser Energy Systems

January 27, 2025 |

| Atlas Energy Solutions (NYSE: AESI) | January 2025

Disclaimer

2

Forward-Looking Statements

This Presentation contains “forward-looking statements” of Atlas Energy Solutions Inc. (“Atlas,” the “Company,” “AESI,” “we,” “us” or “our”) within the meaning of Section 27A of the Securities Act of

1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). Statements that are predictive or prospective in nature, that

depend upon or refer to future events or conditions or that include the words “may,” “assume,” “forecast,” “position,” “strategy,” “potential,” “continue,” “could,” “will,” “plan,” “project,” “budget,”

“predict,” “pursue,” “target,” “seek,” “objective,” “believe,” “expect,” “anticipate,” “intend,” “estimate” and other expressions that are predictions of or indicate future events and trends and that do not

relate to historical matters identify forward-looking statements. Examples of forward-looking statements include, but are not limited to, statements regarding Atlas’s plans to finance the acquisition of

Moser Energy Services, Inc. (d/b/a Moser Energy Systems) (the “Moser Acquisition”); the anticipated financial performance of Atlas following the Moser Acquisition; expected accretion to free cash

flow, cash flow per share, Adjusted EBITDA and earnings per share; expectations regarding the leverage and dividend profile of Atlas following the Moser Acquisition; the expected synergies and

efficiencies to be achieved as a result of the Moser Acquisition; expansion and growth of Atlas’s business following the Moser Acquisition; the receipt of all necessary approvals to close the Moser

Acquisition and the timing associated therewith; our business strategy, industry, future operations and profitability, expected capital expenditures and the impact of such expenditures on our

performance, statements about our financial position, production, revenues and losses, our capital programs, expectations regarding the growth of U.S. electricity demand and the demand for

distributed power generation, management changes, current and potential future long-term contracts and our future business and financial performance.

Although forward-looking statements reflect our good faith beliefs at the time they are made, we caution you that these forward-looking statements are subject to a number of risks and uncertainties,

most of which are difficult to predict and many of which are beyond our control. These risks include but are not limited to: the completion of the Moser Acquisition on anticipated terms and timing or at

all, including obtaining any required governmental or regulatory approval and satisfying other conditions to the completion of the Moser Acquisition; uncertainties as to whether the Moser Acquisition,

if consummated, will achieve its anticipated benefits and projected synergies within the expected time period or at all; Atlas’s ability to integrate Moser’s operations in a successful manner and in the

expected time period; the occurrence of any event, change, or other circumstance that could give rise to the termination of the Moser Acquisition; risks that the anticipated tax treatment of the Moser

Acquisition is not obtained; unforeseen or unknown liabilities; potential litigation relating to the Moser Acquisition; the possibility that the Moser Acquisition may be more expensive to complete than

anticipated, including as a result of unexpected factors or events; the effect of the announcement, pendency or completion of the Moser Acquisition on the parties’ business relationships and

business generally; risks that the Moser Acquisition disrupts current plans and operations of Atlas and its management team and potential difficulties in retaining employees as a result of the Moser

Acquisition; the risks related to Atlas’s financing of the Moser Acquisition; potential negative effects of this announcement and the pendency or completion of the Moser Acquisition on the market

price of Atlas’s common stock or operating results; unexpected future capital expenditures; our ability to successfully execute our stock repurchase program or implement future stock repurchase

programs; commodity price volatility, including volatility stemming from the ongoing armed conflicts between Russia and Ukraine and Israel and Hamas; increasing hostilities and instability in the

Middle East; adverse developments affecting the financial services industry; our ability to complete growth projects on time and on budget; the risk that stockholder litigation in connection with our

recent corporate reorganization may result in significant costs of defense, indemnification and liability; changes in general economic, business and political conditions, including changes in the

financial markets; transaction costs; actions of OPEC+ to set and maintain oil production levels; the level of production of crude oil, natural gas and other hydrocarbons and the resultant market

prices of crude oil; inflation; environmental risks; operating risks; regulatory changes; lack of demand; market share growth; the uncertainty inherent in projecting future rates of reserves; production;

cash flow; access to capital; the timing of development expenditures; the ability of our customers to meet their obligations to us; our ability to maintain effective internal controls; and other factors

discussed or referenced in our filings made from time to time with the U.S. Securities and Exchange Commission (“SEC”), including those discussed under the heading “Risk Factors” in our Annual

Report on Form 10-K, filed with the SEC on February 27, 2024, and any subsequently filed Quarterly Reports on Form 10-Q and Current Reports on Form 8-K. Readers are cautioned not to place

undue reliance on forward-looking statements, which speak only as of the date hereof. Factors or events that could cause our actual results to differ may emerge from time to time, and it is not

possible for us to predict all of them. We undertake no obligation to publicly update or revise any forward-looking statement, whether as a result of new information, future developments or otherwise,

except as may be required by law.

Trademarks and Trade Names

The Company owns or has rights to various trademarks, service marks and trade names that it uses in connection with the operation of its business. This Presentation also contains trademarks,

service marks and trade names of third parties, which are the property of their respective owners. The use or display of third parties’ trademarks, service marks, trade names or products in this

Presentation is not intended to, and does not imply, a relationship with the Company, or an endorsement or sponsorship by or of the Company. Solely for convenience, the trademarks, service marks

and trade names referred to in this Presentation may appear without the ®, TM or SM symbols, but such references are not intended to indicate, in any way, that the Company will not assert, to the

fullest extent under applicable law, its rights or the rights of the applicable licensor to these trademarks, service marks and trade names. |

| Atlas Energy Solutions (NYSE: AESI) | January 2025

Disclaimer (cont’d)

3

Industry and Market Data

This Presentation has been prepared by the Company and includes market data and certain other statistical information from third-party sources, including independent industry publications,

government publications, and other published independent sources. Although we believe these third-party sources are reliable as of their respective dates, we have not independently verified the

accuracy or completeness of this information. Some data is also based on our good faith estimates, which are derived from our review of internal sources as well as the third-party sources described

above. The industry in which we operate is subject to a high degree of uncertainty and risk due to a variety of factors. These and other factors could cause results to differ materially from those

expressed in these third-party publications. Additionally, descriptions herein of market conditions and opportunities are presented for informational purposes only; there can be no assurance that

such conditions will actually occur. Please also see “Forward-Looking Statements” disclaimer above.

Non-GAAP Financial Measures

This press release includes or references certain forward-looking financial measures not prepared in conformity with generally accepted accounting principles (“GAAP”), including free cash flow, cash

flow per share, Adjusted EBITDA and earnings per share. Because Atlas provides these measures on a forward-looking basis, it cannot reliably or reasonably predict certain of the necessary

components of the most directly comparable forward-looking GAAP financial measures, such as Gross Profit, Net Income, Operating Income, or any other measure derived in accordance with GAAP.

Accordingly, Atlas is unable to present a quantitative reconciliation of such forward-looking, non-GAAP financial measures to the respective most directly comparable forward-looking GAAP financial

measures. Atlas believes that these forward-looking, non-GAAP measures may be a useful tool for the investment community in comparing Atlas’s forecasted financial performance to the forecasted

financial performance of other companies in the industry.

