BNY Mellon Municipal Income, Inc.

BNY Mellon Municipal Income, Inc.

| |

ANNUAL REPORT September 30, 2024 |

| |

|

| |

BNY Mellon Municipal Income, Inc. Protecting Your Privacy

Our

Pledge to You THE FUND IS COMMITTED TO YOUR PRIVACY. On this page, you will

find the fund’s policies and practices for collecting, disclosing, and safeguarding “nonpublic personal

information,” which may include financial or other customer information. These policies apply to individuals

who purchase fund shares for personal, family, or household purposes, or have done so in the past. This

notification replaces all previous statements of the fund’s consumer privacy policy, and may be amended

at any time. We’ll keep you informed of changes as required by law. YOUR

ACCOUNT IS PROVIDED IN A SECURE ENVIRONMENT. The fund maintains physical, electronic and procedural safeguards

that comply with federal regulations to guard nonpublic personal information. The fund’s agents and

service providers have limited access to customer information based on their role in servicing your account. THE FUND COLLECTS INFORMATION IN ORDER TO SERVICE AND ADMINISTER YOUR ACCOUNT.

The

fund collects a variety of nonpublic personal information, which may include: • Information we receive from you, such as your name, address,

and social security number. • Information

about your transactions with us, such as the purchase or sale of fund shares. • Information we receive from agents and service providers,

such as proxy voting information. THE FUND DOES NOT SHARE NONPUBLIC PERSONAL

INFORMATION WITH ANYONE, EXCEPT AS PERMITTED BY LAW. Thank you for this opportunity

to serve you. |

| |

The views expressed

in this report reflect those of the portfolio manager(s) only through the end of the period covered and

do not necessarily represent the views of BNY Mellon Investment Adviser, Inc. or any other person in

the BNY Mellon Investment Adviser, Inc. organization. Any such views are subject to change at any time

based upon market or other conditions and BNY Mellon Investment Adviser, Inc. disclaims any responsibility

to update such views. These views may not be relied on as investment advice and, because investment decisions

for a fund in the BNY Mellon Family of Funds are based on numerous factors, may not be relied on as an

indication of trading intent on behalf of any fund in the BNY Mellon Family of Funds. |

| |

Not FDIC-Insured • Not Bank-Guaranteed • May Lose Value |

Contents

T H E F U N D

F O R M O R E I N F O R M AT I O N

Back Cover

| |

| |

Save time. Save paper. View your next shareholder report online as soon as it’s

available. Log into www.bny.com/investments and sign up for eCommunications. It’s simple and only takes

a few minutes. |

DISCUSSION

OF FUND PERFORMANCE (Unaudited)

How did the Fund perform last year?

For the 12-month period ended September

30, 2024, BNY Mellon Municipal Income, Inc. (the “fund”) produced a total return of 18.63% on a net-asset-value

basis and 32.73% on a market basis.1 Over the same period, the fund provided

tax-exempt income dividends of $.196 per share, which reflects a distribution rate of 2.68%.2

In comparison, the Bloomberg U.S. Municipal Bond Index (the “Index”), the fund’s benchmark, posted

a total return of 10.37% for the same period.3

What affected the Fund’s

performance?

· Early

in the period, the market was hampered by higher inflation and a tight monetary policy. The market rebounded

later in the period supported by anticipation that Fed rate-hiking was nearing an end and then additionally

by the Fed rate cut in September.

· Security

selections added most to performance, especially in the education, special tax and water & sewer

sectors. Longer relative duration and curve positioning also contributed positively as rates declined.

· Though

an overweight to revenue bonds was broadly positive, overweight allocations to pre-refunded bonds and

to tobacco bonds hampered fund performance.

1

Total return includes reinvestment of dividends and any capital

gains paid, based upon net asset value per share or market price per share, as applicable. Past performance

is no guarantee of future results. Market price per share, net asset value per share and investment return

fluctuate.

2 Distribution

rate per share is based upon dividends per share paid from net investment income during the period, divided

by the market price per share at the end of the period, adjusted for any capital gain distributions.

3 Source:

Lipper Inc. — The Bloomberg U.S. Municipal Bond Index covers the U.S. dollar denominated long term

tax exempt bond market. Unlike a fund, the Index is not subject to fees and other expenses. Investors

can not invest directly in any index.

2

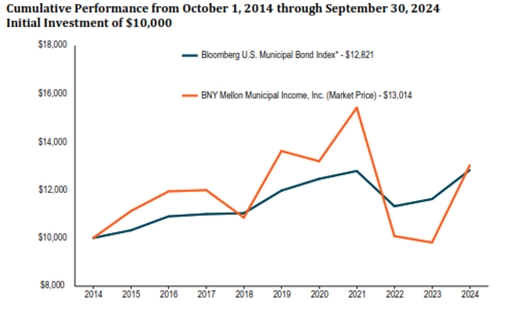

FUND

PERFORMANCE (Unaudited)

Years Ended 9/30

* Source:

Lipper Inc.

Past performance is not predictive of future performance.

The above graph compares a hypothetical investment of $10,000 made in BNY Mellon

Municipal Income, Inc. on 10/1/2014 to a hypothetical investment of $10,000 made in the Index on that

date. All figures for the fund are based on market price. All dividends and capital gain distributions

are reinvested.

The fund invests primarily in municipal securities and its

performance shown in the line graph takes into account fees and expenses. The Index covers the U.S. dollar-denominated

long-term tax-exempt bond market. Unlike a fund, the Index is not subject to fees and other expenses.

Investors cannot invest directly in any index. Further information relating to fund performance, including

expense reimbursements, if applicable, is contained in the Financial Highlights within this report and

elsewhere in this report.

3

FUND

PERFORMANCE (Unaudited) (continued)

| | | | |

Average Annual Total Returns as of 9/30/2024 |

| 1

Year | 5 Years | 10 Years |

BNY Mellon Municipal

Income, Inc. Market Price | 32.73% | -.85% | 2.70% |

BNY Mellon Municipal Income, Inc. Net Asset Value | 18.63% | .57% | 2.79% |

Bloomberg

U.S. Municipal Bond Index | 10.37% | 1.39% | 2.52% |

The performance data quoted

represents past performance, which is no guarantee of future results. Share price and investment return

fluctuate and an investor’s shares may be worth more or less than original cost upon sale of the shares.

Current performance may be lower or higher than the performance quoted. Go to www.bny.com/investments

for the fund’s most recent month-end returns.

The fund’s performance shown in the graph

and table does not reflect the deduction of taxes that a shareholder would pay on fund distributions

or the sale of fund shares.

4

DISTRIBUTION

INFORMATION (Unaudited)

The following information regarding the

fund’s distributions is current as of September 30, 2024, the fund’s fiscal year end. The fund’s

returns during the period were sufficient to meet fund distributions.

The

fund’s distribution policy is intended to provide shareholders with stable, but not guaranteed, cash

flow, independent of the amount or timing of income earned or capital gains realized by the fund. The

fund intends to distribute all or substantially all of its net investment income through its regular

monthly distribution and to distribute realized capital gains at least annually. In addition, in any

monthly period, in order to try to maintain a level distribution amount, the fund may pay out more or

less than its net investment income during the period. As a result, distributions sources may include

net investment income, realized gains and return of capital. You should not draw any conclusions about

the fund’s investment performance from the amount of the distribution or from the terms of the level

distribution program. A return of capital is a non-taxable distribution of a portion of a fund’s capital.

A return of capital distribution does not necessarily reflect a fund’s investment performance and should

not be confused with “yield” or “income.”

The amounts and sources

of distributions reported below are for financial reporting purposes and are not being provided for tax

reporting purposes. The actual amounts and character of the distributions for tax reporting purposes

will be reported to shareholders on Form 1099-DIV, which will be sent to shareholders shortly after

calendar year-end. Because distribution source estimates are updated throughout the current fiscal

year based on the fund’s performance, those estimates may differ from both the tax information reported

to you in your fund’s 1099 statement, as well as the ultimate economic sources of distributions over

the life of your investment. The figures in the table below provide the sources of distributions and

may include amounts attributed to realized gains and/or returns of capital.

| | | | | | | | |

Distributions |

| | Current Month

Percentage of Distributions | Fiscal

Year Ended

Per Share Amounts |

| Net Investment Income | Realized Gains | Return of Capital | Total

Distributions | Net

Investment Income | Realized

Gains | Return of Capital |

BNY Mellon Municipal Income, Inc. | 100.00% | .00% | .00% | $.20 | $.20 | $.00 | $.00 |

5

SELECTED

INFORMATION

September

30, 2024 (Unaudited)

| | | | | | | | | | | | | | | |

Market Price per share September 30, 2024 | | $7.31 | | |

Shares

Outstanding September 30, 2024 | | 20,757,267 | | |

NYSE

MKT Ticker Symbol | | DMF | | |

MARKET PRICE (NYSE MKT) |

| | | | Fiscal Year Ended September

30, 2024 | | |

| | Quarter | | Quarter | | Quarter | | Quarter |

| | Ended | | Ended | | Ended | | Ended |

| | December 31, 2023 | | March

31, 2024 | | June 30, 2024 | | September 30, 2024 |

High | $6.55 | | $6.83 | | $7.20 | | $7.49 |

Low | 5.40 | | 6.47 | | 6.58 | | 7.16 |

Close | 6.50 | | 6.83 | | 7.19 | | 7.31 |

PERCENTAGE

GAIN (LOSS) based on change in Market Price† |

October

24, 1988 (commencement of operations) through

September 30, 2024 | 568.08% |

October

1, 2014 through September 30, 2024 | 30.47 |

October

1, 2019 through September 30, 2024 | (4.20) |

October

1, 2023 through September 30, 2024 | 32.73 |

January

1, 2024 through September 30, 2024 | 14.92 |

April

1, 2024 through September 30, 2024 | 8.63 |

July

1, 2024 through September 30, 2024 | 2.47 |

| | | | | |

NET

ASSET VALUE PER SHARE | |

October 24, 1988 (commencement of operations) | $9.26 |

September 30, 2023 | 6.82 |

December

31, 2023 | | | 7.70 |

March

31, 2024 | 7.64 |

June

30, 2024 | 7.66 |

September

30, 2024 | 7.86 |

PERCENTAGE

GAIN (LOSS) based on change in Net Asset Value† | |

October

24, 1988 (commencement of operations) through

September 30, 2024 | 675.63% |

October

1, 2014 through September 30, 2024 | 31.70 |

October

1, 2019 through September 30, 2024 | 2.88 |

October

1, 2023 through September 30, 2024 | 18.63 |

January

1, 2024 through September 30, 2024 | 4.29 |

April

1, 2024 through September 30, 2024 | 4.27 |

July

1, 2024 through September 30, 2024 | 3.40 |

† Total return includes reinvestment of dividends and any capital

gains paid. | |

6

STATEMENT

OF INVESTMENTS

September 30, 2024

| | | | | | | | | | |

| |

Description | Coupon

Rate

(%) | | Maturity

Date | | Principal

Amount

($) | | Value

($) | |

Long-Term

Municipal Investments - 147.8% | | | |

Alabama - 3.4% | | | | | |

Black

Belt Energy Gas District, Revenue Bonds, Refunding (Gas Project) Ser. D1 | | 5.50 | | 2/1/2029 | | 2,320,000 | a | 2,511,156 | |

