The

information in this preliminary pricing supplement is not complete and may be changed. A registration statement relating to these

notes has been filed with the Securities and Exchange Commission. This preliminary pricing supplement and the accompanying product

supplement, underlying supplement, prospectus supplement and prospectus are not an offer to sell these notes, nor are they soliciting

an offer to buy these notes, in any state where the offer or sale is not permitted.

SUBJECT

TO COMPLETION, DATED FEBRUARY 13, 2025 |

| Citigroup Global Markets Holdings Inc. |

February

, 2025

Medium-Term

Senior Notes, Series N

Pricing

Supplement No. 2025-USNCH25883

Filed

Pursuant to Rule 424(b)(2)

Registration

Statement Nos. 333-270327 and 333-270327-01 |

Autocallable Market-Linked Notes Linked to the S&P

500 Futures 35% Edge Volatility 6% Decrement Index (USD) ER Due March 5, 2035

Overview

| ▪ | The notes offered by this pricing supplement are unsecured senior debt securities issued by Citigroup Global Markets Holdings Inc.

and guaranteed by Citigroup Inc. Unlike conventional debt securities, the notes do not pay interest. Instead, the notes offer

the potential for automatic early redemption at a premium on a periodic basis on the terms described below. Your return on the notes will

depend on the performance of the S&P 500 Futures 35% Edge Volatility 6% Decrement Index (USD) ER (the “underlying”) specified

below. |

| ▪ | The notes offer the potential for automatic early redemption at a premium following the first valuation date (other than the final

valuation date) on which the closing value of the underlying is greater than or equal to the initial underlying value. If the notes are

not automatically redeemed prior to maturity, the notes will provide for repayment of the stated principal amount plus a premium

at maturity if the final underlying value is greater than or equal to the final premium threshold value. However, if the notes are

not automatically redeemed prior to maturity and the final underlying value is less than the final premium threshold value, you will be

repaid the stated principal amount of your notes at maturity but will not receive any return on your investment. You will not receive

dividends with respect to the underlying or participate in any appreciation of the underlying. |

| ▪ | The notes are designed for investors who are willing to forgo interest on the notes and accept the risk of not receiving any return

on the notes in exchange for the possibility of automatic early redemption at a premium or, if the notes are not automatically redeemed

prior to maturity, a premium at maturity, based in each case on the performance of the underlying. Investors should understand that there

is no guarantee that they will receive a positive return on their investment in the notes and that even if they do receive a positive

return, there is no assurance that their total return at maturity on the notes will compensate them for the effects of inflation or be

as great as the yield they could have achieved on a conventional debt security of ours of comparable maturity. |

| ▪ | The underlying is highly risky because it may reflect highly leveraged exposure to any decline in the S&P 500 Futures Excess

Return Index. The S&P 500 Futures Excess Return Index tracks futures contracts on the S&P 500® Index and is likely

to underperform the S&P 500® Index because of an implicit financing cost. In addition, the underlying is subject to

a decrement of 6% per annum, which will be a significant drag on its performance. You should carefully review the section “Summary

Risk Factors—Risks relating to the S&P 500 Futures 35% Edge Volatility 6% Decrement Index (USD) ER” in this pricing supplement. |

| ▪ | Investors in the notes must be willing to accept (i) an investment that may have limited or no liquidity and (ii) the risk of not

receiving any payments due under the notes if we and Citigroup Inc. default on our obligations. All payments on the notes are subject

to the credit risk of Citigroup Global Markets Holdings Inc. and Citigroup Inc. |

| KEY TERMS |

| Issuer: |

Citigroup Global Markets Holdings Inc., a wholly owned subsidiary of Citigroup Inc. |

| Guarantee: |

All payments due on the notes are fully and unconditionally guaranteed by Citigroup

Inc. |

| Underlying: |

The S&P 500 Futures 35% Edge Volatility 6% Decrement Index (USD) ER |

| Stated principal amount: |

$1,000 per note |

| Pricing date: |

February 26, 2025 |

| Issue date: |

February 28, 2025 |

| Maturity date: |

Unless earlier redeemed, March 5, 2035 |

| Automatic early redemption: |

If, on any valuation date prior to the final valuation date, the closing value of the

underlying is greater than or equal to the initial underlying value, the notes will be automatically redeemed on the third business

day immediately following that valuation date for an amount in cash per note equal to $1,000 plus the premium applicable to that

valuation date. If the notes are automatically redeemed following any valuation date prior to the final valuation date, they will

cease to be outstanding and you will no longer have the opportunity to receive the premium applicable to any later valuation date. |

| Payment at maturity: |

If the notes are not automatically

redeemed prior to maturity, you will receive at maturity for each note you then hold:

§

If

the final underlying value is greater than or equal to the final premium threshold value:

$1,000 + the premium applicable

to the final valuation date

§

If

the final underlying value is less than the final premium threshold value:

$1,000 |

| Initial underlying value: |

, the closing value of the underlying

on the pricing date |

| Final underlying value: |

The closing value of the underlying on the final valuation date |

| Final premium threshold value: |

, 60% of the initial underlying

value |

| Listing: |

The notes will not be listed on any securities exchange |

| Underwriter: |

Citigroup Global Markets Inc. (“CGMI”), an affiliate of the issuer,

acting as principal |

| Underwriting fee and issue price: |

Issue price(1) |

Underwriting fee(2) |

Proceeds to issuer |

| Per note: |

$1,000.00 |

$50.00 |

$950.00 |

| Total: |

$ |

$ |

$ |

(Key Terms continued

on next page)

(1) Citigroup Global Markets Holdings

Inc. currently expects that the estimated value of the notes on the pricing date will be at least $850.00 per note, which will be less

than the issue price. The estimated value of the notes is based on CGMI’s proprietary pricing models and our internal funding rate.

It is not an indication of actual profit to CGMI or other of our affiliates, nor is it an indication of the price, if any, at which CGMI

or any other person may be willing to buy the notes from you at any time after issuance. See “Valuation of the Notes” in

this pricing supplement.

(2) For more information on the distribution

of the notes, see “Supplemental Plan of Distribution” in this pricing supplement. In addition to the underwriting fee, CGMI

and its affiliates may profit from expected hedging activity related to this offering, even if the value of the notes declines. See “Use

of Proceeds and Hedging” in the accompanying prospectus.

Concurrent with this offering of the notes,

the issuer is offering other notes that are similar to the notes but that have economic terms that differ from those provided by the

notes. The differences in the economic terms reflect differences in costs to the issuer in connection with the distribution of the notes

and such other notes.

Investing in the notes involves risks

not associated with an investment in conventional debt securities. See “Summary Risk Factors” beginning on page PS-9.

Neither the Securities

and Exchange Commission (the “SEC”) nor any state securities commission has approved or disapproved of the notes or determined

that this pricing supplement and the accompanying product supplement, underlying supplement, prospectus supplement and prospectus are

truthful or complete. Any representation to the contrary is a criminal offense.

