SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 6-K

REPORT OF FOREIGN PRIVATE ISSUER PURSUANT

TO RULE 13A-16

OR 15D-16 OF THE SECURITIES EXCHANGE ACT OF 1934

For the month of November, 2023

(Commission File No. 1-14862 )

BRASKEM S.A.

(Exact Name as Specified in its Charter)

N/A

(Translation of registrant's name into English)

Rua Eteno, 1561, Polo Petroquimico de Camacari

Camacari, Bahia - CEP 42810-000 Brazil

(Address of principal executive offices)

Indicate by check mark whether the registrant

files or will file annual reports under cover Form 20-F or Form 40-F.

Form 20-F ___X___ Form 40-F ______

Indicate by check mark if the registrant is

submitting the Form 6-K

in paper as permitted by Regulation S-T Rule 101(b)(1). _____

Indicate by check mark if the registrant is

submitting the Form 6-K

in paper as permitted by Regulation S-T Rule 101(b)(7). _____

Indicate by check mark whether the

registrant by furnishing the information contained in this Form is also thereby furnishing the information to the Commission pursuant

to Rule 12g3-2(b) under the Securities Exchange Act of 1934.

Yes ______ No ___X___

If "Yes" is marked, indicate below

the file number assigned to the registrant in connection with Rule 12g3-2(b): 82- _____.

CONTENTS

| 1. 3Q23 HIGHLIGHTS |

5 |

| 2. KEY INDICATORS |

6 |

| 3. MESSAGE FROM MANAGEMENT |

7 |

| 4. GLOBAL PETROCHEMICAL INDUSTRY |

8 |

| 5. PERFORMANCE BY SEGMENT |

10 |

| 5.1 BRAZIL |

10 |

| 5.2 UNITED STATES & EUROPE |

17 |

| 5.3 MEXICO |

19 |

| 6. CONSOLIDATED FINANCIAL OVERVIEW |

25 |

| 6.1 CONSOLIDATED REVENUE |

26 |

| 6.2 COST OF GOODS SOLD (COGS) |

26 |

| 6.3 OTHER REVENUE (EXPENSE), NET |

27 |

| 6.4 RECURRING EBITDA |

27 |

| 6.5 CONSOLIDATED FINANCIAL RESULT |

28 |

| 6.6 NET INCOME (LOSS) |

29 |

| 6.7 INVESTMENTS |

29 |

| 6.8 CASH FLOW |

31 |

| 6.9 DEBT MATURITY PROFILE AND RATING |

32 |

| 7. CAPITAL MARKETS |

33 |

| 8. LIST OF ANNEXES: |

35 |

FORWARD-LOOKING STATEMENTS

This Earnings Release may

contain forward-looking statements. These statements are not historical facts, but rather are based on the current view and estimates

of the Company's management regarding future economic and other circumstances, industry conditions, financial performance and results,

including any potential or projected impact regarding the geological event in Alagoas and related legal procedures on the Company's business,

financial condition and operating results. The words “project,” “believe,” “estimate,” “expect,”

“plan”, “objective” and other similar expressions, when referring to the Company, are used to identify forward-looking

statements. Statements related to the possible outcome of legal and administrative proceedings, implementation of operational and financing

strategies and investment plans, guidance on future operations, the objective of expanding its efforts to achieve the sustainable macro

objectives disclosed by the Company, as well as factors or trends that affect the financial condition, liquidity or operating results

of the Company are examples of forward-looking statements. Such statements reflect the current views of the Company's management and are

subject to various risks and uncertainties, many of which are beyond the Company’s control. There is no guarantee that the events,

trends or expected results will actually occur. The statements are based on various assumptions and factors, including, but not limited

to, general economic and market conditions, industry conditions and operating factors, availability, development and financial access

to new technologies. Any change in these assumptions or factors, including the projected impact from the joint venture and its development

of technologies, from the geological event in Alagoas and related legal procedures and the unprecedented impact on businesses, employees,

service providers, shareholders, investors and other stakeholders of the Company could cause effective results to differ significantly

from current expectations. For a comprehensive description of the risks and other factors that could impact any forward-looking statements

in this document, especially the factors discussed in the sections, see the reports filed with the Brazilian Securities and Exchange Commission

(CVM). This Earnings Release does not constitute any offer of securities for sale in Brazil. No securities may be offered or sold in Brazil

without being registered or exempted from registration, and any public offer of securities carried out in Brazil must be made through

a prospectus, which would be made available by Braskem and contain detailed information on Braskem and its management, as well as its

financial statements.

BRASKEM S.A. (B3:

BRKM3, BRKM5 and BRKM6; NYSE: BAK; LATIBEX: XBRK), the leading resins producer in the Americas and the world leader in biopolymers, announces

the calendar for its 3Q23 disclosures, as follows.

Conference

Call

|

Portuguese (Original

Audio)

November 9, 2023 (Thursday)

Time: 11:00 a.m. (Brasília)

Telephone:

+55 (11) 4090 1621

Dial-in: Braskem

Webcast:

Click here |

|

English (Simultaneous

Translation)

November 9, 2023 (Thursday)

Time:

9:00 a.m. (US ET), 2:00 p.m. (London)

Telephone:

+1 (412) 717-9627

Dial-in: Braskem

Webcast:

Click here |

Investor

Relations Channels

Investor

Relations Website: http://ri.braskem.com.br

IR mailbox:

braskem-ri@braskem.com.br

Telephone:

+55 (11) 3576-9531

Braskem

Invest: podcast for investors, available on Spotify (in Portuguese) in this

link.

Braskem’s Recurring EBITDA

in the quarter was US$187 million, 34% higher than 2Q23

Green PE’s operational

performance was above nominal capacity of 260,000 tons/year with utilization rate of 108% in the quarter

| 3. | MESSAGE FROM MANAGEMENT |

During the third quarter

of 2023, global demand remained at historical low levels due to (i) lower global consumption resulting from high interest rates and inflationary

pressures; and (ii) the industrial slowdown in major economies such as the Euro Zone, China and United States, which contracted 1.7% and

5.6%, and expanded 0.6%, lower than historical level, respectively. Additionally, the continuous addition of new PE and PP capacities

in the United States and China continued to put pressure on petrochemical spreads in the international market, resulting in lower spreads

in the quarter when compared to 2Q23. Specifically, while looking into the spreads path during the quarter, some petrochemical spreads

showed an upward trend between the months of July and September mainly due to the increase in the price of petrochemical resins in the

international market as a consequence of the increase in the oil and naphtha prices after the announcements of cuts in oil production

by OPEC1, impacting the production cost of the marginal producers.

Regarding the Company’s

operating performance, the utilization rates of petrochemical complexes in Brazil and Mexico were affected by operational instabilities

caused by external factors, such as power outages in some regions of Brazil, unscheduled shutdowns at customers of main chemicals in Brazil,

failures in the electricity grid due to thunderstorms in the region of the Mexican petrochemical complex as well as lower ethane availability

from PEMEX. In this scenario, the Company optimized its inventory management process and increased its resins sales’ volume in Brazil,

which were above the growth of the Brazilian resin demand while maintaining its PE sales’ volume in Mexico. In the United States

and Europe segment, the utilization rate and sales volume remained stable in relation to 2Q23. It is worth highlighting the operational

performance of Green PE above its nominal capacity. This increased operating rate is the outcome after the conclusion of the ramp-up process

of the expanded capacity and the implementation of industrial efficiency initiatives, which enabled an increase in sales volume in the

period.

In the nine months ended

in September, Brazilian imports of chemical products increased, pushing down domestic production to the lowest level in 17 years, which

affected utilization rates of the entire industry and sales of chemicals for industrial use by Brazilian producers. In this regard, it

is important to highlight the execution of a decree regulating the Special Regime for the Chemical Industry (REIQ) in Brazil. The reinstatement

of REIQ improves the competitiveness of the sector that creates 2 million jobs across the country and accounts for 11% of Brazil’s

industrial GDP2.

In this context, the Recurring

EBITDA for the third quarter was US$187 million (R$921 million), an increase of 34% in relation to the previous quarter, mainly due to:

(i) the increase in sales volume of resins in Brazil due to the increase in demand for resins in the Brazilian market; (ii) the increase

in Brazil’s segment resin exports due to better opportunities in the international market; (iii) the posting of REIQ tax credits

from January to September, 2023 in the Profit and Loss; and (iv) the increase in PP sales volume in the United States and Europe’s

segment.

In the quarter, the Company

continued to implement financial preservation initiatives by issuing a bond in the international market in the amount of US$850 million

with a seven-year term. It is important to highlight that the Company’s debt profile remains very long and its cash position is

solid, enough to cover debt maturities over the next 75 months.