No Offer or Solicitation

This communication includes information relating to the Moser Acquisition. This communication is for informational purposes only and does not constitute an offer to sell or the solicitation of an offer

to buy any securities or a solicitation of any vote or approval, in any jurisdiction, in connection with the Moser Acquisition or otherwise, nor shall there be any sale, issuance, exchange or transfer of

the securities referred to in this document in any jurisdiction in contravention of applicable law. No offer of securities shall be made except by means of a prospectus meeting the requirements of

Section 10 of the Securities Act. |

| Atlas Energy Solutions (NYSE: AESI) | January 2025 4

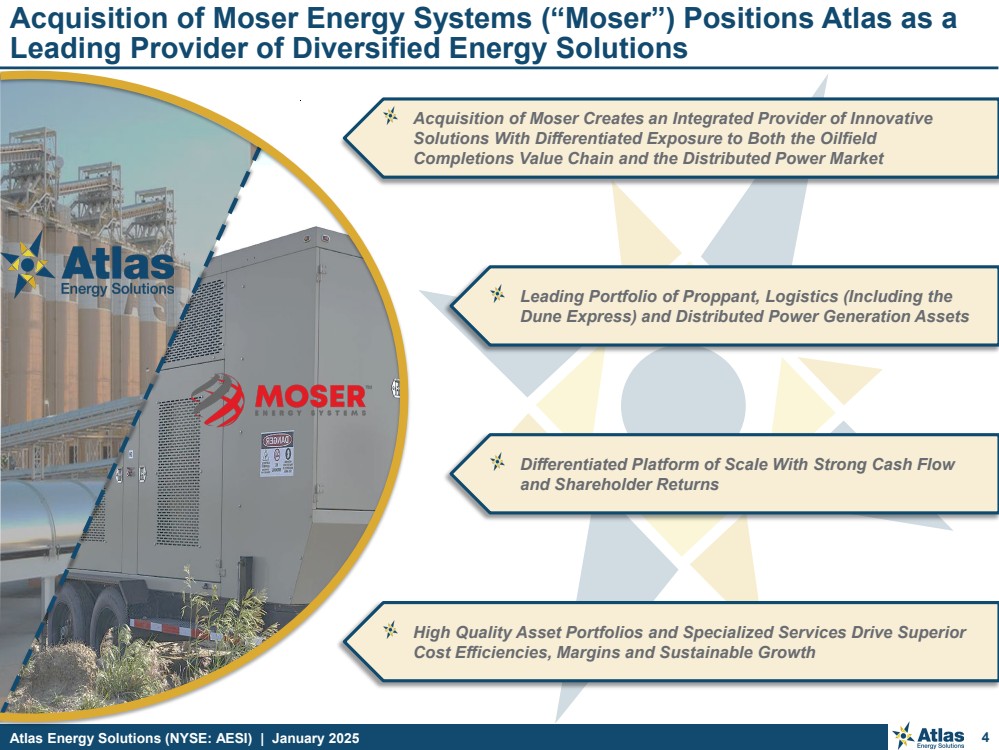

Acquisition of Moser Energy Systems (“Moser”) Positions Atlas as a

Leading Provider of Diversified Energy Solutions

Acquisition of Moser Creates an Integrated Provider of Innovative

Solutions With Differentiated Exposure to Both the Oilfield

Completions Value Chain and the Distributed Power Market

Leading Portfolio of Proppant, Logistics (Including the

Dune Express) and Distributed Power Generation Assets

Differentiated Platform of Scale With Strong Cash Flow

and Shareholder Returns

High Quality Asset Portfolios and Specialized Services Drive Superior

Cost Efficiencies, Margins and Sustainable Growth |

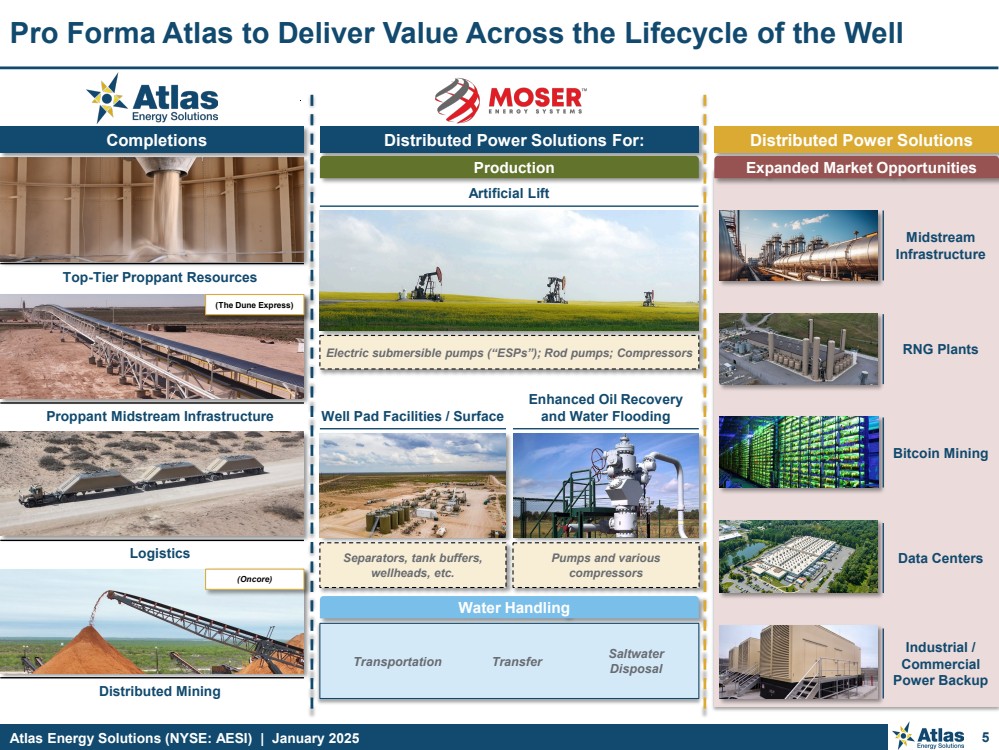

| Atlas Energy Solutions (NYSE: AESI) | January 2025 5

Pro Forma Atlas to Deliver Value Across the Lifecycle of the Well

Completions Distributed Power Solutions For:

Production

Proppant Midstream Infrastructure

(The Dune Express)

Artificial Lift

Enhanced Oil Recovery

Well Pad Facilities / Surface and Water Flooding

Pumps and various

compressors

Separators, tank buffers,

wellheads, etc.

Electric submersible pumps (“ESPs”); Rod pumps; Compressors

(Oncore)

Water Handling

Midstream

Infrastructure

Logistics

Distributed Mining

Saltwater

Disposal Transportation Transfer

Distributed Power Solutions

Expanded Market Opportunities

Top-Tier Proppant Resources

RNG Plants

Bitcoin Mining

Data Centers

Industrial /

Commercial

Power Backup |

| Atlas Energy Solutions (NYSE: AESI) | January 2025

Acquisition expands on Atlas’s initial thesis to build an organization with strong competitive

differentiation that enables the company to deliver superior through-cycle returns to shareholders

6

Atlas and Moser are a Compelling Strategic Fit

+

Creates a Diversified Energy Solutions Provider of Scale With Strong Growth Opportunities

In Core Markets

Establishes strong foothold in the distributed power market via the acquired low-emission, grid interactive ~212MW fleet

supporting production / artificial lift operations

Increases Atlas’s customer reach with a critical power service offering in Atlas’s core geography while providing geographic

diversity (operating locations in the Bakken, DJ, Uinta, and Eagle Ford basins)

1

Dynamic Power Generation Portfolio Provides Entry Into Adjacent End Markets

Provides a platform of scale, >900-unit natural gas-powered generator fleet, enabling Atlas to mitigate existing grid constraints,

a key factor driving the demand growth for distributed power assets, both in and out of energy markets

Expanded opportunities are immediately available in markets where Moser has a developing and growing presence

(e.g., midstream infrastructure, RNG plants, bitcoin mining, data centers and industrial / commercial backup power)

Provides increased exposure to production-end of Oil & Gas value chain, which we expect to lower volatility of future cash flows

2

Differentiated Assets and Capabilities Drive Strong Margins and Lower Through-Cycle

Maintenance / Replacement Costs

Strong EBITDA(1) margin profile of 50%+ expected to enhance pro forma free cash flow(1)

In-house R&D and manufacturing capabilities, coupled with critical in-field service, provide quality control and standardization

across the fleet ensuring market-leading uptime for customers in demanding applications