Jefferson County, Revenue Bonds, Refunding | | 5.25 | | 10/1/2049 | | 1,000,000 | | 1,089,775 | |

Jefferson County, Revenue Bonds, Refunding | | 5.50 | | 10/1/2053 | | 1,800,000 | | 1,983,406 | |

| | 5,584,337 | |

Alaska

- 1.3% | | | | | |

Northern Tobacco Securitization Corp., Revenue Bonds, Refunding,

Ser. A | | 4.00 | | 6/1/2050 | | 2,345,000 | | 2,184,380 | |

Arizona

- 5.6% | | | | | |

Arizona Industrial Development Authority, Revenue Bonds (Sustainable

Bond) (Equitable School Revolving Fund Obligated Group) Ser. A | | 4.00 | | 11/1/2050 | | 1,200,000 | | 1,162,513 | |

Arizona Industrial Development Authority, Revenue Bonds (Sustainable

Bond) (Equitable School Revolving Fund Obligated Group) Ser. A | | 4.00 | | 11/1/2045 | | 1,355,000 | | 1,342,182 | |

Glendale Industrial Development Authority, Revenue Bonds,

Refunding (Sun Health Services Obligated Group) Ser. A | | 5.00 | | 11/15/2054 | | 1,500,000 | | 1,496,781 | |

La Paz County Industrial Development Authority, Revenue Bonds

(Harmony Public Schools) Ser. A | | 5.00 | | 2/15/2046 | | 1,500,000 | b | 1,505,339 | |

7

STATEMENT

OF INVESTMENTS (continued)

| | | | | | | | | | |

| |

Description

| Coupon

Rate

(%) | | Maturity

Date | | Principal

Amount

($) | | Value

($) | |

Long-Term

Municipal Investments - 147.8% (continued) | | | |

Arizona

- 5.6% (continued) | | | | | |

La Paz County Industrial

Development Authority, Revenue Bonds (Harmony Public Schools) Ser. A | | 5.00 | | 2/15/2036 | | 1,100,000 | b | 1,112,091 | |

Salt Verde Financial Corp., Revenue Bonds | | 5.00 | | 12/1/2037 | | 2,190,000 | | 2,450,820 | |

| | 9,069,726 | |

California

- 8.0% | | | | | |

Golden State Tobacco Securitization Corp., Revenue Bonds,

Refunding (Tobacco Settlement Asset) Ser. B | | 5.00 | | 6/1/2051 | | 2,000,000 | | 2,110,689 | |

San Diego County Regional Airport Authority, Revenue Bonds,

Ser. B | | 5.00 | | 7/1/2051 | | 3,750,000 | | 3,956,086 | |

Tender Option Bond

Trust Receipts (Series 2022-XF3024), (San Francisco City & County, Revenue Bonds, Refunding, Ser.

A) Recourse, Underlying Coupon Rate 5.00% | | 9.21 | | 5/1/2044 | | 3,360,000 | b,c,d | 3,486,216 | |

Tender Option Bond Trust Receipts (Series 2023-XM1114), (Long

Beach Finance Authority, Revenue Bonds) Non-recourse, Underlying Coupon Rate 4.00% | | 4.84 | | 8/1/2053 | | 3,600,000 | b,c,d | 3,578,513 | |

| | 13,131,504 | |

Colorado

- 5.8% | | | | | |

Colorado Health Facilities Authority, Revenue Bonds, Refunding

(Covenant Living Communities & Services Obligated Group) Ser. A | | 4.00 | | 12/1/2050 | | 2,000,000 | | 1,833,200 | |

Colorado High Performance Transportation Enterprise, Revenue

Bonds (C-470 Express Lanes System) | | 5.00 | | 12/31/2056 | | 3,000,000 | | 3,001,656 | |

8

| | | | | | | | | | |

| |

Description

| Coupon

Rate

(%) | | Maturity

Date | | Principal

Amount

($) | | Value

($) | |

Long-Term

Municipal Investments - 147.8% (continued) | | | |

Colorado

- 5.8% (continued) | | | | | |

Tender Option Bond

Trust Receipts (Series 2020-XM0829), (Colorado Health Facilities Authority, Revenue Bonds, Refunding

(CommonSpirit Health Obligated Group) Ser. A1) Recourse, Underlying Coupon Rate 4.00% | | 8.13 | | 8/1/2044 | | 1,645,000 | b,c,d | 1,926,255 | |

Tender Option Bond Trust Receipts (Series 2023-XM1124), (Colorado

Health Facilities Authority, Revenue Bonds (Adventist Health System/Sunbelt Obligated Group) Ser. A)

Recourse, Underlying Coupon Rate 4.00% | | 5.23 | | 11/15/2048 | | 2,770,000 | b,c,d | 2,711,083 | |

| | 9,472,194 | |

Delaware

- .6% | | | | | |

Delaware Economic Development Authority, Revenue Bonds (ACTS

Retirement-Life Communities Obligated Group) Ser. B | | 5.25 | | 11/15/2053 | | 1,000,000 | | 1,047,320 | |

Florida - 11.0% | | | | | |

Atlantic

Beach, Revenue Bonds (Fleet Landing Project) Ser. A | | 5.00 | | 11/15/2053 | | 1,670,000 | | 1,699,128 | |

Collier County Industrial Development Authority, Revenue

Bonds (NCH Healthcare System Project) (Insured; Assured Guaranty Municipal Corp.) Ser. A | | 5.00 | | 10/1/2054 | | 1,480,000 | | 1,600,456 | |

Florida Housing Finance

Corp., Revenue Bonds (Insured; GNMA, FNMA, FHLMC) Ser. 1 | | 4.40 | | 7/1/2044 | | 1,090,000 | | 1,100,791 | |

Greater Orlando Aviation Authority, Revenue Bonds, Ser. A | | 4.00 | | 10/1/2049 | | 1,380,000 | | 1,343,843 | |

9

STATEMENT

OF INVESTMENTS (continued)

| | | | | | | | | | |

| |

Description

| Coupon

Rate

(%) | | Maturity

Date | | Principal

Amount

($) | | Value

($) | |

Long-Term

Municipal Investments - 147.8% (continued) | | | |

Florida

- 11.0% (continued) | | | | | |

Hillsborough County

Port District, Revenue Bonds (Tampa Port Authority Project) Ser. B | | 5.00 | | 6/1/2046 | | 1,450,000 | | 1,491,160 | |

Palm Beach County Health Facilities Authority, Revenue Bonds,

Refunding (Lifespace Communities Obligated Group) Ser. C | | 7.63 | | 5/15/2058 | | 1,000,000 | | 1,145,660 | |

Tender Option Bond Trust Receipts (Series 2023-XM1122), (Miami-Dade

FL County Water & Sewer System, Revenue Bonds, Refunding, Ser. B) Recourse, Underlying Coupon Rate

4.00% | | 4.83 | | 10/1/2049 | | 9,750,000 | b,c,d | 9,564,850 | |

| | 17,945,888 | |

Georgia - 5.9% | | | | | |

Georgia

Municipal Electric Authority, Revenue Bonds (Plant Vogtle Units 3&4 Project) Ser. A | | 5.00 | | 7/1/2052 | | 1,250,000 | | 1,323,817 | |

Main Street Natural

Gas, Revenue Bonds, Ser. A | | 5.00 | | 9/1/2031 | | 1,550,000 | a | 1,695,326 | |

Tender Option Bond Trust Receipts (Series 2020-XM0825), (Brookhaven

Development Authority, Revenue Bonds (Children's Healthcare of Atlanta) Ser. A) Recourse, Underlying

Coupon Rate 4.00% | | 6.52 | | 7/1/2044 | | 2,660,000 | b,c,d | 2,870,759 | |

Tender Option Bond Trust Receipts (Series 2023-XF3183), (Municipal

Electric Authority of Georgia, Revenue Bonds (Plant Vogtle Units 3 & 4 Project) Ser. A) Recourse,

Underlying Coupon Rate 5.00% | | 8.87 | | 1/1/2059 | | 1,270,000 | b,c,d | 1,293,717 | |

10

| | | | | | | | | | |

| |

Description

| Coupon

Rate

(%) | | Maturity

Date | | Principal

Amount

($) | | Value

($) | |

Long-Term

Municipal Investments - 147.8% (continued) | | | |

Georgia

- 5.9% (continued) | | | | | |

The Atlanta Development

Authority, Revenue Bonds, Ser. A1 | | 5.25 | | 7/1/2040 | | 1,500,000 | | 1,518,711 | |

The Burke County Development Authority, Revenue Bonds, Refunding

(Oglethorpe Power Corp.) Ser. D | | 4.13 | | 11/1/2045 | | 1,000,000 | | 970,863 | |

| | 9,673,193 | |

Hawaii

- .8% | | | | | |

Hawaii Airports System, Revenue Bonds, Ser. A | | 5.00 | | 7/1/2047 | | 1,250,000 | | 1,325,720 | |

Illinois

- 13.0% | | | | | |

Chicago II, GO, Refunding, Ser. A | | 6.00 | | 1/1/2038 | | 2,000,000 | | 2,091,129 | |

Chicago II, GO, Ser. A | | 5.00 | | 1/1/2044 | | 1,000,000 | | 1,030,672 | |

Chicago II Wastewater Transmission, Revenue Bonds, Refunding,

Ser. C | | 5.00 | | 1/1/2039 | | 1,100,000 | | 1,103,299 | |

Chicago Midway International

Airport, Revenue Bonds, Refunding, Ser. C | | 5.00 | | 1/1/2040 | | 1,000,000 | | 1,073,257 | |

Chicago O'Hare International Airport, Revenue Bonds, Ser.