Finally, Braskem and its

Team Members remain focused on the implementation of different initiatives to maximize cash generation as well as prioritizing investments

aligned with its growth strategy avenues, named traditional business, bio-based and recycling.

1 Organization

of the Petroleum Exporting Countries (OPEC)

2 Data

from Brazilian Chemical Manufacturers’ Association (ABIQUIM)

| 4. | GLOBAL PETROCHEMICAL INDUSTRY |

Petrochemical

Spreads – 3Q23 vs. 2Q23

BRAZIL

PE spreads decreased

(-23%) in relation to 2Q23, impacted by lower PE prices in the U.S. (-6%) and explained by (i) the lower demand in the period related

to macroeconomic factors, such as persistent inflationary pressures; and (ii) the higher product supply in the region with the startup

of new capacities. Naphtha ARA price increased (+6%) in relation to 2Q23, due to the increase in oil prices during the period (+11%) as

a consequence of the announcements of cuts in oil production by OPEC to align supply with lower global demand.

PP spreads decreased

(-22%) in relation to 2Q23, impacted by lower PP prices in Asia (-4%), explained by (i) the weaker demand associated with the global economic

slowdown; and (ii) the higher product supply in the region, resulting from the startup of new capacities in China. The impacts of the

naphtha ARA price explained above is applicable to the PP spreads.

PVC Par spreads

were lower (-20%) in relation to 2Q23. PVC prices in Asia remained in line compared to 2Q23. On the other hand, caustic soda prices in

the U.S. decreased (-34%) in relation to 2Q23, due to the lower demand, mainly in the pulp and paper and aluminum sectors, which resulted

in higher product availability in the international market, mainly in United States, as well as higher products supply at competitive

prices from Asian producers.

Spreads on Main

Basic Chemicals were lower (-24%) than in the previous quarter, mainly due to the increase in the naphtha ARA price (+6%) during the

period, as explained above. The price of main chemicals was lower (-8%) in relation to 2Q23, impacted mainly by (i) the lower price of

butadiene (-40%) in the period that was caused by lower demand for rubber as well as a higher supply with the startup of new petrochemical

complexes in Asia; (ii) the lower price of benzene (-16%) as a consequence of higher product availability in the United States due to

higher imports supply from Asia; (iii) the lower price of ethylene (-6%) resulting from lower demand in Europe and competition with the

imported product with competitive prices in the region; and the positive impact of higher gasoline prices (+6%) during the period, mainly

due to the increase in oil price during 3Q23 and a higher demand as a result of the driving season in the U.S.

UNITED STATES & EUROPE

PP spreads in the

U.S. remained in line with 2Q23. PP spreads in Europe were lower (-8%) than 2Q23, due to lower PP prices in Europe (-8%). The

spreads were impacted by (i) the weaker demand given high levels of inflation and interest rates in the region; and (ii) the entrance

of imported products with a more competitive production costs in the region. Propylene prices in Europe also decreased (-8%) compared

to 2Q23, due to lower demand, also influenced by macroeconomic factors.

MEXICO

PE spreads in Mexico

were lower (-16%) when compared to 2Q23, impacted by lower PE prices in the U.S. (-7%), as explained on the Brazilian spreads. Ethane

prices increased (+40%) impacted by the natural gas supply and demand dynamics in the United States, given that natural gas contains ethane

in its composition. This dynamic is explained by the lower supply of natural gas in the United States as a result of a lower availability

due to operational issues in the pipelines due to higher temperatures during the summer, which restricted the ethane extraction.

For more information

on the petrochemical scenario in the quarter, see appendix 8.1.

Recurring EBITDA was US$115

million (R$572 million), higher than 2Q23 (+42%) and accounting for 63% of the Company’s segment consolidated recurring EBITDA,

mainly due to (i) the increase in sales volume of resins in Brazil of 95,000 tons, or 12%, due to the 9% increase in demand for resins

in the Brazilian market; (ii) the increase of 35,000 tons, or 20%, in resins’ exports; and (iii) the recording of US$60 million

(R$297 million) related to the REIQ tax credits from January to September, 2023.

Compared to 3Q22, Recurring

EBITDA in U.S. dollar decreased 63%, mainly due to (i) the reduction in the international market of 38% in PE spread, of 15% in PP spread,

of 51% in PVC spread Par and 43% in main chemicals spread; and (ii) the reduction of 143,000 tons, or 21%, in the sales volume of

the main chemicals in the Brazilian market and of 34,000 tons, or 28%, in the exports of main chemicals. In Brazilian real, the 65% reduction

is also explained by the appreciation in the average of the Brazilian real against the U.S. dollar during the period of 7%.

| 5.1.1 | OPERATIONAL OVERVIEW |

a) Demand for resins

in Brazil (PE, PP and PVC): in relation to 2Q23, demand for resins in the Brazilian market increased (+9%), due to (i) seasonality,

driven by the home appliances, packaging, consumer goods, beverage and hygiene sectors; and (ii) higher demand for PVC driven by the milestone

of sanitation and the construction sector. Compared to 3Q22, demand for resins decreased (-2%), mainly for PE and PP, explained by the

lower consumption of the packaging sector.

b) Average utilization

rate of petrochemical plants: reduction in relation to 2Q23 (-4 p.p.) and in relation to 3Q22 (-10 p.p.) due to (i) the continuous

adjustment of production in light of global demand, with emphasis on the unscheduled shutdowns of chemical customers in Brazil; (ii) unscheduled

shutdowns related to power outages in some regions of the country; (iii) operational instabilities in the PE units in Rio Grande do Sul;

and (iv) the process of returning to operations after a scheduled pit-stop at the Rio de Janeiro plant.

c) Resin sales volume:

in the Brazilian market, resin sales increased in relation to 2Q23 (+12%) due to the seasonality effect of the period, driven mainly by

the household appliances, packaging, consumer goods, beverages, hygiene, civil construction sectors, and the milestone of sanitation.

Compared to 3Q22, resin sales volume in the Brazilian market remained in line.

In 3Q23, exports were

higher when compared to 2Q23 (+20%) and 3Q22 (+9%) due to the expectation of price increases in the international market, supporting the

decision to build inventories in the transformation chain.

d)

Sales volume of main chemicals3:

in the Brazilian market, sales were lower compared to 2Q23 (-10%), mainly explained by the lower sales volume (i) of propylene and paraxylene

due to the scheduled shutdown of customers in the period; and (ii) of gasoline due to lower product availability for sale. In relation

to 3Q22, the reduction (-21%) is explained by the lower product availability for sale, given the lower utilization rate in the period.

Exports decreased compared

to 2Q23 (-16%) and 3Q22 (-28%), mainly due to the lower product availability for sale, which was partially offset by better commercial

opportunities in the international gasoline market.

3 Main

chemicals refer to ethylene, propylene, butadiene, cumene, gasoline, benzene, toluene and paraxylene due to the share of these products

in net revenue of this segment.

| 5.1.2 | GEOLOGICAL EVENT IN ALAGOAS |

The Management of Braskem,

based on its assessment and that of its external advisors, considering the measures recommended on technical studies in the short and

long-term and the existing information and refined estimates of expenses for implementing several measures connected with the geological

event in Alagoas, the provision shows the following changes in the period ended September 30, 2023:

For more information

on advances made on the action fronts related to the geological event in Alagoas during the quarter, see appendix 8.2.

A) Net Revenue: decreased

in U.S. dollar (-6%) and Brazilian real (-8%) in relation to 2Q23 explained by (i) the reduction of 6% in PE prices, 4% in PP prices and

8% in the average price of the main chemicals in the international market; and (ii) the reduction of 59,000 tons, or 10%, in the

sales volume of the main chemicals in the Brazilian market and of 17,000 tons, or 16%, in the exports of main chemicals. In Brazilian

real, the reduction is also explained by the appreciation in the average of the Brazilian real against the U.S. dollar during the period

of 1.4%.

Compared to 3Q22, the decrease

in U.S. dollar (-32%) and Brazilian real (-36%) is explained by (i) the reduction of 23% in PE prices, 9% in PP prices, 16% in PVC prices

and 24% in the average price of the main chemicals in the international market; and (ii) the reduction of 143,000 tons, or 21%, in

the sales volume of the main chemicals in the Brazilian market and of 34,000 tons, or 28%, in exports of main chemicals. These combined

effects resulted in a R$5.2 billion reduction in net revenue. In Brazilian real, the reduction is also explained by the appreciation in

the average of the Brazilian real against the U.S. dollar during the period of 7%.