You should read

this pricing supplement together with the accompanying product supplement, underlying supplement, prospectus supplement and prospectus,

which can be accessed via the hyperlinks below:

Prospectus

Supplement and Prospectus each dated March 7, 2023

The notes are not

bank deposits and are not insured or guaranteed by the Federal Deposit Insurance Corporation or any other governmental agency, nor are

they obligations of, or guaranteed by, a bank.

| Citigroup Global Markets Holdings Inc. |

| |

| KEY TERMS (continued) |

| Valuation dates and premiums: |

The premium applicable to each valuation

date is the percentage of the stated principal amount set forth below. The premium may be significantly less than the appreciation

of the underlying from the pricing date to the applicable valuation date.

|

| |

Valuation date* |

Premium |

| |

March 1, 2027 |

20.0000% of the stated principal amount |

| |

March 29, 2027 |

20.8333% of the stated principal amount |

| |

April 28, 2027 |

21.6667% of the stated principal amount |

| |

May 28, 2027 |

22.5000% of the stated principal amount |

| |

June 28, 2027 |

23.3333% of the stated principal amount |

| |

July 28, 2027 |

24.1667% of the stated principal amount |

| |

August 30, 2027 |

25.0000% of the stated principal amount |

| |

September 28, 2027 |

25.8333% of the stated principal amount |

| |

October 28, 2027 |

26.6667% of the stated principal amount |

| |

November 29, 2027 |

27.5000% of the stated principal amount |

| |

December 28, 2027 |

28.3333% of the stated principal amount |

| |

January 28, 2028 |

29.1667% of the stated principal amount |

| |

February 28, 2028 |

30.0000% of the stated principal amount |

| |

March 28, 2028 |

30.8333% of the stated principal amount |

| |

April 28, 2028 |

31.6667% of the stated principal amount |

| |

May 30, 2028 |

32.5000% of the stated principal amount |

| |

June 28, 2028 |

33.3333% of the stated principal amount |

| |

July 28, 2028 |

34.1667% of the stated principal amount |

| |

August 28, 2028 |

35.0000% of the stated principal amount |

| |

September 28, 2028 |

35.8333% of the stated principal amount |

| |

October 30, 2028 |

36.6667% of the stated principal amount |

| |

November 28, 2028 |

37.5000% of the stated principal amount |

| |

December 28, 2028 |

38.3333% of the stated principal amount |

| |

January 29, 2029 |

39.1667% of the stated principal amount |

| |

February 28, 2029 |

40.0000% of the stated principal amount |

| |

March 28, 2029 |

40.8333% of the stated principal amount |

| |

April 30, 2029 |

41.6667% of the stated principal amount |

| |

May 29, 2029 |

42.5000% of the stated principal amount |

| |

June 28, 2029 |

43.3333% of the stated principal amount |

| |

July 30, 2029 |

44.1667% of the stated principal amount |

| |

August 28, 2029 |

45.0000% of the stated principal amount |

| |

September 28, 2029 |

45.8333% of the stated principal amount |

| |

October 29, 2029 |

46.6667% of the stated principal amount |

| |

November 28, 2029 |

47.5000% of the stated principal amount |

| |

December 28, 2029 |

48.3333% of the stated principal amount |

| |

January 28, 2030 |

49.1667% of the stated principal amount |

| |

February 28, 2030 |

50.0000% of the stated principal amount |

| |

March 28, 2030 |

50.8333% of the stated principal amount |

| |

April 29, 2030 |

51.6667% of the stated principal amount |

| |

May 28, 2030 |

52.5000% of the stated principal amount |

| |

June 28, 2030 |

53.3333% of the stated principal amount |

| |

July 29, 2030 |

54.1667% of the stated principal amount |

| |

August 28, 2030 |

55.0000% of the stated principal amount |

| |

September 30, 2030 |

55.8333% of the stated principal amount |

| |

October 28, 2030 |

56.6667% of the stated principal amount |

| |

November 29, 2030 |

57.5000% of the stated principal amount |

| |

December 30, 2030 |

58.3333% of the stated principal amount |

| |

January 28, 2031 |

59.1667% of the stated principal amount |

| |

February 28, 2031 |

60.0000% of the stated principal amount |

| |

March 28, 2031 |

60.8333% of the stated principal amount |

| |

April 28, 2031 |

61.6667% of the stated principal amount |

| |

May 28, 2031 |

62.5000% of the stated principal amount |

| |

June 30, 2031 |

63.3333% of the stated principal amount |

| |

July 28, 2031 |

64.1667% of the stated principal amount |

| |

August 28, 2031 |

65.0000% of the stated principal amount |

| |

September 29, 2031 |

65.8333% of the stated principal amount |

| |

October 28, 2031 |

66.6667% of the stated principal amount |

| |

November 28, 2031 |

67.5000% of the stated principal amount |

| |

December 29, 2031 |

68.3333% of the stated principal amount |

| |

January 28, 2032 |

69.1667% of the stated principal amount |

| |

March 1, 2032 |

70.0000% of the stated principal amount |

| |

March 29, 2032 |

70.8333% of the stated principal amount |

| |

April 28, 2032 |

71.6667% of the stated principal amount |

| |

May 28, 2032 |

72.5000% of the stated principal amount |

| |

June 28, 2032 |

73.3333% of the stated principal amount |

| |

July 28, 2032 |

74.1667% of the stated principal amount |

| |

August 30, 2032 |

75.0000% of the stated principal amount |

| |

September 28, 2032 |

75.8333% of the stated principal amount |

| |

October 28, 2032 |

76.6667% of the stated principal amount |

| Citigroup Global Markets Holdings Inc. |

| |

| |

November 29, 2032 |

77.5000% of the stated principal amount |

| |

December 28, 2032 |

78.3333% of the stated principal amount |

| |

January 28, 2033 |

79.1667% of the stated principal amount |

| |

February 28, 2033 |

80.0000% of the stated principal amount |

| |

March 28, 2033 |

80.8333% of the stated principal amount |

| |

April 28, 2033 |

81.6667% of the stated principal amount |

| |

May 31, 2033 |

82.5000% of the stated principal amount |

| |

June 28, 2033 |

83.3333% of the stated principal amount |

| |

July 28, 2033 |

84.1667% of the stated principal amount |

| |

August 29, 2033 |

85.0000% of the stated principal amount |

| |

September 28, 2033 |

85.8333% of the stated principal amount |

| |

October 28, 2033 |

86.6667% of the stated principal amount |

| |

November 28, 2033 |

87.5000% of the stated principal amount |

| |

December 28, 2033 |

88.3333% of the stated principal amount |

| |

January 30, 2034 |

89.1667% of the stated principal amount |

| |

February 28, 2034 |

90.0000% of the stated principal amount |

| |

March 28, 2034 |

90.8333% of the stated principal amount |

| |

April 28, 2034 |

91.6667% of the stated principal amount |

| |

May 30, 2034 |

92.5000% of the stated principal amount |

| |

June 28, 2034 |

93.3333% of the stated principal amount |

| |

July 28, 2034 |

94.1667% of the stated principal amount |

| |

August 28, 2034 |

95.0000% of the stated principal amount |

| |

September 28, 2034 |

95.8333% of the stated principal amount |

| |

October 30, 2034 |

96.6667% of the stated principal amount |

| |

November 28, 2034 |

97.5000% of the stated principal amount |

| |

December 28, 2034 |

98.3333% of the stated principal amount |

| |

January 29, 2035 |

99.1667% of the stated principal amount |

| |

February 28, 2035 (the “final valuation date”) |

100.0000% of the stated principal amount |

| |

*Each valuation date is subject to

postponement if such date is not a scheduled trading day or certain market disruption events occur

|

| CUSIP / ISIN: |

17333HVC5 / US17333HVC59 |

| Citigroup Global Markets Holdings Inc. |

| |

Additional Information

General. The terms of the notes are set forth in the accompanying

product supplement, prospectus supplement and prospectus, as supplemented by this pricing supplement. The accompanying product supplement,

prospectus supplement and prospectus contain important disclosures that are not repeated in this pricing supplement. For example, the

accompanying product supplement contains important information about how the closing value of the underlying will be determined and about

adjustments that may be made to the terms of the notes upon the occurrence of market disruption events and other specified events with

respect to the underlying. The accompanying underlying supplement contains important disclosures regarding the S&P 500® Index,

on which the S&P 500 Futures 35% Edge Volatility 6% Decrement Index (USD) ER is ultimately based. It is important that you read the

accompanying product supplement, underlying supplement, prospectus supplement and prospectus together with this pricing supplement in

deciding whether to invest in the notes. Certain terms used but not defined in this pricing supplement are defined in the accompanying

product supplement.

