As filed with the Securities and Exchange

Commission on February 21, 2025

Registration No. 333-276254

UNITED

STATES

SECURITIES

AND EXCHANGE COMMISSION

WASHINGTON,

D.C. 20549

POST-EFFECTIVE AMENDMENT NO.1 TO

FORM

S-1

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933

Tidal Commodities

Trust I

(Registrant)

Delaware

(State or other jurisdiction of incorporation or organization)

6799

(Primary Standard Industrial Classification Code Number)

92-6468665

(I.R.S. Employer Identification No.)

c/o Tidal Investments LLC

(f/k/a Toroso Investments, LLC)

234 West Florida Street, Suite 203

Milwaukee, WI 53204

Phone: (844) 986-7700

(Address, including zip code, and telephone

number,

including area code, of Registrant’s principal executive offices)

Guillermo Trias

Chief Executive Officer

Tidal Investments LLC

234 West Florida Street, Suite 203

Milwaukee, WI 53204

Phone: (844) 986-7700

(Name, address, including zip code, and

telephone number,

including area code, of agent for service)

Copy to:

Michael Pellegrino

Tidal Investments LLC

234 West Florida Street, Suite 203

Milwaukee, WI 53204

(844) 986-7700

Eric D. Simanek

Eversheds Sutherland (US) LLP

700 Sixth Street, N.W.

Washington, D.C. 2001

(202) 220-8412

Approximate date of commencement of proposed sale to the public:

As soon as practicable after the effective date of this Registration Statement.

If any of the securities being registered

on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the

following box. ☒

If this Form is filed to register additional

securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act

registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment

filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement

number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment

filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement

number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant

is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company.

See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,”

and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ☐ |

Accelerated filer ☐ |

| Non-accelerated filer ☒ |

Smaller reporting company ☒ |

| |

Emerging growth company ☒ |

If an emerging growth company, indicate

by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial

accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

The Registrant hereby amends this Registration Statement

on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which

specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities

Act or until this Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section

8(a), may determine.

Hashdex

Bitcoin ETF

Hashdex

Bitcoin ETF (f/k/a Hashdex Bitcoin Futures ETF, the “Fund” or “DEFI”) is designed to provide investors

with price exposure to the bitcoin market. The Fund issues shares (“Shares”) that trade on NYSE Arca stock exchange

(“NYSE Arca”) under the symbol “DEFI”. Shares can be purchased and sold by investors through their broker-dealer.

Under its current investment objective, the Fund may hold bitcoin and bitcoin futures contracts. Purchasing Shares of the Fund

is subject to the risks of bitcoin as well as the additional risks of investing in the Fund.

The

Fund’s investment objective is for changes in the Shares’ net asset value (“NAV”) to reflect the daily

changes of the price of the Nasdaq Bitcoin Reference Price - Settlement (NQBTCS) (the “Benchmark”), less expenses

from the Fund’s operations. The Benchmark is designed to track the price performance of bitcoin. The Fund invests in bitcoin,

bitcoin futures contracts (“Bitcoin Futures Contracts”) listed on the Chicago Mercantile Exchange Inc. (“CME”),

and cash and cash equivalents. Because the Fund’s investment objective is to track the price of the Benchmark, changes in

the price of the Shares may vary from changes in the spot price of bitcoin.

An

investment in the Fund is subject to the risks of an investment in bitcoin and in futures contracts, both of which subject to

a high degree of price variability. An investment in the Fund may be riskier than other exchange-traded products that do not directly

hold bitcoin or financial instruments related to bitcoin and may not be suitable for all investors. In addition, bitcoin and Bitcoin

Futures Contracts may experience pronounced and swift price changes. Accordingly, there is a potential for movement in the price

of Shares between the time an investor places an order to purchase or sell with its broker-dealer and the time of the actual purchase

or sale resulting from the price volatility of bitcoin or Bitcoin Futures Contracts.

Investing

in the Fund involves significant risks. See “What Are the Risk Factors Involved with an Investment in the Fund?” beginning

on page 19. The Fund is not a mutual fund registered under the Investment Company Act of 1940, and Fund Shareholders will not

be afforded the protections associated with ownership of shares in a registered investment company. See “The Fund is

not a registered investment company, so you do not have the protections of the Investment Company Act of 1940” on

page 40.

