UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 8-K

CURRENT REPORT

PURSUANT

TO SECTION 13 OR 15(D)

OF THE SECURITIES EXCHANGE ACT OF 1934

Date of Report (Date of earliest event reported): August 10, 2023

Flame Acquisition Corp.

(Exact name of registrant as specified in its charter)

|

|

|

|

|

| Delaware |

|

001-40111 |

|

85-3514078 |

| (State or other jurisdiction

of incorporation) |

|

(Commission

File Number) |

|

(I.R.S. Employer

Identification No.) |

|

|

|

| 700 Milam Street, Suite 3300

Houston, Texas |

|

77002 |

| (Address of Principal Executive Offices) |

|

(Zip Code) |

(713) 579-6106

(Registrant’s telephone number, including area code)

Check the appropriate box below if the Form 8-K is intended to simultaneously satisfy the filing obligation of the registrant under any of the following

provisions:

| |

☐ |

Written communication pursuant to Rule 425 under the Securities Act (17 CFR 230.425) |

| |

☒ |

Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) |

| |

☐ |

Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b))

|

| |

☐ |

Pre-commencements communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c))

|

Securities registered pursuant to Section 12(b) of the Act:

|

|

|

|

|

| Title of each class |

|

Trading

Symbol(s) |

|

Name of each exchange

on which registered |

| Units, each consisting of one share of Class A common stock and one-half of one warrant |

|

FLME.U |

|

The New York Stock Exchange |

| Class A common stock, par value $0.0001 per share |

|

FLME |

|

The New York Stock Exchange |

| Warrants, each whole warrant exercisable for one share of Class A common stock at an exercise price of $11.50 per share |

|

FLME.WS |

|

The New York Stock Exchange |

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of

1933 (§230.405 of this chapter) or Rule 12b-2 of the Securities Exchange Act of 1934 (§240.12b-2 of this chapter).

Emerging growth company

☒

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with

any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

IMPORTANT NOTICES

Additional Information and Where to Find It

This

communication relates to the proposed Business Combination (as defined in the Current Report on Form 8-K filed with the SEC on November 2, 2022) by and among Flame Acquisition Corp. (“Flame”),

Sable Offshore Holdings LLC, a Delaware limited liability company (“Holdco”) and Sable Offshore Corp., a Texas corporation and a wholly owned subsidiary of Holdco (“Sable”). In connection with the proposed Business Combination,

Flame filed with the SEC a preliminary proxy statement on Schedule 14A on November 10, 2022 (as may be amended from time to time, including on December 23, 2022 and January 27, 2023, the “Proxy Statement”). Flame may also

file other documents regarding the proposed Business Combination with the SEC. The Proxy Statement which will be sent or given to the Flame stockholders will contain important information about the proposed Business Combination and related matters.

INVESTORS ARE URGED TO READ THE PROXY STATEMENT (INCLUDING ALL AMENDMENTS AND SUPPLEMENTS THERETO), WHICH IS CURRENTLY AVAILABLE, AND OTHER RELEVANT DOCUMENTS FILED WITH THE SEC IF AND WHEN THEY BECOME AVAILABLE BECAUSE THEY CONTAIN, AND WILL

CONTAIN, IMPORTANT INFORMATION WITH RESPECT TO THE PROPOSED BUSINESS COMBINATION AND THE OTHER TRANSACTIONS CONTEMPLATED BY THE BUSINESS COMBINATION AGREEMENT (AS DEFINED IN THE PROXY STATEMENT). You may obtain a free copy of the Proxy Statement and

other relevant documents filed by Flame with the SEC at the SEC’s website at www.sec.gov. You may also obtain Flame’s documents on its website at www.Flameacq.com.

Participants in the Solicitation

Flame and its directors

and officers may be deemed participants in the solicitation of proxies of Flame’s stockholders in connection with the Business Combination. Flame’s stockholders and other interested persons may obtain, without charge, more detailed

information regarding the directors and officers of Flame in Flame’s Registration Statement on Form S-1, which was initially filed with the SEC on February 5, 2021 and amended on February 18,

2021 and February 22, 2021, in Flame’s Annual Report on Form 10-K for the fiscal year ended December 31, 2022, which was filed with the SEC on March 31, 2023, and in the Proxy Statement.

Information regarding the persons who may, under SEC rules, be deemed participants in the solicitation of proxies of Flame’s stockholders in

connection with the Business Combination and other matters to be voted upon at the special meeting will be set forth in the definitive proxy statement for the Business Combination.

Forward-Looking Statements

This communication contains a number of “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended

(the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). Forward-looking statements include information concerning the SYU Assets (as defined in the Proxy Statement),

Sable’s, Holdco’s or Flame’s possible or assumed future results of operations, business strategies, debt levels, competitive position, industry environment, potential growth opportunities and effects of regulation, including

Sable’s ability to close the transaction to acquire the SYU Assets and Flame’s ability to close the transaction with Sable. When used in this communication, including any oral statements made in connection therewith, the words

“could,” “should,” “will,” “ may,” “ believe,” “ anticipate,” “ intend,” “ estimate,” “ expect,” “project,” “continue,” “plan,”

forecast,” “predict,” “potential,” “future,” “outlook,” and “target,” the negative of such terms and other similar expressions are intended to identify forward-looking statements, although not

all forward-looking statements will contain such identifying words. These forward-looking statements are based on Sable’s, Holdco’s and Flame’s management’s current expectations and assumptions about future events and are based

on currently available information as to the outcome and timing of future events. Except as otherwise required by applicable law, Sable, Holdco and Flame disclaim any duty to update any forward-looking statements, all of which are expressly

qualified by the statements in this section, to reflect events or circumstances after the date of this communication. Sable, Holdco and Flame caution you that these forward-looking statements are subject to all of the risks and uncertainties, most

of which are difficult to predict and many of which are beyond the control of Sable and Flame, incidental to the development, production, gathering, transportation and sale of oil, natural gas and natural gas liquids. These risks include, but are

not limited to, (a) the occurrence of any event, change or other circumstance that could give rise to the termination of negotiations and any subsequent definitive agreements with respect to the Business Combination; (b) the outcome of any

legal proceedings that may be instituted against Sable, Holdco, Flame or others following the announcement of the Business Combination and any definitive agreements with respect thereto; (c) the inability to complete the Business Combination

due to the failure to obtain approval of the stockholders of Flame, to obtain financing to complete the Business Combination or to satisfy other conditions to closing the Business Combination; (d) the ability to meet the applicable stock

exchange listing standards following the consummation of the Business Combination; (e) the ability to recommence production of the SYU Assets and the cost and time required therefor, and production levels once recommenced; (f) commodity

price volatility, low prices for oil, natural gas and/or natural gas liquids, global economic conditions, inflation, increased operating costs, lack of availability of drilling and production equipment, supplies, services and qualified personnel,

processing volumes and pipeline throughput; (g) uncertainties related to new technologies, geographical concentration of operations, environmental risks, weather risks, security risks, drilling and other operating risks, regulatory changes and

regulatory risks; (h) the uncertainty inherent in estimating oil and natural gas reserves and in projecting future rates of production; (i) reductions in cash flow and lack of access to capital; (j) Flame’s ability to satisfy

future cash obligations; (k) restrictions in existing or future debt agreements or structured or other financing arrangements; (l) the timing of development expenditures, managing growth and integration of acquisitions, and failure to

realize expected value creation from acquisitions; and (m) the ability to recognize the anticipated benefits of the Business Combination. While forward-looking statements are based on assumptions and analyses that management of Flame, Holdco

and Sable believe to be reasonable under the circumstances, whether actual results and developments will meet such expectations and predictions depends on a number of risks and uncertainties that could cause actual results, performance, and

financial condition to differ materially from such expectations. Any forward-looking statement made in this communication speaks only as of the date on which it is made. Factors or events that could cause actual results to differ may emerge from

time to time, and it is not possible to predict all of them. These forward-looking statements are provided for illustrative purposes only and are not intended to serve as, and must not be relied on by any investor as, a guarantee, an assurance, a

prediction or a definitive statement of fact or probability. You should carefully consider the foregoing factors and the other risks and uncertainties described in the “Risk Factors” section of the Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Proxy Statement and other documents filed by Flame from time to time with the SEC. These filings identify and address other important

risks and uncertainties that could cause actual events and results to differ materially from those contained in the forward-looking statements. Forward-looking statements speak only as of the date they are made. Readers are cautioned not to put

undue reliance on forward-looking statements, and Flame, Holdco and Sable assume no obligation and do not intend to update or revise these forward-looking statements, whether as a result of new information, future events, or otherwise, except as

required by securities and other applicable laws. Neither Flame, Holdco nor Sable gives any assurance that any of Flame, Holdco, Sable or the combined company will achieve its expectations.

Item 7.01 Regulation FD Disclosure

Furnished as Exhibit 99.1 hereto and incorporated into this Item 7.01 by reference is an investor presentation that Flame and Sable have prepared for use in

presentations to potential PIPE Investors (as defined in the Proxy Statement) and other persons with respect to the proposed Business Combination.

The

statements under this Item 7.01 and Exhibit 99.1 are being furnished pursuant to Item 7.01 and will not be deemed to be filed for purposes of Section 18 of the Exchange Act or otherwise be subject to the liabilities of that section, nor will

they be deemed to be incorporated by reference in any filing under the Securities Act or the Exchange Act.

| Item 9.01. |

Financial Statements and Exhibits. |

|

|

|

| Exhibit No. |

|

Description of Exhibits |

|

|

| 99.1 |

|

Investor Presentation, dated August 10, 2023. |

|

|

| 104 |

|

Cover Page Interactive Data File (embedded within Inline XBRL document) |

SIGNATURE

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by

the undersigned hereunto duly authorized.

|

|

|

|

|

|

|

|

|

|

|

Flame Acquisition Corp. |

|

|

|

|

| Date: August 10, 2023 |

|

|

|

By: |

|

/s/ Gregory D. Patrinely |

|

|

|

|

Name: |

|

Gregory D. Patrinely |

|

|

|

|

Title: |

|

Executive Vice President and Chief

Financial Officer |

Exhibit 99.1 Sable Offshore Corp. Investor Presentation August

2023

Disclaimer CONFIDENTIALITY The information in this presentation,

together with oral statements made in connection herewith, is highly confidential. The distribution of this presentation by an authorized recipient to any other person is unauthorized. Any photocopying, disclosure, reproduction or alteration of the

contents of this presentation and any forwarding of a copy of this presentation or any portion of this presentation to any other person is prohibited. The recipient of this presentation shall keep this presentation and its contents confidential,

shall not use this presentation and its contents for any purpose other than as expressly authorized by Sable Offshore Corp. (“Sable”). By accepting delivery of this presentation, the recipient is deemed to agree to the foregoing

confidentiality requirements and to return or destroy (and direct its representatives to return or destroy) all copies of this presentation or portions thereof in its possession upon request. This presentation has been prepared solely for

informational purposes and is being provided to you solely in your capacity as a prospective investor in considering an investment in Flame Acquisition Corp., (the “SPAC”), which will become the successor to Sable in a business

combination (as defined below) and will be the issuer, in a private placement, of the PIPE securities described in this presentation. This presentation does not purport to contain all of the information that may be required or desired by you in

order to evaluate the investment described in this presentation. This presentation shall not constitute an offer to sell, or the solicitation of an offer to buy, any securities, nor shall there be any sale of securities in any states or

jurisdictions in which such offer, solicitation or sale would be unlawful. Neither the U.S. Securities and Exchange Commission (the “SEC”) nor any securities commission of any other U.S. or non-U.S. jurisdiction has approved or

disapproved of the securities in the proposed PIPE offering or of the proposed business combination as contemplated hereby or determined that this presentation is truthful or complete. Any representation to the contrary is a criminal offense. In all

cases, interested parties should consult their own legal, regulatory, tax, business, financial and accounting advisors to the extent they deem necessary, and must make their own investment decision and perform their own independent investigation and

analysis of the investment described in this presentation. Investors should be aware that they might be required to bear the final risk of their investment for an indefinite period of time. The securities referred to herein have not been registered

under the Securities Act of 1933, as amended (the “Securities Act”), or the securities laws of any other jurisdiction. Unless they are registered, any such securities may be offered and sold only in transactions that are exempt from

registration under the Securities Act and the securities laws of any other jurisdiction. No representations or warranties, express or implied are given in, or in respect of, this presentation and the accuracy, completeness or reliability of the

information contained in this presentation. To the fullest extent permitted by law, in no circumstances will Sable, the SPAC, any bank serving as a placement agent in the proposed PIPE securities or any of their respective subsidiaries, security

holders, affiliates, representatives, partners, directors, officers, employees, advisers, or agents be responsible or liable for any direct, indirect, or consequential loss or loss of profit arising from the use of this presentation, its contents,

its omissions, reliance on the information contained within it, or on opinions communicated in relation thereto or otherwise arising in connection therewith. This information is subject to change. FORWARD LOOKING STATEMENTS The information in this

presentation and the oral statements made in connection therewith include “forward looking statements” within the meaning of Section 27 A of the Securities Act and Section 21 E of the Securities Exchange Act of 1934 as amended.