Closing value. The closing value of the underlying is its closing

level, as described in the accompanying product supplement.

| Citigroup Global Markets Holdings Inc. |

| |

Hypothetical Payment Upon Automatic Early Redemption

The following table illustrates how the amount payable per note upon

automatic early redemption will be calculated if the closing value of the underlying on any valuation date prior to the final valuation

date is greater than or equal to the initial underlying value.

| If the first valuation date on which the closing value of the underlying is greater than or equal to the initial underlying value is... |

...then you will receive the following payment per note upon automatic early redemption: |

| 1st valuation date |

$1,000 + applicable premium = $1,000 + $200.000 = $1,200.000 |

| 2nd valuation date |

$1,000 + applicable premium = $1,000 + $208.333 = $1,208.333 |

| 3rd valuation date |

$1,000 + applicable premium = $1,000 + $216.667 = $1,216.667 |

| 4th valuation date |

$1,000 + applicable premium = $1,000 + $225.000 = $1,225.000 |

| 5th valuation date |

$1,000 + applicable premium = $1,000 + $233.333 = $1,233.333 |

| 6th valuation date |

$1,000 + applicable premium = $1,000 + $241.667 = $1,241.667 |

| 7th valuation date |

$1,000 + applicable premium = $1,000 + $250.000 = $1,250.000 |

| 8th valuation date |

$1,000 + applicable premium = $1,000 + $258.333 = $1,258.333 |

| 9th valuation date |

$1,000 + applicable premium = $1,000 + $266.667 = $1,266.667 |

| 10th valuation date |

$1,000 + applicable premium = $1,000 + $275.000 = $1,275.000 |

| 11th valuation date |

$1,000 + applicable premium = $1,000 + $283.333 = $1,283.333 |

| 12th valuation date |

$1,000 + applicable premium = $1,000 + $291.667 = $1,291.667 |

| 13th valuation date |

$1,000 + applicable premium = $1,000 + $300.000 = $1,300.000 |

| 14th valuation date |

$1,000 + applicable premium = $1,000 + $308.333 = $1,308.333 |

| 15th valuation date |

$1,000 + applicable premium = $1,000 + $316.667 = $1,316.667 |

| 16th valuation date |

$1,000 + applicable premium = $1,000 + $325.000 = $1,325.000 |

| 17th valuation date |

$1,000 + applicable premium = $1,000 + $333.333 = $1,333.333 |

| 18th valuation date |

$1,000 + applicable premium = $1,000 + $341.667 = $1,341.667 |

| 19th valuation date |

$1,000 + applicable premium = $1,000 + $350.000 = $1,350.000 |

| 20th valuation date |

$1,000 + applicable premium = $1,000 + $358.333 = $1,358.333 |

| 21st valuation date |

$1,000 + applicable premium = $1,000 + $366.667 = $1,366.667 |

| 22nd valuation date |

$1,000 + applicable premium = $1,000 + $375.000 = $1,375.000 |

| 23rd valuation date |

$1,000 + applicable premium = $1,000 + $383.333 = $1,383.333 |

| 24th valuation date |

$1,000 + applicable premium = $1,000 + $391.667 = $1,391.667 |

| 25th valuation date |

$1,000 + applicable premium = $1,000 + $400.000 = $1,400.000 |

| 26th valuation date |

$1,000 + applicable premium = $1,000 + $408.333 = $1,408.333 |

| 27th valuation date |

$1,000 + applicable premium = $1,000 + $416.667 = $1,416.667 |

| 28th valuation date |

$1,000 + applicable premium = $1,000 + $425.000 = $1,425.000 |

| 29th valuation date |

$1,000 + applicable premium = $1,000 + $433.333 = $1,433.333 |

| 30th valuation date |

$1,000 + applicable premium = $1,000 + $441.667 = $1,441.667 |

| 31st valuation date |

$1,000 + applicable premium = $1,000 + $450.000 = $1,450.000 |

| 32nd valuation date |

$1,000 + applicable premium = $1,000 + $458.333 = $1,458.333 |

| 33rd valuation date |

$1,000 + applicable premium = $1,000 + $466.667 = $1,466.667 |

| 34th valuation date |

$1,000 + applicable premium = $1,000 + $475.000 = $1,475.000 |

| 35th valuation date |

$1,000 + applicable premium = $1,000 + $483.333 = $1,483.333 |

| 36th valuation date |

$1,000 + applicable premium = $1,000 + $491.667 = $1,491.667 |

| 37th valuation date |

$1,000 + applicable premium = $1,000 + $500.000 = $1,500.000 |

| 38th valuation date |

$1,000 + applicable premium = $1,000 + $508.333 = $1,508.333 |

| 39th valuation date |

$1,000 + applicable premium = $1,000 + $516.667 = $1,516.667 |

| 40th valuation date |

$1,000 + applicable premium = $1,000 + $525.000 = $1,525.000 |

| 41st valuation date |

$1,000 + applicable premium = $1,000 + $533.333 = $1,533.333 |

| 42nd valuation date |

$1,000 + applicable premium = $1,000 + $541.667 = $1,541.667 |

| 43rd valuation date |

$1,000 + applicable premium = $1,000 + $550.000 = $1,550.000 |

| 44th valuation date |

$1,000 + applicable premium = $1,000 + $558.333 = $1,558.333 |

| 45th valuation date |

$1,000 + applicable premium = $1,000 + $566.667 = $1,566.667 |

| 46th valuation date |

$1,000 + applicable premium = $1,000 + $575.000 = $1,575.000 |

| 47th valuation date |

$1,000 + applicable premium = $1,000 + $583.333 = $1,583.333 |

| 48th valuation date |

$1,000 + applicable premium = $1,000 + $591.667 = $1,591.667 |

| 49th valuation date |

$1,000 + applicable premium = $1,000 + $600.000 = $1,600.000 |

| Citigroup Global Markets Holdings Inc. |

| |

| 50th valuation date |

$1,000 + applicable premium = $1,000 + $608.333 = $1,608.333 |

| 51st valuation date |

$1,000 + applicable premium = $1,000 + $616.667 = $1,616.667 |

| 52nd valuation date |

$1,000 + applicable premium = $1,000 + $625.000 = $1,625.000 |

| 53rd valuation date |

$1,000 + applicable premium = $1,000 + $633.333 = $1,633.333 |

| 54th valuation date |

$1,000 + applicable premium = $1,000 + $641.667 = $1,641.667 |

| 55th valuation date |

$1,000 + applicable premium = $1,000 + $650.000 = $1,650.000 |

| 56th valuation date |

$1,000 + applicable premium = $1,000 + $658.333 = $1,658.333 |

| 57th valuation date |

$1,000 + applicable premium = $1,000 + $666.667 = $1,666.667 |

| 58th valuation date |

$1,000 + applicable premium = $1,000 + $675.000 = $1,675.000 |

| 59th valuation date |

$1,000 + applicable premium = $1,000 + $683.333 = $1,683.333 |

| 60th valuation date |

$1,000 + applicable premium = $1,000 + $691.667 = $1,691.667 |

| 61st valuation date |

$1,000 + applicable premium = $1,000 + $700.000 = $1,700.000 |

| 62nd valuation date |

$1,000 + applicable premium = $1,000 + $708.333 = $1,708.333 |

| 63rd valuation date |

$1,000 + applicable premium = $1,000 + $716.667 = $1,716.667 |

| 64th valuation date |

$1,000 + applicable premium = $1,000 + $725.000 = $1,725.000 |

| 65th valuation date |

$1,000 + applicable premium = $1,000 + $733.333 = $1,733.333 |

| 66th valuation date |

$1,000 + applicable premium = $1,000 + $741.667 = $1,741.667 |

| 67th valuation date |

$1,000 + applicable premium = $1,000 + $750.000 = $1,750.000 |

| 68th valuation date |

$1,000 + applicable premium = $1,000 + $758.333 = $1,758.333 |

| 69th valuation date |

$1,000 + applicable premium = $1,000 + $766.667 = $1,766.667 |

| 70th valuation date |

$1,000 + applicable premium = $1,000 + $775.000 = $1,775.000 |

| 71st valuation date |

$1,000 + applicable premium = $1,000 + $783.333 = $1,783.333 |

| 72nd valuation date |

$1,000 + applicable premium = $1,000 + $791.667 = $1,791.667 |

| 73rd valuation date |

$1,000 + applicable premium = $1,000 + $800.000 = $1,800.000 |

| 74th valuation date |

$1,000 + applicable premium = $1,000 + $808.333 = $1,808.333 |

| 75th valuation date |

$1,000 + applicable premium = $1,000 + $816.667 = $1,816.667 |