A | | 5.50 | | 1/1/2055 | | 1,500,000 | | 1,636,005 | |

Chicago Park District, GO,

Refunding, Ser. A | | 5.00 | | 1/1/2045 | | 1,000,000 | | 1,076,274 | |

Illinois, GO, Refunding,

Ser. A | | 5.00 | | 10/1/2029 | | 1,000,000 | | 1,080,227 | |

Illinois, GO, Ser.

A | | 5.00 | | 5/1/2038 | | 1,250,000 | | 1,302,971 | |

Illinois, GO, Ser.

D | | 5.00 | | 11/1/2028 | | 1,000,000 | | 1,062,555 | |

Illinois Finance Authority, Revenue

Bonds, Refunding (Rosalind Franklin University of Medicine & Science) | | 5.00 | | 8/1/2047 | | 1,350,000 | | 1,366,988 | |

Metropolitan Pier & Exposition Authority, Revenue Bonds

(McCormick Place Expansion Project) | | 5.00 | | 6/15/2057 | | 2,500,000 | | 2,552,210 | |

11

STATEMENT

OF INVESTMENTS (continued)

| | | | | | | | | | |

| |

Description

| Coupon

Rate

(%) | | Maturity

Date | | Principal

Amount

($) | | Value

($) | |

Long-Term

Municipal Investments - 147.8% (continued) | | | |

Illinois

- 13.0% (continued) | | | | | |

Metropolitan Pier &

Exposition Authority, Revenue Bonds (McCormick Place Expansion Project) (Insured; National Public Finance

Guarantee Corp.) Ser. A | | 0.00 | | 12/15/2036 | | 2,500,000 | e | 1,591,083 | |

Sales Tax Securitization Corp., Revenue Bonds, Refunding,

Ser. A | | 4.00 | | 1/1/2039 | | 1,500,000 | | 1,518,060 | |

Tender Option Bond

Trust Receipts (Series 2023-XF1623), (Regional Transportation Authority Illinois, Revenue Bonds, Ser.

B) Non-Recourse, Underlying Coupon Rate 4.00% | | 4.46 | | 6/1/2048 | | 1,125,000 | b,c,d | 1,089,120 | |

Tender Option Bond Trust Receipts (Series 2024-XF3244), (Chicago

O'Hare International Airport, Revenue Bonds, Refunding) Recourse, Underlying Coupon Rate 5.50% | | 10.83 | | 1/1/2059 | | 1,450,000 | b,c,d | 1,603,364 | |

| | 21,177,214 | |

Indiana - .7% | | | | | |

Indianapolis

Local Public Improvement Bond Bank, Revenue Bonds (Insured; Build America Mutual) Ser. F1 | | 5.25 | | 3/1/2067 | | 1,000,000 | | 1,080,866 | |

Iowa

- 1.1% | | | | | |

Iowa Finance Authority, Revenue Bonds, Refunding (Iowa Fertilizer

Co. Project) | | 5.00 | | 12/1/2032 | | 1,500,000 | f | 1,758,385 | |

Kentucky

- 2.1% | | | | | |

Kentucky Public Energy Authority, Revenue Bonds, Ser. A | | 5.00 | | 7/1/2030 | | 1,000,000 | a | 1,076,230 | |

Kentucky Public Energy Authority, Revenue Bonds, Ser. A1 | | 4.00 | | 8/1/2030 | | 2,320,000 | a | 2,382,883 | |

| | 3,459,113 | |

12

| | | | | | | | | | |

| |

Description

| Coupon

Rate

(%) | | Maturity

Date | | Principal

Amount

($) | | Value

($) | |

Long-Term

Municipal Investments - 147.8% (continued) | | | |

Louisiana

- 5.4% | | | | | |

Louisiana Public Facilities Authority, Revenue Bonds (Calcasieu

Bridge Partners) | | 5.75 | | 9/1/2064 | | 1,165,000 | | 1,296,685 | |

New Orleans Aviation

Board, Revenue Bonds (General Airport-N Terminal Project) Ser. A | | 5.00 | | 1/1/2048 | | 1,000,000 | | 1,020,943 | |

Tender Option Bond Trust Receipts (Series 2018-XF2584), (Louisiana

Public Facilities Authority, Revenue Bonds (Franciscan Missionaries of Our Lady Health System Project))

Non-recourse, Underlying Coupon Rate 5.00% | | 8.78 | | 7/1/2047 | | 6,320,000 | b,c,d | 6,468,795 | |

| | 8,786,423 | |

Maryland

- 1.9% | | | | | |

Maryland Economic Development Corp., Revenue Bonds (College

Park Leonardtown Project) (Insured; Assured Guaranty Municipal Corp.) | | 5.25 | | 7/1/2064 | | 500,000 | | 538,382 | |

Maryland Economic Development Corp., Revenue Bonds (Sustainable

Bond) (Purple Line Transit Partners) Ser. B | | 5.25 | | 6/30/2055 | | 1,000,000 | | 1,048,295 | |

Maryland Health & Higher Educational Facilities Authority, Revenue

Bonds (Adventist Healthcare Obligated Group) Ser. A | | 5.50 | | 1/1/2046 | | 1,500,000 | | 1,527,951 | |

| | 3,114,628 | |

13

STATEMENT

OF INVESTMENTS (continued)

| | | | | | | | | | |

| |

Description

| Coupon

Rate

(%) | | Maturity

Date | | Principal

Amount

($) | | Value

($) | |

Long-Term

Municipal Investments - 147.8% (continued) | | | |

Massachusetts

- 1.7% | | | | | |

Massachusetts Development Finance Agency, Revenue Bonds,

Refunding (UMass Memorial Health Care Obligated Group) | | 5.00 | | 7/1/2046 | | 1,835,000 | | 1,854,926 | |

Massachusetts Development Finance Agency, Revenue Bonds,

Ser. T | | 4.00 | | 3/1/2054 | | 1,000,000 | | 979,376 | |

| | 2,834,302 | |

Michigan

- 3.6% | | | | | |

Detroit Downtown Development Authority, Tax Allocation Bonds,

Refunding (Catalyst Development Project) | | 5.00 | | 7/1/2048 | | 1,250,000 | | 1,332,928 | |

Michigan Finance Authority, Revenue Bonds (Sustainable Bond)

(Henry Ford) | | 4.13 | | 2/29/2044 | | 650,000 | | 646,498 | |

Michigan Finance Authority, Revenue

Bonds, Refunding (Beaumont-Spectrum) | | 4.00 | | 4/15/2042 | | 1,000,000 | | 1,008,609 | |

Michigan Finance Authority, Revenue Bonds, Refunding, Ser.

A | | 4.00 | | 12/1/2049 | | 2,000,000 | | 1,919,752 | |

Pontiac School District, GO

(Insured; Qualified School Board Loan Fund) | | 4.00 | | 5/1/2045 | | 1,000,000 | | 1,000,388 | |

| | 5,908,175 | |

Minnesota

- 1.3% | | | | | |

Duluth Economic Development Authority, Revenue Bonds, Refunding

(Essentia Health Obligated Group) Ser. A | | 5.00 | | 2/15/2058 | | 1,000,000 | | 1,018,767 | |

Minnesota Agricultural & Economic Development Board, Revenue

Bonds (HealthPartners Obligated Group) | | 5.25 | | 1/1/2054 | | 1,000,000 | | 1,103,274 | |

| | 2,122,041 | |

14

| | | | | | | | | | |

| |

Description

| Coupon

Rate

(%) | | Maturity

Date | | Principal

Amount

($) | | Value

($) | |

Long-Term

Municipal Investments - 147.8% (continued) | | | |

Missouri

- 3.1% | | | | | |

Tender Option Bond Trust Receipts (Series 2023-XM1116), (Jackson

County Missouri Special Obligation, Revenue Bonds, Refunding, Ser. A) Non-Recourse, Underlying Coupon

Rate 4.25% | | 3.23 | | 12/1/2053 | | 3,000,000 | b,c,d | 2,963,159 | |

The Missouri Health & Educational Facilities Authority, Revenue

Bonds (Lutheran Senior Services Projects) Ser. A | | 5.00 | | 2/1/2042 | | 2,000,000 | | 2,064,880 | |

| | 5,028,039 | |

Nebraska

- 1.4% | | | | | |

Douglas County Hospital Authority No. 2, Revenue Bonds (Children's

Hospital Obligated Group) | | 5.00 | | 11/15/2036 | | 1,000,000 | | 1,044,767 | |

Omaha Public Power

District, Revenue Bonds, Ser. A | | 4.00 | | 2/1/2051 | | 1,250,000 | | 1,219,026 | |

| | 2,263,793 | |

Nevada

- 2.3% | | | | | |

Clark County School District, GO (Insured; Assured Guaranty

Municipal Corp.) Ser. A | | 4.25 | | 6/15/2041 | | 1,340,000 | | 1,397,036 | |

Reno, Revenue Bonds,

Refunding (Insured; Assured Guaranty Municipal Corp.) | | 4.00 | | 6/1/2058 | | 1,250,000 | | 1,180,683 | |