Forward-looking statements include information concerning assets of Exxon Mobil Corporation's (“Exxon”), Sable's or the SPAC's possible or assumed future results of operations, business strategies, debt levels, competitive position,

industry environment, potential growth opportunities and effects of regulation, including Sable's ability to close the transaction to acquire Exxon's assets (the asset acquisition ), Sable’s ability to close the transaction with Sable Offshore

Holdings, LLC (“HoldCo”) and the SPAC (the “SPAC transaction” and, together with the asset acquisition, the “business combination”). When used in this presentation, including any oral statements made in connection

therewith, the words “could,” “should,” “will,” “ may,” “ believe,” “ anticipate,” “ intend,” “ estimate,” “ expect,” “project,”

“continue,” “plan,” forecast,” “predict,” “potential,” “future,” “outlook,” and “target,” the negative of such terms and other similar expressions are intended

to identify forward looking statements, although not all forward looking statements will contain such identifying words. These forward looking statements are based on Sable’s, HoldCo’s and the SPAC’s management’s current

expectations and assumptions about future events and are based on currently available information as to the outcome and timing of future events. Except as otherwise required by applicable law, Sable, HoldCo and the SPAC disclaim any duty to update

any forward looking statements, all of which are expressly qualified by the statements in this section, to reflect events or circumstances after the date of this presentation. Sable, HoldCo and the SPAC caution you that these forward looking

statements are subject to all of the risks and uncertainties, most of which are difficult to predict and many of which are beyond the control of Sable and the SPAC, incidental to the development, production, gathering, transportation and sale of

oil, natural gas and natural gas liquids. These risks include, but are not limited to, (a) the occurrence of any event, change or other circumstance that could give rise to the termination of negotiations and any subsequent definitive agreements

with respect to the business combination; (b) the outcome of any legal proceedings that may be instituted against Sable, HoldCo, the SPAC or others following the announcement of the business combination and any definitive agreements with respect

thereto; (c) the inability to complete the business combination due to the failure to obtain approval of the shareholders of the SPAC, to obtain financing to complete the business combination or to satisfy other conditions to closing; (d) the

ability to meet the applicable stock exchange listing standards following the consummation of the business combination; (e) the ability to recommence production of the assets acquired in the asset acquisition and the cost and time required therefor,

production levels once recommenced; (f) commodity price volatility, low prices for oil and/or natural gas, global economic conditions, inflation, increased operating costs, lack of availability of drilling and production equipment, supplies,

services and qualified personnel, processing volumes and pipeline throughput; (g) uncertainties related to new technologies, geographical concentration of operations, environmentalrisks, weather risks, security risks, drilling and other operating

risks, regulatory changes and regulatory risks; (h) the uncertainty inherent in estimating oil and natural gas resources and in projecting future rates of production; (i) reductions in cash flow and lack of access to capital; (j) the SPAC’s

ability to satisfy future cash obligations; (k) restrictions in existing or future debt agreements or structured or other financing arrangements; (l) the timing of development expenditures, managing growth and integration of acquisitions, and

failure to realize expected value creation from acquisitions; and (m) the ability to recognize the anticipated benefits of the business combination. Should one or more of the risks or uncertainties described in this presentation and the oral

statements made in connection therewith occur, or should underlying assumptions prove incorrect, actual results and plans could differ materially from those expressed in any forward looking statements. You should also carefully consider the risks

and uncertainties described in the “Risk Factors” section of the SPAC’s Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, preliminary proxy statement on Schedule 14A filed with the SEC on November 10, 2022 (as may be

amended from time to time, including on December 23, 2022 and January 27, 2023), and other documents filed by the SPAC, HoldCo and Sable from time to time with the SEC. These filings identify and address other important risks and uncertainties that

could cause actual events and results to differ materially from those contained in the forward-looking statements. The SPAC’s SEC filings are available publicly on the SEC’s website at www sec gov. 1

Disclaimer (Cont’d) PARTICIPANTS IN A SOLICITATION Sable, the

SPAC, and certain of their respective directors, executive officers and employees may be deemed to be participants in the solicitation of proxies in connection with certain matters related to the business combination and may have direct or indirect

interests in the business combination. Additional information regarding the interests of those persons and other persons who may be deemed participants in the proposed business combination may be obtained by reading the proxy statement relating to

the business combination. Stockholders may obtain free copies of the preliminary proxy statement, the definitive proxy statement and other documents filed with the SEC, once available, without charge, at the SEC’s website located at

www.sec.gov, or by directing a request to Flame Acquisition Corp., 700 Milam Street Suite 3300, Houston, TX 77002. NON-PRODUCING ASSETS The assets that are the subject of the asset acquisition and the business combination have not produced

commercial quantities of hydrocarbons since the assets were shut-in during May of 2015 when the only pipeline transporting hydrocarbons produced from such assets to market ceased operations. We estimate in this presentation that production can be

recommenced by July 1, 2024; however, there can be no assurance that the necessary permits will be obtained that would allow the pipeline to recommence transportation and allow the assets to recommence production by that date or at all. If

production is not recommenced by January 1, 2026, the terms of the asset acquisition with Exxon Mobil Corporation (“Exxon”) would result in the assets, which are expected to be the major assets of the SPAC at the closing of the business

combination, being reverted to Exxon without any compensation to the SPAC therefor as further described in this presentation. OIL AND GAS RESOURCE INFORMATION This presentation includes information regarding estimates of oil and natural gas

resources attributable to the assets that are the subject of the business combination. None of the oil and gas resources attributable to the assets are currently classifiable as proved or other reserves because, since the cessation of operations on

the pipeline transporting production from the assets, there has been no means to deliver production from the assets to market. Sable has obtained a report (the “NSAI Report”) from Netherland, Sewell & Associates, Inc.

(“NSAI”), independent petroleum consultants, with respect to the net estimated contingent resources attributable to the acquired assets and the related pre-tax discounted (at 10%) future net contingent cash flow from such contingent

resources, as of December 31, 2021, based on 12-month unweighted arithmetic average of the first-day-of-the-month prices for each month in the period from January to December 2021. As defined by the Society of Petroleum Engineers and used in the

NSAI Report, “contingent resources” are those quantities of petroleum which are estimated, on a given date, to be potentially recoverable from known accumulations, but which are not currently considered to be commercially recoverable.

Contingent resource estimates may be characterized further as 1C (low estimate), 2C (best estimate) and 3C (high estimate). The contingent resources reflected in the NSAI Report are, as stated in the report, category 1C (low estimate). The NSAI

Report states that the estimates included in the report are contingent on (1) approval from federal, state and local regulators to restart production, (2) reestablishment of oil transportation systems to deliver production to market, and (3)

commitment to restart the wells and facilities. The NSAI Report states that, if these contingencies are successfully addressed, some portion of the contingent resources estimated in the report may be reclassified as reserves but notes that the

estimates have not been risked to account for the possibility that the contingencies are not successfully addressed. The NSAI Report does not address (1) the portion of the contingent resources that could be reclassified as reserves if the

contingencies are successfully addressed or (2) whether or to what extentany of the contingent resources that could be so reclassified would be classified as proved, probable or possible reserves. As defined in the Society of Petroleum

Engineers’ Petroleum Resources Management System (“PRMS”), best estimate is the most realistic assessment of recoverable quantities if only a single result were reported. There is at least a 50% probability that the quantities

actually recovered will equal or exceed the “best estimate.” As defined in the PRMS, low estimate is a conservative estimate of the quantity that will actually be recovered from the accumulation by a project. There is at least a 90%

probability that the quantities actually recovered will equal or exceed the “low estimate.” The resource estimates and related future cash flow information included in this presentation reflect management's estimates, based in part on

the contingent resources estimated in the NSAI Report and supplemented by management's own estimates of contingent resources attributable to the acquired assets and using the pricing and other assumptions noted in this presentation, of the

contingent resources and cash flow that may have been attributable to the acquired assets if the contingencies had been addressed successfully on the date as of which the information is presented. Resource engineering is a process of estimating

underground accumulations of hydrocarbons that cannot be measured in an exact way. The accuracy of any resource or reserve estimate depends on the quality of available data, the interpretation of such data, and price and cost assumptions made by

reserve engineers. In addition, the results of drilling, testing, and production activities may justify revisions of estimates that were made previously. If significant, such revisions could impact the combined company’s strategy and change

the schedule of any production and development drilling. Accordingly, resource estimates may differ significantly from the quantitiesof oil and natural gas that are ultimately recovered. 2

Disclaimer (Cont’d) USE OF PROJECTIONS This presentation contains

financial projections for Sable and the SPAC (as successor to Sable in the business combination) after giving effect to the business combination, including with respect to its future revenues, EBITDA, capital expenditures and non-GAAP cash flow

measures referred to under “Use of Non-GAAP Financial Measures” below. Neither Sable’s nor the SPAC’s auditors have audited, reviewed, compiled or performed any procedures with respect to the projections for the purpose of

their inclusion in this presentation, and, accordingly, no such auditors have expressed an opinion or provided any other form of assurance with respect thereto for the purpose of this presentation. These projections are for illustrative purposes

only and should not be relied upon as being necessarily indicative of future results. The assumptions and estimates underlying the projected informationare inherently uncertain and are subject to a wide variety of significant business, regulatory,

economic and competitive risks and uncertainties that could cause actual results to differ materially from those contained in the projected information. Even if the assumptions and estimates are correct, projections are inherently uncertain due to a

number of factors outside Sable and the SPAC’s control. Accordingly, there can be no assurance that the projected results are indicative of the future performance of the SPAC after completion of the business combination or that actual results

will not differ materially from those presented in the projected information. Inclusion of the projected information in this presentation should not be regarded as a representation by any person, including, without limitation, Sable, the SPAC and

any placement agent, that the results contained in the projected information will be achieved. USE OF NON-GAAP FINANCIAL MEASURES This presentation includes projections for Sable and the SPAC (as successor to Sable in the business combination) of

certain non-GAAP financial measures (including on a forward-looking basis) after giving effect to the business combination, including EBITDA, Unlevered Free Cash Flow, and Levered Free Cash Flow. Sable defines EBITDA as net income before interest

expense, income tax expense and depletion, depreciation and amortization. Sable defines (1) Unlevered Free Cash Flow as EBITDA minus capital expenditures, (2) Levered Free Cash Flow as Unlevered Free Cash Flow minus interest expense, and (3) Net

free cash flow as revenue less operating expenses, taxes, and capital expenditures. Sable believes that these measures are useful to investors for the following reasons. First, Sable believes that these measures may assist investors in evaluating

the SPAC’s projected future performance and ability to pay cash dividends to its stockholders by excluding the impact of items that do not reflect core operating performance or that are not expected to affect the ability of the SPAC to pay

cash dividends to its stockholders. Second, these measures are expected to be used by Sable’s management to assess the SPAC’s performance following completion of the business combination. Sable believes that the future, continuing use of

these non-GAAP financial measures will provide an additional tool for investors to use in evaluating ongoing operating results and trends over various reporting periods on a consistent basis. These non-GAAP financial measures should not be

considered in isolation from, or as an alternative to, financial measures determinedinaccordancewithGAAP. Other companies may calculate these non-GAAP financial measures differently, and therefore such financial measures may not be directly

comparable to similarly tilted measures of other companies. INDUSTRY AND MARKET DATA This presentation has been prepared by Sable and includes market data and other statistical information from sources believed by Sable to be reliable, including

independent industry publications, governmental publications or other published independent sources. Some data is also based on the good faith estimates of Sable, which are derived from their review of internal sources as well as the independent

sources described above. Although Sable believes these sources are reliable, neither Sable, the SPAC nor any placement agent has independently verified the information and can guarantee its accuracy and completeness. TRADEMARKS This presentation may

contain trademarks, service marks, trade names and copyrights of other companies, which are the property of their respective owners, and the SPAC's and Sable's use thereof does not imply an affiliation with, or endorsement by, the owners of such

trademarks, service marks, trade names and copyrights. Solely for convenience, some of the trademarks, service marks, trade names and copyrights referred to in this presentation may be listed without the TM, © or ® symbols, but the SPAC

and Sable will assert, to the fullest extent under applicable law, the rights of the applicable owners, if any, to these trademarks, service marks, trade names and copyrights. 3

Key Transaction Highlights Sable Offshore Corp. (“Sable”)

has entered into an agreement to merge with Flame Acquisition Corp. (“FLME”, “Flame”, or the “Company”). Sable has separately agreed to acquire the Santa Ynez Field and associated assets (“Santa Ynez”,

“SYU”, or the “Acquired Assets”) from ExxonMobil (“Exxon”) Proprietarily sourced, bi-laterally negotiated, and seller financed Santa Ynez Unit Acquisition n Identified by Sable / Flame executives as a

foundational public company Background asset and exclusively negotiated with Exxon st n Purchase price is financed by a 1 Lien Term Loan held by Exxon Santa Ynez is a massive oil-weighted resource n Three offshore platforms located in

federal waters north of Santa Barbara, California High Quality n Wholly owned onshore production treatment facilities Asset n Discovered in 1968 with significant production history n >100 identified infill drilling and step-out

opportunities, along with (1) workovers and ESP installation on existing wellbores Asset re-start process well underway n Facilities well maintained during downtime; ~34 MBoe/d average gross Las Flores Canyon Processing Facility Pathway to

production in 2014 prior to shut-in for pipeline leak Production n March 2020 consent decree establishes path for pipeline restart; permitting process well underway n Target online date of July 2024 Sable management are well-qualified to

operate Santa Ynez (2) Highly-Qualified n Exemplary track record of operating safely in California and offshore Stewards n Demonstrated expertise via numerous awards from state and federal agencies of the Asset n Developing strategy

for carbon capture and underground storage (“CCUS”) leveraging existing infrastructure and access (1) Electric submersible pump. (2) While at Plains Exploration & Production, current Sable management team operated platforms included