| 76th valuation date |

$1,000 + applicable premium = $1,000 + $825.000 = $1,825.000 |

| 77th valuation date |

$1,000 + applicable premium = $1,000 + $833.333 = $1,833.333 |

| 78th valuation date |

$1,000 + applicable premium = $1,000 + $841.667 = $1,841.667 |

| 79th valuation date |

$1,000 + applicable premium = $1,000 + $850.000 = $1,850.000 |

| 80th valuation date |

$1,000 + applicable premium = $1,000 + $858.333 = $1,858.333 |

| 81st valuation date |

$1,000 + applicable premium = $1,000 + $866.667 = $1,866.667 |

| 82nd valuation date |

$1,000 + applicable premium = $1,000 + $875.000 = $1,875.000 |

| 83rd valuation date |

$1,000 + applicable premium = $1,000 + $883.333 = $1,883.333 |

| 84th valuation date |

$1,000 + applicable premium = $1,000 + $891.667 = $1,891.667 |

| 85th valuation date |

$1,000 + applicable premium = $1,000 + $900.000 = $1,900.000 |

| 86th valuation date |

$1,000 + applicable premium = $1,000 + $908.333 = $1,908.333 |

| 87th valuation date |

$1,000 + applicable premium = $1,000 + $916.667 = $1,916.667 |

| 88th valuation date |

$1,000 + applicable premium = $1,000 + $925.000 = $1,925.000 |

| 89th valuation date |

$1,000 + applicable premium = $1,000 + $933.333 = $1,933.333 |

| 90th valuation date |

$1,000 + applicable premium = $1,000 + $941.667 = $1,941.667 |

| 91st valuation date |

$1,000 + applicable premium = $1,000 + $950.000 = $1,950.000 |

| 92nd valuation date |

$1,000 + applicable premium = $1,000 + $958.333 = $1,958.333 |

| 93rd valuation date |

$1,000 + applicable premium = $1,000 + $966.667 = $1,966.667 |

| 94th valuation date |

$1,000 + applicable premium = $1,000 + $975.000 = $1,975.000 |

| 95th valuation date |

$1,000 + applicable premium = $1,000 + $983.333 = $1,983.333 |

| 96th valuation date |

$1,000 + applicable premium = $1,000 + $991.667 = $1,991.667 |

If, on any valuation date prior to the final valuation date, the

closing value of the underlying is less than the initial underlying value, you will not receive the premium indicated above following

that valuation date. In order to receive the premium indicated above, the closing value of the underlying on the applicable valuation

date must be greater than or equal to the initial underlying value.

| Citigroup Global Markets Holdings Inc. |

| |

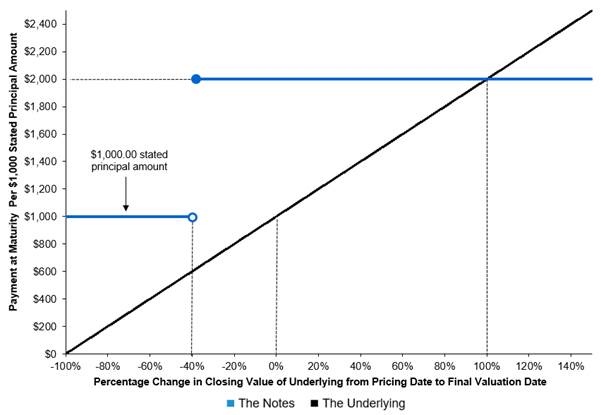

Payment at Maturity Diagram

The diagram below illustrates your payment at maturity of the notes,

assuming the notes have not previously been automatically redeemed, for a range of hypothetical underlying performance.

Investors in the notes will not receive any dividends with respect

to the underlying. The diagram and examples below do not show any effect of lost dividend yield over the term of the notes. See “Summary

Risk Factors—You will not receive dividends or have any other rights with respect to the underlying” below.

Market-Linked Notes

Payment at Maturity Diagram |

|

| Citigroup Global Markets Holdings Inc. |

| |

Hypothetical Examples of the Payment at Maturity

The examples below are intended to illustrate how, if the notes are

not automatically redeemed prior to maturity, your payment at maturity will depend on the final underlying value. Your actual payment

at maturity per note, if the notes are not automatically redeemed prior to maturity, will depend on the actual final underlying value.

The examples are solely for illustrative purposes, do not show all possible outcomes and are not a prediction of any payment that may

be made on the notes.

The examples below are based on a hypothetical initial underlying value

of 100 and a hypothetical final premium threshold value of 60 and do not reflect the actual initial underlying value or final premium

threshold value. For the actual initial underlying value and final premium threshold value, see the cover page of this pricing supplement.

We have used this hypothetical value, rather than the actual value, to simplify the calculations and aid understanding of how the notes

work. However, you should understand that the actual payment at maturity on the notes will be calculated based on the actual initial underlying

value and final premium threshold value and not the hypothetical values. For ease of analysis, figures below have been rounded.

Example 1—Upside Scenario A. The final underlying value

is 110.00 (a 10% increase from the initial underlying value), which is greater than or equal to the final premium threshold value.

Payment at maturity per note = $1,000 + the premium applicable to the

final valuation date

= $1,000 + $1,000.00

= $2,000.00

In this scenario, because the final underlying value is greater than

or equal to the final premium threshold value, you would be repaid the stated principal amount of your notes at maturity plus the

premium applicable to the final valuation date.

Example 2—Upside Scenario B. The final underlying value

is 80.00 (a 20% decrease from the initial underlying value), which is greater than or equal to the final premium threshold value.

Payment at maturity per note = $1,000 + the premium applicable to the

final valuation date

= $1,000 + $1,000.00

= $2,000.00

In this scenario, because the final underlying value is greater than

or equal to the final premium threshold value, you would be repaid the stated principal amount of your notes at maturity plus the

premium applicable to the final valuation date.

Example 2—Par Scenario. The final underlying value is 50.00

(a 50% decrease from the initial underlying value), which is less than the final premium threshold value.

Payment at maturity per note = $1,000

In this scenario, because the underlying has depreciated from the initial

underlying value to the final underlying value and is less than the final premium threshold value, you would be repaid the stated principal

amount of your notes at maturity but you would not receive any positive return on your investment.

| Citigroup Global Markets Holdings Inc. |

| |

Summary Risk Factors

An investment in the notes is significantly riskier than an investment

in conventional debt securities. The notes are subject to all of the risks associated with an investment in our conventional debt securities

(guaranteed by Citigroup Inc.), including the risk that we and Citigroup Inc. may default on our obligations under the notes, and are

also subject to risks associated with the underlying. Accordingly, the notes are suitable only for investors who are capable of understanding

the complexities and risks of the notes. You should consult your own financial, tax and legal advisors as to the risks of an investment

in the notes and the suitability of the notes in light of your particular circumstances.

The following is a summary of certain key risk factors for investors

in the notes. You should read this summary together with the more detailed description of risks relating to an investment in the notes

contained in the section “Risk Factors Relating to the Notes” beginning on page EA-6 in the accompanying product supplement.

You should also carefully read the risk factors included in the accompanying prospectus supplement and in the documents incorporated by

reference in the accompanying prospectus, including Citigroup Inc.’s most recent Annual Report on Form 10-K and any subsequent Quarterly

Reports on Form 10-Q, which describe risks relating to the business of Citigroup Inc. more generally.