Resin sales by sector (%)

Resin sales by region (% in tons)

B) Cost of Goods

Sold (COGS): decreased in U.S. dollar (-8%) and Brazilian real (-9%) in relation to 2Q23, mainly due to (i) the inventory effect of

naphtha acquired in previous periods; and (ii) the reduction of 59,000 tons, or 10%, in the sales volume of main chemicals in the

Brazilian market and of 17,000 tons, or 16%, in exports of main chemicals. In Brazilian real, the reduction is also explained by the appreciation

in the average of the Brazilian real against the U.S. dollar during the period of 1.4%.

Compared to 3Q22, the reduction

in U.S. dollar (-26%) and Brazilian real (-32%) is mainly explained by (i) the 7%, 46% and 37% decrease, respectively, in naphtha, ethane

and propane prices in the international market, based on the moving average; and (ii) the reduction of 143,000 tons, or 21%, in the

sales volume of the main chemicals in the Brazilian market and of 34,000 tons, or 28%, in exports of main chemicals. In Brazilian real,

the reduction is also explained by the appreciation in the average of the Brazilian real against the U.S. dollar during the period of

7%.

In the quarter, COGS

was affected by the Reintegra tax credit totaling approximately US$0.4 million (R$2.1 million).

In August, as established

in Federal Law 14,374/2022 and through Decree 11,668/2023, the Federal Government regulated the necessary conditions for the use of the

Special Regime for the Chemical Industry (REIQ), which have a retroactive effect as of January 1, 2023. The Company, through an exhaustive

analysis met all the requirements of said decree and therefore filed a statement of commitment in September with the Brazilian Federal

Revenue Office. As a consequence of this filing, US$60 million (R$297 million) related to the calculation of tax credits from January

to September, 2023 were posted in the books during the quarter.

C) SG&A EXPENSES:

in U.S. dollar, the increase in relation to 2Q23 (+11%) is due to higher product sales expenses and expenses with third parties. Compared

to 3Q22, SG&A expenses remained stable.

D) Recurring EBITDA:

represented 63% of the Company’s segment consolidated Recurring EBITDA.

| 5.1.4.1 | OPERATIONAL OVERVIEW |

a)

Utilization rate (Green Ethylene)4:

increase in relation to 2Q23 (+24 p.p.) and in relation to 3Q22 (+6 p.p.) explained mainly due to (i) the conclusion of the ramp-up process

considering the expansion of 60,000 tons in the production capacity of the green ethylene unit in Rio Grande do Sul; and (ii) operational

performance above nominal capacity in the period, as a result of industrial efficiency initiatives implemented during the scheduled shutdown

carried out in 1H23.

4 Due

to the conclusion of the project to expand of 60,000 tons of green ethylene capacity at the Rio Grande do Sul unit, the calculation of

the utilization rate considers the production capacity of (i) 200,000 tons/year for 3Q22; (ii) 228,000 tons/year for 2Q23; and (iii) 260,000

tons/year for 3Q23.

b) Green PE sales volume:

increased in comparison to 2Q23 (+48%) and 3Q22 (+9%) due to higher product availability for sale, given the higher utilization rate in

the period.

| 5.1.4.2 | FINANCIAL OVERVIEW |

A)

Net Revenue of Green PE and ETBE5:

increased from 2Q23 (+23%) mainly due to higher ETBE and Green PE sales volume, and higher ETBE prices in the period. Compared to 3Q22,

net revenue decreased (-6%) due to the lower green PE prices and ETBE sales volume, partially offset by the higher green PE sales volume

resulting from higher product availability for sale.

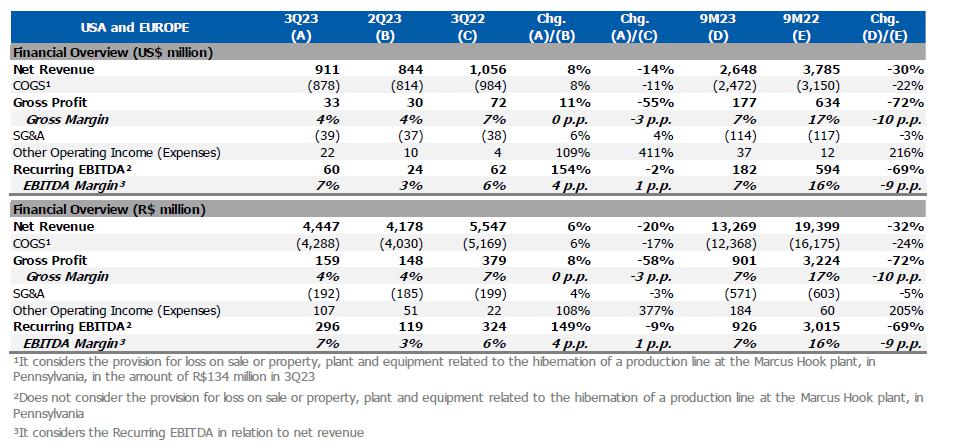

| 5.2 | UNITED STATES & EUROPE |

Recurring EBITDA was US$60 million

(R$296 million), 154% higher than 2Q23, accounting for 33% of the Company’s segment consolidated Recurring EBITDA, due to (i) the

increase of 7,000 tons, or 1%, in PP sales volume during the period; (ii) the flexibility in purchasing propylene in the United States;

and (iii) the lower inventory effect of finished goods produced in prior periods due to a less volatile feedstock price in the United

States within the quarter.

}In

relation to 3Q22, Recurring EBITDA decreased 2% in U.S. dollar, mainly explained by the 54% reduction in the average of PP spread in the

United States and Europe. In Brazilian real, the 9% reduction is also explained by the appreciation in the average of the Brazilian real

against the U.S. dollar during the period of 7%.

| 5.2.1 | OPERATIONAL OVERVIEW |

a) PP demand:

in relation to 2Q23, PP demand in the United States increased (+3%) explained

by the continued rebuilding of inventories in the transformation chain that started in 2Q23, after the destocking process across the chain

observed in previous quarters. Compared to 3Q22, PP demand remained stable.

In Europe, PP demand was lower

(-5%) when compared to 2Q23 due to seasonality. In relation to 3Q22, the increase in demand (+6%) is explained by lower demand observed

due to (i) lower consumption given high levels of inflation; and (ii) high levels of inventories across the transformation chain during

the same period of the previous year.

b) Average utilization

rate of PP plants: remained in line with 2Q23. Production in the United States was higher due to the return of operations after a

scheduled maintenance shutdown in 2Q23. In Europe, production volume was lower due to the lower feedstock availability and the planned

maintenance shutdown at one of the plants in the region.

Compared to 3Q22, the

average utilization rate increased (+6 p.p.) due to shutdowns at PP plants in that period.

5 Product

that uses a renewable feedstock, ethanol, in its composition

c) PP sales volume:

remained in line with 2Q23. In relation to 3Q22, the higher sales volume (+7%) is mainly explained by the chain destocking process

that occurred in 3Q22 due to the impacts of the global economic slowdown.

A) Net Revenue: higher

in U.S. dollar (+8%) and Brazilian real (+6%) compared to 2Q23, given the increase of 7,000 tons, or 1%, in PP sales volume during the

period.

Compared to 3Q22, net revenue

was lower in U.S. dollar (-14%) and Brazilian real (-20%), mainly due to the 36% reduction in average PP prices in the international market.

In Brazilian real, the reduction is also explained by the appreciation in the average of the Brazilian real against the U.S. dollar during

the period of 7%.

B) Cost of Goods Sold

(COGS): higher in U.S. dollar (+8%) and Brazilian real (+6%) in relation to 2Q23, explained by (i) the recognition of provision for

loss on sale or property, plant and equipment in the United States; and (ii) the increase of 7,000 tons, or 1%, in PP sales volume. These

impacts were partially offset by the flexibility in propylene purchases and the lower inventory effect of finished goods produced in prior

periods due to a less volatile feedstock price in the United States within the quarter.

In September 2023, COGS in

the United States was affected by the recognition of a provision for loss on sale or property, plant and equipment due to the hibernation

of a 207,000 tons/year production line at the Marcus Hook plant in Pennsylvania. The hibernation of this line is to ensure the long-term

resilience of the United States amid continuing global economic uncertainty and a trough in the chemical industry business cycle.

Compared to 3Q22, the decrease

in U.S. dollar (-11%) and Brazilian real (-17%) is mainly explained by the 21% decrease in average propylene prices, based on the moving

average, in the international market in the United States and Europe. In Brazilian real, is also explained by the appreciation in the

average of the Brazilian real against the U.S. dollar during the period of 7%.

C) SG&A EXPENSES:

in U.S. dollar, increase in relation to 2Q23 (+6%) due to higher sales volume and higher expenses with third parties. In relation to 3Q22,

the increase (+4%) is explained by higher expenses with industrial and building services and IT services.

