| 29

Reconciliation of Non

-GAAP Disclosures

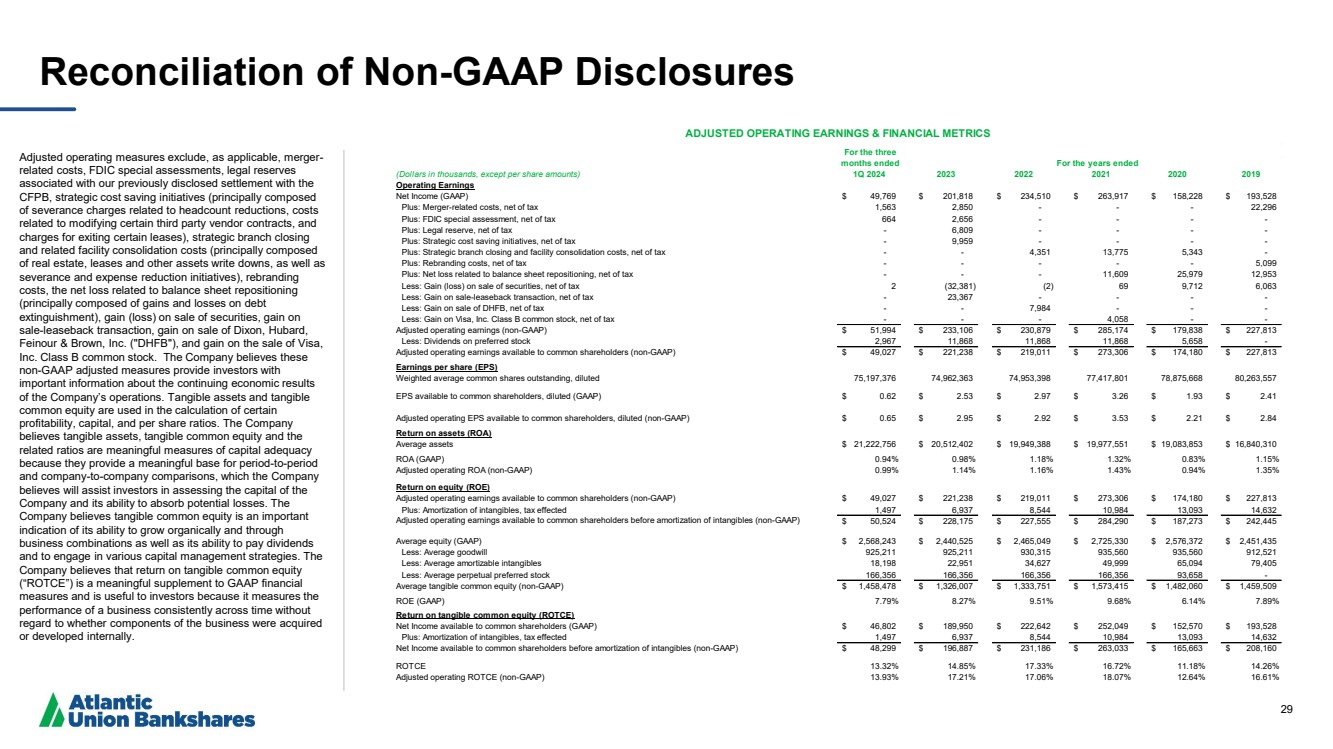

Adjusted operating measures exclude, as applicable, merger

-

related costs, FDIC special assessments, legal reserves

associated with our previously disclosed settlement with the

CFPB, strategic cost saving initiatives (principally composed

of severance charges related to headcount reductions, costs

related to modifying certain third party vendor contracts, and

charges for exiting certain leases), strategic branch closing

and related facility consolidation costs (principally composed

of real estate, leases and other assets write downs, as well as

severance and expense reduction initiatives), rebranding

costs, the net loss related to balance sheet repositioning

(principally composed of gains and losses on debt

extinguishment), gain (loss) on sale of securities, gain on

sale

-leaseback transaction, gain on sale of Dixon, Hubard,

Feinour & Brown, Inc. ("DHFB"), and gain on the sale of Visa,

Inc. Class B common stock. The Company believes these

non

-GAAP adjusted measures provide investors with

important information about the continuing economic results

of the Company’s operations. Tangible assets and tangible

common equity are used in the calculation of certain

profitability, capital, and per share ratios. The Company

believes tangible assets, tangible common equity and the

related ratios are meaningful measures of capital adequacy

because they provide a meaningful base for period

-to

-period

and company

-to

-company comparisons, which the Company

believes will assist investors in assessing the capital of the

Company and its ability to absorb potential losses. The

Company believes tangible common equity is an important

indication of its ability to grow organically and through

business combinations as well as its ability to pay dividends

and to engage in various capital management strategies. The

Company believes that return on tangible common equity

(“ROTCE”) is a meaningful supplement to GAAP financial

measures and is useful to investors because it measures the

performance of a business consistently across time without

regard to whether components of the business were acquired

or developed internally.