Risks relating to the notes

| § | You may not receive any return on your investment in the notes. If, on each valuation date prior to the final valuation date,

the closing value of the underlying is not greater than or equal to the initial underlying value, then the notes will not be automatically

redeemed at a premium. In that event, you will receive a positive return on your investment in the notes only if the final

underlying value is greater than or equal to the final premium threshold value. If the final underlying value is less than the final premium

threshold value, you will receive only the stated principal amount of $1,000 for each note you hold at maturity. |

| § | The notes are riskier than notes with a shorter term. The notes are relatively long-dated. Because the

notes are relatively long-dated, many of the risks of the notes are heightened as compared to notes with a shorter term, because you will

be subject to those risks for a longer period of time. In addition, the value of a longer-dated note is typically less than

the value of an otherwise comparable note with a shorter term. |

| § | The notes do not pay interest. Unlike conventional debt securities, the notes do not pay interest prior to maturity. You should

not invest in the notes if you seek current income during the term of the notes. |

| § | Your potential return on the notes is limited. Your potential return on the notes is limited to the applicable premium payable

upon automatic early redemption or at maturity, as described on the cover page of this pricing supplement. If the closing value of the

underlying on one of the valuation dates prior to the final valuation date is greater than or equal to the initial underlying value, or

if the final underlying value is greater than or equal to the final premium threshold value, you will be repaid the stated principal amount

of your notes and will receive the fixed premium applicable to that valuation date, regardless of how significantly the closing value

of the underlying on that valuation date may exceed the initial underlying value. Accordingly, any premium may result in a return on the

notes that is significantly less than the return you could have achieved on a direct investment in the underlying. |

| § | The notes may be automatically redeemed prior to maturity, limiting the term of the notes. If the closing value of the underlying

on any valuation date prior to the final valuation date is greater than or equal to the initial underlying value, the notes will be automatically

redeemed. If the notes are automatically redeemed following any valuation date prior to the final valuation date, they will cease to be

outstanding and you will not receive the premium applicable to any later valuation date. Moreover, you may not be able to reinvest your

funds in another investment that provides a similar yield with a similar level of risk. |

| § | Although the notes provide for the repayment of the stated principal amount at maturity, you may nevertheless suffer a loss on

your investment in real value terms. This is because inflation may cause the real value of the stated principal amount to be less

at maturity than it is at the time you invest, and because an investment in the notes represents a forgone opportunity to invest in an

alternative asset that does generate a positive real return. This potential loss in real value terms is significant given the term of

the notes. You should carefully consider whether an investment that may not provide for any return on your investment, or may provide

a return that is lower than the return on alternative investments, is appropriate for you. |

| § | The performance of the notes will depend on the closing values of the underlying solely on the valuation dates, which makes the

notes particularly sensitive to volatility in the closing values of the underlying on or near the valuation dates. Whether the notes

will be automatically redeemed prior to maturity will depend on the closing values of the underlying solely on the valuation dates (other

than the final valuation date), regardless of the closing values of the underlying on other days during the term of the notes. If the

notes are not automatically redeemed prior to maturity, what you receive at maturity will depend solely on the closing value of the underlying

on the final valuation date, and not on any other day during the term of the notes. Because the performance of the notes depends on the

closing values of the underlying on a limited number of dates, the notes will be particularly sensitive to volatility in the closing values

of the underlying on or near the valuation dates. You should understand that the closing value of the underlying has historically been

highly volatile. |

| § | The notes are subject to the credit risk of Citigroup Global Markets Holdings Inc. and Citigroup Inc. If we default on our

obligations under the notes and Citigroup Inc. defaults on its guarantee obligations, you may not receive anything owed to you under the

notes. |

| § | The notes will not be listed on any securities exchange and you may not be able to sell them prior to maturity. The notes will

not be listed on any securities exchange. Therefore, there may be little or no secondary market for the notes. CGMI currently intends

to make a secondary market in relation to the notes and to provide an indicative bid price for the notes on a daily basis. Any indicative

bid price for the notes provided by CGMI will be determined in CGMI’s sole discretion, taking into account prevailing market conditions

and other relevant factors, and will not be a representation by CGMI that the notes can be sold at that price, or at all. CGMI may suspend

or terminate making a market and providing indicative bid prices without notice, at any time and for any reason. If CGMI suspends or |

| Citigroup Global Markets Holdings Inc. |

| |

terminates making a market, there may be

no secondary market at all for the notes because it is likely that CGMI will be the only broker-dealer that is willing to buy your notes

prior to maturity. Accordingly, an investor must be prepared to hold the notes until maturity.

| § | Sale of the notes prior to maturity may result in a loss of principal. You will be entitled to receive at least the full stated

principal amount of your notes, subject to the credit risk of Citigroup Global Markets Holdings Inc. and Citigroup Inc., only if you hold

the notes to maturity. The value of the notes may fluctuate during the term of the notes, and if you are able to sell your notes prior

to maturity, you may receive less than the full stated principal amount of your notes. |

| § | The estimated value of the notes on the pricing date, based on CGMI’s proprietary pricing models and our internal funding

rate, is less than the issue price. The difference is attributable to certain costs associated with selling, structuring and hedging

the notes that are included in the issue price. These costs include (i) any selling concessions or other fees paid in connection with

the offering of the notes, (ii) hedging and other costs incurred by us and our affiliates in connection with the offering of the notes

and (iii) the expected profit (which may be more or less than actual profit) to CGMI or other of our affiliates in connection with hedging

our obligations under the notes. These costs adversely affect the economic terms of the notes because, if they were lower, the economic

terms of the notes would be more favorable to you. The economic terms of the notes are also likely to be adversely affected by the use

of our internal funding rate, rather than our secondary market rate, to price the notes. See “The estimated value of the notes would

be lower if it were calculated based on our secondary market rate” below. |

| § | The estimated value of the notes was determined for us by our affiliate using proprietary pricing models. CGMI derived the

estimated value disclosed on the cover page of this pricing supplement from its proprietary pricing models. In doing so, it may have made

discretionary judgments about the inputs to its models, such as the volatility of the closing value of the underlying, dividend yields

on the stocks that constitute the underlying and interest rates. CGMI’s views on these inputs may differ from your or others’

views, and as an underwriter in this offering, CGMI’s interests may conflict with yours. Both the models and the inputs to the models

may prove to be wrong and therefore not an accurate reflection of the value of the notes. Moreover, the estimated value of the notes set

forth on the cover page of this pricing supplement may differ from the value that we or our affiliates may determine for the notes for

other purposes, including for accounting purposes. You should not invest in the notes because of the estimated value of the notes. Instead,

you should be willing to hold the notes to maturity irrespective of the initial estimated value. |

| § | The estimated value of the notes would be lower if it were calculated based on our secondary market rate. The estimated value

of the notes included in this pricing supplement is calculated based on our internal funding rate, which is the rate at which we are willing

to borrow funds through the issuance of the notes. Our internal funding rate is generally lower than our secondary market rate, which

is the rate that CGMI will use in determining the value of the notes for purposes of any purchases of the notes from you in the secondary

market. If the estimated value included in this pricing supplement were based on our secondary market rate, rather than our internal funding

rate, it would likely be lower. We determine our internal funding rate based on factors such as the costs associated with the notes, which

are generally higher than the costs associated with conventional debt securities, and our liquidity needs and preferences. Our internal

funding rate is not an interest rate that we will pay to investors in the notes, which do not bear interest. |

Because there is not an active market for traded instruments

referencing our outstanding debt obligations, CGMI determines our secondary market rate based on the market price of traded instruments

referencing the debt obligations of Citigroup Inc., our parent company and the guarantor of all payments due on the notes, but subject

to adjustments that CGMI makes in its sole discretion. As a result, our secondary market rate is not a market-determined measure of our

creditworthiness, but rather reflects the market’s perception of our parent company’s creditworthiness as adjusted for discretionary

factors such as CGMI’s preferences with respect to purchasing the notes prior to maturity.

| § | The estimated value of the notes is not an indication of the price, if any, at which CGMI or any other person may be willing to

buy the notes from you in the secondary market. Any such secondary market price will fluctuate over the term of the notes based on

the market and other factors described in the next risk factor. Moreover, unlike the estimated value included in this pricing supplement,

any value of the notes determined for purposes of a secondary market transaction will be based on our secondary market rate, which will

likely result in a lower value for the notes than if our internal funding rate were used. In addition, any secondary market price for

the notes will be reduced by a bid-ask spread, which may vary depending on the aggregate stated principal amount of the notes to be purchased

in the secondary market transaction, and the expected cost of unwinding related hedging transactions. As a result, it is likely that any

secondary market price for the notes will be less than the issue price. |

| § | The value of the notes prior to maturity will fluctuate based on many unpredictable factors. The value of your notes prior

to maturity will fluctuate based on the closing value of the underlying, the volatility of the closing value of the underlying, dividend

yields on the stocks that constitute the underlying, interest rates generally, the time remaining to maturity and our and Citigroup Inc.’s

creditworthiness, as reflected in our secondary market rate, among other factors described under “Risk Factors Relating to the Notes—Risk