Moser’s commitment to innovation has led to continuous in-house product advancements, including designing the engines to

utilize field gas as a fuel source, enabling operators to mitigate flaring

In-house remanufacturing competencies enable Moser to provide exceptional runtimes with remanufactured assets while

reducing the cost relative to a new build by ~50%+

3

Critical Nature of Power Service Offering Provides Sticky Customer Retention With Solid Utilization

and Cash Flow Visibility

Robust backlog of MSAs with top oil and gas producers and Moser’s reliable performance provide increased visibility into

future cash flows

4

Acquisition Expected to Be Accretive to Free Cash Flow and Shareholder Returns

Compelling transaction value of ~4.3x Adjusted EBITDA(1)

Expected to enhance free cash flow, accelerating shareholder returns

5

(1) This is a non-GAAP metric. Please see the Appendix at the back of this presentation for definitions of non-GAAP measures. |

| Atlas Energy Solutions (NYSE: AESI) | January 2025

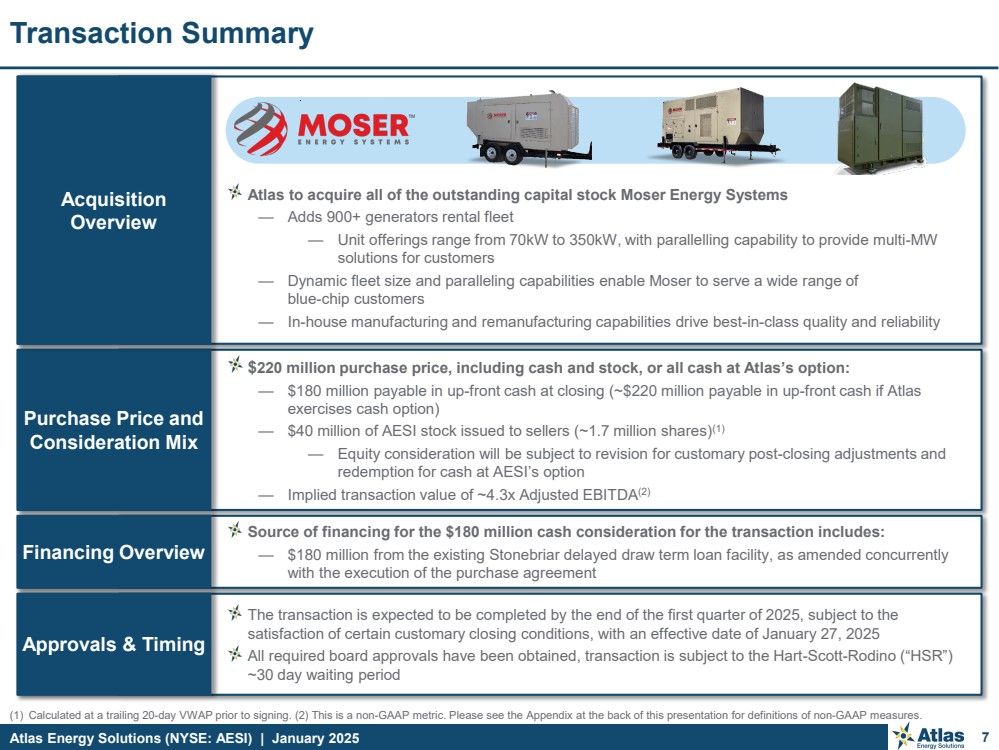

$220 million purchase price, including cash and stock, or all cash at Atlas’s option:

— $180 million payable in up-front cash at closing (~$220 million payable in up-front cash if Atlas

exercises cash option)

— $40 million of AESI stock issued to sellers (~1.7 million shares)(1)

— Equity consideration will be subject to revision for customary post-closing adjustments and

redemption for cash at AESI’s option

— Implied transaction value of ~4.3x Adjusted EBITDA(2)

Purchase Price and

Consideration Mix

Source of financing for the $180 million cash consideration for the transaction includes:

— $180 million from the existing Stonebriar delayed draw term loan facility, as amended concurrently

with the execution of the purchase agreement

Financing Overview

The transaction is expected to be completed by the end of the first quarter of 2025, subject to the

satisfaction of certain customary closing conditions, with an effective date of January 27, 2025

All required board approvals have been obtained, transaction is subject to the Hart-Scott-Rodino (“HSR”)

~30 day waiting period

Approvals & Timing

(1) Calculated at a trailing 20-day VWAP prior to signing. (2) This is a non-GAAP metric. Please see the Appendix at the back of this presentation for definitions of non-GAAP measures.

7

Transaction Summary

Atlas to acquire all of the outstanding capital stock Moser Energy Systems

— Adds 900+ generators rental fleet

— Unit offerings range from 70kW to 350kW, with parallelling capability to provide multi-MW

solutions for customers

— Dynamic fleet size and paralleling capabilities enable Moser to serve a wide range of

blue-chip customers

— In-house manufacturing and remanufacturing capabilities drive best-in-class quality and reliability

Acquisition

Overview |

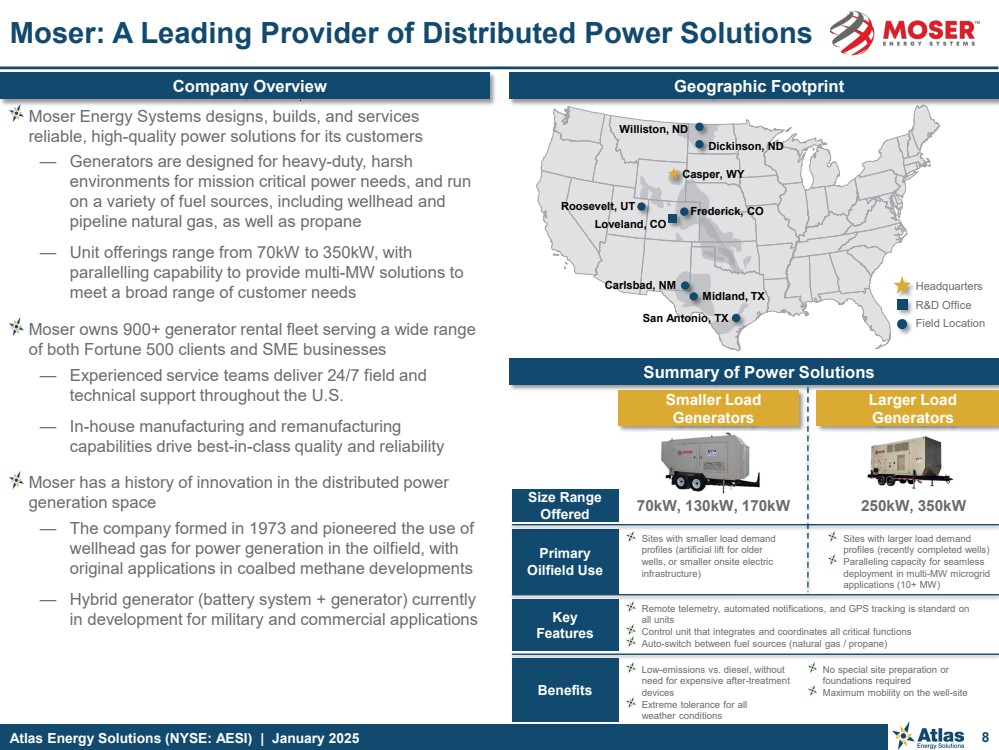

| Atlas Energy Solutions (NYSE: AESI) | January 2025 8

Moser: A Leading Provider of Distributed Power Solutions

Geographic Footprint

Moser Energy Systems designs, builds, and services

reliable, high-quality power solutions for its customers

— Generators are designed for heavy-duty, harsh

environments for mission critical power needs, and run

on a variety of fuel sources, including wellhead and

pipeline natural gas, as well as propane

— Unit offerings range from 70kW to 350kW, with

parallelling capability to provide multi-MW solutions to

meet a broad range of customer needs

Moser owns 900+ generator rental fleet serving a wide range

of both Fortune 500 clients and SME businesses

— Experienced service teams deliver 24/7 field and

technical support throughout the U.S.