D) Recurring EBITDA:

Represented 33% of the Company’s segment consolidated Recurring EBITDA.

Recurring EBITDA was US$8

million (R$36 million), 81% lower when compared to 2Q23, accounting for 4% of the Company’s segment consolidated Recurring EBITDA.

This decrease is explained mainly by (i) the 16% decrease in PE spreads in the international

market during the period; and (ii) the 40% and 20% increase, respectively, in ethane and natural gas costs in the international market.

Compared to 3Q22, Recurring

EBITDA decreased 45% in U.S. dollar, mainly explained by the 7% decrease in PE spreads in the international market during the period.

In Brazilian real, the 51% reduction is also explained by the appreciation in the average of the Brazilian real against the U.S. dollar

during the period of 7%.

| 5.3.1 | OPERATIONAL OVERVIEW |

a) PE demand in

Mexico: demand for resins increased in 3Q23 in relation to 2Q23 (+10%), due to the rebuilding of inventories because of the expected

price increases in the international market in subsequent periods. Compared to 3Q22, demand was higher (+6%) driven by the rebuilding

of inventories, given lower volumes across the chain in relation to the same period last year.

b) Average utilization

rate of PE plants: lower compared to 2Q23 (-20 p.p.) and compared to 3Q22 (-10 p.p.) due to (i) unscheduled shutdowns due to failures

in the national electrical system caused by electrical storms occurred in the region; and (ii) lower ethane availability from PEMEX. During

the period, Pemex's average ethane supply was 26 thousand barrels per day, and the average ethane imported through the Fast Track solution

was 17 thousand barrels per day.

c) PE sales volume:

despite the lower utilization rate of the petrochemical plant in the period, sales volume remained in line when compared to 2Q23 due to

inventory optimization. In relation to 3Q22, the increase (+19%) is explained by higher demand in the period, driven by the replenishment

of the chain's inventories.

A) Net Revenue: decreased

in U.S. dollar (-10%) and Brazilian real (-11%) in relation to 2Q23, mainly due to the 7% reduction in PE prices in the international

market. In Brazilian real, the reduction is also explained by the appreciation in the average of the Brazilian real against the U.S. dollar

during the period of 1.4%.

Compared to 3Q22, the decrease

in U.S. dollar (-17%) and Brazilian real (-23%) is explained, mainly, due to the 21% reduction in PE prices in the international market.

In Brazilian real, the reduction is also explained by the appreciation in the average of the Brazilian real against the U.S. dollar during

the period of 7%.

Sales by sector (%)

Sales by region (% in

tons)

B) Cost of Goods Sold

(COGS): higher in U.S. dollar (+6%) and Brazilian real (+5%) when compared to 2Q23, mainly due to the 40% and 20% increase of prices

in the international market, based on moving average, of ethane and natural gas, respectively.

Compared to 3Q22, the decrease

in U.S. dollar (-11%) and Brazilian real (-17%) is mainly explained by the reduction of 46% and 64% in ethane and natural gas prices in

the international market, respectively, based on the moving average. In Brazilian real, the reduction is also explained by the appreciation

in the average of the Brazilian real against the U.S. dollar during the period of 7%.

C) SG&A EXPENSES:

in U.S. dollar, the increase in relation to 2Q23 (+46%) and 3Q22 (+94%) is mainly explained by the increase in operating expenses with

logistics, storage, tanking and third parties.

D) Recurring EBITDA:

Represented 4% of the Company’s segment consolidated Recurring EBITDA.

Investments planned by

Braskem Idesa for 2023 is of US$112 million (R$618 million). At the end of 9M23, Braskem Idesa had invested approximately US$90 million

(R$449 million).

Operating Investments

in 3Q23: the main operating investments made by Braskem Idesa were in reliability initiatives and spare parts.

Strategic Investments

in 3Q23: strategic investments refer to the ongoing construction of the ethane import terminal through the Terminal Química

Puerto México, which exceeded expectations for the year due to additional disbursements until the conclusion of project financing.

| 5.3.3.1 | ETHANE IMPORT TERMINAL |

In September 2021,

Braskem Idesa approved and started the Ethane Import Terminal construction project in Mexico, which involves building an ethane

import terminal with capacity of 80,000 barrels of ethane per day, enabling Braskem Idesa to operate at 100% of its capacity. In

December 2021, the subsidiary Terminal Química Puerto México (“TQPM”) was formed, which is the company

responsible for building and operating the terminal. In June 2022, Braskem Idesa

announced the sale of 50% of the capital of TQPM to form a joint venture with Advario B.V., a global leader in the storage sector.

On

March 1, 2023, Braskem Idesa met all the conditions for concluding the investment agreement signed with Advario, receiving payment of

US$56 million6 referring to the retroactive

capital contribution equivalent to the 50% ownership interest in TQPM's capital disbursed by Braskem Idesa as of said date, corresponding

to US$112 million6. In addition, the estimated investment for building TQPM was updated to US$446 million, after reviewing

project costs and finalizing mandatory activities. In April 2023, the laying of the cornerstone ceremony was carried out with the participation

of federal and local authorities in Mexico and, in July 2023, the Energy Regulation Commission (CRE) approved the operating permit. Finally,

on November 1, 2023, Braskem Idesa concluded through its subsidiary TQPM the process to obtain the financing of US$408 million for the

construction of the terminal. Such financing, in the Syndicated Project Finance Loan modality, was issued by TQPM with the support of

both shareholders, Braskem Idesa and Advario, with 5-year term deal and with usual guarantees for transactions of this nature.

The

project, whose construction phase was launched in July 2022, reached 48% of physical completion as of October 2023. The total amount disbursed

by Braskem Idesa as of September 2023 was around US$103 million7 since

the beginning of the project, being that of this total the amount of US$58 million was disbursed in the 9M23, with startup expected in

the second half of 2024.

| 5.3.4 | DEBT MATURITY PROFILE AND RATING |

On September

30, 2023, the average debt term was around 7.1 years, with 93% of the maturities concentrated from 2029. Braskem

Idesa’s average weighted cost of debt was exchange variation plus 7.3% p.a.

The liquidity position of

US$287 million is enough to cover the payment of all liabilities coming due in the next 37 months.

6 The amounts

disbursed by Braskem Idesa include Value Added Tax (VAT).

7 Considers

the reimbursement made by Advario in the amount of US$56 million and it includes Value Added Tax (VAT).

Ratings

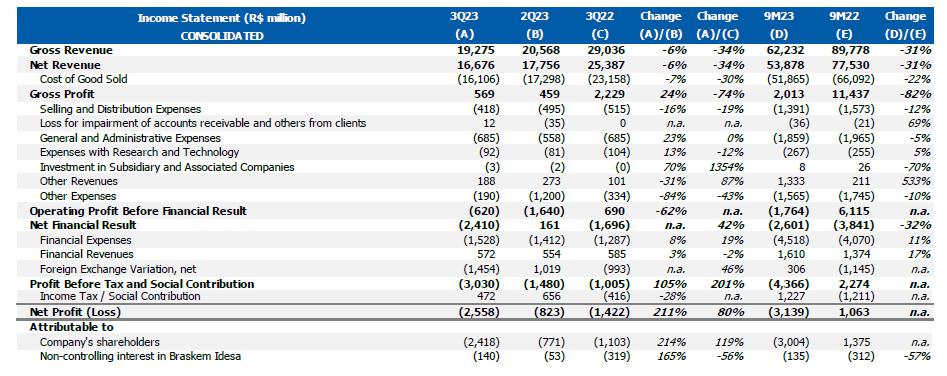

| 6. | CONSOLIDATED FINANCIAL OVERVIEW |

| 6.2 | COST OF GOODS SOLD (COGS) |

| 6.3 | OTHER REVENUE (EXPENSE), NET |

The Company recorded in 3Q23

a total net expense of R$2 million, mainly due to the adjustment in the accounting provision for the geological event in Alagoas, as described

in appendix 8.2, which was partially offset by (i) the recovery of taxes related to the Reintegra tax benefit; and (ii) the other revenues

related to the sale of sundry materials and inputs and the monetization of credit rights.

The Company’s

Recurring EBITDA in 3Q23 was US$187 million (R$921 million), 34% higher than 2Q23, mainly due to (i) the increase in sales volume of resins

in Brazil of 95,000 tons, or 12%, due to the 9% increase in demand for resins in the Brazilian market; (ii) the increase of 35,000 tons,

or 20%, in resin exports in the Brazil segment; (iii) the recognition in the result of US$60 million (R$297 million) related to the REIQ

tax credits from January to September, 2023; and (iv) the increase of 7,000 tons in

PP sales volume in the United States and Europe segment.