Factors Relating to All Notes—The value of your notes prior to maturity will fluctuate based on many unpredictable factors”

in the accompanying product supplement. Changes in the closing value of the underlying may not result in a comparable change in the value

of your notes. You should understand that the value of your notes at any time prior to maturity may be significantly less than the issue

price. |

| § | Immediately following issuance, any secondary market bid price provided by CGMI, and the value that will be indicated on any brokerage

account statements prepared by CGMI or its affiliates, will reflect a temporary upward adjustment. The amount of this temporary upward

adjustment will steadily decline to zero over the temporary adjustment period. See “Valuation of the Notes” in this pricing

supplement. |

| § | Our offering of the notes is not a recommendation of the underlying. The fact that we are offering the notes does not mean

that we believe that investing in an instrument linked to the underlying is likely to achieve favorable returns. In fact, as we are part

of a global financial institution, our affiliates may have positions (including short positions) in the stocks that constitute the underlying

or in instruments related to the underlying or such stocks, and may publish research or express opinions, that in each case are inconsistent |

| Citigroup Global Markets Holdings Inc. |

| |

with an investment linked to the underlying.

These and other activities of our affiliates may affect the closing value of the underlying in a way that negatively affects the value

of and your return on the notes.

| § | The closing value of the underlying may be adversely affected by our or our affiliates’ hedging and other trading activities.

We expect to hedge our obligations under the notes through CGMI or other of our affiliates, who may take positions in the underlying or

in financial instruments related to the underlying and may adjust such positions during the term of the notes. Our affiliates also take

positions in the underlying or in financial instruments related to the underlying on a regular basis (taking long or short positions or

both), for their accounts, for other accounts under their management or to facilitate transactions on behalf of customers. These activities

could affect the closing value of the underlying in a way that negatively affects the value of and your return on the notes. They could

also result in substantial returns for us or our affiliates while the value of the notes declines. |

| § | We and our affiliates may have economic interests that are adverse to yours as a result of our affiliates’ business activities.

Our affiliates engage in business activities with a wide range of companies. These activities include extending loans, making and facilitating

investments, underwriting securities offerings and providing advisory services. These activities could involve or affect the underlying

in a way that negatively affects the value of and your return on the notes. They could also result in substantial returns for us or our

affiliates while the value of the notes declines. In addition, in the course of this business, we or our affiliates may acquire non-public

information, which will not be disclosed to you. |

| § | The calculation agent, which is an affiliate of ours, will make important determinations with respect to the notes. If certain

events occur during the term of the notes, such as market disruption events and other events with respect to the underlying, CGMI, as

calculation agent, will be required to make discretionary judgments that could significantly affect your return on the notes. In making

these judgments, the calculation agent’s interests as an affiliate of ours could be adverse to your interests as a holder of the

notes. See “Risk Factors Relating to the Notes—Risk Factors Relating to All Notes—The calculation agent, which is an

affiliate of ours, will make important determinations with respect to the notes” in the accompanying product supplement. |

Risks relating to the S&P 500

Futures 35% Edge Volatility 6% Decrement Index (USD) ER

The following discussion of risks relating

to the S&P 500 Futures 35% Edge Volatility 6% Decrement Index (USD) ER, which we refer to in this section as the “Index”,

should be read together with the description of the Index in Annex A to this pricing supplement, which defines and further describes a

number of the terms and concepts referred to in this section.

| § | The Index is highly risky because it may reflect highly leveraged exposure to the Underlying Futures Index and may therefore experience

a decline that is many multiples of any decline in the Underlying Futures Index. The Index tracks exposure to the S&P

500 Futures Excess Return Index (which we refer to as the “Underlying Futures Index”) on a volatility targeted basis,

less a decrement of 6% per annum. The Index has a volatility target of 35%, which it attempts to achieve by applying leverage

to its exposure to the Underlying Futures Index (up to a maximum of 500%) when the implied volatility of the S&P 500®

Index is less than the volatility target, and by reducing its exposure to the Underlying Futures Index below 100% when the implied volatility

of the S&P 500® Index is greater than the volatility target. It is expected that the implied volatility

of the S&P 500® Index will frequently be less than the volatility target, and therefore it is expected that the Index

will frequently have leveraged (more than 100%) exposure to the Underlying Futures Index. If the Underlying Futures Index declines

at a time when the Index has leveraged exposure to it, the decline in the Index will be equal to the decline in the Underlying Futures

Index multiplied by the leverage (subject to further reduction as a result of the decrement). For example, if the Underlying

Futures Index declines by 5% at a time when the Index has 500% leveraged exposure to the Underlying Futures Index, the Index will decline

by 25% over that time (subject to further reduction as a result of the decrement). This potential for losses on a highly leveraged

basis makes the Index highly risky. |

| § | The Index may realize significant losses if it is not consistently successful in increasing exposure to the Underlying Futures

Index in advance of increases in the Underlying Futures Index and reducing exposure to the Underlying Futures Index in advance of declines

in the Underlying Futures Index. The Index methodology is premised on the following key assumptions: (1) that there will

be an inverse relationship between performance and volatility, so that the Underlying Futures Index will tend to increase in times of

lower volatility and decline in times of higher volatility; (2) that the implied volatility of the S&P 500® Index,

as derived from the market prices of exchange-traded options on the S&P 500® Index on each weekly rebalancing date,

will be an effective predictor of future volatility of the Underlying Futures Index over the next week; and (3) that 35% will be an effective

level of volatility at which to draw the line between leveraged exposure and deleveraged exposure to the Underlying Futures Index. There

is no guarantee that these assumptions will be proven correct over any given time period. If any of these assumptions does

not prove to be consistently correct, then the Index may perform poorly as a result of having highly leveraged exposure to the Underlying

Futures Index at a time of declines and/or having reduced exposure to the Underlying Futures Index at a time of increases. |

| § | The Index may be adversely affected by a time lag in its volatility targeting mechanism. The Index resets the leveraged

exposure of each sub-index to the Underlying Futures Index on a weekly basis. If the implied volatility of the S&P 500®

Index at the rebalancing time on the rebalancing date for a given sub-index is relatively low, that sub-index will retain relatively high

leveraged exposure to the Underlying Futures Index for the next week even if the volatility of the S&P 500® Index spikes

and the Underlying Futures Index declines significantly in value immediately after the rebalancing time on that rebalancing date. That

sub-index may consequently have highly leveraged exposure to a week’s worth of declines in the value of the Underlying Futures Index

before it has a chance to reset its leverage. In the case of a sudden increase in volatility and a sudden decline in value,

multiple sub-indexes may have highly leveraged exposure to declines over multiple days, and the Index may experience poor performance

as a result. Conversely, if significant appreciation in the Underlying Futures Index follows closely on a period of high S&P

500® Index volatility, the time lag may cause the Index to have low exposure to the Underlying Futures Index when that

appreciation occurs. Taken together, these factors may cause the Index to perform particularly poorly in a temporary market

crash – a sudden significant decline that is quickly reversed. In that scenario, the Index would participate on a highly

leveraged basis in the decline and then fail to participate fully in the recovery. |

| Citigroup Global Markets Holdings Inc. |

| |

| § | The Index may be adversely affected by a “decay” effect. If the Index is not consistently successful

in increasing exposure to the Underlying Futures Index in advance of increases in the Underlying Futures Index and reducing exposure to

the Underlying Futures Index in advance of declines in the Underlying Futures Index, then the Index is also expected to be subject to

a “decay” effect, which will exacerbate the decline that results from having highly leveraged exposure to declines in the