Irene at Point Pedernales and Hidalgo, Harvest and Hermosa at Point Arguello. 4

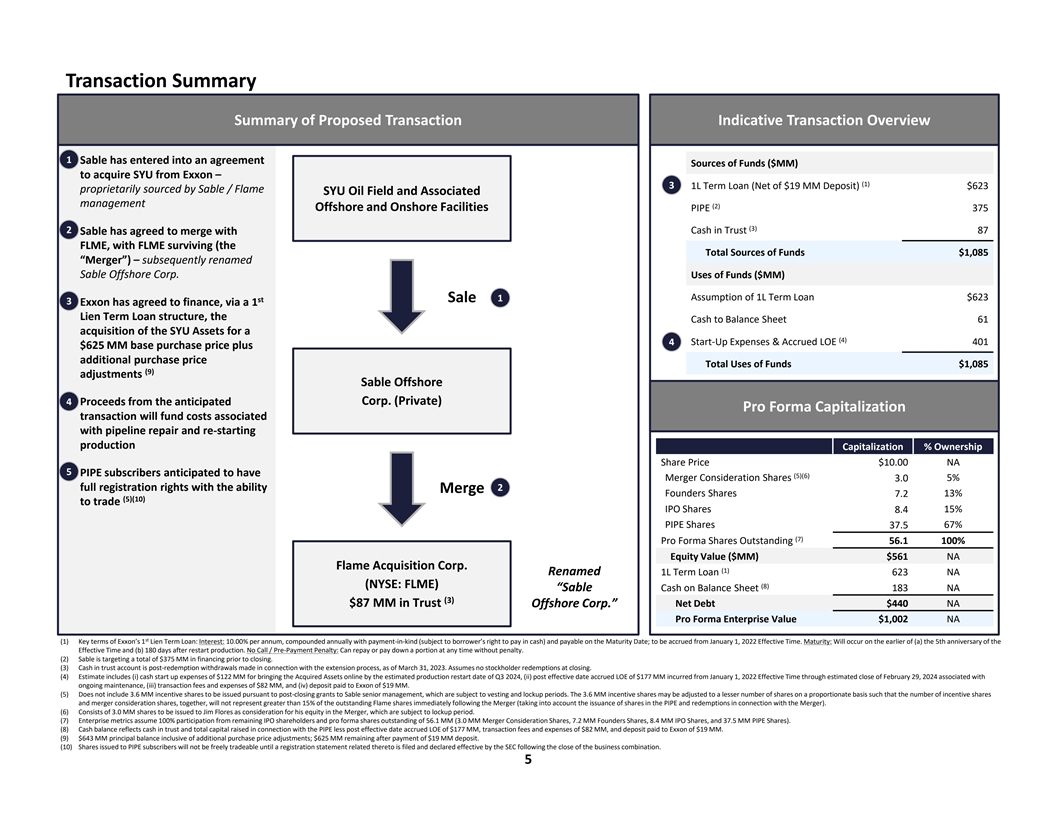

Transaction Summary Summary of Proposed Transaction Indicative

Transaction Overview 1 n Sable has entered into an agreement Sources of Funds ($MM) to acquire SYU from Exxon – (1) 3 1L Term Loan (Net of $19 MM Deposit) $623 proprietarily sourced by Sable / Flame SYU Oil Field and Associated management

(2) Offshore and Onshore Facilities PIPE 375 (3) 2 Cash in Trust 87 n Sable has agreed to merge with FLME, with FLME surviving (the Total Sources of Funds $1,085 “Merger”) – subsequently renamed Sable Offshore Corp. Uses of

Funds ($MM) Assumption of 1L Term Loan $623 1 st Sale 3 n Exxon has agreed to finance, via a 1 Lien Term Loan structure, the Cash to Balance Sheet 61 acquisition of the SYU Assets for a (4) 4 Start-Up Expenses & Accrued LOE 401 $625 MM base

purchase price plus additional purchase price Total Uses of Funds $1,085 (9) adjustments Sable Offshore n 4 Proceeds from the anticipated Corp. (Private) Pro Forma Capitalization transaction will fund costs associated with pipeline repair and

re-starting production Capitalization % Ownership Share Price $10.00 NA 5 n PIPE subscribers anticipated to have (5)(6) Merger Consideration Shares 3.0 5% full registration rights with the ability 2 Merge Founders Shares 7.2 13% (5)(10) to

trade IPO Shares 15% 8.4 PIPE Shares 67% 37.5 (7) Pro Forma Shares Outstanding 56.1 100% Equity Value ($MM) $561 NA Flame Acquisition Corp. (1) Renamed 1L Term Loan 623 NA (NYSE: FLME) (8) “Sable Cash on Balance Sheet 183 NA (3) $87 MM in

Trust Net Debt $440 NA Offshore Corp.” Pro Forma Enterprise Value $1,002 NA st (1) Key terms of Exxon’s 1 Lien Term Loan: Interest: 10.00% per annum, compounded annually with payment-in-kind (subject to borrower’s right to pay in

cash) and payable on the Maturity Date; to be accrued from January 1, 2022 Effective Time. Maturity: Will occur on the earlier of (a) the 5th anniversary of the Effective Time and (b) 180 days after restart production. No Call / Pre-Payment Penalty:

Can repay or pay down a portion at any time without penalty. (2) Sable is targeting a total of $375 MM in financing prior to closing. (3) Cash in trust account is post-redemption withdrawals made in connection with the extension process, as of March

31, 2023. Assumes no stockholder redemptions at closing. (4) Estimate includes (i) cash start up expenses of $122 MM for bringing the Acquired Assets online by the estimated production restart date of Q3 2024, (ii) post effective date accrued LOE of

$177 MM incurred from January 1, 2022 Effective Time through estimated close of February 29, 2024 associated with ongoing maintenance, (iii) transaction fees and expenses of $82 MM, and (iv) deposit paid to Exxon of $19 MM. (5) Does not include 3.6

MM incentive shares to be issued pursuant to post-closing grants to Sable senior management, which are subject to vesting and lockup periods. The 3.6 MM incentive shares may be adjusted to a lesser number of shares on a proportionate basis such that

the number of incentive shares and merger consideration shares, together, will not represent greater than 15% of the outstanding Flame shares immediately following the Merger (taking into account the issuance of shares in the PIPE and redemptions in

connection with the Merger). (6) Consists of 3.0 MM shares to be issued to Jim Flores as consideration for his equity in the Merger, which are subject to lockup period. (7) Enterprise metrics assume 100% participation from remaining IPO shareholders

and pro forma shares outstanding of 56.1 MM (3.0 MM Merger Consideration Shares, 7.2 MM Founders Shares, 8.4 MM IPO Shares, and 37.5 MM PIPE Shares). (8) Cash balance reflects cash in trust and total capital raised in connection with the PIPE less

post effective date accrued LOE of $177 MM, transaction fees and expenses of $82 MM, and deposit paid to Exxon of $19 MM. (9) $643 MM principal balance inclusive of additional purchase price adjustments; $625 MM remaining after payment of $19 MM

deposit. (10) Shares issued to PIPE subscribers will not be freely tradeable until a registration statement related thereto is filed and declared effective by the SEC following the close of the business combination. 5

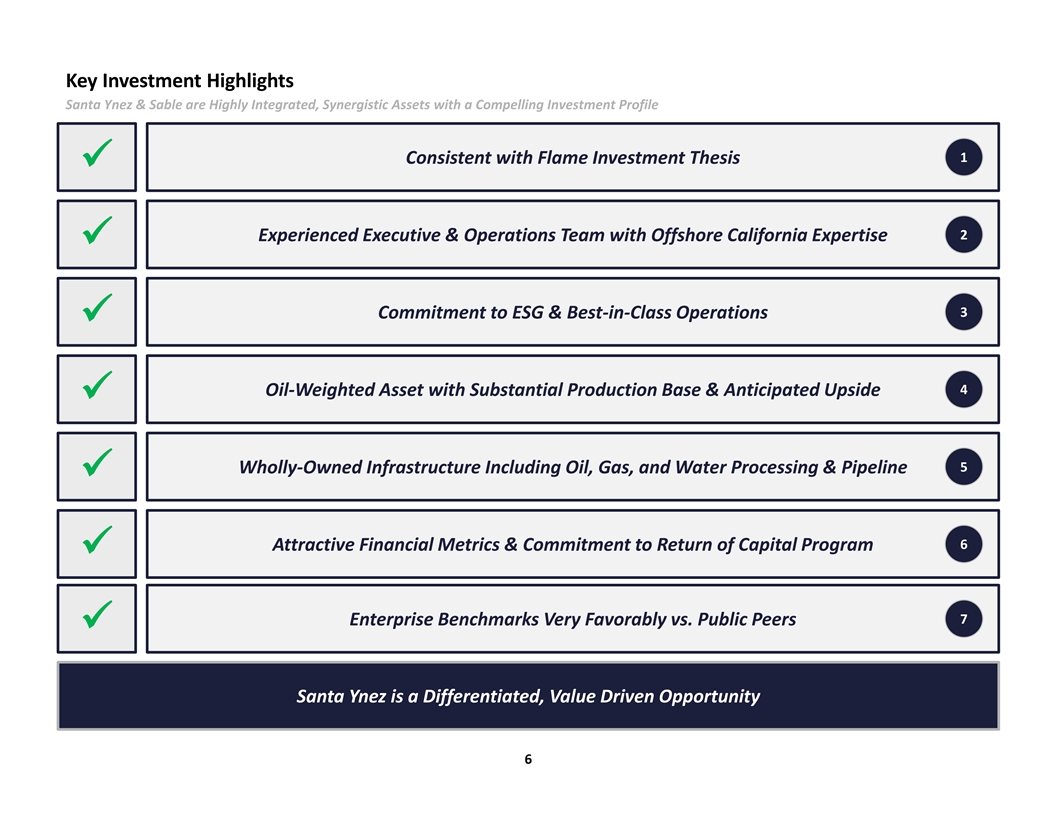

Key Investment Highlights Santa Ynez & Sable are Highly Integrated,

Synergistic Assets with a Compelling Investment Profile 1 Consistent with Flame Investment Thesis ü 2 Experienced Executive & Operations Team with Offshore California Expertise ü 3 Commitment to ESG & Best-in-Class Operations

ü 4 Oil-Weighted Asset with Substantial Production Base & Anticipated Upside ü 5 Wholly-Owned Infrastructure Including Oil, Gas, and Water Processing & Pipeline ü 6 Attractive Financial Metrics & Commitment to Return of

Capital Program ü 7 Enterprise Benchmarks Very Favorably vs. Public Peers ü Santa Ynez is a Differentiated, Value Driven Opportunity 6

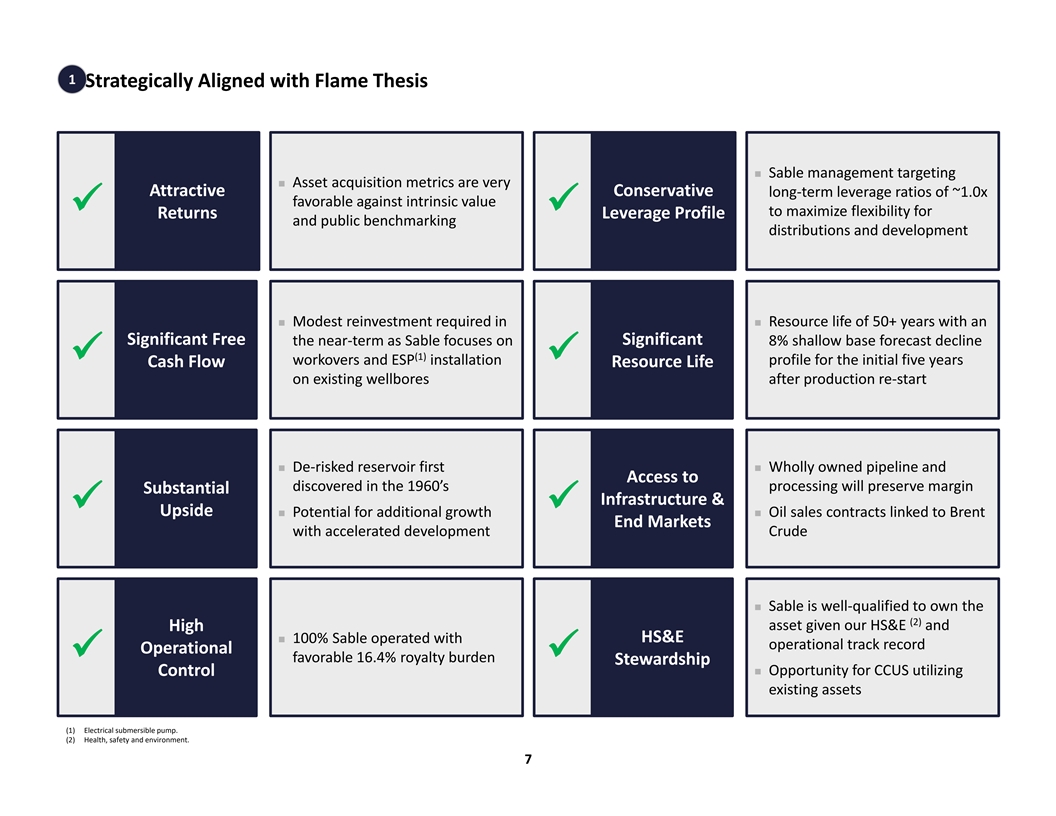

1 Strategically Aligned with Flame Thesis n Sable management

targeting n Asset acquisition metrics are very Attractive Conservative long-term leverage ratios of ~1.0x favorable against intrinsic value üü to maximize flexibility for Returns Leverage Profile and public benchmarking distributions

and development n Modest reinvestment required in n Resource life of 50+ years with an Significant Free the near-term as Sable focuses on Significant 8% shallow base forecast decline (1) ü workovers and ESP installation ü profile

for the initial five years Cash Flow Resource Life on existing wellbores after production re-start n De-risked reservoir first n Wholly owned pipeline and Access to discovered in the 1960’s processing will preserve margin Substantial

Infrastructure & üü Upside n Potential for additional growth n Oil sales contracts linked to Brent End Markets with accelerated development Crude n Sable is well-qualified to own the (2) asset given our HS&E and High

n 100% Sable operated with HS&E operational track record Operational ü favorable 16.4% royalty burdenü Stewardship Controln Opportunity for CCUS utilizing existing assets (1) Electrical submersible pump. (2) Health, safety

and environment. 7

2 Sable – Management Team Sable has Re-Assembled its Premier

Management and Operations Team n Mr. Flores is Sable’s founder and has served as the Chairman and Chief Executive Officer since its inception Jim Flores n From May 2017 until February 2021, Mr. Flores served as Chairman, Chief