Reno, Revenue Bonds, Refunding (Insured; Assured Guaranty

Municipal Corp.) | | 4.13 | | 6/1/2058 | | 1,250,000 | | 1,225,719 | |

| | 3,803,438 | |

15

STATEMENT

OF INVESTMENTS (continued)

| | | | | | | | | | |

| |

Description

| Coupon

Rate

(%) | | Maturity

Date | | Principal

Amount

($) | | Value

($) | |

Long-Term

Municipal Investments - 147.8% (continued) | | | |

New Hampshire

- 1.3% | | | | | |

New Hampshire Business Finance Authority, Revenue Bonds (University

of Nevada Reno Project) (Insured; Build America Mutual) Ser. A | | 5.25 | | 6/1/2051 | | 1,000,000 | | 1,096,882 | |

New Hampshire Business Finance Authority, Revenue Bonds,

Refunding (Springpoint Senior Living Obligated Group) | | 4.00 | | 1/1/2041 | | 1,000,000 | | 941,645 | |

| | 2,038,527 | |

New

Jersey - 6.3% | | | | | |

New Jersey Health Care Facilities Financing Authority, Revenue

Bonds (RWJ Barnabas Health Obligated Group) | | 4.00 | | 7/1/2051 | | 855,000 | | 847,049 | |

New Jersey Transportation Trust Fund Authority, Revenue Bonds | | 5.00 | | 6/15/2044 | | 1,250,000 | | 1,370,928 | |

New Jersey Transportation

Trust Fund Authority, Revenue Bonds | | 5.25 | | 6/15/2043 | | 2,000,000 | | 2,137,511 | |

New Jersey Transportation Trust Fund Authority, Revenue Bonds,

Ser. AA | | 5.25 | | 6/15/2033 | | 1,000,000 | | 1,014,790 | |

South Jersey Port Corp., Revenue

Bonds, Ser. B | | 5.00 | | 1/1/2048 | | 1,000,000 | | 1,022,927 | |

Tobacco Settlement

Financing Corp., Revenue Bonds, Refunding, Ser. A | | 5.00 | | 6/1/2046 | | 3,860,000 | | 3,965,031 | |

| | 10,358,236 | |

New

Mexico - .6% | | | | | |

New Mexico Mortgage Finance Authority, Revenue Bonds (Insured;

GNMA, FNMA, FHLMC) Ser. E | | 4.70 | | 9/1/2054 | | 1,000,000 | | 1,019,219 | |

New

York - 8.2% | | | | | |

New York Convention Center Development Corp., Revenue Bonds

(Hotel Unit Fee) (Insured; Assured Guaranty Municipal Corp.) Ser. B | | 0.00 | | 11/15/2052 | | 6,400,000 | e | 1,800,073 | |

16

| | | | | | | | | | |

| |

Description

| Coupon

Rate

(%) | | Maturity

Date | | Principal

Amount

($) | | Value

($) | |

Long-Term

Municipal Investments - 147.8% (continued) | | | |

New York

- 8.2% (continued) | | | | | |

New York State Housing

Finance Agency, Revenue Bonds (Sustainable Bond) Ser. B1 | | 4.70 | | 11/1/2059 | | 1,000,000 | | 1,014,394 | |

New York Transportation Development Corp., Revenue Bonds

(JFK International Airport Terminal) | | 5.00 | | 12/1/2040 | | 1,000,000 | | 1,058,165 | |

New York Transportation Development Corp., Revenue Bonds

(LaGuardia Airport Terminal B Redevelopment Project) Ser. A | | 5.00 | | 7/1/2046 | | 1,500,000 | | 1,500,022 | |

New York Transportation Development Corp., Revenue Bonds

(Sustainable Bond) (JFK International Airport Terminal One Project) (Insured; Assured Guaranty Municipal

Corp.) | | 5.13 | | 6/30/2060 | | 1,000,000 | | 1,045,214 | |

Tender Option Bond

Trust Receipts (Series 2022-XM1004), (Metropolitan Transportation Authority, Revenue Bonds, Refunding

(Sustainable Bond) (Insured; Assured Guaranty Municipal Corp.) Ser. C) Non-Recourse, Underlying Coupon

Rate 4.00% | | 4.31 | | 11/15/2047 | | 2,000,000 | b,c,d | 1,971,239 | |

Tender Option Bond Trust Receipts (Series 2024-XM1174), (New

York State Transportation Development Corp., Revenue Bonds (Sustainable Bond) (JFK International Airport

Terminal one Project) (Insured; Assured Guaranty Municipal Corp.)) Recourse, Underlying Coupon Rate 5.25% | | 9.85 | | 6/30/2060 | | 1,360,000 | b,c,d | 1,451,867 | |

17

STATEMENT

OF INVESTMENTS (continued)

| | | | | | | | | | |

| |

Description

| Coupon

Rate

(%) | | Maturity

Date | | Principal

Amount

($) | | Value

($) | |

Long-Term

Municipal Investments - 147.8% (continued) | | | |

New York

- 8.2% (continued) | | | | | |

Tender Option Bond

Trust Receipts (Series 2024-XM1181), (Triborough New York Bridge & Tunnel Authority, Revenue Bonds,

Ser. A1) Non-Recourse, Underlying Coupon Rate 4.13% | | 4.13 | | 5/15/2064 | | 1,500,000 | b,c,d | 1,471,370 | |

Triborough Bridge & Tunnel Authority, Revenue Bonds,

Ser. C1A | | 4.00 | | 5/15/2046 | | 2,000,000 | | 2,006,915 | |

| | 13,319,259 | |

North

Carolina - 1.3% | | | | | |

North Carolina Medical Care Commission, Revenue Bonds (Carolina

Meadows Obligated Group) | | 5.25 | | 12/1/2054 | | 2,000,000 | | 2,170,477 | |

Ohio

- 3.7% | | | | | |

Cuyahoga County, Revenue Bonds, Refunding (The MetroHealth

System) | | 5.00 | | 2/15/2057 | | 1,155,000 | | 1,167,187 | |

Cuyahoga County, Revenue

Bonds, Refunding (The MetroHealth System) | | 5.00 | | 2/15/2052 | | 1,000,000 | | 1,012,161 | |

Port of Greater Cincinnati Development Authority, Revenue

Bonds, Refunding (Duke Energy Co.) (Insured; Assured Guaranty Municipal Corp.) Ser. B | | 4.38 | | 12/1/2058 | | 750,000 | | 757,715 | |

Tender Option Bond Trust Receipts (Series 2024-XF1711), (University

of Cincinnati Ohio Receipt, Revenue Bonds, Ser. A) Non-Recourse, Underlying Coupon Rate 5.00% | | 9.31 | | 6/1/2049 | | 2,800,000 | b,c,d | 3,056,500 | |

| | 5,993,563 | |

18

| | | | | | | | | | |

| |

Description

| Coupon

Rate

(%) | | Maturity

Date | | Principal

Amount

($) | | Value

($) | |

Long-Term

Municipal Investments - 147.8% (continued) | | | |

Oklahoma

- 2.2% | | | | | |

Tender Option Bond Trust Receipts (Series 2024-XM1163), (Oklahoma

City Water Utilities Trust, Revenue Bonds, Refunding) Non-Recourse, Underlying Coupon Rate 5.25% | | 10.17 | | 7/1/2064 | | 3,200,000 | b,c,d | 3,549,913 | |

Oregon

- .5% | | | | | |

Salem Hospital Facility Authority, Revenue Bonds, Refunding

(Capital Manor Project) | | 4.00 | | 5/15/2057 | | 1,000,000 | | 821,882 | |

Pennsylvania

- 8.4% | | | | | |

Allentown School District, GO, Refunding (Insured; Build

America Mutual) Ser. B | | 5.00 | | 2/1/2033 | | 1,255,000 | | 1,340,142 | |

Clairton Municipal

Authority, Revenue Bonds, Refunding, Ser. B | | 4.38 | | 12/1/2042 | | 1,000,000 | | 1,022,077 | |

Montgomery County Industrial Development Authority, Revenue

Bonds, Refunding (ACTS Retirement-Life Communities Obligated Group) | | 5.00 | | 11/15/2036 | | 1,000,000 | | 1,027,494 | |

Pennsylvania Economic Development Financing Authority, Revenue

Bonds (The Penndot Major Bridges) | | 6.00 | | 6/30/2061 | | 1,000,000 | | 1,130,962 | |

Pennsylvania Turnpike Commission, Revenue Bonds, Ser. A | | 4.00 | | 12/1/2050 | | 1,000,000 | | 971,473 | |

Pennsylvania Turnpike

Commission, Revenue Bonds, Ser. A1 | | 5.00 | | 12/1/2046 | | 1,000,000 | | 1,019,329 | |

Tender Option Bond Trust Receipts (Series 2022-XF1525), (Pennsylvania

Economic Development Financing Authority UPMC, Revenue Bonds, Ser. A) Recourse, Underlying Coupon Rate

4.00% | | 4.23 | | 5/15/2053 | | 1,700,000 | b,c,d | 1,628,878 | |

19

STATEMENT

OF INVESTMENTS (continued)

| | | | | | | | | | |

| |

Description

| Coupon

Rate

(%) | | Maturity

Date | | Principal

Amount

($) | | Value

($) | |

Long-Term

Municipal Investments - 147.8% (continued) | | | |

Pennsylvania

- 8.4% (continued) | | | | | |

Tender Option Bond

Trust Receipts (Series 2023-XM1133), (Philadelphia Water & Wastewater, Revenue Bonds, Refunding

(Insured; Assured Guaranty Municipal Corp.) Ser. B) Non-Recourse, Underlying Coupon Rate 5.50% | | 10.93 | | 9/1/2053 | | 2,400,000 | b,c,d | 2,740,456 | |