Underlying Futures Index. The decay effect would result from the fact that each sub-index of the Index resets its leveraged

exposure to the Underlying Futures Index on a weekly basis, and would manifest any time the Underlying Futures Index moves in one direction

one week and another direction the next. The decay effect would result because resetting leverage after an increase but in

advance of a decline would cause the Index to have increased exposure to that decline, and resetting leverage following a decline but

in advance of an increase would cause the Index to have decreased exposure to that increase. The more this fact pattern repeats,

the lower the performance of the Index would be relative to the performance of the Underlying Futures Index. |

| § | The Underlying Futures Index is expected to underperform the S&P 500® Index because of an implicit financing

cost. The Underlying Futures Index is a futures-based index. As a futures-based index, it is expected to reflect

not only the performance of its reference index (the S&P 500® Index), but also the implicit cost of a financed position

in that reference index. The cost of this financed position will adversely affect the value of the Underlying Futures Index. Any

increase in market interest rates will be expected to further increase this implicit financing cost and will increase the negative effect

on the performance of the Underlying Futures Index. Because of this implicit financing cost, the Underlying Futures Index is

expected to underperform the total return performance of the S&P 500® Index. |

| § | The performance of the Index will be reduced by a decrement of 6% per annum. The Index is a decrement index, which

means that the value of each sub-index of the Index will be reduced at a rate of 6% per annum. The decrement will be a significant

drag on the performance of the Index, potentially offsetting positive returns that would otherwise result from the Index methodology,

exacerbating negative returns of the Index methodology and causing the level of the Index to decline steadily if the return of the Index

methodology would otherwise be relatively flat. The Index will not appreciate unless the return of the Index methodology is

sufficient to offset the negative effects of the decrement, and then only to the extent that the return of the Index methodology is greater

than the decrement. As a result of the decrement, the level of the Index may decline even if the return of the Index methodology

would otherwise have been positive. |

| § | The Index may not fully participate in any appreciation of the Underlying Futures Index. At any time when the implied

volatility of the S&P 500® Index is greater than the volatility target, the Index will have less than 100% exposure

to the Underlying Futures Index and therefore will not fully participate in any appreciation of the Underlying Futures Index. For

example, if the Index has 50% exposure to the Underlying Futures Index at a time when the Underlying Futures Index appreciates by 5%,

the Index would appreciate by only 2.5% (before giving effect to the decrement). The decrement is deducted daily at a rate of 6% per annum

even when the Index has less than 100% exposure to the Underlying Futures Index. |

| § | The Index may perform less favorably than it would if its volatility targeting mechanism were based on an alternative volatility

measure, such as actual realized volatility, rather than implied volatility. The Index attempts to achieve its volatility

target by adjusting its exposure to the Underlying Futures Index based on the implied volatility of the S&P 500® Index. Implied

volatility represents market expectations of future volatility as derived from the price of exchange-traded options on the S&P 500®

Index. Market expectations of future volatility may not accurately forecast future volatility. Accordingly, relying

on implied volatility may cause the Index to be less successful in maintaining its volatility target than it would have been if it had

relied instead on an alternative measure of volatility, such as actual realized volatility. As a result, the Index may have

lower participation in Underlying Futures Index increases, and greater participation in Underlying Futures Index declines, resulting in

less favorable overall Index performance, than it would have had if another measure of volatility had been used. |

| § | The Index may significantly underperform the S&P 500® Index. It is important to understand that

the Index provides exposure to the S&P 500® Index that: (1) may be leveraged up to 500%, or alternatively may reflect

less than 100% participation; (2) is reduced by an implicit financing cost; (3) may be subject to a decay effect; and (4) is reduced by

a decrement of 6% per annum. As a result of these features, the Index may significantly underperform the S&P 500®

Index. The Index is likely to significantly underperform the S&P 500® Index if it is not consistently successful

in increasing exposure to the Underlying Futures Index in advance of increases in the Underlying Futures Index and reducing exposure to

the Underlying Futures Index in advance of declines in the Underlying Futures Index. The Index may significantly underperform

the S&P 500® Index even if it is consistently successful in these respects because of the implicit financing cost and

the decrement, or because the reduced exposure the Index has to the Underlying Futures Index at a time of a decline may nevertheless reflect

significantly greater than 100% participation in the decline of the Underlying Futures Index. |

| § | The Index has limited actual performance information. The Index launched on May 10, 2024. Accordingly,

the Index has limited actual performance data. Because the Index is of recent origin with limited performance history, an investment

linked to the Index may involve a greater risk than an investment linked to one or more indices with an established record of performance. A

longer history of actual performance may have provided more reliable information on which to assess the validity of the Index’s

methodology. However, any historical performance of the Index is not an indication of how the Index will perform in the future. |

| § | Hypothetical back-tested Index performance information is subject to significant limitations. All information regarding

the performance of the Index prior to May 10, 2024 is hypothetical and back-tested, as the Index did not exist prior to that time. It

is important to understand that hypothetical back-tested Index performance information is subject to significant limitations, in addition

to the fact that past performance is never a guarantee of future performance. In particular: |

| o | The sponsor of the Index developed the rules of the Index with the benefit of hindsight—that is, with the benefit of being able

to evaluate how the Index rules would have caused the Index to perform had it existed during the hypothetical back-tested period. The

fact that the Index generally appreciated over any portion of the hypothetical back-tested period may not therefore be an accurate or

reliable indication of any fundamental aspect of the Index methodology. |

| Citigroup Global Markets Holdings Inc. |

| |

| o | The hypothetical back-tested performance of the Index might look different if it covered a different historical period. The

market conditions that existed during the historical period covered by the hypothetical back-tested Index performance information are

not necessarily representative of the market conditions that will exist in the future. |

| o | SPXW options were not published as frequently prior to May 11, 2022 as they are now, and as a result the calculation of the hypothetical

back-tested values of the Index prior to that date differs from the calculation of the Index today. The hypothetical back-tested

performance of the Index prior to May 11, 2022 may therefore differ from how the Index would have performed if SPXW options had been available

with expirations on every weekday, as they are now. |

It is impossible to predict whether the

Index will rise or fall. The actual future performance of the Index may bear no relation to the historical or hypothetical back-tested

levels of the Index.

| § | An affiliate of ours participated in the development of the Index. CGMI worked with the sponsor of the Index in

developing the guidelines and policies governing the composition and calculation of the Index, and in that role made judgments and determinations

about the Index methodology. Although CGMI no longer has a role in making any judgments and determinations relating to the

Index, the judgments and determinations previously made by CGMI could continue to have an impact, positive or negative, on the level of

the Index and the value of your notes. CGMI was under no obligation to consider your interests as an investor in the notes

in its role in developing the guidelines and policies governing the Index. |

| § | Changes that affect the Index may affect the value of your notes. The sponsor of the Index may at any time make

methodological changes or other changes in the manner in which it operates that could affect the value of the Index. We are

not affiliated with the Index sponsor and, accordingly, we have no control over any changes such sponsor may make. Such changes

could adversely affect the performance of the Index and the value of and your return on the notes. |

| Citigroup Global Markets Holdings Inc. |

| |

Additional Terms of the Notes

Market disruption events. For purposes of determining whether

a market disruption event occurs with respect to the S&P 500 Futures 35% Edge Volatility 6% Decrement Index (USD) ER, each reference

to the “Underlying Index” in the section “Description of the Notes—Certain Additional Terms for Notes Linked to

an Underlying Index—Consequences of a Market Disruption Event; Postponement of a Valuation Date” in the accompanying product

supplement shall be deemed replaced with a reference to the “Underlying Index, the S&P 500 Futures Excess Return Index or the

S&P 500® Index”. References in the section “Description of the Notes—Certain Additional

Terms for Notes Linked to an Underlying Index—Consequences of a Market Disruption Event; Postponement of a Valuation Date”

in the accompanying product supplement to the securities comprising an Underlying Index shall be deemed to include futures contracts comprising

an Underlying Index.

| Citigroup Global Markets Holdings Inc. |

| |

Information About the S&P 500 Futures 35% Edge Volatility

6% Decrement Index (USD) ER

For information about the S&P 500 Futures 35% Edge Volatility 6%

Decrement Index (USD) ER, see Annex A to this pricing supplement.