Executive Officer and President of Sable Permian Resources n Prior to Sable Permian Resources, Mr. Flores served as Vice Chairman of Freeport-McMoRan, Inc. and CEO of Freeport-McMoRan Oil & Gas, a Chairman of wholly owned subsidiary of

Freeport-McMoRan Inc. the Board n From 2001 until 2013, Mr. Flores was the Chairman, CEO and President of Plains Exploration & Production Company and Chairman and CEO and Chief of Plains Resources Inc. Executive n Mr. Flores founded

and oversaw the IPO of Flores & Rucks, renamed Ocean Energy, and served multiple offices including President, CEO, Officer Vice Chair and Chairman through 2001 n Mr. Patrinely has served as the Chief Financial Officer of Sable since its

inception Gregory n From June 2018 until February 2021, Mr. Patrinely served as Executive Vice President and Chief Financial Officer of Sable Permian Resources Patrinely n Mr. Patrinely previously served as Treasurer for Sable Permian

Resources, from May 2017 to June 2018, where he oversaw the financial Chief analysis and execution of refinancing, restructuring and acquisition efforts Financial n Prior to Sable Permian Resources, Mr. Patrinely was a Manager in the

Acquisitions & Divestments Group of Freeport-McMoRan Oil & Gas, a Officer wholly owned subsidiary of Freeport-McMoRan Inc. Sable Organizational Structure Jim Flores Chairman and CEO Management Team Caldwell Flores Doss Bourgeois Gregory

Patrinely Anthony Duenner President Chief Operating Officer Chief Financial Officer General Counsel 8

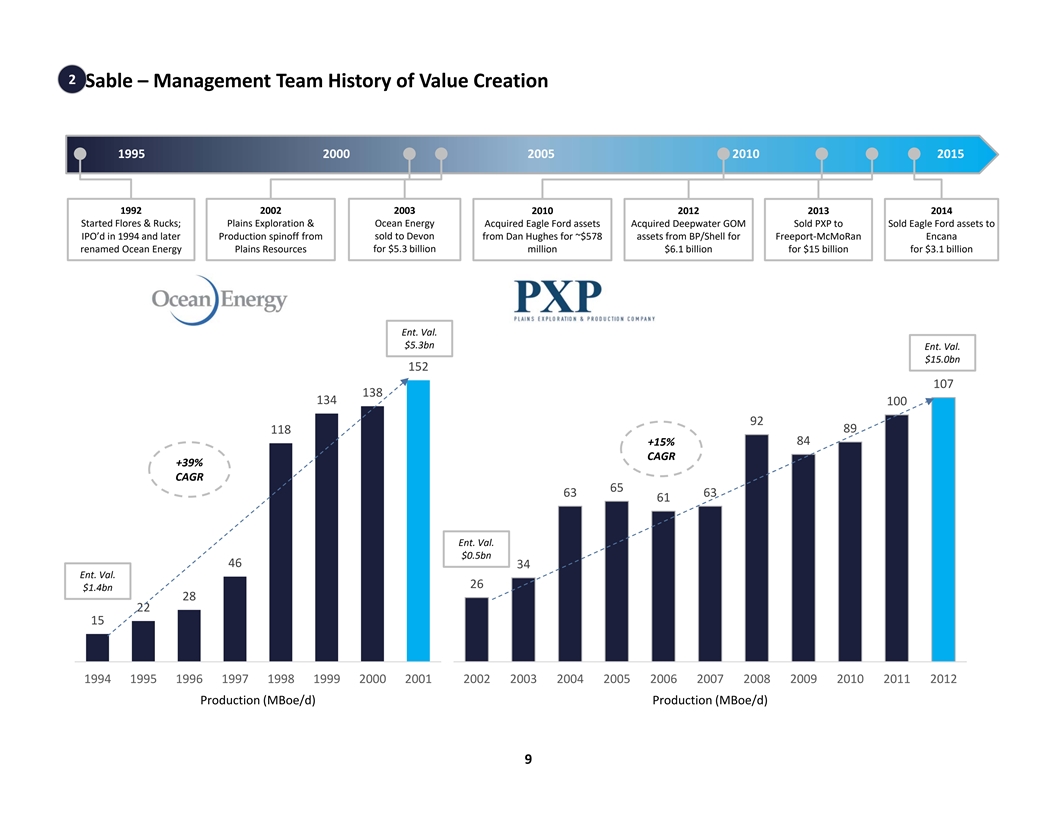

2 Sable – Management Team History of Value Creation 1995 2000

2005 2010 2015 1992 2002 2003 2010 2012 2013 2014 Started Flores & Rucks; Plains Exploration & Ocean Energy Acquired Eagle Ford assets Acquired Deepwater GOM Sold PXP to Sold Eagle Ford assets to IPO’d in 1994 and later Production

spinoff from sold to Devon from Dan Hughes for ~$578 assets from BP/Shell for Freeport-McMoRan Encana renamed Ocean Energy Plains Resources for $5.3 billion million for $15 billion for $3.1 billion $6.1 billion Ent. Val. $5.3bn Ent. Val. $15.0bn 152

107 138 134 100 92 118 89 +15% 84 CAGR +39% CAGR 65 63 63 61 Ent. Val. $0.5bn 46 34 Ent. Val. 26 $1.4bn 28 22 15 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 Production (MBoe/d) Production (MBoe/d)

9

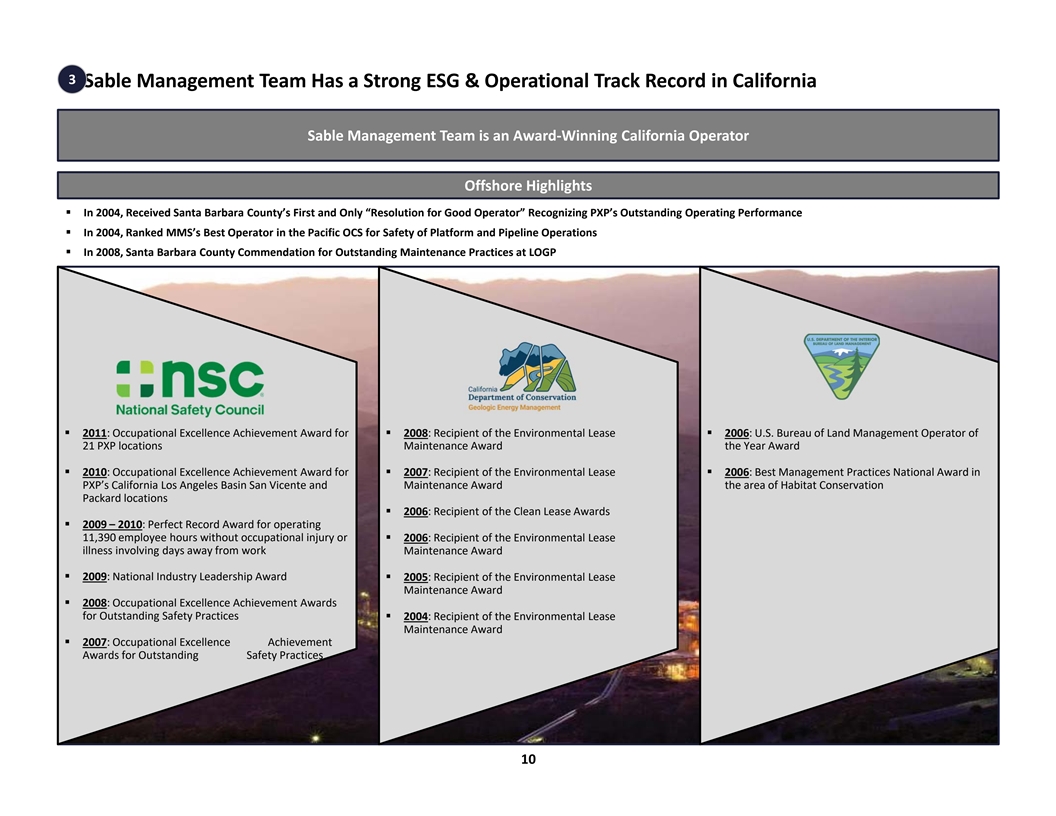

3 Sable Management Team Has a Strong ESG & Operational Track Record

in California Sable Management Team is an Award-Winning California Operator Offshore Highlights § In 2004, Received Santa Barbara County’s First and Only “Resolution for Good Operator” Recognizing PXP’s Outstanding

Operating Performance § In 2004, Ranked MMS’s Best Operator in the Pacific OCS for Safety of Platform and Pipeline Operations § In 2008, Santa Barbara County Commendation for Outstanding Maintenance Practices at LOGP § 2011:

Occupational Excellence Achievement Award for § 2008: Recipient of the Environmental Lease § 2006: U.S. Bureau of Land Management Operator of 21 PXP locations Maintenance Award the Year Award § 2010: Occupational Excellence

Achievement Award for § 2007: Recipient of the Environmental Lease § 2006: Best Management Practices National Award in PXP’s California Los Angeles Basin San Vicente and Maintenance Award the area of Habitat Conservation Packard

locations § 2006: Recipient of the Clean Lease Awards § 2009 – 2010: Perfect Record Award for operating 11,390 employee hours without occupational injury or § 2006: Recipient of the Environmental Lease illness involving days

away from work Maintenance Award § 2009: National Industry Leadership Award § 2005: Recipient of the Environmental Lease Maintenance Award § 2008: Occupational Excellence Achievement Awards for Outstanding Safety Practices§ 2004:

Recipient of the Environmental Lease Maintenance Award § 2007: Occupational Excellence Achievement Awards Awards f for or O Outstanding utstanding Safety Safety Practices Practices 10

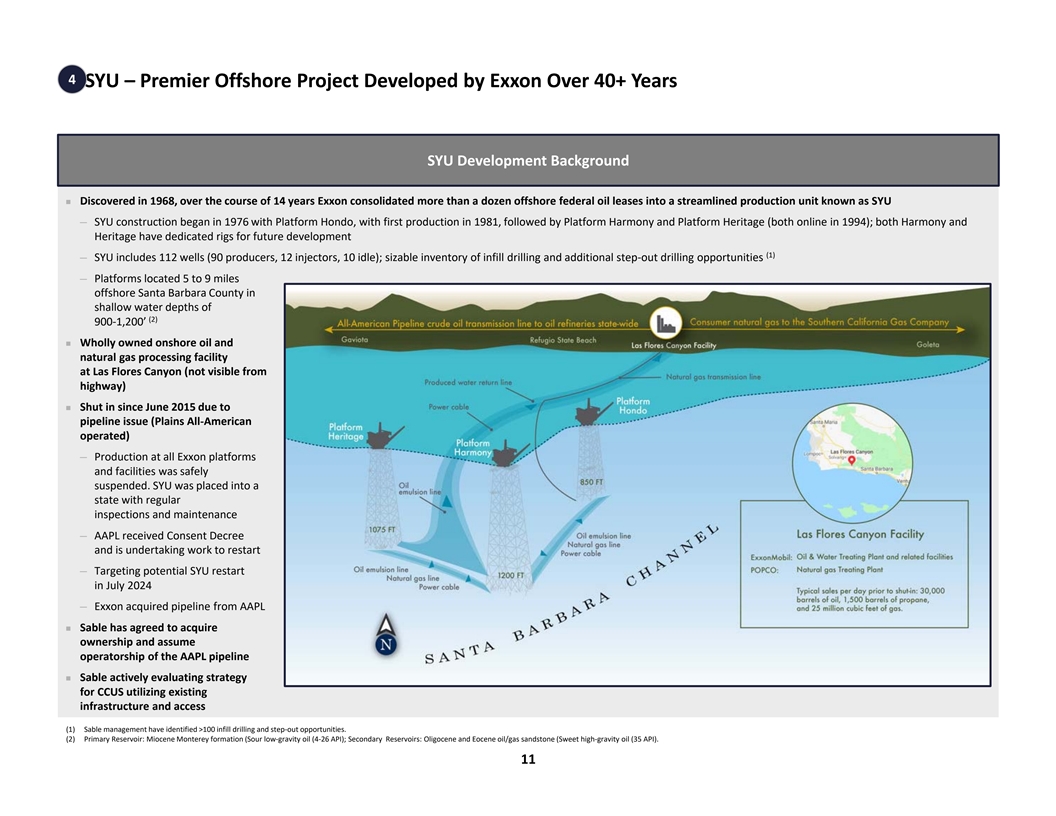

4 SYU – Premier Offshore Project Developed by Exxon Over 40+

Years SYU Development Background n Discovered in 1968, over the course of 14 years Exxon consolidated more than a dozen offshore federal oil leases into a streamlined production unit known as SYU ─ SYU construction began in 1976 with

Platform Hondo, with first production in 1981, followed by Platform Harmony and Platform Heritage (both online in 1994); both Harmony and Heritage have dedicated rigs for future development (1) ─ SYU includes 112 wells (90 producers, 12

injectors, 10 idle); sizable inventory of infill drilling and additional step-out drilling opportunities ─ Platforms located 5 to 9 miles offshore Santa Barbara County in shallow water depths of (2) 900-1,200’ n Wholly owned onshore

oil and natural gas processing facility at Las Flores Canyon (not visible from highway) n Shut in since June 2015 due to pipeline issue (Plains All-American Pipeline (“AAPL”) operated) ─ Production at all Exxon platforms and

facilities was safely suspended. SYU was placed into a preserved state with regular inspections and maintenance ─ AAPL received Consent Decree and is undertaking work to restart ─ Targeting potential SYU restart in July 2024 ─

Exxon acquired pipeline from AAPL n Sable has agreed to acquire ownership and assume operatorship of the AAPL pipeline n Sable actively evaluating strategy for CCUS utilizing existing infrastructure and access (1) Sable management have

identified >100 infill drilling and step-out opportunities. (2) Primary Reservoir: Miocene Monterey formation (Sour low-gravity oil (4-26 API); Secondary Reservoirs: Oligocene and Eocene oil/gas sandstone (Sweet high-gravity oil (35 API).