— In-house manufacturing and remanufacturing

capabilities drive best-in-class quality and reliability

Moser has a history of innovation in the distributed power

generation space

— The company formed in 1973 and pioneered the use of

wellhead gas for power generation in the oilfield, with

original applications in coalbed methane developments

— Hybrid generator (battery system + generator) currently

in development for military and commercial applications

Summary of Power Solutions

Larger Load

Generators

Smaller Load

Generators

Size Range

Offered

Primary

Oilfield Use

Benefits

Key

Features

70kW, 130kW, 170kW 250kW, 350kW

Sites with smaller load demand

profiles (artificial lift for older

wells, or smaller onsite electric

infrastructure)

Sites with larger load demand

profiles (recently completed wells)

Paralleling capacity for seamless

deployment in multi-MW microgrid

applications (10+ MW)

Low-emissions vs. diesel, without

need for expensive after-treatment

devices

Extreme tolerance for all

weather conditions

No special site preparation or

foundations required

Maximum mobility on the well-site

Remote telemetry, automated notifications, and GPS tracking is standard on

all units

Control unit that integrates and coordinates all critical functions

Auto-switch between fuel sources (natural gas / propane)

Headquarters

R&D Office

Field Location

Williston, ND

Dickinson, ND

Casper, WY

Roosevelt, UT Frederick, CO

Loveland, CO

Carlsbad, NM

Midland, TX

San Antonio, TX

Company Overview |

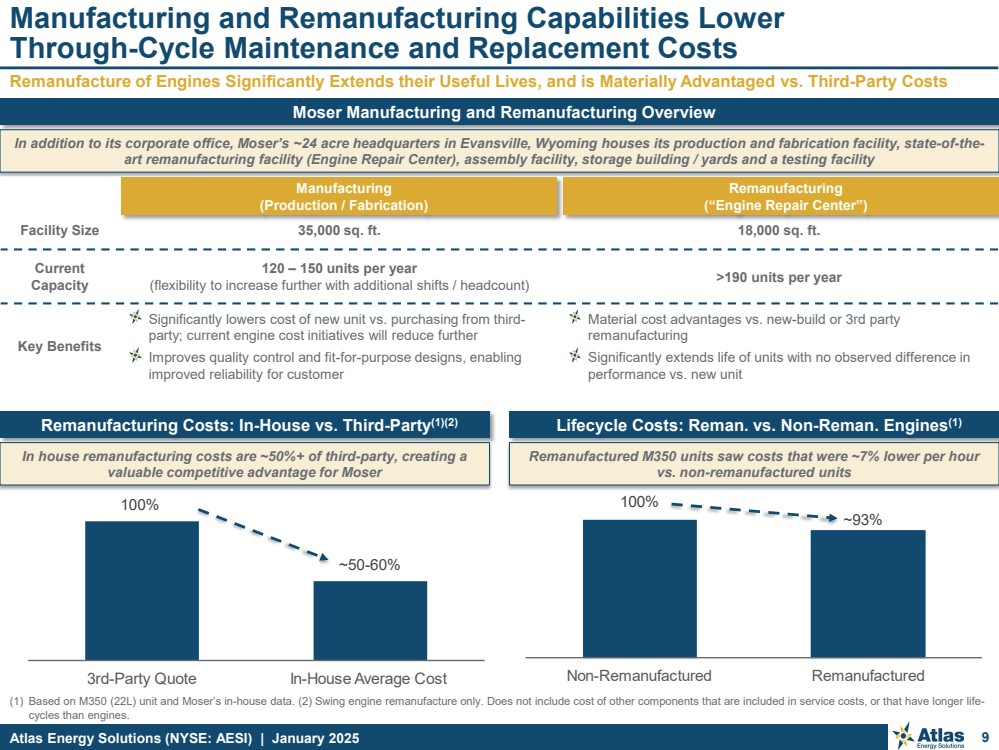

| Atlas Energy Solutions (NYSE: AESI) | January 2025

Moser Manufacturing and Remanufacturing Overview

Remanufacturing Costs: In-House vs. Third-Party(1)(2) Lifecycle Costs: Reman. vs. Non-Reman. Engines(1)

(1) Based on M350 (22L) unit and Moser’s in-house data. (2) Swing engine remanufacture only. Does not include cost of other components that are included in service costs, or that have longer life-cycles than engines.

9

Remanufacture of Engines Significantly Extends their Useful Lives, and is Materially Advantaged vs. Third-Party Costs

Manufacturing and Remanufacturing Capabilities Lower

Through-Cycle Maintenance and Replacement Costs

In addition to its corporate office, Moser’s ~24 acre headquarters in Evansville, Wyoming houses its production and fabrication facility, state-of-the-art remanufacturing facility (Engine Repair Center), assembly facility, storage building / yards and a testing facility

Facility Size 35,000 sq. ft. 18,000 sq. ft.

Current

Capacity

120 – 150 units per year

(flexibility to increase further with additional shifts / headcount) >190 units per year

Key Benefits

Significantly lowers cost of new unit vs. purchasing from third-party; current engine cost initiatives will reduce further

Improves quality control and fit-for-purpose designs, enabling

improved reliability for customer

Material cost advantages vs. new-build or 3rd party

remanufacturing

Significantly extends life of units with no observed difference in

performance vs. new unit

Remanufactured M350 units saw costs that were ~7% lower per hour

vs. non-remanufactured units

In house remanufacturing costs are ~50%+ of third-party, creating a

valuable competitive advantage for Moser

100%

3rd-Party Quote In-House Average Cost Non-Remanufactured Remanufactured

100%

~50-60%

Remanufacturing

(“Engine Repair Center”)

Manufacturing

(Production / Fabrication)

~93% |

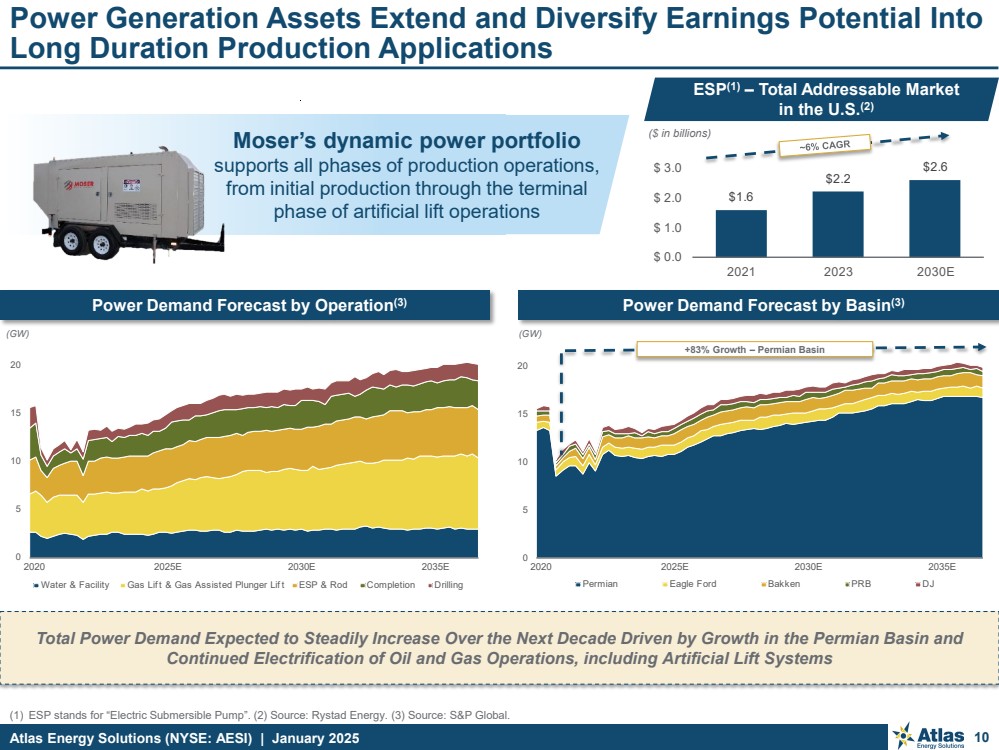

| Atlas Energy Solutions (NYSE: AESI) | January 2025

Moser’s dynamic power portfolio

supports all phases of production operations,

from initial production through the terminal

phase of artificial lift operations

(1) ESP stands for “Electric Submersible Pump”. (2) Source: Rystad Energy. (3) Source: S&P Global.