Tender Option Bond Trust Receipts (Series 2024-XF1750), (Philadelphia

Gas Works, Revenue Bonds, Refunding (Insured; Assured Guaranty Corp.) Ser. A) Non-Recourse, Underlying

Coupon Rate 5.25% | | 9.97 | | 8/1/2054 | | 1,400,000 | b,c,d | 1,549,432 | |

The Philadelphia School District, GO (Insured; State Aid

Withholding) Ser. A | | 4.00 | | 9/1/2037 | | 1,250,000 | | 1,281,131 | |

| | 13,711,374 | |

Rhode

Island - 3.1% | | | | | |

Rhode Island Health & Educational Building Corp., Revenue

Bonds (Lifespan Obligated Group) | | 5.25 | | 5/15/2054 | | 1,000,000 | | 1,081,249 | |

Tender Option Bond Trust Receipts (Series 2023-XM1117), (Rhode

Island Infrastructure Bank State Revolving Fund, Revenue Bonds, Ser. A) Non-recourse, Underlying Coupon

Rate 4.25% | | 3.81 | | 10/1/2053 | | 4,000,000 | b,c,d | 4,048,161 | |

| | 5,129,410 | |

South Carolina - 7.1% | | | | | |

South

Carolina Jobs-Economic Development Authority, Revenue Bonds, Refunding (Bon Secours Mercy Health) | | 4.00 | | 12/1/2044 | | 1,000,000 | | 999,827 | |

20

| | | | | | | | | | |

| |

Description

| Coupon

Rate

(%) | | Maturity

Date | | Principal

Amount

($) | | Value

($) | |

Long-Term

Municipal Investments - 147.8% (continued) | | | |

South

Carolina - 7.1% (continued) | | | | | |

South

Carolina Public Service Authority, Revenue Bonds, Refunding (Santee Cooper) Ser. A | | 4.00 | | 12/1/2055 | | 1,000,000 | | 949,780 | |

Tender Option Bond Trust Receipts (Series 2024-XM1175), (South

Carolina Public Service Authority,Revenue Bonds, Refunding (Insured; Assured Guaranty Municipal Corp.)

Ser. B) Non-Recourse, Underlying Coupon Rate 5.00% | | 7.57 | | 12/1/2054 | | 4,800,000 | b,c,d | 5,176,670 | |

Tobacco Settlement Revenue Management Authority, Revenue

Bonds, Ser. B | | 6.38 | | 5/15/2030 | | 3,750,000 | | 4,382,416 | |

| | 11,508,693 | |

South

Dakota - 1.3% | | | | | |

Tender Option Bond Trust Receipts (Series 2022-XF1409), (South

Dakota Heath & Educational Facilities

Authority, Revenue Bonds,

Refunding (Avera Health Obligated Group)) Non-Recourse, Underlying Coupon Rate 5.00% | | 9.32 | | 7/1/2046 | | 2,000,000 | b,c,d | 2,038,914 | |

Texas

- 14.7% | | | | | |

Clifton Higher Education Finance Corp., Revenue Bonds (IDEA

Public Schools) Ser. A | | 4.00 | | 8/15/2051 | | 1,100,000 | | 1,027,726 | |

Clifton Higher Education

Finance Corp., Revenue Bonds (Uplift Education) Ser. A | | 4.25 | | 12/1/2034 | | 1,000,000 | | 1,000,114 | |

21

STATEMENT

OF INVESTMENTS (continued)

| | | | | | | | | | |

| |

Description

| Coupon

Rate

(%) | | Maturity

Date | | Principal

Amount

($) | | Value

($) | |

Long-Term

Municipal Investments - 147.8% (continued) | | | |

Texas

- 14.7% (continued) | | | | | |

Clifton Higher Education

Finance Corp., Revenue Bonds, Refunding (International Leadership of Texas) (Insured; Permanent School

Fund Guarantee Program) Ser. A | | 4.25 | | 8/15/2053 | | 1,000,000 | | 1,023,119 | |

Dallas Independent

School District, GO, Refunding (Insured; Permanent School Fund Guarantee Program) | | 4.00 | | 2/15/2054 | | 1,000,000 | | 983,504 | |

Harris County-Houston Sports Authority, Revenue Bonds, Refunding

(Insured; Assured Guaranty Municipal Corp.) Ser. A | | 0.00 | | 11/15/2052 | | 4,000,000 | e | 1,035,326 | |

Houston Airport System, Revenue Bonds, Refunding (Insured;

Assured Guaranty Municipal Corp.) Ser. A | | 4.50 | | 7/1/2053 | | 1,000,000 | | 1,017,117 | |

Houston Airport System, Revenue Bonds, Refunding, Ser. A | | 4.00 | | 7/1/2047 | | 1,560,000 | | 1,512,380 | |

Lamar Consolidated

Independent School District, GO | | 4.00 | | 2/15/2053 | | 1,000,000 | | 970,248 | |

Midland Independent School District, GO (Insured; Permanent

School Fund Guarantee Program) | | 5.00 | | 2/15/2050 | | 1,000,000 | | 1,045,725 | |

New Hope Cultural Education

Facilities Finance Corp., Revenue Bonds, Refunding (Westminster Project) | | 4.00 | | 11/1/2055 | | 1,650,000 | | 1,507,438 | |

North Texas Tollway Authority, Revenue Bonds, Refunding,

Ser. A | | 4.00 | | 1/2/2038 | | 1,000,000 | | 1,015,982 | |

San Antonio Education

Facilities Corp., Revenue Bonds, Refunding (University of the Incarnate Word) | | 4.00 | | 4/1/2046 | | 1,675,000 | | 1,452,895 | |

22

| | | | | | | | | | |

| |

Description

| Coupon

Rate

(%) | | Maturity

Date | | Principal

Amount

($) | | Value

($) | |

Long-Term

Municipal Investments - 147.8% (continued) | | | |

Texas

- 14.7% (continued) | | | | | |

Tender Option Bond

Trust Receipts (Series 2023-XM1125), (Medina Valley Independent School District, GO (Insured; Permanent

School Fund Guarantee Program)) Non-recourse, Underlying Coupon Rate 4.00% | | 3.18 | | 2/15/2053 | | 3,000,000 | b,c,d | 2,925,230 | |

Tender Option Bond Trust Receipts (Series 2024-XM1164), (Texas

University System, Revenue Bonds, Refunding) Non-Recourse, Underlying Coupon Rate 5.25% | | 3.18 | | 3/15/2054 | | 2,800,000 | b,c,d | 3,096,122 | |

Texas Municipal Gas Acquisition & Supply Corp. IV, Revenue

Bonds, Ser. B | | 5.50 | | 1/1/2034 | | 1,000,000 | a | 1,137,968 | |

Texas Private Activity Bond Surface Transportation Corp., Revenue

Bonds (Blueridge Transportation Group) | | 5.00 | | 12/31/2055 | | 1,000,000 | | 1,000,200 | |

Texas Private Activity Bond Surface Transportation Corp., Revenue

Bonds (Blueridge Transportation Group) | | 5.00 | | 12/31/2050 | | 1,200,000 | | 1,200,240 | |

Waxahachie Independent School District, GO (Insured; Permanent

School Fund Guarantee Program) | | 4.25 | | 2/15/2053 | | 1,000,000 | | 1,007,615 | |

| | 23,958,949 | |

Utah

- 1.6% | | | | | |

Salt Lake City, Revenue Bonds, Ser. A | | 5.00 | | 7/1/2048 | | 1,000,000 | | 1,026,926 | |

Utah Infrastructure Agency, Revenue Bonds, Refunding, Ser.

A | | 5.00 | | 10/15/2037 | | 1,500,000 | | 1,540,801 | |

| | 2,567,727 | |

23

STATEMENT

OF INVESTMENTS (continued)

| | | | | | | | | | |

| |

Description

| Coupon

Rate

(%) | | Maturity

Date | | Principal

Amount

($) | | Value

($) | |

Long-Term

Municipal Investments - 147.8% (continued) | | | |

Virginia

- 3.0% | | | | | |

Tender Option Bond Trust Receipts (Series 2024-XM1176), (Virginia

State Housing Development Authority, Revenue Bonds, Ser. A) Recourse, Underlying Coupon Rate 4.80% | | 8.50 | | 9/1/2059 | | 1,800,000 | b,c,d | 1,848,060 | |

Virginia Small Business Financing Authority, Revenue Bonds

(Transform 66 P3 Project) | | 5.00 | | 12/31/2052 | | 2,000,000 | | 2,032,670 | |

Williamsburg Economic

Development Authority, Revenue Bonds (William & Mary Project) (Insured; Assured Guaranty Municipal

Corp.) Ser. A | | 4.13 | | 7/1/2058 | | 1,000,000 | | 1,002,244 | |

| | 4,882,974 | |

Washington

- 1.3% | | | | | |

Tender Option Bond Trust Receipts (Series 2024--XF1730), (Port

of Seattle Washington, Revenue Bonds, Refunding, Ser. B) Non-Recourse, Underlying Coupon Rate 5.25% | | 9.98 | | 7/1/2049 | | 1,000,000 | b,c,d | 1,083,811 | |

Washington Housing Finance Commission, Revenue Bonds, Refunding

(Seattle Academy of Arts & Sciences) | | 6.38 | | 7/1/2063 | | 1,000,000 | b | 1,111,069 | |

| | 2,194,880 | |

Wisconsin

- 3.2% | | | | | |

Public Finance Authority, Revenue Bonds (EMU Campus Living)

(Insured; Build America Mutual) Ser. A1 | | 5.50 | | 7/1/2052 | | 1,000,000 | | 1,095,432 | |

Public Finance Authority, Revenue Bonds (EMU Campus Living)

(Insured; Build America Mutual) Ser. A1 | | 5.63 | | 7/1/2055 | | 1,000,000 | | 1,104,254 | |