11

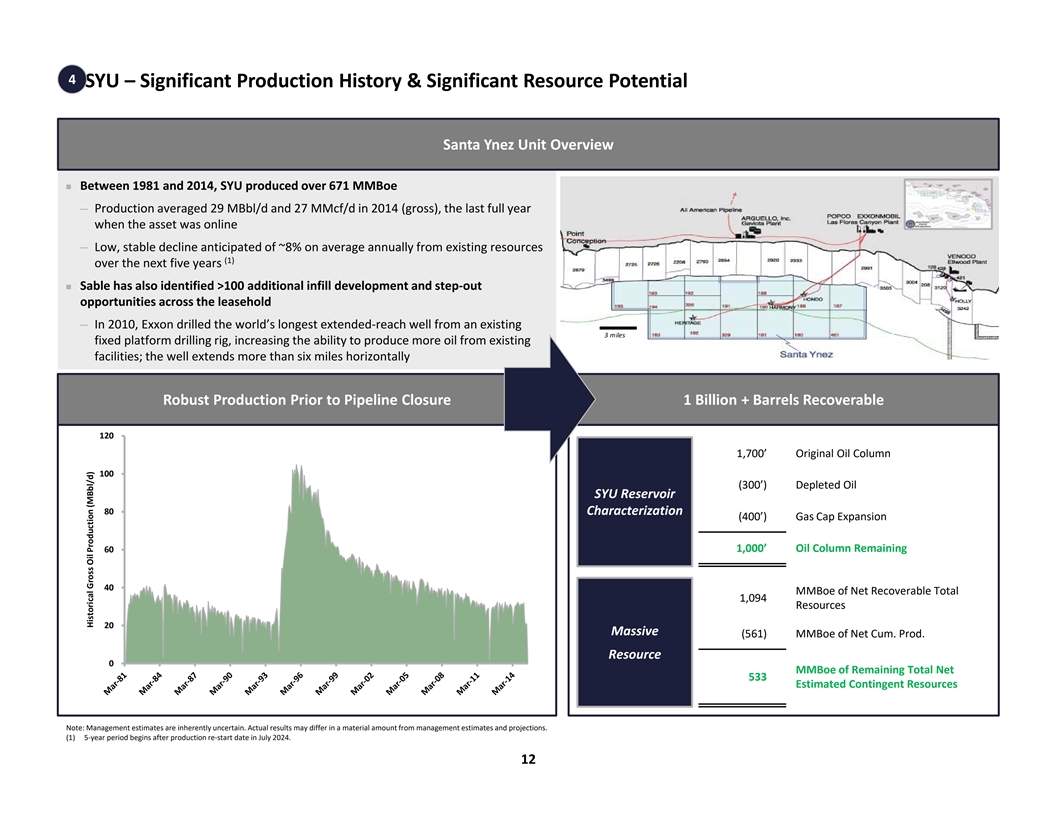

4 SYU – Significant Production History & Significant Resource

Potential Santa Ynez Unit Overview n Between 1981 and 2014, SYU produced over 671 MMBoe ─ Production averaged 29 MBbl/d and 27 MMcf/d in 2014 (gross), the last full year when the asset was online ─ Low, stable decline anticipated of

~8% on average annually from existing resources (1) over the next five years n Sable has also identified >100 additional infill development and step-out opportunities across the leasehold ─ In 2010, Exxon drilled the world’s

longest extended-reach well from an existing 3 miles fixed platform drilling rig, increasing the ability to produce more oil from existing facilities; the well extends more than six miles horizontally Robust Production Prior to Pipeline Closure 1

Billion + Barrels Recoverable 120 1,700’ Original Oil Column 100 (300’) Depleted Oil SYU Reservoir 80 Characterization (400’) Gas Cap Expansion 60 1,000’ Oil Column Remaining 40 MMBoe of Net Recoverable Total 1,094 Resources

20 Massive (561) MMBoe of Net Cum. Prod. Resource 0 MMBoe of Remaining Total Net 533 Estimated Contingent Resources Note: Management estimates are inherently uncertain. Actual results may differ in a material amount from management estimates and

projections. (1) 5-year period begins after production re-start date in July 2024. 12 Historical Gross Oil Production (MBbl/d)

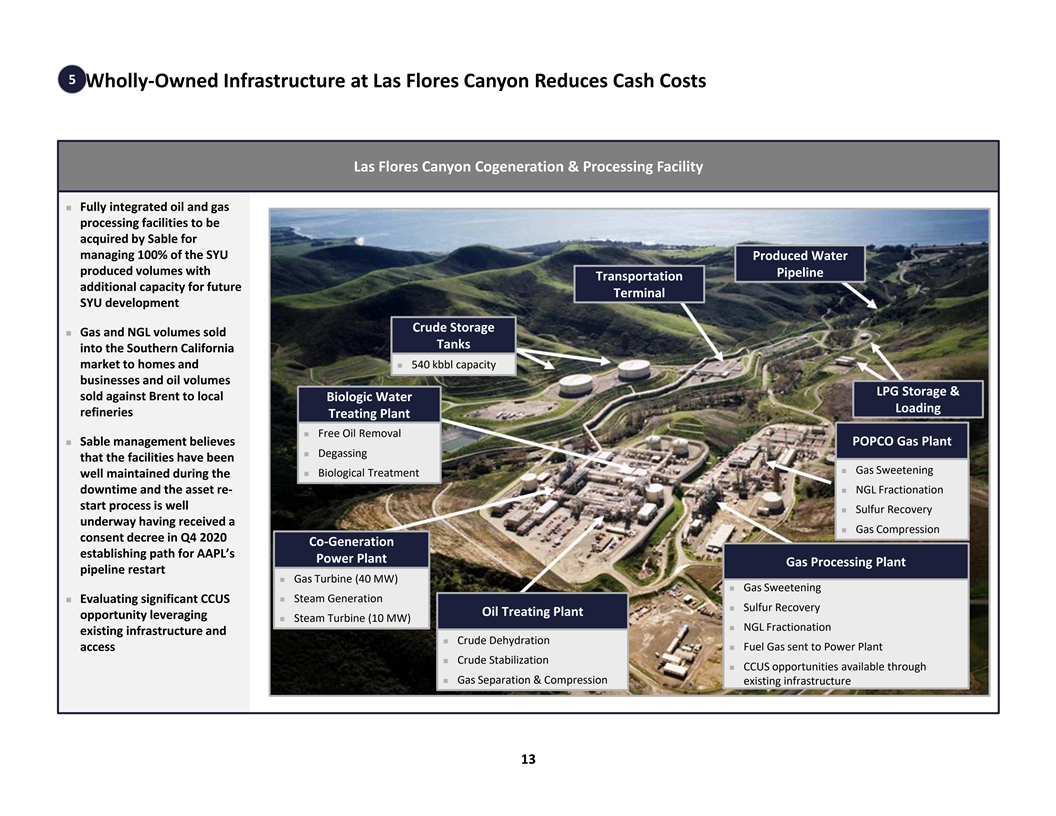

5 Wholly-Owned Infrastructure at Las Flores Canyon Reduces Cash Costs

Las Flores Canyon Cogeneration & Processing Facility n Fully integrated oil and gas processing facilities to be acquired by Sable for managing 100% of the SYU Produced Water produced volumes with Pipeline Transportation additional capacity

for future Terminal SYU development Crude Storage n Gas and NGL volumes sold Tanks into the Southern California market to homes and n 540 kbbl capacity businesses and oil volumes LPG Storage & sold against Brent to local Biologic Water

Loading refineries Treating Plant n Free Oil Removal n Sable management believes POPCO Gas Plant n Degassing that the facilities have been n Gas Sweetening well maintained during the n Biological Treatment downtime and the

asset re-n NGL Fractionation start process is well n Sulfur Recovery underway having received a n Gas Compression consent decree in Q4 2020 Co-Generation establishing path for AAPL’s Power Plant Gas Processing Plant pipeline

restart n Gas Turbine (40 MW) n Gas Sweetening n Evaluating significant CCUS n Steam Generation n Sulfur Recovery Oil Treating Plant opportunity leveraging n Steam Turbine (10 MW) n NGL Fractionation existing

infrastructure and n Crude Dehydration accessn Fuel Gas sent to Power Plant n Crude Stabilization n CCUS opportunities available through n Gas Separation & Compression existing infrastructure 13

6 Substantial Run-Rate Cash Flow Generation Once SYU Re-Start is

Complete… Ability to Implement a Robust Shareholder Return Policy Once SYU is Online (1) Forecast & Financial Summary Overview of Financial Projections – “Run Rate” Annual Cash Flow (2) Strip $90 / $4.50 $80.00 / $4.50

n Run-Rate period reflects the first 12 months after production Benchmark Price ($ / Bbl) $79.37 $90.00 $80.00 re-start, which is July 2024 through June 2025 Benchmark Price ($ / MMBtu) $6.48 $4.50 $4.50 n Sable management anticipate

initial production rates of 28.2 Oil Production (MMBoe) 9 9 9 MBoe/d based upon historic production, reservoir Gas Production (Bcf) 9 9 9 characteristics, and precedent shut-in events NGL Production (MMBoe) 0 0 0 n Base forecast production

decline of ~8% per annum for the Total Production (MMBoe) 10 10 10 initial five years after production re-start based upon Daily Rate (MBoe/d) 28.2 28.2 28.2 management forecast; NSAI decline forecast of ~8% % Oil 85% 85% 85% n Management

capital forecast assumes ~$27 MM of annual Oil Revenue $651 $744 $657 ESP capex in first three years of production, along with ~$5 Gas Revenue 59 42 42 MM of annual average capex attributable to the workover NGL Revenue 4 4 4 program over the same

period; ~$36 MM of annual average Total Revenue $714 $790 $703 capex attributable to sidetrack drilling beginning one year Production Expenses (168) (168) (168) (5) after production start Production Taxes (6) (6) (6) n Asset generates

significant free cash flow and Sable General & Administrative (38) (38) (38) anticipates implementing a robust dividend policy once the Interest Expense (83) (83) (83) asset is online Depreciation Expense (0) (0) (0) Income Taxes (0) (0) (0)

n As part of the acquisition and asset re-start, Sable will have Net Income $419 $495 $408 a large NOL that will limit corporate cash taxes in the near- Interest Expense 83 83 83 term Depreciation Expense 0 0 0 n Sable management also

plans to implement a hedging Income Taxes 0 0 0 strategy after production restarts that caps downside and (3) EBITDA $502 $578 $491 (7) preserves upside (4) Pro Forma Enterprise Value / EBITDA 2.0x 1.7x 2.0x (5) Capital Expenditures (30) (30) (30)

(8) (3) Pre-Production Estimated Costs & Expenses ($MM) Unlevered Free Cash Flow $472 $548 $461 (9) Operating Expenses $20 Interest Expense (83) (83) (83) (3) (9) General & Administrative 12 Levered Free Cash Flow $389 $465 $378 (10) (6)

Pipeline Repair and Restart 90 Total Debt $623 $623 $623 Total Debt / Run-Rate EBITDA 1.2x 1.1x 1.3x Total Pre-Production Costs & Expenses $122 Note: Sable metrics are based on management estimates. Management estimates are inherently uncertain.

Actual results may differ in a material amount from management estimates and projections. (1) Estimated re-start date of July 2024. Run-rate period reflects 12 months of cash flows following production re-start, which is July 2024 through June 2025.

In $MM unless otherwise noted. (2) 2024 monthly NYMEX Brent Crude and Socal Citygate pricing as of July 31, 2023. (3) Sable defines EBITDA as net income before interest expense, income tax expense and depletion, depreciation and amortization. Sable

defines Unlevered Free Cash Flow as EBITDA minus capital expenditures. Sable defines Levered Free Cash Flow as Unlevered Free Cash Flow minus interest expense. (4) Pro Forma Enterprise Value (“TEV”) metrics assume 100% participation from

remaining IPO shareholders, $375 MM in PIPE financing and pro forma shares outstanding of 56.1 MM (3.0 MM Merger Consideration Shares, 7.2 MM Founders Shares, 8.4 MM IPO Shares, and 37.5 MM PIPE Shares), and $10.00 per share. (5) Sable management

anticipates near-term capital expenditures will be focused on workovers and ESP installation to improve production from existing producing wellbores. st (6) Reflects initial balance of the Exxon 1 Lien Term Loan less $19 MM deposit. (7) Hedge plan

likely to consist of costless deferred premium put spread / 3-way collar strategy. Hedging strategy is consistent with Sable management prior experience. (8) Estimated costs for the period prior to production re-start in July 2024. Excludes post

effective date accrued LOE of $177 MM post Effective Time incurred from January 1, 2022 effective date associated with ongoing maintenance, transaction fees and expenses of $82 MM, and deposit paid to Exxon of $19 MM. (9) Estimated pre-production

opex from March 1, 2024 through June 30, 2024. G&A estimate reflects the same time period. (10) Estimated pipeline repair and restart accrued prior to production start date. 14

7 …& Attractive Valuation Relative to Peer Group (1) (2)

Category Acquired Asset Metric PF Multiple Peer Average st 1 Full Year Unlevered Free (4) (5) Highest Yield of the Peer Group $472 MM 47% 17% (3) Cash Flow Yield (%) st 42% Discount to Peer Group TEV / 1 Full Year (4) (5) $502 MM 2.0x 3.5x (3) on

TEV / EBITDA EBITDA NSAI Adjusted Low Estimate (1) (6) Deep Discount to Intrinsic Value Base $1,728 MM 1.7x NA Forecast PV-10 / TEV TEV / 66% Discount to Peer Group NSAI Adjusted Low Estimate (8) 133 MMBoe $7.53 $22.32 (7) on PDP Reserves Base

Contingent Resources ($/Boe) TEV / 26% Discount to Peer Group (9) 28.2 MBoe/d $35,493 $48,087 on Net Production Net Production ($/MBoe/d) Note: Sable metrics assume NYMEX Brent and Socal Citygate Pricing as of July 31, 2023 and effective date of

January 1, 2022, and are based on management estimates. Management estimates are inherently uncertain. Actual results may differ in a material amount from management estimates and projections. Sable TEV assumes 100% participation from remaining IPO

shareholders and pro forma shares outstanding of 56.1 MM (3.0 MM Merger Consideration Shares, 7.2 MM Founders Shares, 8.4 MM IPO Shares, and 37.5 MM PIPE Shares). (1) Assumes NYMEX Brent and Socal Citygate Pricing as of July 31, 2023. (5) Reflects

2024E metrics. (2) Peer group includes: BRY, CHRD, CIVI, CRC, KOS, MGY, MUR, TALO and WTI as of July 31, 2023. (6) Peer group does not disclose PDP PV-10 metrics at a similar pricing and effective date. (3) Sable defines EBITDA as net income before

interest expense, income tax expense and depletion, depreciation and amortization. Sable defines Unlevered Free Cash (7) Peer metrics assume PDP and Sable estimates are based on Low Estimate Contingent Resources. Flow as EBITDA minus capital

expenditures. (8) NYMEX SEC category for nonproducing reserves is contingent; NSAI estimate increased due to extension (4) Reflects cash flows from first 12 months online: July 2024 – June 2025. of field life with development drilling program

and management estimated LOE. 15 (9) Reflects July 2024 through June 2025 production.