In relation to 3Q22, Recurring

EBITDA was lower in U.S. dollar (-50%) and Brazilian real (-53%) mainly due to (i) the decrease in spreads in the international market

of 43% in main chemicals, 38% in PE, 15% in PP, 51% in PVC spread Par in Brazil, 59% in PP in the United States and 7% in PE in Mexico’s

segment; (ii) the reduction of 143,000 tons, or 21%, in the sales volume of main chemicals in the Brazilian market and of 34,000

tons, or 28%, in the exports of main chemicals in the Brazil segment; and (iii) the appreciation in the average of the Brazilian real

against the U.S. dollar during the period of 7%. These effects were partially offset by the increase of 18,000 tons, or 9%, in resins

exports in Brazil, of 34,000 tons, or 7%, in PP sales volume in the United States and Europe’s segment, and of 34,000 tons, or 19%,

in PE sales volume in Mexico’s segment.

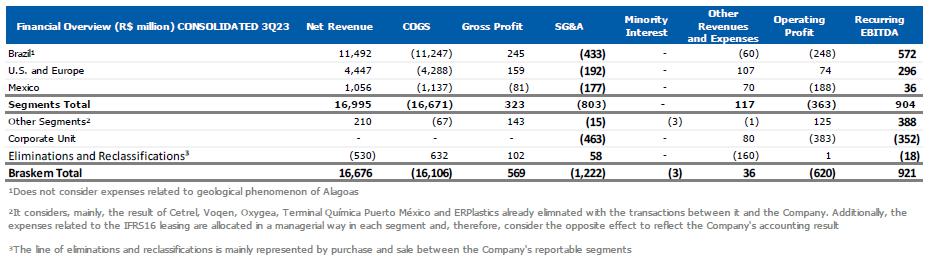

8 Braskem’s

consolidated result corresponds to the sum of the results in Brazil, United States & Europe and Mexico, less eliminations and reclassifications

of purchases and sales among the segments reported by the Company.

| 6.5 | CONSOLIDATED FINANCIAL RESULT |

Financial expenses:

increased in relation to 2Q23 (+8%), mainly due to higher expenses (i) with interest due to the increase in gross debt balance during

the quarter; (ii) with present value adjustment on transactions with third parties; and (iii) with interest on tax liabilities. Compared

to 3Q22, financial expenses increased (+19%), mainly due to higher expenses (i) with interest due to the increase in gross debt balance

between the periods; (ii) with present value adjustment on transactions with third parties; and (iii) financial expenses with derivatives.

Financial revenue:

increase from 2Q23 (+3%), mainly due to higher revenue on financial investments in the Brazilian and international markets due to the

increase in the balance during the period. Compared to 3Q22, financial income decreased (-2%) due to lower returns on financial investments,

given the lower basic interest rate in the period.

Net exchange variation:

positive variation in 3Q23, mainly explained by (i) the effect of depreciation in the end-of-period Brazilian real against the U.S. dollar

on the average net exposure to the currency in the amount of US$4.0 billion; and (ii) the effect of depreciation in the end-of-period

Mexican peso against the U.S. dollar on the average net exposure to the U.S. dollar at Braskem Idesa in the amount of US$2.1 billion.

Transactions in financial

instruments under hedge accounting

In relation to the exports hedge

accounting of Braskem S.A., the Company registered US$200 million (R$395 million) in exports from a discontinued flow from 2019 in the

quarter. The initial designation rate was R$/US$2.0017, defined in March 2013, while the realization rate was R$/US$3.9786, defined in

November 2019. The balance of financial instruments designated for this hedge accounting at the end of 3Q23 was US$4.9 billion.

Regarding the exports hedge

accounting of Braskem Idesa's, the Company registered US$85 million (MXN 550 million) in exports of discontinued flows in the quarter

between 2016 and 2021. The average initial designation rate was MXN/US$13.6533 and the average realization rate was MXN/US$20.1160. The

balance of instruments designated for this hedge accounting at the end of 3Q23 was US$2.2 billion.

Long-term Currency Hedge

Program

Braskem’s feedstock and

products have prices denominated or strongly influenced by international commodity prices, which are usually denominated in U.S. dollar.

Since 2016, Braskem has contracted derivative instruments to mitigate part of the exposure of its cash flow denominated in Brazilian real.

The main purpose of the program is to mitigate U.S. dollar call and put option agreements, thus protecting the estimated flows for a horizon

of up to 18 months.

On September 30, 2023, Braskem

held a long position in puts totaling US$1.7 billion (notional value), at an average strike price of R$/US$4.56. At the same time, the

Company also held a short position in calls totaling US$1.1 billion (notional value), at an average strike price of R$/US$6.90. The contracted

operations have a maximum term of 18 months. The fair value of these Zero Cost Collar (“ZCC”) operations was positive in R$5.1

million at the end of the quarter.

Due to higher volatility of

the dollar during the period, options were exercised. The total effect on cash flow for 3Q23 was a gain of R$15.3 million in the quarter.

In

the quarter, the Company reported net loss9 of

US$497 million, or R$2.4 billion, mainly due to the impact of exchange variation on the financial result caused by the depreciation of

the end-of-period Brazilian real against the U.S. dollar of 4% on the net exposure in the amount of US$4.0 billion. In the year, the Company

recorded net loss attributable to shareholders of US$618 million, or R$3.0 billion.

The corporate investment

planned by Braskem for 2023 is of US$724 million (R$4.0 billion). At the end of 9M23, Braskem had made investments of approximately US$526

million (R$2.6 billion).

Operating Investments

in 3Q23: the main operating investments made in the quarter include (i) pre-scheduled maintenance shutdown of the petrochemical

cracker in Bahia; (ii) the construction of a new fire-fighting water reservoir at the Santo André Industrial Complex; (iii) the

construction of a new R&D facility in Boston, United States, focused on biotechnology,

chemical catalysis and open innovation; and

(iv) the investments related to increasing the reliability and operating safety of industrial assets.

9 Based

on net income (loss) attributable to the shareholders of the Company.

Strategic Investments

in 3Q23: the funds were mainly allocated to (i) investments related to the acquisition of strategic inputs, including catalysts;

(ii) the installation of a desulfurization unit to reduce atmospheric emissions and increase energy efficiency of the Triunfo Petrochemical

Complex in Rio Grande do Sul; and (iii) the initiatives related to innovation and technology development.

In 3Q23, the main investments

related to the Sustainable Development Macro-Goals were (ii) the projects associated with reducing CO2 emissions and enhancing the energy

efficiency of industrial assets; (ii) the construction of a new fire-fighting water reservoir at the Santo André Industrial Complex;

(iii) the construction of a new R&D facility in Boston, United States, focused on biotechnology, chemical catalysis and open innovation;

and (iv) the industrial safety projects.

| 6.7.1 | GLOBAL GROWTH STRATEGY |

Aligned with the Company's

Corporate Growth Strategy, Braskem continued to focus on the development of several projects related to growth avenues, with emphasis

on the following projects.

| a. | Construction

of an Ethane Import Terminal in Mexico |

The project, whose

construction phase was launched in July 2022, reached 48% of physical completion as of October 2023. The total amount disbursed by Braskem

Idesa as of September 2023 was around US$103 million since the beginning of the project, being that of this total the amount of US$58

million was disbursed in the 9M23, with startup expected in the second half of 2024.

More details about

the project are available in section 5.3.3.1.

| 2. | Bio-based

investments and initiatives: |

| a. | Joint Venture with SCG Chemicals |

In August, Braskem

and SCG Chemicals signed a joint venture agreement to create Braskem Siam Company Limited. Subject to approval by antitrust authorities

and final investment decision by the partners, this joint venture aims to produce green ethylene from bioethanol dehydration, using EtE

EverGreenTM technology. The technology results from the partnership between Lummus Technology LLC and Braskem B.V to develop

and license this technology.

| 3. | Investments

and initiatives in recycling: |

| a. | Expansion of portfolio of products and segments |

| · | In 3Q23, the sales

volume of resins with recycled content in Brazil was higher (+12%) when compared to 2Q23 and 3Q22 (+36%), due to the consolidation of

volumes from Wise Plásticos, a recycling company controlled by Braskem. In Mexico, the sales volume was higher in 3Q23 when compared

to 2Q23 (+25%) and 3Q22 (+88%), due to advancement in the development of new solutions in conjunction with brand owners, such as Colgate

– Mission Hills, L'Oreal, Henkel and Unilever. |

| · | In September, Braskem

and Vitol, a multinational energy and commodities company, announced an agreement to supply circular feedstock, derived from plastic waste.