24

| | | | | | | | | | |

| |

Description

| Coupon

Rate

(%) | | Maturity

Date | | Principal

Amount

($) | | Value

($) | |

Long-Term

Municipal Investments - 147.8% (continued) | | | |

Wisconsin

- 3.2% (continued) | | | | | |

Public Finance Authority, Revenue

Bonds, Ser. 1 | | 5.75 | | 7/1/2062 | | 1,717,549 | | 1,835,021 | |

Wisconsin Health &

Educational Facilities Authority, Revenue Bonds (Bellin Memorial Hospital Obligated Group) | | 5.50 | | 12/1/2052 | | 1,000,000 | | 1,120,179 | |

| | 5,154,886 | |

Total Investments (cost $232,095,105) | | 147.8% | 241,189,562 | |

Liabilities, Less Cash and Receivables | | (47.8%) | (78,008,018) | |

Net Assets Applicable

to Common Stockholders | | 100.0% | 163,181,544 | |

a These securities have a put feature; the date shown represents

the put date and the bond holder can take a specific action to retain the bond after the put date.

b Security

exempt from registration pursuant to Rule 144A under the Securities Act of 1933. These securities may

be resold in transactions exempt from registration, normally to qualified institutional buyers. At September

30, 2024, these securities were valued at $78,920,953 or 48.36% of net assets.

c The Variable Rate is determined by the Remarketing Agent in

its sole discretion based on prevailing market conditions and may, but need not, be established by reference

to one or more financial indices.

d Collateral for floating rate borrowings. The coupon rate given

represents the current interest rate for the inverse floating rate security.

e Security issued with a zero coupon. Income is recognized through

the accretion of discount.

f These

securities are prerefunded; the date shown represents the prerefunded date. Bonds which are prerefunded

are collateralized by U.S. Government securities which are held in escrow and are used to pay principal

and interest on the municipal issue and to retire the bonds in full at the earliest refunding date.

See notes to financial statements.

25

| | | | |

| |

Summary

of Abbreviations (Unaudited) |

| |

ABAG | Association

of Bay Area Governments | AGC | ACE Guaranty Corporation |

AGIC | Asset Guaranty Insurance Company | AMBAC | American Municipal Bond Assurance Corporation |

BAN | Bond Anticipation Notes | BSBY | Bloomberg

Short-Term Bank Yield Index |

CIFG | CDC

Ixis Financial Guaranty | COP | Certificate of Participation |

CP | Commercial Paper | DRIVERS | Derivative

Inverse Tax-Exempt Receipts |

EFFR | Effective

Federal Funds Rate | FGIC | Financial Guaranty Insurance Company |

FHA | Federal Housing Administration | FHLB | Federal Home Loan Bank |

FHLMC | Federal Home Loan Mortgage Corporation | FNMA | Federal National Mortgage Association |

GAN | Grant Anticipation Notes | GIC | Guaranteed

Investment Contract |

GNMA | Government National Mortgage Association | GO | General Obligation |

IDC | Industrial

Development Corporation | LOC | Letter of Credit |

LR | Lease

Revenue | NAN | Note Anticipation Notes |

MFHR | Multi-Family Housing Revenue | MFMR | Multi-Family Mortgage Revenue |

MUNIPSA | Securities Industry and Financial Markets

Association Municipal Swap Index Yield | OBFR | Overnight

Bank Funding Rate |

PILOT | Payment in Lieu of Taxes | PRIME | Prime

Lending Rate |

PUTTERS | Puttable Tax-Exempt Receipts | RAC | Revenue Anticipation Certificates |

RAN | Revenue Anticipation Notes | RIB | Residual Interest Bonds |

SFHR | Single Family Housing Revenue | SFMR | Single Family Mortgage Revenue |

SOFR | Secured Overnight Financing Rate | TAN | Tax Anticipation Notes |

TRAN | Tax and Revenue Anticipation Notes | TSFR | Term Secured Overnight

Financing Rate |

USBMMY | U.S. Treasury Bill Money Market Yield | U.S. T-BILL | U.S. Treasury Bill |

XLCA | XL Capital Assurance | VMTP Shares | Variable Rate MuniFund Term Preferred Shares |

| | | | |

See notes to financial statements.

26

STATEMENT

OF ASSETS AND LIABILITIES

September 30, 2024

| | | | | | | |

| | | | | | |

| | | Cost | | Value | |

Assets ($): | | | | |

Investments in securities—See Statement

of Investments | 232,095,105

| | 241,189,562 | |

Cash | | | | | 787,261 | |

Interest

receivable | | 3,108,429 | |

Prepaid expenses | | | | | 7,877 | |

| | | | |

245,093,129 | |

Liabilities ($): | | | | |

Due to BNY Mellon Investment Adviser, Inc.

and affiliates—Note 2(b) | | 116,808 | |

Payable for inverse floater notes issued—Note

3 | | 50,750,000 | |

VMTP

Shares at liquidation value—Note 1 ($30,225,000 face amount,

respectively, report net of unamortized VMTP Shares

deferred offering cost

of $168,836)—Note 1(g) | | 30,056,164 | |

Interest

and expense payable related to

inverse floater notes issued—Note 3 | | 560,476 | |

Dividends

payable to Common Stockholders | | 394,390 | |

Directors’ fees and expenses payable | | 1,100 | |

Other

accrued expenses | | | | | 32,647 | |

| | | | |

81,911,585 | |

Net Assets Applicable to Common Stockholders

($) | | | 163,181,544 | |

Composition

of Net Assets ($): | | | | |

Common Stock, par value, $.001 per share

(20,757,267

shares issued and outstanding) | | | | | 20,757 | |

Paid-in

capital | | | | | 179,014,708 | |

Total distributable earnings

(loss) | | | | | (15,853,921) | |

Net

Assets Applicable to Common Stockholders ($) | | | 163,181,544 | |

| | | | | |

Shares Outstanding | | |

(110 million shares authorized) | 20,757,267 | |

Net

Asset Value Per Share of Common Stock ($) | | 7.86 | |

| | | | |

See notes to financial statements. | | | | |

27

STATEMENT

OF OPERATIONS

Year

Ended September 30, 2024

| | | | | | | |

| | | | | | |

| | | | | | |

Investment

Income ($): | | | | |

Interest Income | | | 10,156,817 | |

Expenses: | | | | |

Management

fee—Note 2(a) | | | 1,304,394 | |

Interest

and expense related to inverse

floater notes issued—Note 3 | | | 1,714,487 | |

VMTP

Shares interest expense

and amortization of offering costs—Note1(g) | | | 1,430,413 | |

Professional

fees | | | 284,717 | |

Shareholders’

reports | | | 166,006 | |

Directors’

fees and expenses—Note 2(c) | | | 142,965 | |

Shareholder

servicing costs | | | 22,151 | |

Registration

fees | | | 13,333 | |

Chief

Compliance Officer fees—Note 2(b) | | | 12,410 | |

Redemption and Paying Agent fees—Note 2(b) | | | 10,000 | |

Custodian

fees—Note 2(b) | | | 4,768 | |

Miscellaneous | | | 37,441 | |

Total

Expenses | | |

5,143,085 | |

Less—reduction

in fees due to

earnings credits—Note 2(b) | | | (4,768) | |

Net

Expenses | | | 5,138,317 | |

Net Investment Income | | | 5,018,500 | |

Realized

and Unrealized Gain (Loss) on Investments—Note 3 ($): | | |

Net realized gain (loss) on

investments | (4,361,212) | |

Net

change in unrealized appreciation (depreciation) on

investments | 24,938,491 | |

Net Realized and Unrealized Gain (Loss) on

Investments | 20,577,279

| |

Net Increase in Net Assets Applicable to

Common

Stockholders Resulting from Operations | 25,595,779 | |

| | | | | | |

See notes to financial statements. | | | | | |

28

STATEMENT

OF CASH FLOWS

Year

Ended September 30, 2024

| | | | | | | |

| | | | | |

| | | | | | |

Cash Flows from Operating Activities ($): | | | | | |

Purchases of portfolio securities | |

(83,786,259) | | | |

Proceeds

from sales of portfolio securities |

79,687,795 | | | |

Interest

income received | | 10,115,339 | | | |

Interest and expense related to inverse

floater notes issued | | (1,740,655) | | | |

VMTP

Shares interest expense and amortization

of offering costs paid | | (1,335,913) | | | |

Expenses paid to BNY Mellon Investment

Adviser, Inc. and affiliates | | (1,324,716) | | | |

Operating expenses paid | | (715,896) | | | |

Net Cash Provided (or Used) in Operating Activities | | 899,695 | |

Cash

Flows from Financing Activities ($): | | | | | |

Dividends paid to Common Stockholders | | (3,985,261) | | | |

Increase in payable for inverse floater notes

issued | | 3,622,907 | | | |

Net

Cash Provided (or Used) in Financing Activities | | (362,354) | |

Net Increase (Decrease) in Cash | | 537,341 | |

Cash

at beginning of period | | 249,920 | |

Cash

at End of Period | |

787,261 | |

Reconciliation

of Net Increase (Decrease) in Net Assets Applicable

to Common Stockholders

Resulting from Operations to

Net Cash Provided (or Used) in Operating Activities

($): | | | |

Net

Increase in Net Assets Resulting From Operations | | 25,595,779 | | | |

Adjustments

to Reconcile Net Increase (Decrease)