10

Power Generation Assets Extend and Diversify Earnings Potential Into

Long Duration Production Applications

$1.6

$2.2

$2.6

$ 0.0

$ 1.0

$ 2.0

$ 3.0

2021 2023 2030E

ESP(1) – Total Addressable Market

in the U.S.(2)

Power Demand Forecast by Operation(3) Power Demand Forecast by Basin(3)

(GW)

0

5

10

15

20

Water & Facility Gas Lif t & Gas Assisted Plunger Lif t ESP & Rod Completion Drilling

0

5

10

15

20

Permian Eagle Ford Bakken PRB DJ

2020 2025E 2030E 2035E 2020 2025E 2030E 2035E

(GW)

Total Power Demand Expected to Steadily Increase Over the Next Decade Driven by Growth in the Permian Basin and

Continued Electrification of Oil and Gas Operations, including Artificial Lift Systems

($ in billions)

+83% Growth – Permian Basin |

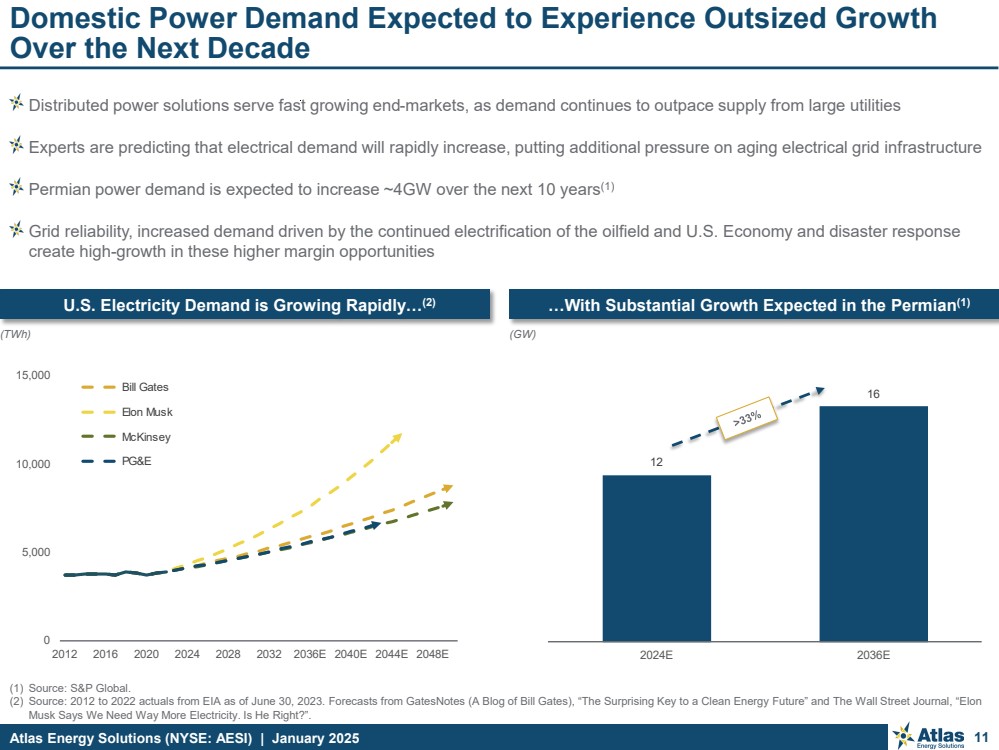

| Atlas Energy Solutions (NYSE: AESI) | January 2025

(1) Source: S&P Global.

(2) Source: 2012 to 2022 actuals from EIA as of June 30, 2023. Forecasts from GatesNotes (A Blog of Bill Gates), “The Surprising Key to a Clean Energy Future” and The Wall Street Journal, “Elon

Musk Says We Need Way More Electricity. Is He Right?”.

11

Domestic Power Demand Expected to Experience Outsized Growth

Over the Next Decade

U.S. Electricity Demand is Growing Rapidly…(2) …With Substantial Growth Expected in the Permian(1)

Distributed power solutions serve fast growing end-markets, as demand continues to outpace supply from large utilities

Experts are predicting that electrical demand will rapidly increase, putting additional pressure on aging electrical grid infrastructure

Permian power demand is expected to increase ~4GW over the next 10 years(1)

Grid reliability, increased demand driven by the continued electrification of the oilfield and U.S. Economy and disaster response

create high-growth in these higher margin opportunities

12

16

2024E 2036E

(TWh)

0

5,000

10,000

15,000

2012 2016 2020 2024 2028 2032 2036E 2040E 2044E 2048E

Bill Gates

Elon Musk

McKinsey

PG&E

(GW) |

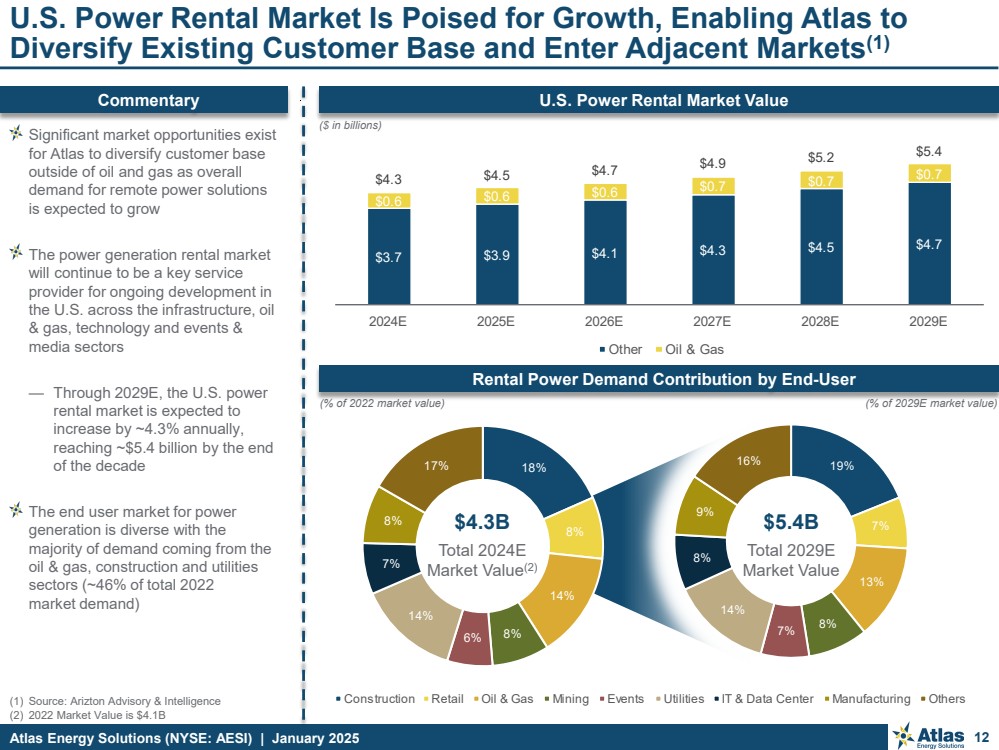

| Atlas Energy Solutions (NYSE: AESI) | January 2025

(1) Source: Arizton Advisory & Intelligence

(2) 2022 Market Value is $4.1B

12

U.S. Power Rental Market Is Poised for Growth, Enabling Atlas to

Diversify Existing Customer Base and Enter Adjacent Markets(1)

U.S. Power Rental Market Value

Significant market opportunities exist

for Atlas to diversify customer base

outside of oil and gas as overall

demand for remote power solutions

is expected to grow

The power generation rental market

will continue to be a key service

provider for ongoing development in

the U.S. across the infrastructure, oil

& gas, technology and events &

media sectors

— Through 2029E, the U.S. power

rental market is expected to

increase by ~4.3% annually,

reaching ~$5.4 billion by the end

of the decade

The end user market for power

generation is diverse with the

majority of demand coming from the

oil & gas, construction and utilities

sectors (~46% of total 2022

market demand)