The agreement provides that Vitol will begin supplying pyrolysis oil to Braskem B.V., produced from the chemical recycling process at

the facilities of WPU - Waste Plastic Upcycling A/S, in Denmark. |

In the quarter, the Company

registered a positive variation in working capital of R$1.3 billion, explained mainly by (i) the optimization of global inventories volume

of finished products and the 6% reduction in average prices of finished product in inventories; and (ii) the increase in the account’s

payable days mainly in optimization initiatives with supplier. This positive effect was offset by higher interest payments mainly on bonds

in the international market, operating and strategic investments made in the period and the payment of income tax and social contribution

due in the quarter, which led to cash consumption of R$329 million in the period.

Adding the disbursements related

to the geological event in Alagoas, the Company registered cash consumption of R$1.4 billion.

| 6.9 | DEBT MATURITY PROFILE AND RATING |

In September 2023, the Company

concluded the issue of bonds in the international market in the amount of US$850 million, maturing in January 2031 and earning interest

of 8.50% p.a. On September 30, 2023, the balance of corporate gross debt was of U$8.5 billion, being 88% denominated in dollars. Regarding

net debt, the balance at the end of 3Q23 was of US$4.9 billion, 5% higher than in 2Q23 due to the balance of corporate gross debt.

On September 30, 2023, the

average corporate debt term was around 12.3 years, with 63% of the maturities concentrated after 2030. The average weighted cost of the

Company’s corporate debt was exchange variation +6.2% p.a.

The liquidity position of

US$3.4 billion in September 2023 is sufficient to cover the payment of all debts coming due in the next 75 months, not considering the

international stand-by credit facility of US$1.0 billion available through 2026.

Ratings

On September 29, 2023,

Braskem’s stock was quoted at R$20.52 (BRKM5) and US$8.21 (BAK). The Company’s shares are listed on the Level

1 corporate governance segment of the B3 – Brasil, Bolsa e Balcão and on the New York Stock Exchange (NYSE) through Level

2 American Depositary Receipts (ADRs), being that each Braskem ADR (BAK) corresponds

to two class “A” preferred shares issued by the Company, and on the Madrid Stock Exchange (LATIBEX) under the ticker XBRK.

| 7.2 | PERFORMANCE OF CORPORATE DEBT SECURITIES |

BRAZIL

| · | PE Spreads10:

decreased in relation to

2Q23 (-23%). |

o

PE prices in the U.S. were lower (-6%) in relation to

2Q23, impacted by (i) the lower demand in the period related to macroeconomic factors, such as persistent inflationary pressures; and

(ii) the higher product supply in the region, resulting from the startup of new capacities.

o

Naphtha ARA prices increased (+6%) in relation to 2Q23,

due to the increase in oil prices during the period (+11%) as a consequence of the announcements of cuts in oil production by OPEC to

align supply with lower global demand.

o

In relation to the same quarter of 2022, spreads declined

(-38%), mainly impacted by lower PE prices (-23%), due to (i) weaker global demand associated with higher inflation and interest rates;

(ii) higher product supply resulting from the continued startup of new capacities in the United States and China; and (iii) the normalization

of international logistics, which reduced maritime freight costs and, consequently, PE prices in the United States.

| · | PP Spreads11:

decreased in relation to

2Q23 (-22%). |

o

PP prices in Asia were lower (-4%) in relation to 2Q23,

impacted by (i) weaker demand associated with the global economic slowdown; and (ii) higher product supply in the region, resulting from

the startup of new capacities in China.

o

The impacts of the naphtha ARA price explained above

is applicable to the PP spreads.

o

In relation to the same quarter in 2022, spreads declined

(-15%), mainly due to lower PP prices (-9%), impacted by (i) weaker global demand associated with higher inflation and interest rates;

and (ii) higher product supply resulting from the startup of new capacities, especially in China.

| · | PVC Par Spreads12:

decreased in relation to

2Q23 (-20%). |

o

PVC prices in Asia remained in line with 2Q23 levels.

On the other hand, caustic soda prices in the U.S. decreased (-34%) in relation to 2Q23, explained by lower demand, mainly in the pulp

and paper and aluminum sectors, which increased product availability in the international market, mainly in the United States, as well

as higher products supply at competitive prices from Asian producers.

o

In relation to 3Q22, PVC Par spreads were lower (-51%),

due to (i) lower PVC prices (-16%) in 3Q23 explained by weaker global demand associated with rising inflation and interest rates and by

lower consumption by real estate and construction sectors, especially in China; and (ii) lower caustic soda prices in the United States

(-57%) explained by the normalization of caustic soda supplies in the international market and the lower demand, mainly in the pulp and

paper and aluminum sectors.

| · | Spreads on Main Basic Chemicals13:

decreased in relation to

2Q23 (-24%). |

o

Spreads on Main Basic Chemicals were lower (-24%) than

previous quarter, impacted by the increase in the naphtha ARA prices (+6%) during the period, as explained above. The price of main chemicals

was lower (-8%) compared to 2Q23, mainly impacted by (i) the lower price of butadiene (-40%) explained by lower demand for rubber as well

as higher supply with the startup of new petrochemicals

complex in Asia; (ii) the

lower price of benzene (-16%) as a consequence of higher product availability in the United States due to higher imports supply from Asia;

(iii) the lower price of ethylene (-6%) explained by lower demand in Europe and competition with the imported product in the region with

more competitive prices; and the positive impact of higher gasoline prices (+6%) during the period, mainly explained by the increase in

oil price and demand, as a result of the driving season in the U.S.

10 (US

PE Price – naphtha ARA price)*82%+(US PE Price – 50% US ethane price – 50% US propane price)*18%.

11 Asia

PP price – Naphtha ARA price.

12 The

PVC Par spread better reflects the profitability of the Vinyls business, which is more profitable compared to the temporary/non-integrated

business model of 2019/20, under which the Company imported EDC and caustic soda to keep serving its customers. Its calculation formula

is: Asia PVC Price + (0.685*US Caustic Soda) - (0.48*Europe Ethylene) - (1.014*Brent).

13 Average

price of base chemicals (Ethylene (20%), Butadiene (10%), Propylene (10%), Cumene (5%), Benzene (20%), Paraxylene (5%), Gasoline (25%)

and Toluene (5%), based on Braskem’s sales volume mix) – naphtha ARA price.

o

Compared to 3Q22, spreads of Main Basic Chemicals were

lower (-43%), mainly impacted by (i) lower prices of chemical products (-24%) caused by lower oil prices during the period (-14%) resulting

from weaker global demand; and (ii) partially offset by lower naphtha ARA prices (-7%) related to weaker global demand from the petrochemical

industry and its relationship with oil prices.

UNITED STATES & EUROPE

| · | U.S. PP Spread14:

in line with 2Q23 levels. |

o

Compared to the same quarter last year, spreads decreased

(-59%) mainly due to lower PP prices (-41%) in the United States, impacted by (i) weaker global demand associated with the economic scenario

of higher inflation and interest rates in the region; and (ii) higher product availability due to the startup of new capacities, especially

in China and the U.S.

| · | Europe PP Spread15:

decreased in relation to

2Q23 (-8%). |

o

PP prices in Europe were lower (-8%) compared to 2Q23,

impacted by (i) weaker demand on account of high inflation and interest rates in the region; and (ii) the entrance of imported products

with a more competitive production costs in the region. Propylene prices in Europe also decreased (-8%) compared to 2Q23, due to lower

demand, also influenced by macroeconomic factors.

o

Compared to the same quarter of the previous year, spreads

were higher (+6%), mainly impacted by the lower propylene prices in Europe (-20%) in 3Q23 as a result of lower demand in the period and

lower costs than 3Q22, after the significant increase caused by the geopolitical conflict between Russia and Ukraine.

MEXICOXICO

TM100 MEXICO

<0

| · | North America PE Spread16:

decreased in relation to

2Q23 (-16%). |

| o | PE prices in the U.S. were lower

(-7%) than 2Q23, as explained on the Brazilian spreads. |

| o | Ethane prices increased (+40%)

impacted by the natural gas supply and demand dynamics in the United States, given that natural gas contains ethane in its composition.

This dynamic is explained by the lower supply of natural gas in the United States as a result of a lower availability due to operational

issues in the pipelines due to higher temperatures during the summer, which restricted the ethane extraction in the region. |

| o | In relation to the same quarter

of the previous year, spreads declined (-7%), mainly impacted by lower PE prices (-21%), due to (i) weaker global demand associated with

higher inflation and interest rates; and (ii) higher product supply resulting from the continued startup of new capacities in the United

States and China. |

14 U.S.

PP – U.S. propylene price

15 EU

PP – EU propylene price

16 U.S.

PE – U.S. ethane price

| 8.2 | GEOLOGICAL EVENT IN ALAGOAS |

a)

Provisions

The The Company operated,

since its formation and subsequently as the successor of the company Salgema, salt mining wells located in Maceió city, Alagoas

state, with the purpose of supplying raw material to its chlor-alkali and dichloroethane plant. In March 2018, an earthquake hit certain

districts of Maceió, where the wells are located, and cracks were found in buildings and public streets of Pinheiro, Bebedouro,

Mutange and Bom Parto districts.