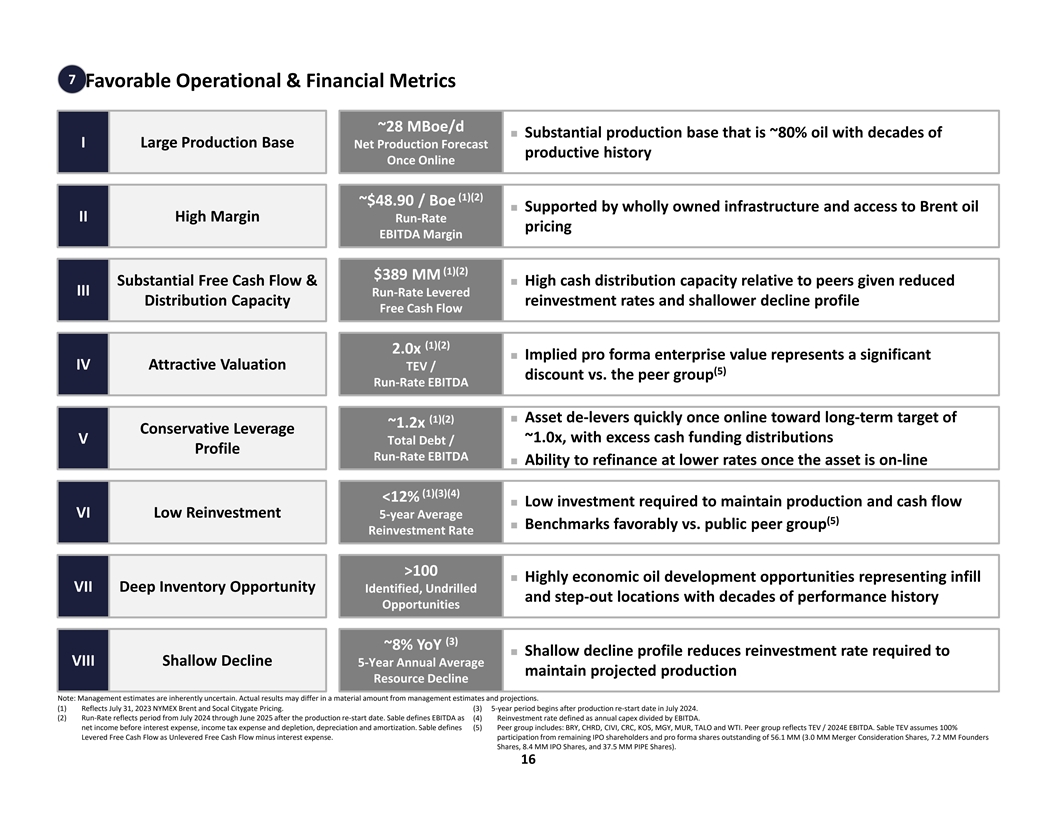

7 Favorable Operational & Financial Metrics ~28 MBoe/d n

Substantial production base that is ~80% oil with decades of I Large Production Base Net Production Forecast productive history Once Online (1)(2) ~$48.90 / Boe n Supported by wholly owned infrastructure and access to Brent oil II High Margin

Run-Rate pricing EBITDA Margin (1)(2) $389 MM Substantial Free Cash Flow & n High cash distribution capacity relative to peers given reduced III Run-Rate Levered Distribution Capacity reinvestment rates and shallower decline profile Free

Cash Flow (1)(2) 2.0x n Implied pro forma enterprise value represents a significant IV Attractive Valuation TEV / (5) discount vs. the peer group Run-Rate EBITDA (1)(2)n Asset de-levers quickly once online toward long-term target of ~1.2x

Conservative Leverage ~1.0x, with excess cash funding distributions V Total Debt / Profile Run-Rate EBITDA n Ability to refinance at lower rates once the asset is on-line (1)(3)(4) <12% n Low investment required to maintain production

and cash flow VI Low Reinvestment 5-year Average (5) n Benchmarks favorably vs. public peer group Reinvestment Rate >100 n Highly economic oil development opportunities representing infill VII Deep Inventory Opportunity Identified,

Undrilled and step-out locations with decades of performance history Opportunities (3) ~8% YoY n Shallow decline profile reduces reinvestment rate required to VIII Shallow Decline 5-Year Annual Average maintain projected production Resource

Decline Note: Management estimates are inherently uncertain. Actual results may differ in a material amount from management estimates and projections. (1) Reflects July 31, 2023 NYMEX Brent and Socal Citygate Pricing. (3) 5-year period begins after

production re-start date in July 2024. (2) Run-Rate reflects period from July 2024 through June 2025 after the production re-start date. Sable defines EBITDA as (4) Reinvestment rate defined as annual capex divided by EBITDA. net income before

interest expense, income tax expense and depletion, depreciation and amortization. Sable defines (5) Peer group includes: BRY, CHRD, CIVI, CRC, KOS, MGY, MUR, TALO and WTI. Peer group reflects TEV / 2024E EBITDA. Sable TEV assumes 100% Levered Free

Cash Flow as Unlevered Free Cash Flow minus interest expense. participation from remaining IPO shareholders and pro forma shares outstanding of 56.1 MM (3.0 MM Merger Consideration Shares, 7.2 MM Founders Shares, 8.4 MM IPO Shares, and 37.5 MM PIPE

Shares). 16

Additional Detail

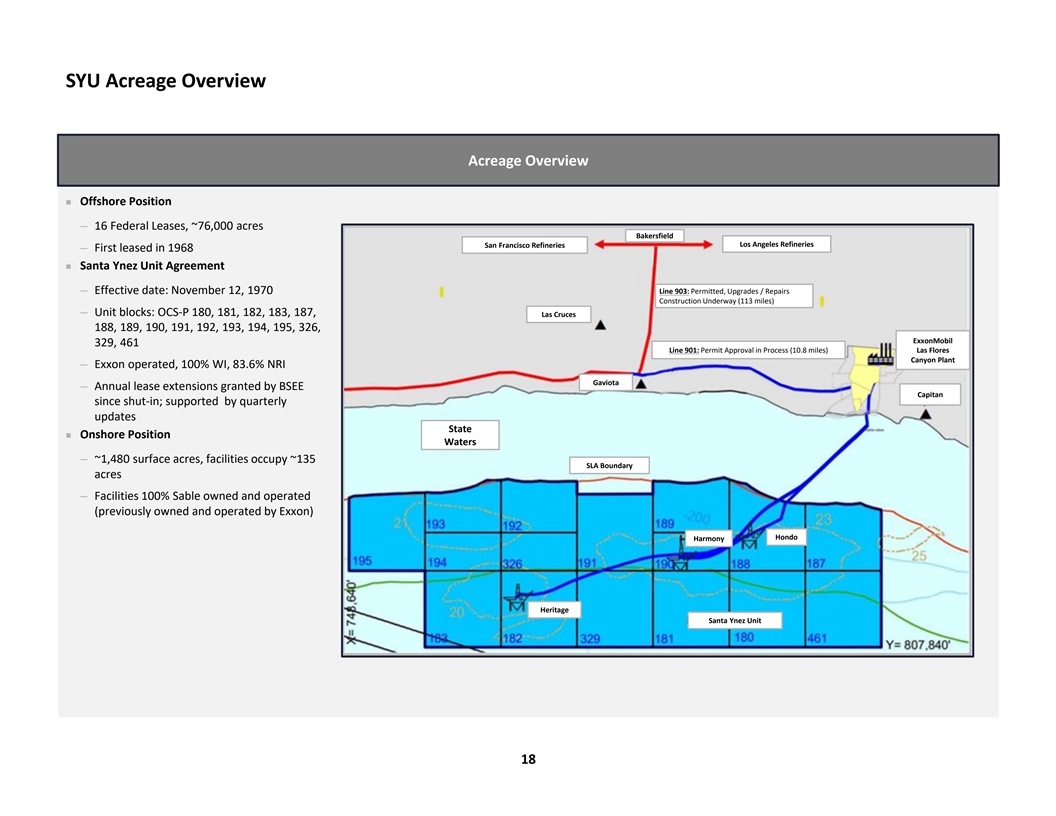

SYU Acreage Overview Acreage Overview n Offshore Position ─

16 Federal Leases, ~76,000 acres Bakersfield Los Angeles Refineries San Francisco Refineries ─ First leased in 1968 n Santa Ynez Unit Agreement ─ Effective date: November 12, 1970 Line 903: Permitted, Upgrades / Repairs Construction

Underway (113 miles) ─ Unit blocks: OCS-P 180, 181, 182, 183, 187, Las Cruces 188, 189, 190, 191, 192, 193, 194, 195, 326, ExxonMobil 329, 461 Line 901: Permit Approval in Process (10.8 miles) Las Flores Canyon Plant ─ Exxon operated,

100% WI, 83.6% NRI Gaviota ─ Annual lease extensions granted by BSEE Capitan since shut-in; supported by quarterly updates State n Onshore Position Waters ─ ~1,480 surface acres, facilities occupy ~135 SLA Boundary acres ─

Facilities 100% Sable owned and operated (previously owned and operated by Exxon) Hondo Harmony Heritage Santa Ynez Unit 18

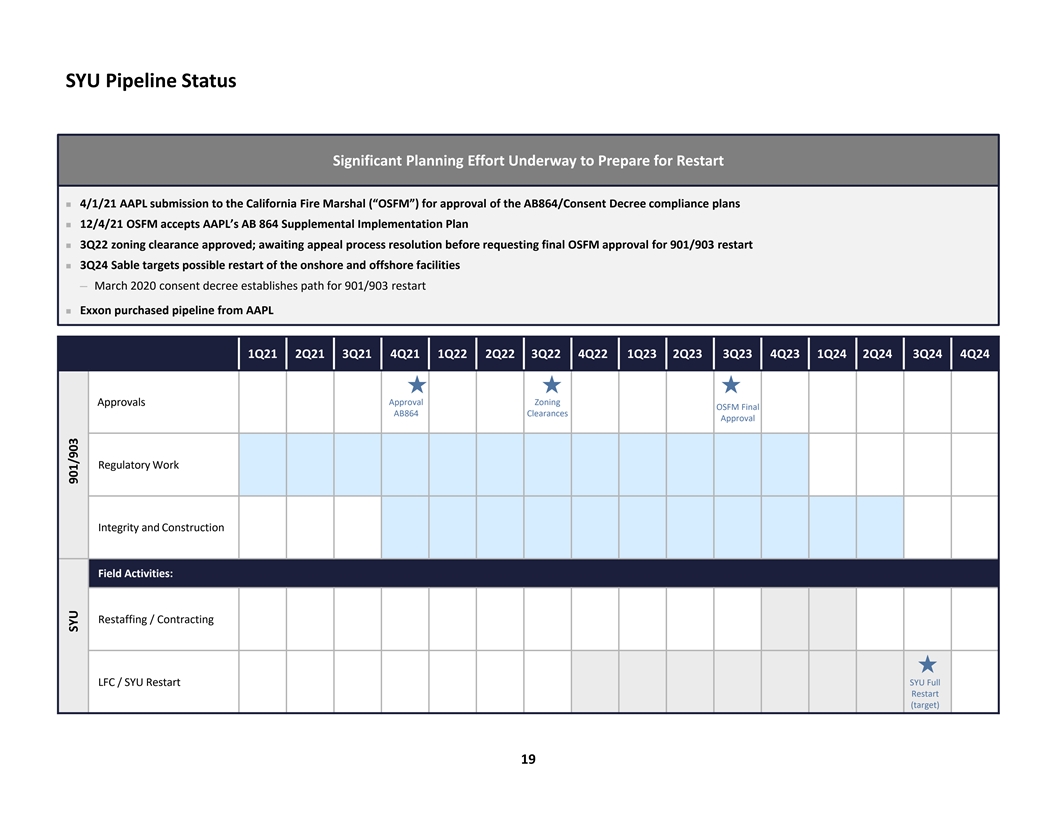

SYU Pipeline Status Significant Planning Effort Underway to Prepare for

Restart n 4/1/21 AAPL submission to the California Fire Marshal (“OSFM”) for approval of the AB864/Consent Decree compliance plans n 12/4/21 OSFM accepts AAPL’s AB 864 Supplemental Implementation Plan n 3Q22 zoning

clearance approved; awaiting appeal process resolution before requesting final OSFM approval for 901/903 restart n 3Q24 Sable targets possible restart of the onshore and offshore facilities ─ March 2020 consent decree establishes path for