THE

COMMODITY FUTURES TRADING COMMISSION HAS NOT PASSED UPON THE MERITS OF PARTICIPATING IN THIS POOL NOR HAS THE COMMISSION PASSED

ON THE ADEQUACY OR ACCURACY OF THIS DISCLOSURE DOCUMENT.

NEITHER

THE SECURITIES AND EXCHANGE COMMISSION (“SEC”) NOR ANY STATE SECURITIES COMMISSION HAS APPROVED OR DISAPPROVED OF

THE SECURITIES OFFERED IN THIS PROSPECTUS OR DETERMINED IF THIS PROSPECTUS IS TRUTHFUL OR COMPLETE. ANY REPRESENTATION TO THE

CONTRARY IS A CRIMINAL OFFENSE.

The

Fund is a series of the Tidal Commodities Trust I (the “Trust”). Shareholders have no voting rights with respect to

the Trust or the Fund except as expressly provided in the Trust’s First Amended and Restated Declaration of Trust and Trust

Agreement (the “Trust Agreement”). The sponsor of the Fund is Tidal Investments LLC (f/k/a Toroso Investments, LLC,

the “Sponsor”), which receives a management fee. The principal office address and telephone number of both the Fund

and the Sponsor is 234 West Florida Street, Suite 203, Milwaukee, Wisconsin 53204 and (844)-986-7700. Tidal ETF Services LLC (“Tidal”

or the “Administrator”) provides administrative services to the Fund and has also engaged the Fund’s Sub-Administrator

(as defined below). Tidal also assists the Fund and the Sponsor with certain functions and duties relating to marketing, which

include the following: marketing, sales strategy, and related services. Hashdex Asset Management Ltd. (“Hashdex” or

the “Digital Asset Adviser”) serves as the Fund’s digital asset adviser and assists the Sponsor and Administrator

with research and investment analysis regarding bitcoin and bitcoin markets for use in the management, marketing, and administration

of the Fund. Hashdex will also provide the Fund with branding, marketing services including, but not limited to, the issuance

of press releases, preparation of website data content, holding promotional webinars and engaging in promotional activities through

social media outlets. Hashdex has no role in maintaining, calculating or publishing the Benchmark. Hashdex also has no responsibility

for the investment or management of the Fund’s investment portfolio or for the overall performance or operation of the Fund.

BitGo Trust Company, Inc (the “Bitcoin Custodian”) is the custodian for the Fund’s bitcoin holdings; and U.S.

Bank, N.A. is the custodian for the Fund’s cash and cash equivalents holdings (the “Cash Custodian” and together

with the Bitcoin Custodian, the “Custodians”).

While

investors will purchase and sell Shares through their broker-dealer, the Fund continuously offers creation baskets consisting

of 10,000 Shares (“Creation Baskets”) at their NAV to certain parties who have entered into an agreement with the

Sponsor (“Authorized Purchasers”). Shares will be sold at the next determined NAV per Share. Authorized Purchasers,

in turn, may sell such Shares, which are listed on NYSE Arca, to the public at per-Share offering prices that are expected to

reflect, among other factors, the trading price of the Shares on NYSE Arca, the NAV of the Fund at the time the Authorized Purchaser

purchased the Creation Baskets and the NAV at the time of the offer of the Shares to the public, the supply of and demand for

Shares at the time of sale, and the liquidity of the markets for bitcoin and Bitcoin Futures Contracts in which the Fund invests.

A list of the Fund’s Authorized Purchasers as of the date of this Prospectus can be found under “Plan of Distribution

– Marketing Agent and Authorized Purchasers,” on page 93. The prices of Shares offered by Authorized Purchasers

are expected to fall between the Fund’s NAV and the trading price of the Shares on NYSE Arca at the time of sale. The Fund’s

Shares may trade in the secondary market on NYSE Arca at prices that are lower or higher than their NAV per Share. The Fund conducts

creation and redemption transactions only for cash, and, with respect to creation transactions, the cash is used to purchase Bitcoin

Futures Contracts only.

The

Fund is the successor and surviving entity from the merger (the “Merger”) into the Fund of Hashdex Bitcoin Futures

ETF (the “Predecessor Fund”) that was a series of the Teucrium Commodity Trust (the “Predecessor Trust”)

sponsored by Teucrium Trading, LLC (“Prior Sponsor”). Prior to the Merger, the Fund had no operations. By being the

surviving entity from the Merger, the Fund acquired all assets and assumed all the liabilities of the Predecessor Fund and succeeded

to the Predecessor Fund’s performance history. The Merger did not materially modify the rights of Fund shareholders. The

Merger closed on January 3, 2024. Unless otherwise indicated, information concerning the Fund for periods before January 3, 2024

is information of the Predecessor Fund.