Hypothetical Back-tested and Historical Performance Information

This section contains hypothetical back-tested performance information

for the S&P 500 Futures 35% Edge Volatility 6% Decrement Index (USD) ER calculated by S&P Dow Jones Indices LLC. All

S&P 500 Futures 35% Edge Volatility 6% Decrement Index (USD) ER performance information prior to May 10, 2024 is hypothetical and

back-tested, as the S&P 500 Futures 35% Edge Volatility 6% Decrement Index (USD) ER did not exist prior to that date. Hypothetical

back-tested performance information is subject to significant limitations. The sponsor of the S&P 500 Futures 35% Edge

Volatility 6% Decrement Index (USD) ER developed the rules of the index with the benefit of hindsight—that is, with the benefit

of being able to evaluate how the rules would have caused the S&P 500 Futures 35% Edge Volatility 6% Decrement Index (USD) ER to perform

had it existed during the hypothetical back-tested period. The fact that the S&P 500 Futures 35% Edge Volatility 6% Decrement

Index (USD) ER appreciated at any time during the hypothetical back-tested period may not therefore be an accurate or reliable indication

of any fundamental aspect of the index methodology. Furthermore, the hypothetical back-tested performance of the S&P 500

Futures 35% Edge Volatility 6% Decrement Index (USD) ER might look different if it covered a different historical period. The

market conditions that existed during the hypothetical back-tested period may not be representative of market conditions that will exist

in the future.

In addition, the SPXW options used by the S&P 500 Futures 35% Edge

Volatility 6% Decrement Index (USD) ER to determine the implied volatility of the S&P 500® Index have traded with expirations

on every weekday only since May 11, 2022. When SPXW options were first launched in 2005, only Friday expirations were available. Wednesday

expirations were added on February 23, 2016; Monday expirations were added on August 15, 2016; Tuesday expirations were added on April

18, 2022; and Thursday expirations were added on May 11, 2022. For purposes of calculating the hypothetical back-tested performance

of the Index, the implied volatility for the one-week period ending on a weekday for which no SPXW option was then traded was calculated

by interpolating between the SPXW options expiring immediately before and immediately after that weekday. In addition, on September

30, 2016, due to data availability, the closing level of the S&P 500 Futures Excess Return Index on that day was used in lieu of its

time-weighted average value. For these reasons, the hypothetical back-tested performance of the S&P 500 Futures 35% Edge

Volatility 6% Decrement Index (USD) ER prior to May 11, 2022 may differ from how the S&P 500 Futures 35% Edge Volatility 6% Decrement

Index (USD) ER would have performed if SPXW options had been available with expirations on every weekday, as they are now, and if the

time-weighted average value of the S&P 500 Futures Excess Return Index had been available on September 30, 2016.

It is impossible to predict whether the S&P 500 Futures 35% Edge

Volatility 6% Decrement Index (USD) ER will rise or fall. By providing the hypothetical back-tested and historical performance

information below, we are not representing that the S&P 500 Futures 35% Edge Volatility 6% Decrement Index (USD) ER is likely to achieve

gains or losses similar to those shown. In fact, there are frequently sharp differences between hypothetical performance results

and the actual results subsequently achieved by any particular investment. One of the limitations of hypothetical performance

information is that it did not involve financial risk and cannot account for all factors that would affect actual performance. The

actual future performance of the S&P 500 Futures 35% Edge Volatility 6% Decrement Index (USD) ER may bear no relation to its hypothetical

back-tested or historical performance.

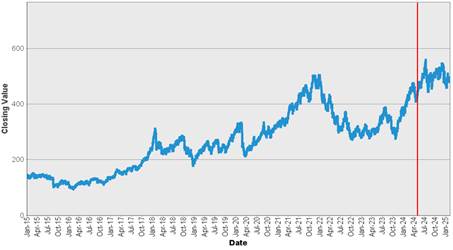

Historical Information

The closing value of the S&P 500 Futures 35% Edge Volatility 6%

Decrement Index (USD) ER on February 11, 2025 was 492.4821. The graph below shows the hypothetical back-tested closing values of the S&P

500 Futures 35% Edge Volatility 6% Decrement Index (USD) ER for the period from January 2, 2015 to May 9, 2024, and historical closing

values of the S&P 500 Futures 35% Edge Volatility 6% Decrement Index (USD) ER for the period from May 10, 2024 to February 11, 2025. All

data to the left of the vertical red line in the graph below are hypothetical and back-tested. We obtained the closing values

from Bloomberg L.P., without independent verification. You should not take the hypothetical back-tested and historical values

of the S&P 500 Futures 35% Edge Volatility 6% Decrement Index (USD) ER as an indication of future performance.

S&P 500 Futures 35% Edge Volatility 6% Decrement Index (USD) ER – Hypothetical Back-Tested and Historical Closing Values

January 2, 2015 to February 11, 2025 |

|

| Citigroup Global Markets Holdings Inc. |

| |

United States Federal Tax Considerations

In the opinion of our counsel, Davis Polk & Wardwell LLP, which

is based on current market conditions, the notes should be treated as “contingent payment debt instruments” for U.S. federal

income tax purposes, as described in the section of the accompanying product supplement called “United States Federal Tax Considerations—Tax

Consequences to U.S. Holders—Notes Treated as Contingent Payment Debt Instruments,” and the remaining discussion is based

on this treatment.

If you are a U.S. Holder (as defined in the accompanying product supplement),

you will be required to recognize interest income during the term of the notes at the “comparable yield,” which generally

is the yield at which we could issue a fixed-rate debt instrument with terms similar to those of the notes, including the level of subordination,

term, timing of payments and general market conditions, but excluding any adjustments for the riskiness of the contingencies or the liquidity

of the notes. Although it is not clear how the comparable yield should be determined for notes that may be automatically redeemed

before maturity, our determination of the comparable yield is based on the maturity date. We are required to construct a “projected

payment schedule” in respect of the notes representing a payment the amount and timing of which would produce a yield to maturity

on the notes equal to the comparable yield. Assuming you hold the notes until their maturity, the amount of interest you include

in income based on the comparable yield in the taxable year in which the notes mature will be adjusted upward or downward to reflect the

difference, if any, between the actual and projected payment on the notes at maturity as determined under the projected payment schedule.

Upon the sale, exchange or retirement of the notes prior to maturity,

you generally will recognize gain or loss equal to the difference between the proceeds received and your adjusted tax basis in the notes. Your

adjusted tax basis will equal your purchase price for the notes, increased by interest previously included in income on the notes. Any

gain generally will be treated as ordinary income, and any loss generally will be treated as ordinary loss to the extent of prior interest

inclusions on the note and as capital loss thereafter.

We have determined that the comparable yield for a note is a rate of %,

compounded semi-annually, and that the projected payment schedule with respect to a note consists of a single payment of $ at

maturity.

Neither the comparable yield nor the projected payment schedule constitutes

a representation by us regarding the actual amount that we will pay on the notes.

Non-U.S. Holders. Subject to the discussions below regarding

Section 871(m) and in “United States Federal Tax Considerations—Tax Consequences to Non-U.S. Holders” and “—FATCA”

in the accompanying product supplement, if you are a Non-U.S. Holder (as defined in the accompanying product supplement) of the notes,

under current law you generally will not be subject to U.S. federal withholding or income tax in respect of any payment on or any amount

received on the sale, exchange or retirement of the notes, provided that (i) income in respect of the notes is not effectively connected

with your conduct of a trade or business in the United States, and (ii) you comply with the applicable certification requirements. See

“United States Federal Tax Considerations—Tax Consequences to Non-U.S. Holders” in the accompanying product supplement

for a more detailed discussion of the rules applicable to Non-U.S. Holders of the notes.

As discussed under “United States Federal Tax Considerations—Tax

Consequences to Non-U.S. Holders—Dividend Equivalents Under Section 871(m) of the Code” in the accompanying product supplement,

Section 871(m) of the Internal Revenue Code of 1986, as amended, and Treasury regulations promulgated thereunder (“Section 871(m)”)

generally impose a 30% withholding tax on dividend equivalents paid or deemed paid to Non-U.S. Holders with respect to certain financial

instruments linked to U.S. equities (“Underlying Securities”) or indices that include Underlying Securities. Section