901/903 restart n Exxon purchased pipeline from AAPL 1Q21 2Q21 3Q21 4Q21 1Q22 2Q22 3Q22 4Q22 1Q23 2Q23 3Q23 4Q23 1Q24 2Q24 3Q24 4Q24 Approval Zoning Approvals OSFM Final AB864 Clearances Approval Regulatory Work Integrity and Construction Field

Activities: Restaffing / Contracting SYU Full LFC / SYU Restart Restart (target) 19 SYU 901/903

Undrilled Inventory Overview New Drill Inventory Overview n SYU

comprises several discrete fault bound accumulations; compartments defined by pressure compartments n 2015 analysis identified step out potential for untested fault compartments or sub accumulations ─ Technical opportunity inventory based

on spacing assumptions range from 20–80 acres (102 total opportunities) ─ For every platform, more opportunities exist than available donor wellbores at current spacing assumptions (i.e., slot-constrained) Hondo Harmony Heritage 13°

API Elevation 2014/2015 Campaign Drillwell Infill / Step-Out Drilling Opportunity Success Case Step-Out Offset Opportunity Being Matured for Drilling Prior To Shut in 20

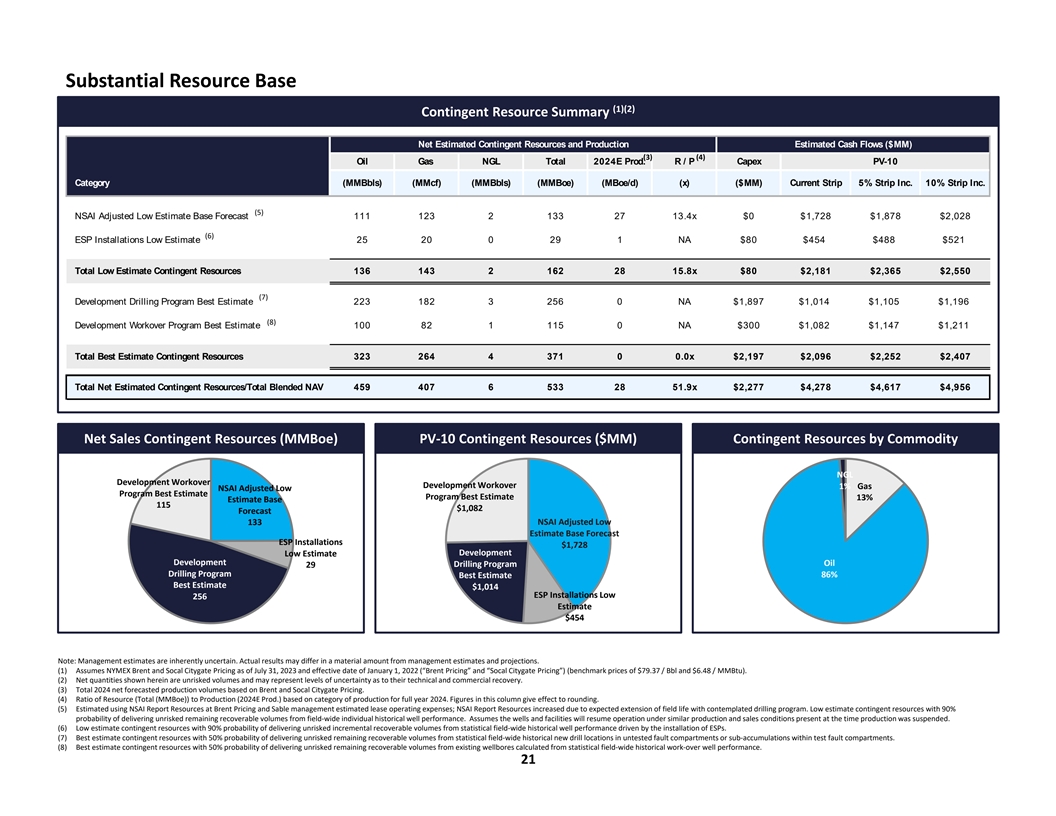

Substantial Resource Base (1)(2) Contingent Resource Summary Net

Estimated Contingent Resources and Production Estimated Cash Flows ($MM) (3) (4) Oil Gas NGL Total 2024E Prod. R / P Capex PV-10 Category (MMBbls) (MMcf) (MMBbls) (MMBoe) (MBoe/d) (x) ($MM) Current Strip 5% Strip Inc. 10% Strip Inc. (5) NSAI

Adjusted Low Estimate Base Forecast 111 123 2 133 27 13.4x $0 $1,728 $1,878 $2,028 (6) ESP Installations Low Estimate 25 20 0 29 1 NA $80 $454 $488 $521 Total Low Estimate Contingent Resources 136 143 2 162 28 15.8x $80 $2,181 $2,365 $2,550 (7)

Development Drilling Program Best Estimate 223 182 3 256 0 NA $1,897 $1,014 $1,105 $1,196 (8) Development Workover Program Best Estimate 100 82 1 115 0 NA $300 $1,082 $1,147 $1,211 Total Best Estimate Contingent Resources 323 264 4 371 0 0.0x $2,197

$2,096 $2,252 $2,407 Total Net Estimated Contingent Resources/Total Blended NAV 459 407 6 533 28 51.9x $2,277 $4,278 $4,617 $4,956 Net Sales Contingent Resources (MMBoe) PV-10 Contingent Resources ($MM) Contingent Resources by Commodity NGL

Development Workover Development Workover 1% Gas NSAI Adjusted Low Program Best Estimate Program Best Estimate 13% Estimate Base 115 $1,082 Forecast 133 NSAI Adjusted Low Estimate Base Forecast ESP Installations $1,728 Development Low Estimate

Development Drilling Program Oil 29 Drilling Program 86% Best Estimate Best Estimate $1,014 ESP Installations Low 256 Estimate $454 Note: Management estimates are inherently uncertain. Actual results may differ in a material amount from management

estimates and projections. (1) Assumes NYMEX Brent and Socal Citygate Pricing as of July 31, 2023 and effective date of January 1, 2022 (“Brent Pricing” and “Socal Citygate Pricing”) (benchmark prices of $79.37 / Bbl and

$6.48 / MMBtu). (2) Net quantities shown herein are unrisked volumes and may represent levels of uncertainty as to their technical and commercial recovery. (3) Total 2024 net forecasted production volumes based on Brent and Socal Citygate Pricing.

(4) Ratio of Resource (Total (MMBoe)) to Production (2024E Prod.) based on category of production for full year 2024. Figures in this column give effect to rounding. (5) Estimated using NSAI Report Resources at Brent Pricing and Sable management

estimated lease operating expenses; NSAI Report Resources increased due to expected extension of field life with contemplated drilling program. Low estimate contingent resources with 90% probability of delivering unrisked remaining recoverable

volumes from field-wide individual historical well performance. Assumes the wells and facilities will resume operation under similar production and sales conditions present at the time production was suspended. (6) Low estimate contingent resources

with 90% probability of delivering unrisked incremental recoverable volumes from statistical field-wide historical well performance driven by the installation of ESPs. (7) Best estimate contingent resources with 50% probability of delivering

unrisked remaining recoverable volumes from statistical field-wide historical new drill locations in untested fault compartments or sub-accumulations within test fault compartments. (8) Best estimate contingent resources with 50% probability of

delivering unrisked remaining recoverable volumes from existing wellbores calculated from statistical field-wide historical work-over well performance. 21

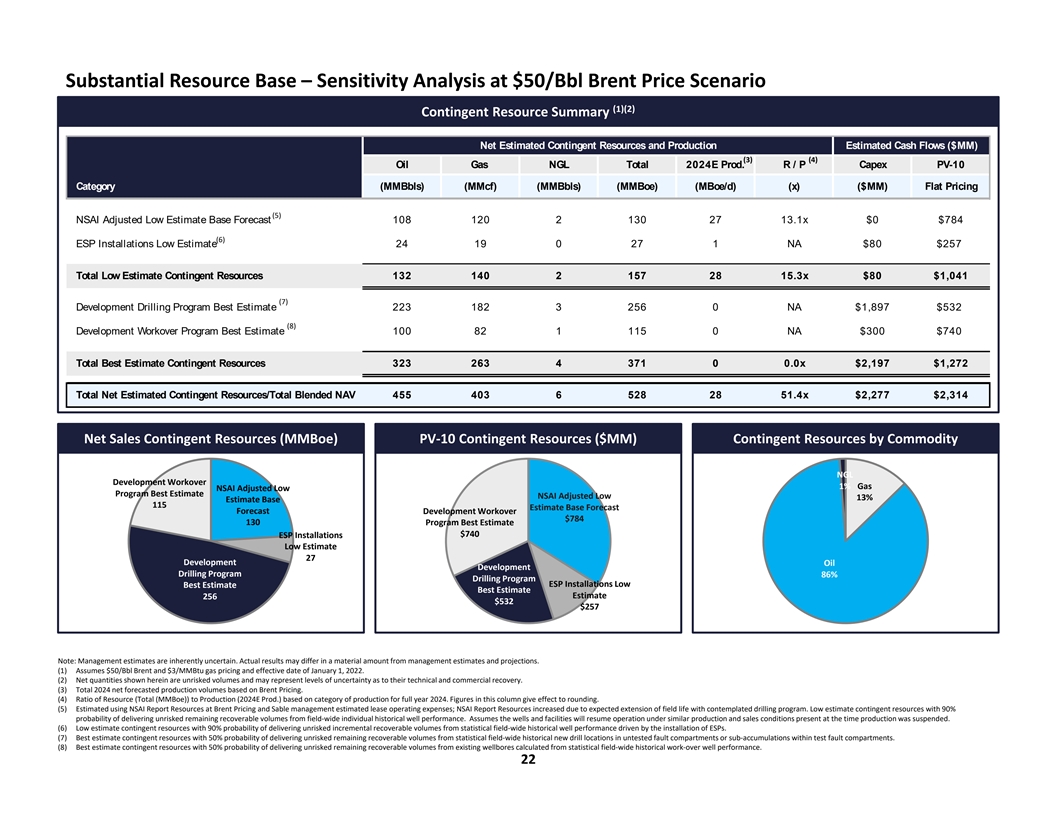

Substantial Resource Base – Sensitivity Analysis at $50/Bbl Brent

Price Scenario (1)(2) Contingent Resource Summary Net Estimated Contingent Resources and Production Estimated Cash Flows ($MM) (3) (4) Oil Gas NGL Total 2024E Prod. R / P Capex PV-10 Category (MMBbls) (MMcf) (MMBbls) (MMBoe) (MBoe/d) (x) ($MM) Flat

Pricing (5) NSAI Adjusted Low Estimate Base Forecast 108 120 2 130 27 13.1x $0 $784 (6) ESP Installations Low Estimate 24 19 0 27 1 NA $80 $257 Total Low Estimate Contingent Resources 132 140 2 157 28 15.3x $80 $1,041 (7) Development Drilling

Program Best Estimate 223 182 3 256 0 NA $1,897 $532 (8) Development Workover Program Best Estimate 100 82 1 115 0 NA $300 $740 Total Best Estimate Contingent Resources 323 263 4 371 0 0.0x $2,197 $1,272 Total Net Estimated Contingent

Resources/Total Blended NAV 455 403 6 528 28 51.4x $2,277 $2,314 Net Sales Contingent Resources (MMBoe) PV-10 Contingent Resources ($MM) Contingent Resources by Commodity NGL Development Workover 1% Gas NSAI Adjusted Low Program Best Estimate NSAI

Adjusted Low 13% Estimate Base 115 Estimate Base Forecast Forecast Development Workover $784 130 Program Best Estimate $740 ESP Installations Low Estimate 27 Development Oil Development Drilling Program 86% Drilling Program ESP Installations Low

Best Estimate Best Estimate Estimate 256 $532 $257 Note: Management estimates are inherently uncertain. Actual results may differ in a material amount from management estimates and projections. (1) Assumes $50/Bbl Brent and $3/MMBtu gas pricing and

effective date of January 1, 2022. (2) Net quantities shown herein are unrisked volumes and may represent levels of uncertainty as to their technical and commercial recovery. (3) Total 2024 net forecasted production volumes based on Brent Pricing.