(% of 2022 market value)

Commentary

Rental Power Demand Contribution by End-User

($ in billions)

$3.7 $3.9 $4.1 $4.3 $4.5 $4.7

$0.6 $0.6 $0.6 $0.7 $0.7 $0.7 $4.3 $4.5 $4.7 $4.9 $5.2 $5.4

2024E 2025E 2026E 2027E 2028E 2029E

Other Oil & Gas

$4.3B

Total 2024E

Market Value(2)

$5.4B

Total 2029E

Market Value

18%

8%

14%

8% 6%

14%

7%

8%

17%

Construction Retail Oil & Gas Mining Events Utilities IT & Data Center Manufacturing Others

19%

7%

13%

8% 7%

14%

8%

9%

16%

(% of 2029E market value) |

| Atlas Energy Solutions (NYSE: AESI) | January 2025

(10%)

0%

10%

20%

30%

40%

50%

(5%) 0% 5% 10% 15% 20% 25%

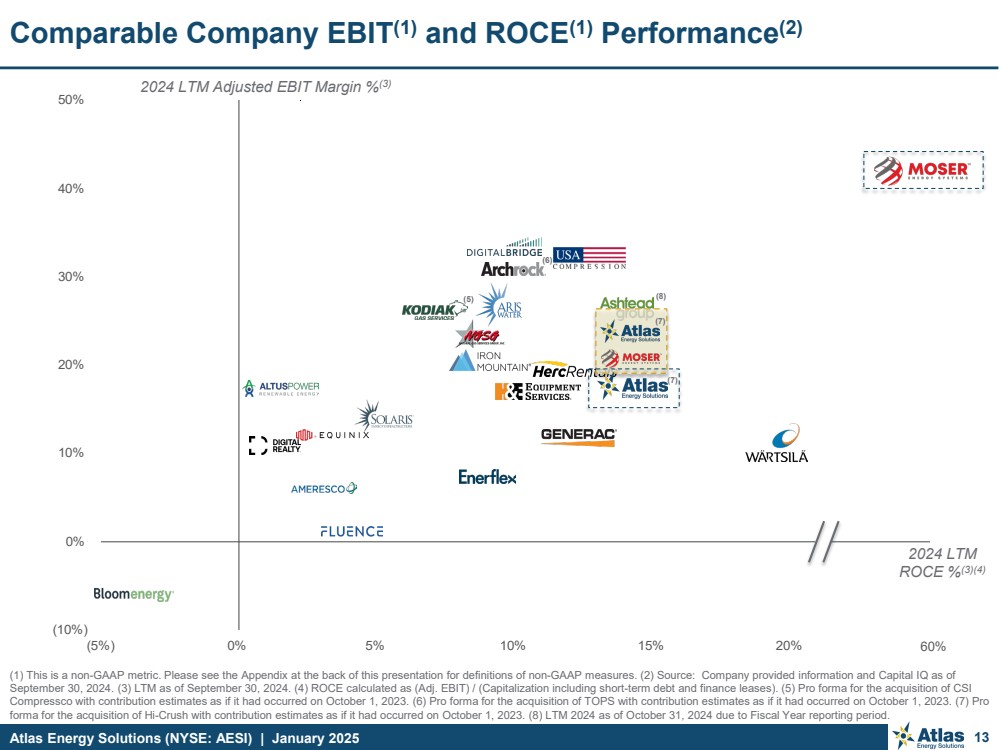

Comparable Company EBIT(1) and ROCE(1) Performance(2)

2024 LTM Adjusted EBIT Margin %(3)

2024 LTM

ROCE %(3)(4)

(1) This is a non-GAAP metric. Please see the Appendix at the back of this presentation for definitions of non-GAAP measures. (2) Source: Company provided information and Capital IQ as of

September 30, 2024. (3) LTM as of September 30, 2024. (4) ROCE calculated as (Adj. EBIT) / (Capitalization including short-term debt and finance leases). (5) Pro forma for the acquisition of CSI

Compressco with contribution estimates as if it had occurred on October 1, 2023. (6) Pro forma for the acquisition of TOPS with contribution estimates as if it had occurred on October 1, 2023. (7) Pro

forma for the acquisition of Hi-Crush with contribution estimates as if it had occurred on October 1, 2023. (8) LTM 2024 as of October 31, 2024 due to Fiscal Year reporting period.

13

(5)

(6)

(7)

(7)

(8)

60% |

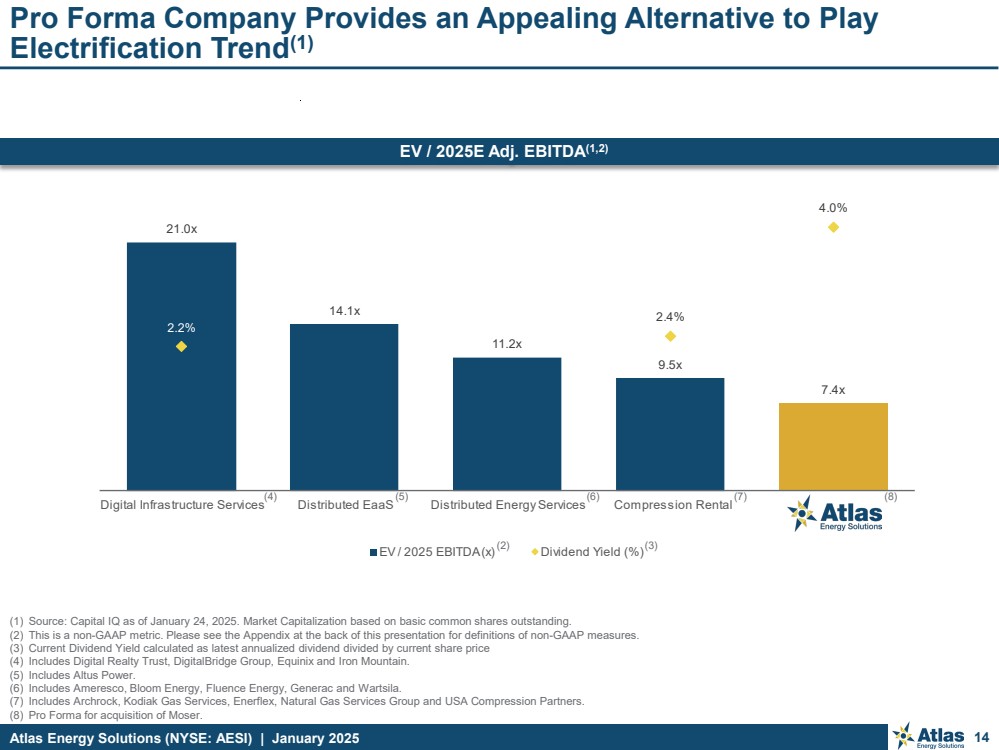

| Atlas Energy Solutions (NYSE: AESI) | January 2025

(1) Source: Capital IQ as of January 24, 2025. Market Capitalization based on basic common shares outstanding.

(2) This is a non-GAAP metric. Please see the Appendix at the back of this presentation for definitions of non-GAAP measures.

(3) Current Dividend Yield calculated as latest annualized dividend divided by current share price

(4) Includes Digital Realty Trust, DigitalBridge Group, Equinix and Iron Mountain.

(5) Includes Altus Power.

(6) Includes Ameresco, Bloom Energy, Fluence Energy, Generac and Wartsila.

(7) Includes Archrock, Kodiak Gas Services, Enerflex, Natural Gas Services Group and USA Compression Partners.

(8) Pro Forma for acquisition of Moser.