This

is a best efforts offering. The Marketing Agent, Foreside Fund Services, LLC, a wholly-owned subsidiary of Foreside Financial

Group, LLC (d/b/a ACA Group) (the “Marketing Agent”) is not required to sell any specific number or dollar amount

of Shares but will use its best efforts to sell Shares. This is intended to be a continuous offering, unless suspended or terminated

at any earlier time for certain reasons specified in this prospectus. See “Prospectus Summary – The Shares”

and “Creation and Redemption of Shares – Rejection of Purchase Orders” below.

The

Fund is a commodity pool and the Sponsor is a commodity pool operator subject to regulation by the Commodity Futures Trading Commission

and the National Futures Association under the Commodity Exchange Act (“CEA”).

COMMODITY

FUTURES TRADING COMMISSION

RISK

DISCLOSURE STATEMENT

YOU

SHOULD CAREFULLY CONSIDER WHETHER YOUR FINANCIAL CONDITION PERMITS YOU TO PARTICIPATE IN A COMMODITY POOL. IN SO DOING, YOU SHOULD

BE AWARE THAT COMMODITY INTEREST TRADING CAN QUICKLY LEAD TO LARGE LOSSES AS WELL AS GAINS. SUCH TRADING LOSSES CAN SHARPLY REDUCE

THE NET ASSET VALUE OF THE POOL AND CONSEQUENTLY THE VALUE OF YOUR INTEREST IN THE POOL. IN ADDITION, RESTRICTIONS ON REDEMPTIONS

MAY AFFECT YOUR ABILITY TO WITHDRAW YOUR PARTICIPATION IN THE POOL.

FURTHER,

COMMODITY POOLS MAY BE SUBJECT TO SUBSTANTIAL CHARGES FOR MANAGEMENT, AND ADVISORY AND BROKERAGE FEES. IT MAY BE NECESSARY FOR

THOSE POOLS THAT ARE SUBJECT TO THESE CHARGES TO MAKE SUBSTANTIAL TRADING PROFITS TO AVOID DEPLETION OR EXHAUSTION OF THEIR ASSETS.

THIS DISCLOSURE DOCUMENT CONTAINS A COMPLETE DESCRIPTION OF EACH EXPENSE TO BE CHARGED THIS POOL AT PAGE 91 AND A STATEMENT OF

THE PERCENTAGE RETURN NECESSARY TO BREAK EVEN, THAT IS, TO RECOVER THE AMOUNT OF YOUR INITIAL INVESTMENT, AT PAGE 13.

THIS

BRIEF STATEMENT CANNOT DISCLOSE ALL THE RISKS AND OTHER FACTORS NECESSARY TO EVALUATE YOUR PARTICIPATION IN THIS COMMODITY POOL.

THEREFORE, BEFORE YOU DECIDE TO PARTICIPATE IN THIS COMMODITY POOL, YOU SHOULD CAREFULLY STUDY THIS DISCLOSURE DOCUMENT, INCLUDING

A DESCRIPTION OF THE PRINCIPAL RISK FACTORS OF THIS INVESTMENT, AT PAGE 10 AND THE “RISK FACTORS” SECTION BEGINNING

ON PAGE 13.

TIDAL

INVESTMENTS LLC (“TIDAL”) IS A MEMBER OF NFA AND IS SUBJECT TO NFA’S REGULATORY OVERSIGHT AND EXAMINATIONS.

TIDAL HAS ENGAGED OR MAY ENGAGE IN UNDERLYING OR SPOT VIRTUAL CURRENCY TRANSACTIONS IN A COMMODITY POOL. ALTHOUGH NFA HAS JURISDICTION

OVER TIDAL AND ITS COMMODITY POOL, YOU SHOULD BE AWARE THAT NFA DOES NOT HAVE REGULATORY OVERSIGHT AUTHORITY FOR UNDERLYING OR

SPOT MARKET VIRTUAL CURRENCY PRODUCTS OR TRANSACTIONS OR VIRTUAL CURRENCY EXCHANGES, CUSTODIANS OR MARKETS. YOU SHOULD ALSO BE

AWARE THAT GIVEN CERTAIN MATERIAL CHARACTERISTICS OF THESE PRODUCTS, INCLUDING LACK OF A CENTRALIZED PRICING SOURCE AND THE OPAQUE

NATURE OF THE VIRTUAL CURRENCY MARKET, THERE CURRENTLY IS NO SOUND OR ACCEPTABLE PRACTICE FOR NFA TO ADEQUATELY VERIFY THE OWNERSHIP

AND CONTROL OF A VIRTUAL CURRENCY OR THE VALUATION ATTRIBUTED TO A VIRTUAL CURRENCY BY TIDAL.