In May 2019, the Geological

Survey of Brazil (“CPRM”) issued a report indicating that the geological phenomenon observed in the region, could be related

to the rock salt exploration activities developed by Braskem. In view of these events, on May 9, 2019, Braskem decided to suspend its

salt mining activities and the operation of its chlor-alkali and dichloroethane plant.

Since then, the Company

has been devoting its best efforts to understand the geological event: (i) possible surface effects; and (ii) the analyses of stability

of salt cavities. The results are being shared with the Brazilian National Mining Agency (“ANM”) and other pertinent authorities,

which the Company has been maintaining constant dialogue.

Braskem presented to ANM

the measures for shutting down its salt mining fronts in Maceió, with measures for the closure of its cavities, and, on November

14, 2019, it proposed the creation of a protective area surrounding certain cavities as a precautionary measure to ensure public safety.

These measures are based on a study conducted by the Institute of Geomechanics of Leipzig (IFG), in Germany, an international reference

in the geomechanical analysis of areas of salt extraction by dissolution and are being adopted in coordination with the Civil Defense

of Maceió and other authorities.

As a result of the geological

phenomenon, negotiations were conducted with public and regulatory authorities that resulted in the Agreements executed, including:

| i. | Agreement to Support the Relocation

of People in Risk Areas (“Agreement for Compensation of Residents"), entered into with State Prosecution Office (“MPE”),

the State Public Defender’s Office (“DPE”), the Federal Prosecution Office (“MPF”) and the Federal Public

Defender’s Office (“DPU”), which was ratified by the court on January 3, 2020, adjusted by its resolutions and subsequent

amendments, , which establish cooperative actions for relocating residents from risk areas, defined in the Map of Sectors of Damages and

Priority Action Lines by the Civil Defense of Maceió (“Civil Defense Map”), as updated in December 2020 (version 4),

and guaranteed their safety, which provides support, under the Financial Compensation and Support for Relocation Program (“PCF”)

implemented by Braskem to the population in the areas of the Civil Defense Map, as well as the dismissal of the Public-Interest Civil

Action (Reparations for Residents), as detailed in Note 24.1 (i). |

| ii. | Agreement to Dismiss the Public-Interest

Civil Action on Socio-Environmental Reparation and the Agreement to define the measures to be adopted regarding the preliminary injunctions

of the Public-Interest Civil Action on Socio-Environmental Reparation (jointly referred to as “Agreement for Socio-Environmental

Reparation”), signed with the MPF with the MPE as the intervening party, on December 30, 2020, in which the Company mainly undertook

to: (i) adopt measures to stabilize and monitor the subsidence phenomenon arising from salt mining; (ii) repair, mitigate or compensate

possible environmental impacts and damages arising from salt mining in the Municipality of Maceió; and (iii) repair, mitigate or

compensate possible socio-environmental impacts and damages arising from salt mining in the Municipality of Maceió, as well as

the termination of the Public-Interest Civil Action (Socio-environmental Reparation) related to the Company, as detailed in Note 24.1

(ii). Moreover, the Agreement for Socio-Environmental Reparation envisages the inclusion of other parties, which depends on specific negotiation

with such potential parties. |

| iii. | Instrument of Global Agreement

with the Municipality of Maceió (“Instrument of Global Agreement”) ratified on July 21, 2023 by the 3rd Federal Court

of Maceió, which establishes, among other things: (a) payment of R$1.7 billion as indemnity, compensation and full reimbursement

for any property and non-property damages caused to the Municipality of Maceió; (b) adherence of the Municipality of Maceió

to the terms of the Socio-environmental Agreement, including the Social Actions Plan (PAS). |

The Management of Braskem,

based on its assessment and that of its external advisors, considering the measures recommended on technical studies in the short and

long-term and the existing information and refined estimates of expenses for implementing several measures connected with the geological

event in Alagoas, the provision shows the following changes in the period ended September 30, 2023:

The current provision can

be segregated into the following action fronts:

| a. | Support Support for relocating

and compensating: Refers to actions to support for relocating and compensating for the residents, business and real state owners of

properties located in the Civil Defense Map (version 4) updated in December 2020, including establishments that requires special measures

for their relocation, such as hospitals, schools and public equipment. |

This action has

a provision of R$1.4 billion (2022: R$2.1 billion) that comprises expenses related to relocation actions, such as relocation allowance,

rent allowance, household goods transportation and negotiation of individual agreements for financial compensation.

| b. | Actions for closing and monitoring

the salt cavities, environmental actions and other technical matters: Based on the findings of sonar and technical studies, stabilization

and monitoring actions were defined for all 35 existing salt mining areas. Based on studies of the specialists, the recommendation was

to fill 9 salt cavities with solid material, a process that should take a total of 4 years. For the remaining 26, the recommended actions

are: closure using the tamponade technique, which consists of promoting the cavity pressurization, applied worldwide for post-operation

cavities; confirmation of natural filling status; and, for some cavities, sonar monitoring. |

The provisioned

balance amount of R$1.1 billion (2022: R$1.4 billion) to implement the measures described in this item was calculated based on existing

techniques and the solutions planned for the current conditions of the cavities, including expenses with technical studies and monitoring,

as well as environmental actions already identified. The provision amount may be changed based on new information, such as: results of

the monitoring of the cavities, progress of implementing the plans to close mining areas, possible changes to be made to the environmental

plan, monitoring of the ongoing measures and other possible natural alterations. The monitoring system implemented by Braskem envisages

actions developed during and after the closure of mining areas, focusing on safety and monitoring of region's stability.

The Company's actions

are based on technical studies conducted by outsourced specialists, with the recommendations presented to the competent authorities. The

Company is implementing the actions approved by the ANM.

In June 2022, in

compliance with the Agreement for Socio-environmental Reparation, Braskem submitted to the MPF the environmental diagnosis containing

the assessment of the potential environmental impacts and damages arising from salt mining activities and the environmental plan with

proposals of the measures required. As established in the agreement, the parties jointly defined the specialized company that will evaluate

and monitor the environmental plan. In December 2022, an additional report on the environmental plan was filed with the MPF. In February

2023, this environmental plan was approved, incorporating the suggestions provided in the additional report. Braskem initiated the actions

foreseen by the plan, implementing the commitments established in the agreement and sharing the results of its actions with the authorities.

Also agreed was that the environmental diagnosis will be updated in December 2025.

| c. | Social and urban measures:

Refers to actions in compliance with social and urban measures, under the Agreement for Socio-environmental Reparation signed on December

30, 2020, allocating R$1.6 billion for the adoption of actions and measures in vacated areas, urban mobility and social compensation actions,

of which R$300 million going to indemnification for social damages and collective pain and suffering and possible contingencies related

to the actions in the vacated areas and urban mobility actions. The amount of this provision is R$1.4 billion (2022: R$1.6 billion). |

| d. | Additional measures:

Refers to actions regarding: (i) Instrument of Global Agreement with the Municipality of Maceió; (ii) actions related to the Technical

Cooperation Agreements entered into by the Company; (iii) expenses with managing the geological event in Alagoas relating to communication,

compliance, legal services, etc.; (iv) additional measures to assist the region and maintenance of areas, including actions for requalification

and indemnification directed to Flexais region; and (v) other matters classified as a present obligation for the Company, even if not

yet formalized. The amount of the provision related additional measures is R$1.7 billion (2022: R$1.6 billion). |

The provisions of the Company

are based on current estimates and assumptions and may be updated in the future due to new facts and circumstances, including, but not

limited to: changes in the execution time, scope and method; the success of action plans; new repercussions or developments arising from

the geological event, including possible revision of the Civil Defense Map; studies that indicate recommendations from specialists, including

the Technical Monitoring Committee, according to Agreement for Compensation of Residents, and other new developments in the matter.

The measures related to

the plans to close mining areas are also subject to the analysis and approval by the ANM, the monitoring of results of the measures under

implementation as well as changes related to the dynamic nature of the geological event.

Continuous monitoring is

essential for confirming the results of the current recommendations. Accordingly, the plan to close mining areas may be updated based

on the need to adopt technical alternatives to stabilize the subsidence phenomena arising from the extraction of salt. In addition, the

assessment of the future behavior of cavities to be monitored using sonar and piezometers could indicate the need for certain additional

measures to stabilize them.