(Dollars in thousands, except per share amounts) 1Q 2024 2023 2022 2021 2020 2019

Operating Earnings

Net Income (GAAP) $ 49,769 $ 201,818 $ 234,510 $ 263,917 $ 158,228 $ 193,528

Plus: Merger-related costs, net of tax 1,563 2,850 - - - 22,296

Plus: FDIC special assessment, net of tax 664 2,656 - - - -

Plus: Legal reserve, net of tax - 6,809 - - - -

Plus: Strategic cost saving initiatives, net of tax - 9,959 - - - -

Plus: Strategic branch closing and facility consolidation costs, net of tax - - 4,351 13,775 5,343 -

Plus: Rebranding costs, net of tax - - - - - 5,099

Plus: Net loss related to balance sheet repositioning, net of tax - - - 11,609 25,979 12,953

Less: Gain (loss) on sale of securities, net of tax 2 (32,381) (2) 69 9,712 6,063

Less: Gain on sale-leaseback transaction, net of tax - 23,367 - - - -

Less: Gain on sale of DHFB, net of tax - - 7,984 - - -

Less: Gain on Visa, Inc. Class B common stock, net of tax - - - 4,058 - -

Adjusted operating earnings (non-GAAP) $ 51,994 $ 233,106 $ 230,879 $ 285,174 $ 179,838 $ 227,813

Less: Dividends on preferred stock 2,967 11,868 11,868 11,868 5,658 -

Adjusted operating earnings available to common shareholders (non-GAAP) $ 49,027 $ 221,238 $ 219,011 $ 273,306 $ 174,180 $ 227,813

Earnings per share (EPS)

Weighted average common shares outstanding, diluted 75,197,376 74,962,363 74,953,398 77,417,801 78,875,668 80,263,557

EPS available to common shareholders, diluted (GAAP) $ 0.62 $ 2.53 $ 2.97 $ 3.26 $ 1.93 $ 2.41

Adjusted operating EPS available to common shareholders, diluted (non-GAAP) $ 0.65 $ 2.95 $ 2.92 $ 3.53 $ 2.21 $ 2.84

Return on assets (ROA)

Average assets $ 21,222,756 $ 20,512,402 $ 19,949,388 $ 19,977,551 $ 19,083,853 $ 16,840,310

ROA (GAAP) 0.94% 0.98% 1.18% 1.32% 0.83% 1.15%

Adjusted operating ROA (non-GAAP) 0.99% 1.14% 1.16% 1.43% 0.94% 1.35%

Return on equity (ROE)

Adjusted operating earnings available to common shareholders (non-GAAP) $ 49,027 $ 221,238 $ 219,011 $ 273,306 $ 174,180 $ 227,813

Plus: Amortization of intangibles, tax effected 1,497 6,937 8,544 10,984 13,093 14,632

Adjusted operating earnings available to common shareholders before amortization of intangibles (non-GAAP) $ 50,524 $ 228,175 $ 227,555 $ 284,290 $ 187,273 $ 242,445

Average equity (GAAP) $ 2,568,243 $ 2,440,525 $ 2,465,049 $ 2,725,330 $ 2,576,372 $ 2,451,435

Less: Average goodwill 925,211 925,211 930,315 935,560 935,560 912,521

Less: Average amortizable intangibles 18,198 22,951 34,627 49,999 65,094 79,405

Less: Average perpetual preferred stock 166,356 166,356 166,356 166,356 93,658 -

Average tangible common equity (non-GAAP) $ 1,458,478 $ 1,326,007 $ 1,333,751 $ 1,573,415 $ 1,482,060 $ 1,459,509

ROE (GAAP) 7.79% 8.27% 9.51% 9.68% 6.14% 7.89%

Return on tangible common equity (ROTCE)

Net Income available to common shareholders (GAAP) $ 46,802 $ 189,950 $ 222,642 $ 252,049 $ 152,570 $ 193,528

Plus: Amortization of intangibles, tax effected 1,497 6,937 8,544 10,984 13,093 14,632

Net Income available to common shareholders before amortization of intangibles (non-GAAP) $ 48,299 $ 196,887 $ 231,186 $ 263,033 $ 165,663 $ 208,160

ROTCE 13.32% 14.85% 17.33% 16.72% 11.18% 14.26%

Adjusted operating ROTCE (non-GAAP) 13.93% 17.21% 17.06% 18.07% 12.64% 16.61%

For the years ended

ADJUSTED OPERATING EARNINGS & FINANCIAL METRICS

For the three

months ended |