(4) Ratio of Resource (Total (MMBoe)) to Production (2024E Prod.) based on category of production for full year 2024. Figures in this column give effect to rounding. (5) Estimated using NSAI Report Resources at Brent Pricing and Sable management

estimated lease operating expenses; NSAI Report Resources increased due to expected extension of field life with contemplated drilling program. Low estimate contingent resources with 90% probability of delivering unrisked remaining recoverable

volumes from field-wide individual historical well performance. Assumes the wells and facilities will resume operation under similar production and sales conditions present at the time production was suspended. (6) Low estimate contingent resources

with 90% probability of delivering unrisked incremental recoverable volumes from statistical field-wide historical well performance driven by the installation of ESPs. (7) Best estimate contingent resources with 50% probability of delivering

unrisked remaining recoverable volumes from statistical field-wide historical new drill locations in untested fault compartments or sub-accumulations within test fault compartments. (8) Best estimate contingent resources with 50% probability of

delivering unrisked remaining recoverable volumes from existing wellbores calculated from statistical field-wide historical work-over well performance. 22

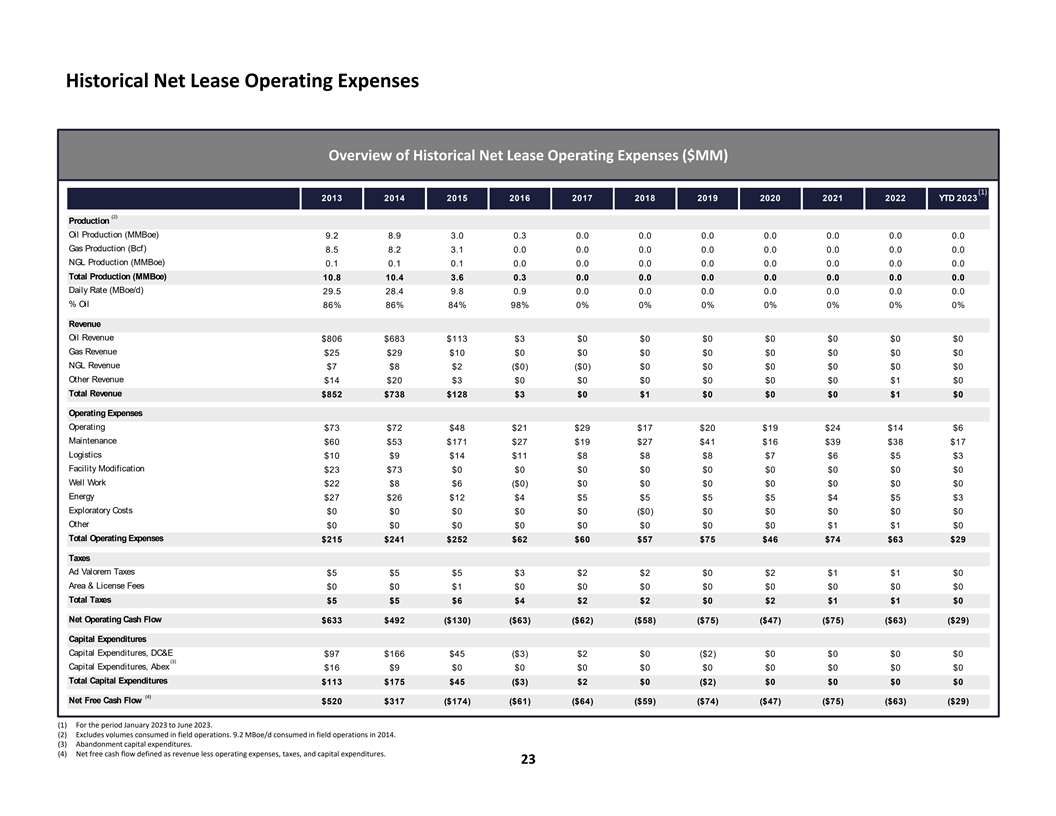

Historical Net Lease Operating Expenses Overview of Historical Net

Lease Operating Expenses ($MM) (1) 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 YTD 2023 (2) Production Oil Production (MMBoe) 9.2 8.9 3.0 0.3 0.0 0.0 0.0 0.0 0.0 0.0 0.0 Gas Production (Bcf) 8.5 8.2 3.1 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 NGL

Production (MMBoe) 0.1 0.1 0.1 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 Total Production (MMBoe) 10.8 10.4 3.6 0.3 0.0 0.0 0.0 0.0 0.0 0.0 0.0 Daily Rate (MBoe/d) 29.5 28.4 9.8 0.9 0.0 0.0 0.0 0.0 0.0 0.0 0.0 % Oil 86% 86% 84% 98% 0% 0% 0% 0% 0% 0% 0%

Revenue Oil Revenue $806 $683 $113 $3 $0 $0 $0 $0 $0 $0 $0 Gas Revenue $25 $29 $10 $0 $0 $0 $0 $0 $0 $0 $0 NGL Revenue $7 $8 $2 ($0) ($0) $0 $0 $0 $0 $0 $0 Other Revenue $14 $20 $3 $0 $0 $0 $0 $0 $0 $1 $0 Total Revenue $852 $738 $128 $3 $0 $1 $0 $0

$0 $1 $0 Operating Expenses Operating $73 $72 $48 $21 $29 $17 $20 $19 $24 $14 $6 Maintenance $60 $53 $171 $27 $19 $27 $41 $16 $39 $38 $17 Logistics $10 $9 $14 $11 $8 $8 $8 $7 $6 $5 $3 Facility Modification $23 $73 $0 $0 $0 $0 $0 $0 $0 $0 $0 Well

Work $22 $8 $6 ($0) $0 $0 $0 $0 $0 $0 $0 Energy $27 $26 $12 $4 $5 $5 $5 $5 $4 $5 $3 Exploratory Costs $0 $0 $0 $0 $0 ($0) $0 $0 $0 $0 $0 Other $0 $0 $0 $0 $0 $0 $0 $0 $1 $1 $0 Total Operating Expenses $215 $241 $252 $62 $60 $57 $75 $46 $74 $63 $29

Taxes Ad Valorem Taxes $5 $5 $5 $3 $2 $2 $0 $2 $1 $1 $0 Area & License Fees $0 $0 $1 $0 $0 $0 $0 $0 $0 $0 $0 Total Taxes $5 $5 $6 $4 $2 $2 $0 $2 $1 $1 $0 Net Operating Cash Flow $633 $492 ($130) ($63) ($62) ($58) ($75) ($47) ($75) ($63) ($29)

Capital Expenditures Capital Expenditures, DC&E $97 $166 $45 ($3) $2 $0 ($2) $0 $0 $0 $0 (3) Capital Expenditures, Abex $16 $9 $0 $0 $0 $0 $0 $0 $0 $0 $0 Total Capital Expenditures $113 $175 $45 ($3) $2 $0 ($2) $0 $0 $0 $0 (4) Net Free Cash Flow

$520 $317 ($174) ($61) ($64) ($59) ($74) ($47) ($75) ($63) ($29) (1) For the period January 2023 to June 2023. (2) Excludes volumes consumed in field operations. 9.2 MBoe/d consumed in field operations in 2014. (3) Abandonment capital expenditures.

(4) Net free cash flow defined as revenue less operating expenses, taxes, and capital expenditures. 23

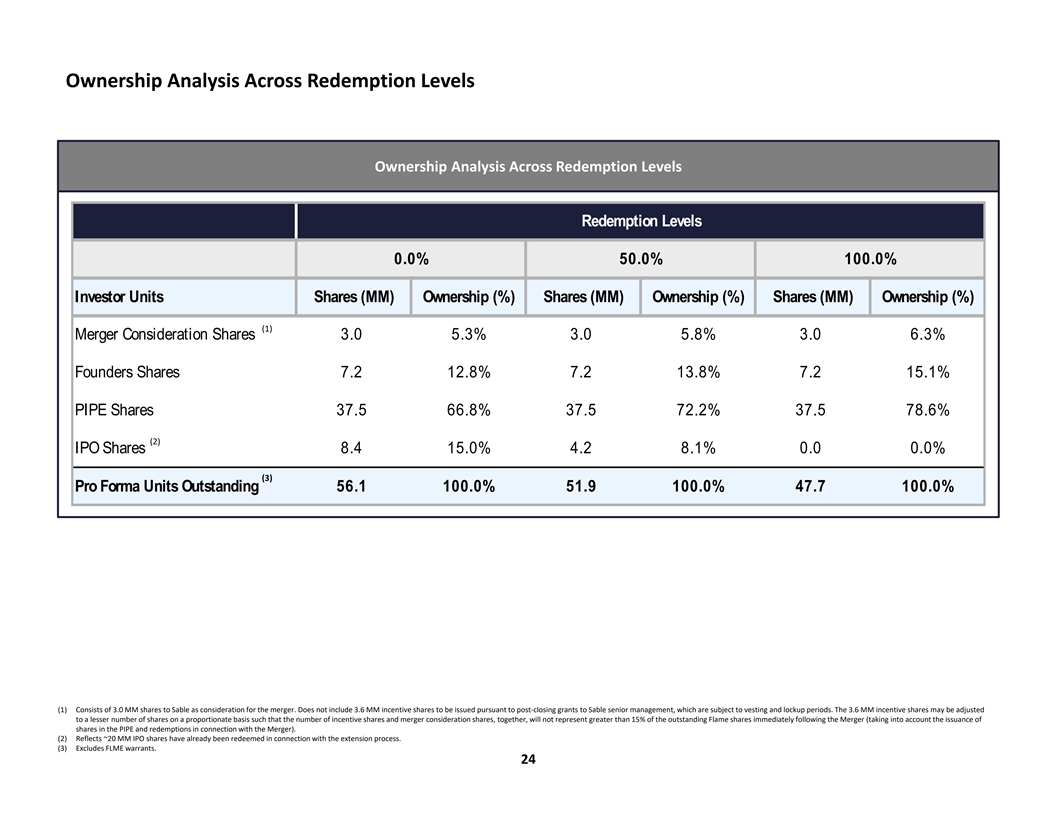

Ownership Analysis Across Redemption Levels Ownership Analysis Across

Redemption Levels Redemption Levels 0.0% 50.0% 100.0% Investor Units Shares (MM) Ownership (%) Shares (MM) Ownership (%) Shares (MM) Ownership (%) (1) Merger Consideration Shares 3.0 5.3% 3.0 5.8% 3.0 6.3% Founders Shares 7.2 12.8% 7.2 13.8% 7.2

15.1% PIPE Shares 37.5 66.8% 37.5 72.2% 37.5 78.6% (2) IPO Shares 8.4 15.0% 4.2 8.1% 0.0 0.0% (3) Pro Forma Units Outstanding 56.1 100.0% 51.9 100.0% 47.7 100.0% (1) Consists of 3.0 MM shares to Sable as consideration for the merger. Does not

include 3.6 MM incentive shares to be issued pursuant to post-closing grants to Sable senior management, which are subject to vesting and lockup periods. The 3.6 MM incentive shares may be adjusted to a lesser number of shares on a proportionate

basis such that the number of incentive shares and merger consideration shares, together, will not represent greater than 15% of the outstanding Flame shares immediately following the Merger (taking into account the issuance of shares in the PIPE

and redemptions in connection with the Merger). (2) Reflects ~20 MM IPO shares have already been redeemed in connection with the extension process. (3) Excludes FLME warrants. 24

Summary Risk Factors Risks Related to Restart of Production We need to

satisfy a number of permitting obligations and other requirements before we can restart production. The requirements to restart Lines 901 and 903 include those set forth in a federal court consent decree. While the operator of the lines has

satisfied most of the conditions to restart including under the consent decree, there is no assurance that we will be successful in satisfying the remainder of the requirements and restarting production in a timely manner. Our assumptions and

estimates regarding the total costs associated with restarting production may be inaccurate. Risks Related to the Business of SYU Our business plans require significant amount of capital. In addition, our future capital needs may require us to issue

additional equity or debt securities that may dilute our shareholders or introduce covenants that may restrict our operations or ability to pay dividends. We are subject to anti-corruption, anti-bribery, anti-money laundering, financial and economic

sanctions and similar laws, and noncompliance with such laws can subject us to administrative, civil and criminal fines and penalties, collateral consequences, remedial measures and legal expenses, all of which could adversely affect out business,

results of operations, financial condition, and reputation. Changes in U.S. or international trade policy, including the continuation or imposition of tariffs and the resulting consequences, could adversely affect our business, prospects, financial

condition, and operating results. Any financial or economic crisis, or perceived threat of such a crisis, including a significant decrease in consumer confidence, may materially and adversely affect our business, financial condition, and results of

operations. Our business, financial condition and results of operations may be adversely affected by pandemics (including COVID-19) and epidemics, natural disasters, terrorist activities, political unrest, and other outbreaks. Our estimated

quantities of petroleum are classified as “contingent resources” rather than “reserves” because they are subject to numerous contingencies. There is no assurance that any of the estimated resources will ever be recovered or

reclassified as “reserves.” Our estimated resources are based on many assumptions that may prove to be inaccurate. Any material inaccuracies in these resource estimates or underlying assumptions will materially affect the quantities and

present value of our resources. We are subject to compliance with environmental and occupational safety and health laws and regulations that may expose us to significant costs and liabilities. Our ability to retain and/or obtain necessary licenses

and permits to operate the business may negatively impact our financial results. Oil, natural gas and natural gas liquids, or “NGL” prices are volatile, due to factors beyond our control, and greatly affect SYU’s business, results

of operations and financial condition. Any decline in, or sustained low levels of, oil, natural gas and NGL prices will cause a decline in SYU’s cash flow from operations, which could materially and adversely affect its business, results of

operations and financial condition. If commodity prices decline and remain depressed for a prolonged period, SYU’s business may become uneconomic and result in write downs of the value of our properties, which may adversely affect our

financial condition and our ability to fund operations. An increase in the differential between the Brent or other benchmark prices of oil and natural gas and the wellhead price we expect to receive for our future production could significantly

reduce our cash flow and adversely affect our financial condition. Our hedging strategy in the future may not effectively mitigate the impact of commodity price volatility from our cash flows, and our hedging activities could result in cash losses

and may limit potential gains. Developing and producing oil, natural gas and NGLs are costly and high-risk activities with many uncertainties that may adversely affect our business, financial condition, results of operations and cash flows. Many of

these risks are heightened for us due to the fact that most of our equipment has been shut-in for more than seven years. Development and production of oil, natural gas and/or NGLs in offshore waters have inherent and historically higher risk than

similar activities onshore. Oil and natural gas producers’ operations are substantially dependent on the availability of water and the disposal of waste, including produced water and drilling fluids. Restrictions on the ability to obtain water

or dispose of waste may impact our operations. The unavailability or high cost of equipment, supplies and crews could delay our operations, increase our costs and delay forecasted revenue. The third parties on whom we rely for transportation

services are subject to complex federal, state and other laws that could adversely affect the cost, manner or feasibility of conducting our business. Our business depends in part on pipelines, gathering systems and processing facilities owned by us

or others. Any limitation in the availability of those facilities could interfere with our ability to market our oil, natural gas and NGL production. We may incur losses as a result of title defects or deficiencies in our properties. We will not own

all of the land on which the assets are located or all of the land that we must traverse in order to conduct our operations. There are disputes with respect to certain of the rights-of-way or other interests and any unfavorable outcomes of such