This

prospectus is in two parts: a disclosure document and a statement of additional information. These parts are bound together, and

both contain important information.

The

date of this prospectus is March 27, 2025.

TABLE

OF CONTENTS

PROSPECTUS

SUMMARY

This

is only a summary of the prospectus and, while it contains material information about the Fund and its Shares, it does not contain

or summarize all of the information about the Fund and the Shares contained in this prospectus that is material and/or which may

be important to you. You should read this entire prospectus, including “What Are the Risk Factors Involved with an Investment

in the Fund?” beginning on page 19, before making an investment decision about the Shares. In addition, this prospectus

includes a statement of additional information that follows and is bound together with the primary disclosure document. Both the

primary disclosure document and the statement of additional information contain important information.

Principal

Offices of the Fund and the Sponsor

The

Fund is a series of the Trust. The principal offices of the Sponsor, the Trust and the Fund are located at 234 West Florida Street,

Suite 203, Milwaukee, Wisconsin 53204. The telephone number is (844)-986-7700.

Breakeven

Point

The

amount of trading income required for the redemption value of a Share at the end of one year to equal the selling price of the

Share, assuming an initial price of $106.00, is $0.00 or 0.00% of the selling price. For more information, see “Breakeven

Analysis” below.

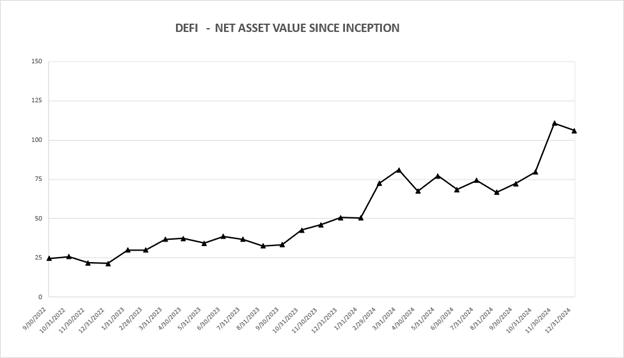

The

Fund’s Current Net Assets and Year to Date Performance

As

of December 31, 2024, the Fund’s total net assets were $14,839,385and the Fund had 140,000shares outstanding. The annual

performance of the Fund’s net asset value (“NAV”) per share from January 1, 2024 through December 31, 2024 was

108.91%, which depicts the change in NAV per share over the time period provided. For current information about outstanding Fund

Shares and other information, see the Fund’s website at www.hashdex-etfs.com/defi. For further discussion of the Fund’s performance,

see “OFFERING -Market Price of Shares and Prior Performance of Shares”.

The

Fund’s Investment Objective

The

Fund is a commodity pool that issues Shares that may be purchased and sold on NYSE Arca. The Fund’s investment objective

is for changes in the Shares’ net asset value (“NAV”) to reflect the daily changes of the price of the Nasdaq

Bitcoin Reference Price - Settlement (NQBTCS) (the “Benchmark”), less expenses from the Fund’s operations. The

Fund invests in bitcoin, Bitcoin Futures Contracts and cash and cash equivalents. The Sponsor employs a passive investment strategy

that is intended to track the changes in the Benchmark regardless of whether the Benchmark goes up or goes down. In order to track

the Benchmark as closely as possible, the Fund aims to maximize its investment in bitcoin. Because the Fund’s investment

objective is to track the price of the Benchmark, the price of the Shares may vary from changes in the spot price of bitcoin.

The NYSE Arca rule under which the Shares will be listed and traded prevents the Fund from utilizing leverage. ICE Data Indices,

LLC calculates an approximate net asset value every 15 seconds throughout each day that the Fund’s Shares are traded on

NYSE Arca for as long as the CME’s main pricing mechanism is open.

The

Fund, the Sponsor and the service providers, including the Custodians, will not loan or pledge the Fund’s assets, nor will

the Fund’s assets serve as collateral for any loan or similar arrangement except to the extent of need to collateralize

margin accounts held by the Fund’s FCMs.