14

21.0x

14.1x

11.2x

9.5x

7.4x

2.2%

2.4%

4.0%

0.0x

5.0x

10.0x

15.0x

20.0x

25.0x

Digital Infrastructure Services Distributed EaaS Distributed Energy Services Compression Rental

EV / 2025 EBITDA (x) Dividend Yield (%)

Pro Forma Company Provides an Appealing Alternative to Play

Electrification Trend(1)

(3)

(4) (5) (6) (7) (8)

EV / 2025E Adj. EBITDA(1,2)

(2) |

| Atlas Energy Solutions (NYSE: AESI) | January 2025

(1) While Atlas believes that its future cash flows will be able to sustain the current level of dividends, there can be no guarantee that Atlas will be able to pay such dividends or at all or otherwise

return capital to its investors in the future, nor is Atlas obligated to do so.

(2) Source: Capital IQ as of January 24, 2025.

15

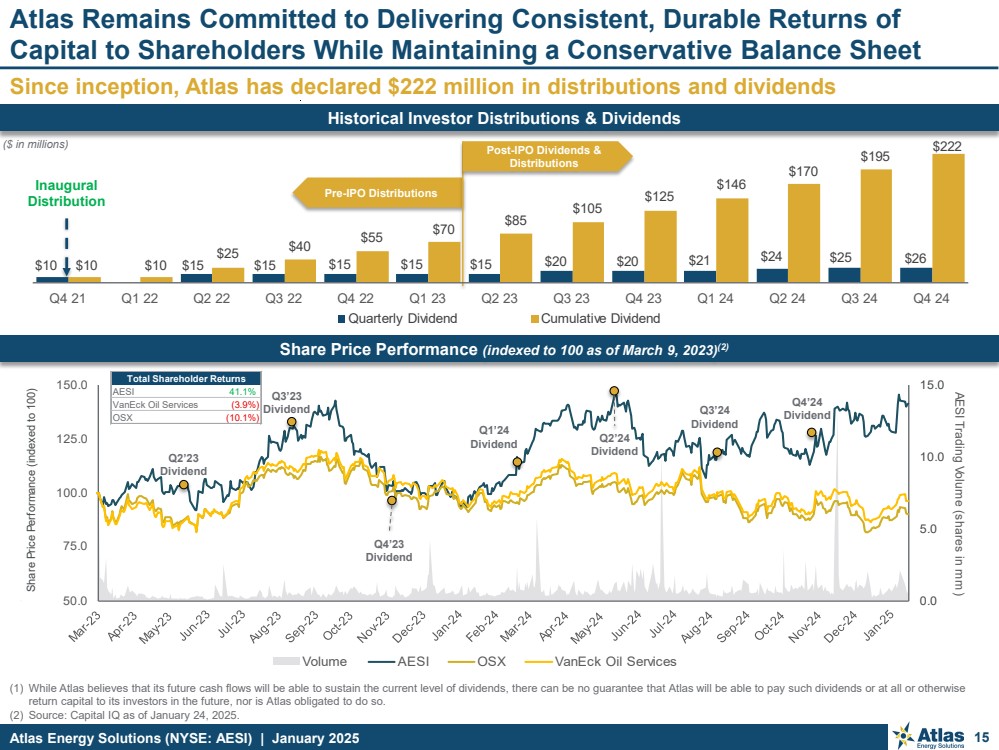

Since inception, Atlas has declared $222 million in distributions and dividends

Atlas Remains Committed to Delivering Consistent, Durable Returns of

Capital to Shareholders While Maintaining a Conservative Balance Sheet

Historical Investor Distributions & Dividends

Share Price Performance (indexed to 100 as of March 9, 2023)(2)

0.0

5.0

10.0

15.0

50.0

75.0

100.0

125.0

150.0

AESI Trading Volume (shares in mm

Share Price Performance

)

(indexed to 100)

Volume AESI OSX VanEck Oil Services

Total Shareholder Returns

AESI 41.1%

VanEck Oil Services (3.9%)

OSX (10.1%)

Q2’23

Dividend

Q3’23

Dividend

Q4’23

Dividend

Q1’24

Dividend

Q3’24

Dividend

Q4’24

Dividend

Inaugural

Distribution

($ in millions)

Pre-IPO Distributions

Post-IPO Dividends &

Distributions

Q2’24

Dividend

$10 $15 $15 $15 $15 $15 $20 $20 $21 $24 $25 $26 $10 $10

$25 $40 $55 $70 $85

$105

$125

$146

$170

$195 $222

Q4 21 Q1 22 Q2 22 Q3 22 Q4 22 Q1 23 Q2 23 Q3 23 Q4 23 Q1 24 Q2 24 Q3 24 Q4 24

Quarterly Dividend Cumulative Dividend |

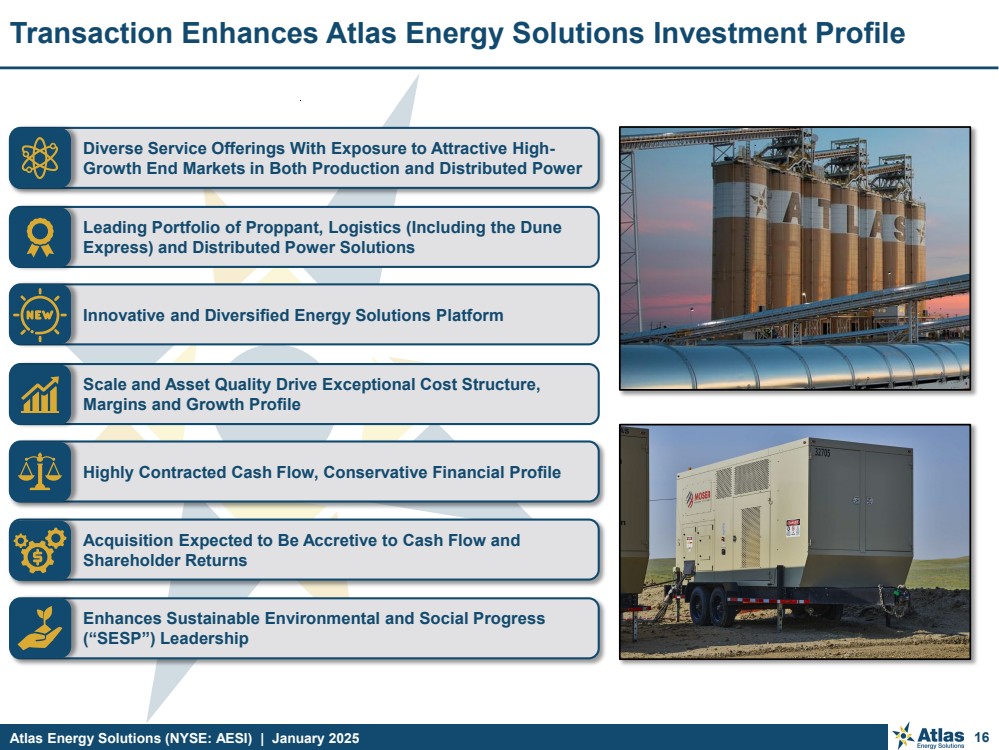

| Atlas Energy Solutions (NYSE: AESI) | January 2025 16

Transaction Enhances Atlas Energy Solutions Investment Profile

Enhances Sustainable Environmental and Social Progress

(“SESP”) Leadership

Highly Contracted Cash Flow, Conservative Financial Profile

Diverse Service Offerings With Exposure to Attractive High-Growth End Markets in Both Production and Distributed Power