The actions to repair,

mitigate or offset potential environmental impacts and damages, as provided for in the Socio-environmental Reparation Agreement, will

be defined considering the environmental diagnosis prepared by a specialized and independent company. After the conclusion of all discussions

with authorities and regulatory agencies, as per the process established in the agreement, an action plan will be agreed to be part of

the measures for a Plan to Recover Degraded Areas (“PRAD”).

Also in the context of

understandings with the authorities to address claims related to the geological event in Alagoas, on October 26, 2022, the 3rd Federal

Court of Alagoas ratified the Term of Agreement for Implementation of Socioeconomic Measures for the Requalification of the Flexal Area

(“Flexais Agreement”), entered into by Braskem and the MPF, the MPE, the DPU, and Municipality of Maceió for the adoption

of action for requalification in the Flexais region, compensation to the Municipality of Maceió and indemnities to the residents

of this location. The expected disbursement amounts to the execution of the obligations defined in the Flexais Agreement are part of the

provision under (d) Additional Measures.

The Company has been making

progress in negotiations with public entities about other indemnification requests to understand them better. Although future disbursements

may occur as a result of said negotiations, as of the reporting date, the Company is unable to predict the results and timeframe for concluding

these negotiations or its possible scope and the total associated costs in addition to those already provisioned for.

It is not possible to anticipate

all new claims, related to damages or other nature, that may be brought by individuals or groups, including public or private entities,

that understand they suffered impacts or damages somehow related to the geological phenomenon and the relocation of people from risk areas,

as well as new notices of violation or administrative penalties of diverse natures. Braskem continues to face and could still face administrative

procedures and various lawsuits filed by individuals or legal entities not included in the PCF or that disagree with the financial compensation

offer for individual settlement, as well as new collective actions and new lawsuits filed by public utility concessionaires, entities

of the direct or indirect administration of the State, Municipalities or Federal level. Therefore, the number of such actions, their nature

or the amounts involved cannot be estimated at this moment.

Consequently, the Company

cannot eliminate the possibility of future developments related to the geological event in Alagoas, the relocation process and actions

in vacated and adjacent areas, so the expenses to be incurred may differ from its estimates and provisions.

In February 2023, the Company

signed a settlement agreement with the insurance companies, closing the claim for the geological event in Alagoas.

For more information, see

note 24 (“Geological event - Alagoas”) of the consolidated and individual Quarterly Information of September 30, 2023.

| b) | Advances on Action Fronts |

Relocation and Compensation

of residents

As of September 30, 2023,

19,073 proposals had been submitted, with an acceptance rate of 99.3%. Additionally, as of September 30, 2023, 18,491 financial compensations

had been accepted. Under the Financial Compensation and Support for Relocation Program (“PCF”), approximately R$3.8 billion

had been disbursed from the beginning of the program until the end of September 2023. The current expectation for the conclusion of PCF

is to the beginning of 2024.

Closing and monitoring

salt wells, environmental actions and other technical matters

All of the Company's actions

are based on technical studies by recognized experts in different fields of knowledge, with recommendations being presented to the competent

authorities. The Company obtained approval from the National Mining Agency (ANM) for the Closing Plan for mining fronts, as well as issuing

periodic reports on the execution of the Plan, which meets the standards and recommendations established by this agency. The actions for

stabilization and monitoring of the 35 Mining Fronts, based on the results of sonars, geomechanical studies and authorization from ANM,

are being carried out according to the schedule, and of the total of 9 cavities planned for filling with sand, in the first group of 4

mining fronts, 3 cavities are completed with technical opinion from ANM confirming their filling, and 1 of them has reached the technical

limit. Of the second group of 5 filling mining fronts, 3 are in progress and 1 is in the commissioning process.

Additionally, there is

a group of 15 mining fronts, with activities related to pressurization and plugging, which are still ongoing. As of September 30, 2023,

of the 15 mining fronts, 14 have completed plugging activities for the original well and 1 has ongoing activities.

Finally, there are 5 mining

fronts with confirmation of natural filling and 6 mining fronts that are in the sonar monitoring group. Regarding those with natural filling,

specialized companies hired concluded, based on studies carried out, that the natural filling was confirmed, the conclusion of which was

approved by ANM. Regarding monitoring, the established schedule for sonar analysis, presented to ANM, is being followed. The current expectation

for the conclusion of the Closing Plan for mining fronts is between 2024 and 2025.

In June 2022, in compliance

with what was established in the Agreement for Socio-Environmental Reparation, Braskem presented the environmental diagnosis to the MPF,

containing the assessment of the potential impacts and environmental damages resulting from the rock salt extraction activity and the

environmental plan with proposals for necessary measures. As provided for in the agreement, after a joint choice between the parties,

a specialized company was defined to evaluate and monitor the execution of the environmental plan. In December 2022, the second opinion

report on the plan was filed with the MPF and, in February 2023, this environmental plan was approved, with the incorporation of the suggestions

made in the second opinion report. Braskem began operationalizing the actions foreseen in the Plan, both for the physical and biotic environments,

and continues to implement the commitments and share the results of its actions with the authorities, as provided for in the agreement,

which also includes updating the environmental diagnosis in Dec/25.

Socio-urban measures

As an integral part of

the unoccupied area transformation agenda, Braskem continues to advance socio-urban measures, which encompass a set of actions focused

on Urban Mobility, Social Compensation and actions in unoccupied areas.

Regarding Urban Mobility

Projects, a total set of 11 actions were defined that include the implementation of 20 km of double roads on the main road corridors (Avenida

Menino Marcelo, Avenida Durval de Góes, Avenida Fernandes Lima / Rua Professor José da Silveira Camerino), construction

of a new 2.37 km connection between the main road corridors, 12 km of restoration of existing roads and a traffic light and video monitoring

system.

The implementation of these

11 actions goes through the stages of projects, licensing, contracting and execution of works, with 8 already having their executive projects

completed and 03 in progress. Of the 11 actions, 03 are in progress for physical execution, with traffic lights having already been implemented

with the intelligent system and is still in assisted operation, 01 referring to the connection of Av. Durval de Góes and Av. Menino

Marcelo scheduled to start in 4Q23, and the others in the licensing and contracting process. The current expectation for the conclusion

of ongoing actions is 2024, and for of all the 11 urban mobility actions the expectation is to 2026.

In relation to the actions

in the unoccupied areas, the activities relating to the demolition process of Encosta do Mutange were completed, and progress is being

made with the Drainage, Earthworks and Vegetation Coverage stages. The current expectation for the conclusion of the Encosta do Mutange

stabilization and drainage project is to 2024. Other activities related to emergency demolitions of the areas continue as requested by

the Civil Defense of Maceió. In addition, the Company maintains actions to care for neighborhoods, including property security,

waste management and pest control.

Regarding the actions of

the Social Action Plan (PAS), a Public Listening was held to present the participatory technical diagnosis and proposed lines of action.

The Public Listening took place in 04 meetings, with an approach in 4 dimensions: Axis 1: Social policies and reduction of vulnerability,

Axis 2: Economic activity, work and income and socio-urban planning, Axis 3: Recovery and Qualification of Urban Space and Axis 4: Preservation

of Memory Culture, with the purpose of exposing the results of the technical-participatory diagnosis and obtaining data, subsidies, information,

suggestions and/or proposals from the community and public bodies, regarding the aforementioned dimensions.

In September 2023, the

Technical-Participatory Post-Public Listening Diagnosis was delivered by the company Diagonal to the MPF and Braskem. The parties to the

Agreement also validated 4 convergent actions of the Culture and Heritage Axis for immediate start (Inventory of Intangible Cultural Heritage;

Promotion notices for Support to Culture - promotion by public agent; Promotion notices to support culture - promotion by private agent

or third sector; Cultural Sponsorships), which are already in negotiations with the Municipal Secretariat of Culture and Creative Economy.

With regard to the Urban

Integration and Development of Flexais Project, progress is highlighted in the process of paying compensation to residents (Financial

Support Program - PAF) - by September 30, 2023, 1,666 proposals had been presented and 1,586 payments had already been made completed.

In relation to urban

requalification actions, of the 23 actions

foreseen in the Agreement, 11 have already been implemented and the others are in progress, with emphasis on actions related to the Urban

Plan, location and projects of equipment to be implemented: UBS, School , Fisherman's Center, Shopping Center and Fair, in addition to

the implementation of the Youth Training Program, which has already provided 03 training courses with 60 places. The objective of the

project is to promote access to essential public services and encourage the local economy of Flexais, aiming to solve the socioeconomic

islanding of the region.

| 8.3 | CONSOLIDATED INCOME STATEMENT |