Bitcoin

is a digital asset or cryptocurrency that is a unit of account on the bitcoin network (“Bitcoin Network”), an open

source, decentralized peer-to-peer computer network. The ownership and operation of bitcoin is determined by purchasers in the

Bitcoin Network. The Bitcoin Network connects computers that run publicly accessible, or open source, software that follows the

rules and procedures governing the Bitcoin Network. This is commonly referred to as the Bitcoin Protocol. Bitcoin may be held,

may be used to purchase goods and services or may be exchanged for fiat currency. No single entity owns or operates the Bitcoin

Network, and the value of bitcoin is not backed by any government, corporation or other entity. Instead the value of bitcoin is

determined in part by the supply and demand in markets created to facilitate the trading of bitcoin. Public key cryptography protects

the ownership and transaction records for bitcoin. Because the source code for the Bitcoin Network is open source, anyone can

contribute to its development. At this time, the ultimate supply of bitcoin is finite and limited to 21 million “coins”

with the number of bitcoin available increasing gradually as new bitcoin supplies are mined until the 21 million current protocol

cap is reached. The following factors, among others, may affect the price and market for bitcoin:

| ● | How

widely bitcoin is adopted, including the use of bitcoin as a payment. |

| ● | The

regulatory environment for cryptocurrencies, which continues to evolve in the U.S., and

which may delay, impede, or restrict the adoption or use of bitcoin. |

| ● | Speculative

activity in the market for bitcoin, including by holders of large amounts of bitcoin,

which may increase volatility. |

| ● | Cyberattacks,

including the risk that malicious actors will exploit flaws in the code or structure

of bitcoin, control the blockchain, steal information or cause disruptions to the internet. |

| ● | Rewards

for mining bitcoin are designed to decline over time, which may lessen the incentive

for miners to process and confirm transactions on the Bitcoin Network. |

| ● | The

open-source nature of the Bitcoin Network may result in forks, or changes to the underlying

code of bitcoin that result in the creation of new, separate digital assets. |

| ● | Fraud,

manipulation, security failure or operational problems at bitcoin exchanges that result

in a decline in adoption or acceptance of bitcoin. |

| ● | Scalability

as the use of bitcoin expands to a greater number of users. |

The

Fund is organized as a series of the Trust, a Delaware statutory trust organized on February 10, 2023. The Trust and the Fund

operate pursuant to the Trust Agreement, dated February 10, 2023. The Trust Agreement may be found on the SEC’s EDGAR filing

database at https://www.sec.gov/Archives/edgar/data/1985840/000138713123008542/ex3-1.htm. The Fund was formed and is managed and

controlled by the Sponsor, a limited liability company formed in Delaware on March 14, 2012. The Sponsor is registered as a commodity

pool operator (“CPO”) with the Commodity Futures Trading Commission (“CFTC”) and is a member of the National

Futures Association (“NFA”). The Fund intends to be treated as a partnership for U.S. federal income tax purposes.

The

Benchmark Methodology

The

Benchmark is governed by the Nasdaq Crypto Index Oversight Committee (“CIOC”), which is responsible for implementation,

administration, and oversight of the Benchmark, including its cessation. The CIOC shall approve any material changes to the methodology

and review the Benchmark methodology at least on an annual basis. The final Benchmark is calculated once every trading day and

it is given by a weighted average across the settlement prices of the following “Core Exchanges” (as of January 31,

2025): Bitstamp, Coinbase, Gemini, itBit, Kraken and LMAX Digital.

The

Benchmark was launched by Nasdaq on June 9, 2021 and is designed to track the price performance of bitcoin. Specifically, the

Benchmark attempts to track the average bitcoin spot price by capturing the notional value of bitcoin USD transactions reported

by selected public data sources as measured by Nasdaq, Inc (“Nasdaq”). The Benchmark applies a rules-based pricing

methodology to a diverse collection of pricing sources to provide a reference price for bitcoin and the pricing methodology is

designed to account for variances in price across a wide range of sources which have been vetted according to criteria identified

in the methodology document. The Benchmark is owned and administered by Nasdaq and may be changed from time to time. Detailed

rules on the Benchmark administration and governance may be found at Nasdaq’s website. The Benchmark does not track the

overall performance of all digital assets generally, nor the performance of any specific digital asset other than bitcoin. The

Benchmark is calculated and published once a day on business days at 3pm, New York Time by CF Benchmarks Limited (https://www.cfbenchmarks.com/data/indices/NQBTCS)

or other Nasdaq designated calculation agent.