Scale and Asset Quality Drive Exceptional Cost Structure,

Margins and Growth Profile

Leading Portfolio of Proppant, Logistics (Including the Dune

Express) and Distributed Power Solutions

Acquisition Expected to Be Accretive to Cash Flow and

Shareholder Returns

Innovative and Diversified Energy Solutions Platform |

| Atlas Energy Solutions (NYSE: AESI) | January 2025 17

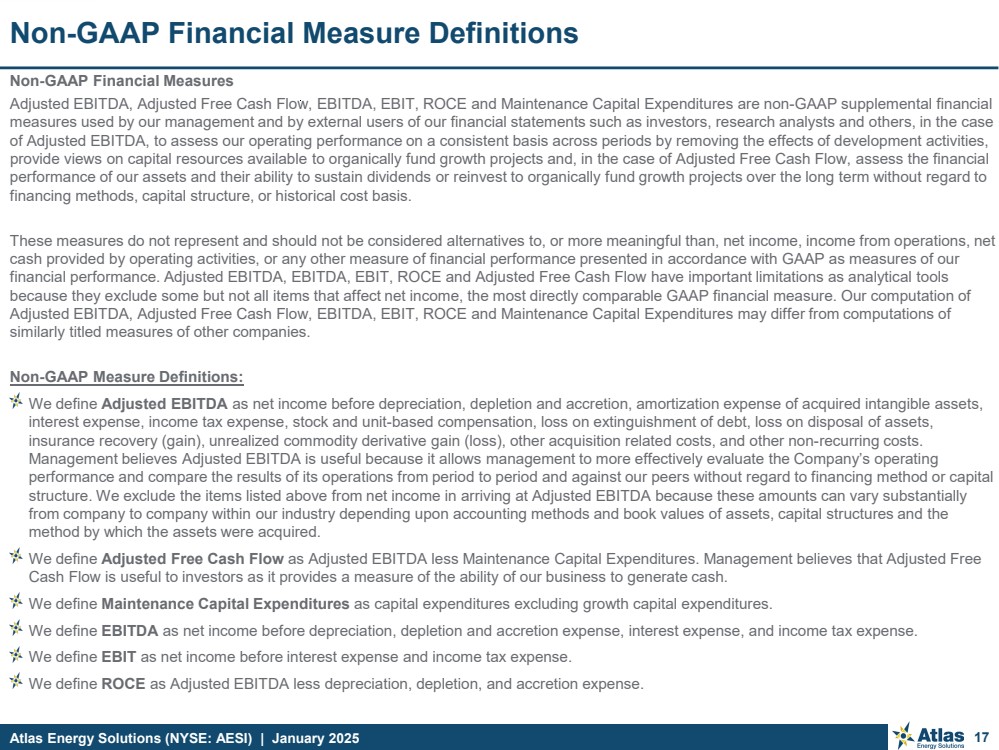

Non-GAAP Financial Measure Definitions

Non-GAAP Financial Measures

Adjusted EBITDA, Adjusted Free Cash Flow, EBITDA, EBIT, ROCE and Maintenance Capital Expenditures are non-GAAP supplemental financial

measures used by our management and by external users of our financial statements such as investors, research analysts and others, in the case

of Adjusted EBITDA, to assess our operating performance on a consistent basis across periods by removing the effects of development activities,

provide views on capital resources available to organically fund growth projects and, in the case of Adjusted Free Cash Flow, assess the financial

performance of our assets and their ability to sustain dividends or reinvest to organically fund growth projects over the long term without regard to

financing methods, capital structure, or historical cost basis.

These measures do not represent and should not be considered alternatives to, or more meaningful than, net income, income from operations, net

cash provided by operating activities, or any other measure of financial performance presented in accordance with GAAP as measures of our

financial performance. Adjusted EBITDA, EBITDA, EBIT, ROCE and Adjusted Free Cash Flow have important limitations as analytical tools

because they exclude some but not all items that affect net income, the most directly comparable GAAP financial measure. Our computation of

Adjusted EBITDA, Adjusted Free Cash Flow, EBITDA, EBIT, ROCE and Maintenance Capital Expenditures may differ from computations of

similarly titled measures of other companies.

Non-GAAP Measure Definitions:

We define Adjusted EBITDA as net income before depreciation, depletion and accretion, amortization expense of acquired intangible assets,

interest expense, income tax expense, stock and unit-based compensation, loss on extinguishment of debt, loss on disposal of assets,

insurance recovery (gain), unrealized commodity derivative gain (loss), other acquisition related costs, and other non-recurring costs.

Management believes Adjusted EBITDA is useful because it allows management to more effectively evaluate the Company’s operating

performance and compare the results of its operations from period to period and against our peers without regard to financing method or capital

structure. We exclude the items listed above from net income in arriving at Adjusted EBITDA because these amounts can vary substantially

from company to company within our industry depending upon accounting methods and book values of assets, capital structures and the

method by which the assets were acquired.

We define Adjusted Free Cash Flow as Adjusted EBITDA less Maintenance Capital Expenditures. Management believes that Adjusted Free

Cash Flow is useful to investors as it provides a measure of the ability of our business to generate cash.

We define Maintenance Capital Expenditures as capital expenditures excluding growth capital expenditures.

We define EBITDA as net income before depreciation, depletion and accretion expense, interest expense, and income tax expense.

We define EBIT as net income before interest expense and income tax expense.

We define ROCE as Adjusted EBITDA less depreciation, depletion, and accretion expense. |

| Atlas Energy Solutions (NYSE: AESI) | January 2025

Investor Relations Contact

For more information, please visit our website at https://atlas.energy/

IR Contact:

Kyle Turlington

5918 W Courtyard Drive, Suite #500; Austin, Texas 78730

(T) 512-220-1200

IR@atlas.energy

NYSE: AESI |

Exhibit 99.3

Updated Risk Factors

Risks Related to the Moser Acquisition

We face a variety of risks related to our

entry into a new line of business following the completion of the Moser Acquisition.

Our entry into scaled distributed power solutions

is expected to enhance our position as a mobile equipment and logistics solution provider to the oil and natural gas industry as well

as diversify our business.

Entry into a new line of business may also subject

us to new laws and regulations with which we are not familiar and may lead to increased litigation and regulatory risk. Further, our management

team has not directly engaged in the distributed power solutions business before, and its lack of experience may result in delays or further

complications to the new business. If we are unable to successfully implement the acquired business of Moser, our revenue and profitability

may not grow as we expect, our competitiveness may be materially and adversely affected, and our reputation and business may be harmed.

The market price for our common stock following

the closing of the Moser Acquisition may be affected by factors different from those that historically have affected or currently affect

our common stock.

Our results of operations following the completion

of the Moser Acquisition may be affected by some factors that are different from those that have affected our results of operations in

the past. Accordingly, the market price and performance of our common stock is likely to be different from the performance of our common

stock in the absence of the Moser Acquisition. In addition, general fluctuations in stock markets could have a material adverse effect

on the market for, or liquidity of, our common stock, regardless of our actual operating performance.

Our newly acquired power solutions segment

is dependent on its relationships with key suppliers to obtain equipment for its business.

Our power generation business is dependent

on a sole key supplier for access to the unique equipment used in the provision of our power solutions offering. If we fail to

maintain an adequate relationship with this supplier, if we fail to receive equipment from this supplier in a timely manner or, if

we are required to find an alternative supplier of equipment, then our competitive position may be harmed and our operations,

financial conditions and/or cash flows may be negatively impacted.

In addition, the prices of certain equipment may

continue to experience inflationary pressures, which may be exacerbated by our reliance on a single key supplier, that could further increase

such costs. We may not be able to pass on these costs to our customers, which could have a material adverse impact on our results of operations,

financial condition or cash flows.

Unavailability of, and lengthy delays in

obtaining, the necessary equipment may result from a number of factors affecting our supplier including capacity constraints, labor

shortages or disputes, supplier product quality issues and our supplier’s allocations to other purchasers. These risks can be

magnified in a weak economic environment or following increases in demand arising from an economic downturn, but are also generally

present due to the nature of our business and its dependence on highly-specialized equipment. Such disruptions could result in our

inability to effectively meet the needs of our customers and could result in a material adverse effect on our operations, financial

condition or cash flows.

Many of our power systems involve long sales

cycles.

The sales cycle for our power systems, from initial

contact with potential customers to the commencement of field delivery, may be lengthy. Customers generally consider a wide range of solutions

before making a decision to rent or to purchase power systems. Before a customer commits to rent or purchase power systems, they often

require a significant technical review, assessment of competitive offerings and approval at a number of management levels within their

organization. During the time our customers are evaluating our power solutions offerings, we may incur substantial sales and marketing,