in Net Assets Applicable to Common Stockholders

Resulting from Operations to Net

Cash

Provided (or Used) in Operating Activities ($): | | | |

Decrease in investments in securities at

cost | | 257,608 | | | |

Increase in interest receivable | | (41,478) | | | |

Decrease in receivable for investment securities

sold | | 955,547 | | | |

Decrease in unamortized VMTP Shares offering

costs | | 94,500 | | | |

Increase in prepaid expenses | | (7,877) | | | |

Increase in Due to BNY Mellon Investment

Adviser, Inc. and affiliates | |

2,088 | | | |

Decrease in payable for investment

securities purchased | | (950,407) | | | |

Decrease in interest and expense payable

related

to inverse floater notes issued | |

(26,168) | | | |

Increase in Directors' fees and expenses payable | |

1,100 | | | |

Decrease in other accrued expenses | | (42,506) | | | |

Net change in unrealized (appreciation) depreciation

on investments | | (24,938,491) | | | |

Net

Cash Provided (or Used) in Operating Activities | | 899,695 | |

See notes to financial statements. | | | | | |

29

STATEMENT

OF CHANGES IN NET ASSETS

| | | | | | | | | | |

| | | Year Ended September

30, |

| | | | 2024 | | 2023 | |

Operations ($): | | | | | | | | |

Net investment income | | | 5,018,500 | | | | 5,804,713 | |

Net

realized gain (loss) on investments | | (4,361,212) | | | | (5,432,377) | |

Net

change in unrealized appreciation

(depreciation) on investments | | 24,938,491

| | | | 3,026,877 | |

Dividends

to Preferred Stockholders | | | - | | | | (1,275,815) | |

Net Increase

(Decrease) in Net Assets

Applicable to Common Stockholders

Resulting from Operations | 25,595,779 | | | | 2,123,398 | |

Distributions

($): | |

Distributions to stockholders | | | (4,068,424) | | | | (4,421,298) | |

Distributions

to Common

Stockholders |

(4,068,424) | | | |

(4,421,298) | |

Capital Stock Transactions ($): | | | | | | |

Net proceeds from VMTP Shares sold | - | | | | 30,225,000 | |

Cost

of Auction Preferred Stock

shares redeemed | - | | | | (30,225,000) | |

Increase

(Decrease) in Net Assets

from Capital Stock Transactions | - | | | | - | |

Total Increase (Decrease) in Net Assets

Applicable to Common Stockholders | 21,527,355

| | | |

(2,297,900) | |

Net Assets

Applicable to Common Stockholders ($): | |

Beginning

of Period | | | 141,654,189 | | | | 143,952,089 | |

End

of Period | | | 163,181,544 | | | | 141,654,189 | |

| | | | | | | | | |

See notes to financial statements. | | | | | | | | |

30

FINANCIAL

HIGHLIGHTS

The following table describes the performance

for the fiscal periods indicated. Market price total return is calculated assuming an initial investment

made at the market price at the beginning of the period, reinvestment of all dividends and distributions

at market price during the period, and sale at the market price on the last day of the period.

| | | | | | | | | | | | |

| | | | | | |

| | Year Ended September 30, |

| | 2024 | 2023a | 2022b | 2021c | 2020d |

Per Share

Data ($): | | | | | | |

Net asset value, beginning of period | | 6.82 | 6.94 | 9.29 | 9.05 | 9.36 |

Investment Operations: | | | | | | |

Net investment incomee | | .24 | .28 | .36 | .41 | .43 |

Net

realized and unrealized gain

(loss) on investments | | 1.00 | (.13) | (2.35) | .25 | (.30) |

Dividends

to Preferred Stockholders

from net investment income | | - | (.06) | (.02) | (.00)f | (.02) |

Total

from Investment Operations | | 1.24 | (.09) | (2.01) | .66 | .11 |

Distributions

to

Common Stockholders: | | | | | | |

Dividends

from net investment

income | | (.20) | (.21) | (.34) | (.42) | (.42) |

Net asset value, end

of period | | 7.86 | 6.82 | 6.94 | 9.29 | 9.05 |

Market value, end of

period | | 7.31 | 5.67 | 6.01 | 9.63 | 8.63 |

Market

Price Total Return (%) | | 32.73 | (2.41) | (34.69) | 16.90 | (3.13) |

31

FINANCIAL

HIGHLIGHTS (continued)

| | | | | | | | | | | |

| | | | | | |

| | Year Ended September 30, |

| | 2024 | 2023a | 2022b | 2021c | 2020d |

Ratios/Supplemental

Data (%): | | | | | | |

Ratio

of total expenses to

average net assets | | 3.29g | 2.48 | 1.48 | 1.25 | 1.68 |

Ratio

of net expenses to

average net assets | | 3.29g | 2.48 | 1.48 | 1.25 | 1.67 |

Ratio

of interest and expense

related to inverse floater notes

issued,

VMTP Shares

interest expense

to

average net assets | | 2.01g | 1.40 | .42 | .25 | .67 |

Ratio

of net investment income

to average net assets | | 3.21g | 3.82 | 4.30 | 4.37 | 4.78 |

Portfolio

Turnover Rate | | 34.88 | 25.17 | 31.87 | 11.33 | 26.85 |

Asset Coverage of VMTP

Shares and Preferred Stock, end of period | | 640 | 569 | 576 | 738 | 721 |

Net Assets applicable to

Common

Stockholders,

end of period ($ x 1,000) | | 163,182 | 141,654 | 143,952 | 192,790 | 187,703 |

VMTP Shares and Preferred

Stock Outstanding, end of period ($ x 1,000) | | 30,225 | 30,225 | 30,225 | 30,225 | 30,225 |

Floating

Rate Notes Outstanding,

end of period ($ x 1,000) | | 50,750 | 47,127 | 57,245 | 67,430 | 71,180 |

a The

ratios based on total average net assets including dividends to Preferred Stockholders are as follows:

total expense ratio of 2.13%, a net expense ratio of 2.13%, an interest expense related to floating rate

notes issued ratio of 1.20% and a net investment income of 3.29%.

b The ratios based on total average net assets including dividends

to Preferred Stockholders are as follows: total expense ratio of 1.26%, a net expense ratio of 1.26%,

an interest expense related to floating rate notes issued ratio of .36% and a net investment income of

3.66%.

c The

ratios based on total average net assets including dividends to Preferred Stockholders are as follows:

total expense ratio of 1.08%, a net expense ratio of 1.08%, an interest expense related to floating rate

notes issued ratio of .22% and a net investment income of 3.78%.

d The ratios based on total average net assets including dividends

to Preferred Stockholders are as follows: total expense ratio of 1.44%, a net expense ratio of 1.44%,

an interest expense related to floating rate notes issued ratio of .58% and a net investment income of

4.12%.

e Based

on average common shares outstanding.

f Amount represents less than $.01 per share.

g Amount inclusive of VMTP Shares amortization of offering cost.

See notes to financial statements.

32

NOTES

TO FINANCIAL STATEMENTS

NOTE 1—Significant Accounting Policies:

BNY

Mellon Municipal Income, Inc. (the “fund”), which is registered under the Investment Company Act

of 1940, as amended (the “Act”), is a diversified closed-end management investment company. The

fund’s investment objective is to maximize current income exempt from federal income tax to the extent

consistent with the preservation of capital. BNY Mellon Investment Adviser, Inc. (the “Adviser”),

a wholly-owned subsidiary of The Bank of New York Mellon Corporation (“BNY”), serves as the fund’s

investment adviser. Insight North America LLC (the “Sub-Adviser”), an indirect wholly-owned subsidiary

of BNY and an affiliate of the Adviser, serves as the fund’s sub-adviser. The fund’s Common Stock

trades on the NYSE American under the ticker symbol DMF.

The fund has outstanding

1,209 shares of Variable Rate MuniFund Term Preferred Shares (“VMTP Shares”). The fund is subject

to certain restrictions relating to the VMTP Shares. Failure to comply with these restrictions could

preclude the fund from declaring any distributions to shareholders of the fund’s Common Stock (“Common

Stockholders”) or repurchasing shares of Common Stock and/or could trigger the mandatory redemption

of VMTP Shares at their liquidation value (i.e., $25,000 per share). Thus, redemptions of VMTP Shares

may be deemed to be outside of the control of the fund.

The VMTP Shares have

a mandatory redemption date of July 14, 2053, and are subject to an initial early redemption date of

July 13, 2026, subject to the option of the shareholders to retain the VMTP Shares. VMTP Shares that

are neither retained by the shareholder nor successfully remarketed by the early redemption date will

be redeemed by the fund.

The shareholders of VMTP Shares, voting as a separate class,

have the right to elect at least two directors. The shareholders of VMTP Shares will vote as a separate

class on certain other matters, as required by law. The fund’s Board of Directors (the “Board”)

has designated Nathan Leventhal and Benaree Pratt Wiley as directors to be elected by the holders of

VMTP Shares.

Dividends on VMTP Shares are normally declared daily and paid

monthly. The Dividend Rate on the VMTP Shares is, except as otherwise provided, equal to the rate per

annum that results from the sum of (1) the Index Rate plus (2) the Applicable Spread as determined for

the VMTP Shares on the Rate Determination Date immediately preceding such Subsequent Rate Period plus

(3) the Failed Remarketing Spread (all defined terms as defined in the fund’s articles supplementary).

33

NOTES

TO FINANCIAL STATEMENTS (continued)

The Financial Accounting Standards Board (“FASB”) Accounting Standards Codification

(“ASC”) is the exclusive reference of authoritative U.S. generally accepted accounting principles

(“GAAP”) recognized by the FASB to be applied by nongovernmental entities. Rules and interpretive

releases of the Securities and Exchange Commission (“SEC”) under authority of federal laws are also

sources of authoritative GAAP for SEC registrants. The fund is an investment company and applies the

accounting and reporting guidance of the FASB ASC Topic 946 Financial Services-Investment Companies.

The fund’s financial statements are prepared in accordance with GAAP, which may require the use of

management estimates and assumptions. Actual results could differ from those estimates.

The fund

enters

into contracts that contain a variety of indemnifications. The fund’s maximum exposure under these

arrangements is unknown. The fund does not anticipate recognizing any loss related to these arrangements.

(a)

Portfolio valuation: The fair value of a financial instrument is the amount that would be received

to sell an asset or paid to transfer a liability in an orderly transaction between market participants

at the measurement date (i.e., the exit price). GAAP establishes a fair value hierarchy that prioritizes

the inputs of valuation techniques used to measure fair value. This hierarchy gives the highest priority

to unadjusted quoted prices in active markets for identical assets or liabilities (Level 1 measurements)

and the lowest priority to unobservable inputs (Level 3 measurements).

Additionally,

GAAP provides guidance on determining whether the volume and activity in a market has decreased significantly

and whether such a decrease in activity results in transactions that are not orderly. GAAP requires enhanced

disclosures around valuation inputs and techniques used during annual and interim periods.

Various

inputs are used in determining the value of the fund’s investments relating to fair value measurements.

These inputs are summarized in the three broad levels listed below:

Level 1—unadjusted quoted

prices in active markets for identical investments.

Level 2—other significant

observable inputs (including quoted prices for similar investments, interest rates, prepayment speeds,

credit risk, etc.).

Level 3—significant unobservable inputs (including

the fund’s own assumptions in determining the fair value of investments).

34

The inputs or methodology used for valuing securities are not necessarily an indication

of the risk associated with investing in those securities.

Changes in valuation

techniques may result in transfers in or out of an assigned level within the disclosure hierarchy. Valuation

techniques used to value the fund’s investments are as follows:

The Board has designated

the Adviser as the fund’s valuation designee to make all fair value determinations with respect to

the fund’s portfolio investments, subject to the Board’s oversight and pursuant to Rule 2a-5 under

the Act.

Investments in municipal securities are valued each business day by an independent

pricing service (the “Service”) approved by the Board. Investments for which quoted bid prices are

readily available and are representative of the bid side of the market in the judgment of the Service

are valued at the mean between the quoted bid prices (as obtained by the Service from dealers in such

securities) and asked prices (as calculated by the Service based upon its evaluation of the market for

such securities). Municipal investments (which constitute a majority of the portfolio securities) are

carried at fair value as determined by the Service, based on methods which include consideration of the

following: yields or prices of municipal securities of comparable quality, coupon, maturity and type;

indications as to values from dealers; and general market conditions. The Service is engaged under the

general oversight of the Board. All of the preceding securities are generally categorized within Level

2 of the fair value hierarchy.

When market quotations or official closing prices are not

readily available, or are determined not to accurately reflect fair value, such as when the value of

a security has been significantly affected by events after the close of the exchange or market on which

the security is principally traded, but before the fund calculates its net asset value, the fund may

value these investments at fair value as determined in accordance with the procedures approved by the

Board. Certain factors may be considered when fair valuing investments such as: fundamental analytical

data, the nature and duration of restrictions on disposition, an evaluation of the forces that influence

the market in which the securities are purchased and sold, and public trading in similar securities of

the issuer or comparable issuers. These securities are either categorized within Level 2 or 3 of the

fair value hierarchy depending on the relevant inputs used.

For securities where

observable inputs are limited, assumptions about market activity and risk are used and such securities

are generally categorized within Level 3 of the fair value hierarchy.

35

NOTES

TO FINANCIAL STATEMENTS (continued)

The

following is a summary of the inputs used as of September 30, 2024 in

valuing the fund’s investments:

| | | | | | | |

| | Level 1-Unadjusted Quoted Prices | Level

2- Other Significant Observable Inputs | | Level 3-Significant Unobservable

Inputs | Total | |

Assets ($) | | |

Investments in Securities:† | | |

Municipal

Securities | - | 241,189,562 | | - | 241,189,562 | |

Liabilities

($) | | |

Other Financial Instruments: | | |

Inverse Floater Notes†† | - | (50,750,000) | | - | (50,750,000) | |

VMTP

Shares†† | - | (30,225,000) | | - | (30,225,000) | |

† See Statement of Investments for additional detailed categorizations,

if any.

†† Certain

of the fund’s liabilities are held at carrying amount, which approximates fair value for financial

reporting purposes.

(b) Securities transactions and investment income: Securities transactions

are recorded on a trade date basis. Realized gains and losses from securities transactions are recorded

on the identified cost basis. Interest income, adjusted for accretion of discount and amortization of

premium on investments, is earned from settlement date and recognized on the accrual basis. Securities

purchased or sold on a when-issued or delayed delivery basis may be settled a month or more after the

trade date.

(c) Market Risk: The value of the securities in which the fund invests may

be affected by political, regulatory, economic and social developments, and developments that impact

specific economic sectors, industries or segments of the market. The value of a security may also decline

due to general market conditions that are not specifically related to a particular company or industry,

such as real or perceived adverse economic conditions, changes in the general outlook for corporate earnings,

changes in interest or currency rates, changes to inflation, adverse changes to credit markets or adverse

investor sentiment generally.

Additional Information section within

this report provides more details about the fund’s principal risk factors.

(d) Dividends and distributions

to Common Stockholders: Dividends and distributions are recorded on the ex-dividend date. Dividends from

net investment income are normally declared and paid monthly. Dividends from net realized capital gains,

if any, are normally declared and paid

36

annually, but the fund may make distributions on a more frequent basis to comply

with the distribution requirements of the Internal Revenue Code of 1986, as amended (the “Code”).

To the extent that net realized capital gains can be offset by capital loss carryovers, it is the policy

of the fund not to distribute such gains. Income and capital gain distributions are determined in accordance

with income tax regulations, which may differ from GAAP.

Common Stockholders

will have their distributions reinvested in additional shares of the fund, unless such Common Stockholders

elect to receive cash, at the lower of the market price or net asset value per share (but not less than

95% of the market price). If market price is equal to or exceeds net asset value, shares will be issued

at net asset value. If net asset value exceeds market price, Computershare Inc., the transfer agent for

the fund’s Common Stock, will buy fund shares in the open market and reinvest those shares accordingly.

On September 27, 2024, the Board declared a cash dividend of $.019 per share from

net investment income, payable on October 31, 2024 to Common Stockholders of record as of the close of

business on October 15, 2024. The ex-dividend date was October 15, 2024.

(e) Dividends to stockholders

of VMTP Shares: The Dividend Rate on the VMTP Shares is, except as otherwise provided, equal

to the rate per annum that results from the sum of (1) the Index Rate plus (2) the Applicable Spread

as determined for the VMTP Shares on the Rate Determination Date immediately preceding such Subsequent

Rate Period plus (3) the Failed Remarketing Spread. The Applicable Rate of the VMTP Shares was equal

to the sum of .95% per annum plus the Securities Industry and Financial Markets Association Municipal

Swap Index rate of 3.15% on September 30, 2024. The dividend rate as of September 30, 2024 for the VMTP

Shares was 4.10% (all terms as defined in the fund’s articles supplementary).

(f) Federal income taxes:

It is the policy of the fund to continue to qualify as a regulated investment company, which can distribute

tax-exempt dividends, by complying with the applicable provisions of the Code, and to make distributions

of income and net realized capital gain sufficient to relieve it from substantially all federal income

and excise taxes.

As of and during the period ended September 30, 2024, the

fund did not have any liabilities for any uncertain tax positions. The fund recognizes interest and penalties,

if any, related to uncertain tax positions as income tax expense in the Statement of Operations. During

the period ended September 30, 2024, the fund did not incur any interest or penalties.

37

NOTES

TO FINANCIAL STATEMENTS (continued)

Each tax year in the four-year period ended September 30, 2024 remains subject

to examination by the Internal Revenue Service and state taxing authorities.

At

September 30, 2024, the components of accumulated earnings on a tax basis were as follows: undistributed

tax-exempt income $1,513,122, accumulated capital losses $26,223,695 and unrealized appreciation $9,251,042.

The fund is permitted to carry forward capital losses for an unlimited period.

Furthermore, capital loss carryovers retain their character as either short-term or long-term capital

losses.

The

accumulated capital loss carryover is available for federal income tax purposes to be applied against

future net realized capital gains, if any, realized

subsequent to September 30, 2024. The fund has $10,322,932 of short-term capital losses and $15,900,763

of long-term capital losses which can be carried forward for an unlimited period.

The

tax character of distributions paid to Common Stockholders during the fiscal years ended September 30,

2024 and September 30, 2023 were as follows: tax-exempt income $4,068,424 and $5,697,113, respectively.

(g)

VMTP Shares: The fund’s VMTP Shares aggregate liquidation preference is shown as a liability

since they have a stated mandatory redemption date of July 14, 2053. Dividends paid on VMTP Shares are

treated as interest expense and recorded on the accrual basis. Costs directly related to the issuance

of the VMTP Shares are considered debt issuance costs which have been deferred and are being amortized

into expense over 36 months from July 12, 2023.

During the period ended

September 30, 2024, total interest expenses and amortized offering costs with respect to VMTP Shares

amounted to $1,430,413 inclusive of $1,335,113 of interest expense and $95,300 amortized deferred cost

fees. These fees are included in VMTP Shares interest expense and amortization of offering costs in the

Statement of Operations.

The average amount of borrowings outstanding for the VMTP

Shares during the period ended September 30, 2024 was approximately $30,225,000, with a related weighted

average annualized interest rate of 4.42%.

38

NOTE

2—Management Fee, Sub-Advisory Fee and Other Transactions with Affiliates:

(a) Pursuant to a management

agreement (the “Agreement”) with the Adviser, the management fee is computed at the annual rate of

..70% of the value of the fund’s average weekly net assets (including net assets representing VMTP Shares

outstanding) and is payable monthly. The Agreement provides that if in any full fiscal year the aggregate

expenses of the fund (excluding taxes, interest on borrowings, brokerage fees and extraordinary expenses)

exceed the expense limitation of any state having jurisdiction over the fund, the fund may deduct from

payments to be made to the Adviser, or the Adviser will bear, the amount of such excess to the extent

required by state law. During the period ended September 30, 2024, there was no expense reimbursement

pursuant to the Agreement.

Pursuant to a sub-investment advisory

agreement between the Adviser and the Sub-Adviser, the Adviser pays the Sub-Adviser a monthly fee at

an annual rate of .336% of the value of the fund’s average weekly net assets (including net assets

representing VMTP Shares outstanding).

(b) The fund

has an arrangement with The Bank of New York Mellon (the “Custodian”), a subsidiary of BNY and an

affiliate of the Adviser, whereby the fund may receive earnings credits when