According

to the Benchmark methodology, any deviations from the Benchmark methodology are made in the sole judgment and discretion of Nasdaq

so that the Benchmark continues to achieve its objective. Nasdaq will provide transparency over the decisions affecting the compilation

of the reference rate and any related determination process, including contingency measures in the event of absence of or insufficient

inputs, market stress or disruption, failure of critical infrastructure, or other relevant factors. Any contingency measures that

are not directly addressed in the Benchmark methodology shall be subject to CIOC governance processes.

The

Sponsor, in its sole discretion, may cause the Fund to track a benchmark other than the Benchmark at any time, with prior notice

to investors. The Sponsor may change the Fund’s benchmark if investment conditions change or the Sponsor believes that another

benchmark or standard better aligns with the Fund’s investment objective and strategy. The Sponsor, however, is under no

obligation whatsoever such a change in any circumstance.

To

the extent CIOC implements a material change to the calculation of the benchmark, the Sponsor will issue a press release describing

such change and its date of implementation which press release will be filed with the SEC on Form 8-K.

To

the extent the Sponsor determines that in the best interest of the Fund to replace the Benchmark with another benchmark reference

price or index, the Sponsor shall issue a press release describing the replacement of the Benchmark and new benchmark at least

60 days in advance of such replacement and will file such press release under Form 8-K with the SEC. For more information on the

Benchmark, see “Offering - Benchmark Calculation” and “Offering - Benchmark Performance” sections below.

Bitcoin

Futures Contracts

The

CME currently offers two Bitcoin Futures Contracts, one contract representing 5 bitcoin (“BTC Contracts”) and another

contract representing 0.10 bitcoin (“MBT Contracts”). The Fund invests in bitcoin BTC Contracts and MBT Contracts

to the extent necessary to achieve exposure to the bitcoin futures market. Because the Fund’s investment objective is to

track the price of the Benchmark by investing in bitcoin and Bitcoin Futures Contracts, changes in the price of the Shares may

vary from changes in the spot price of bitcoin

The

Fund maintains long positions in BTC Contracts and MBT Contracts to achieve exposure to the bitcoin futures market. As discussed

under the “the Fund’s Investment Strategies”, the Sponsor invests the Fund in spot bitcoin and utilizes Bitcoin

Futures Contracts to hedge the cash balance that the Sponsor deems necessary to meet the Fund’s liquidity needs for the

cash payment of Share redemption settlements and of other applicable expenses borne by the Fund. The Fund may purchase MBT Contracts

if the Fund has proceeds remaining from the sale of a Creation Basket that are less than the price of a BTC contract. BTC and

MBT will count toward an aggregate position limit.

BTC

Contracts began trading on the CME Globex trading platform on December 15, 2017 under the CME ClearPort ticker symbol “BTC”

and are cash settled in U.S. dollars. MBT Contracts began trading on the CME Globex trading platform on May 3, 2021 under the

CME ClearPort ticker symbol “MBT” and are also cash settled in U.S. dollars. The daily settlement prices for MBT Contracts

are derived directly from the settlements in the BTC Contracts. BTC Contracts and MBT Contracts are listed for trading in serial

months of six (6), quarterly in serial quarters of four (4). Additionally, when the listing schedule includes only a single futures

contract set to expire in December, an extra December contract will be listed for the subsequent year. This ensures that at any

given time, there are at least two December contracts available for trading.

Because

BTC Contracts and MBT Contracts are exchange-listed, they allow investors to gain price exposure to bitcoin without having to

hold the underlying cryptocurrency. Like a futures contract on a commodity or stock index, BTC Contracts and MBT Contracts provide

a means for investors to hedge investment positions or speculate on the future price of bitcoin.

The

Bitcoin Futures Contracts are cash-settled to the CME CF Bitcoin Reference Rate (BRR). The BRR is a daily reference rate of the

U.S. dollar price of one bitcoin calculated daily as of 4:00 p.m. London time provided by CF Benchmarks. It is calculated based

on the bitcoin trading activity on specified spot bitcoin trading platforms (“Constituent Exchanges”) during an observation

window between 3:00 p.m. and 4:00 p.m. London time, which currently include Bitstamp, Coinbase, Gemini, itBit Kraken, LMAX Digital

and Bullish Exchange but may change from time to time.

Constituent

exchanges for the BRR are selected on the basis of the following criteria, which each must demonstrate that it continues to fulfill

on an ongoing basis:

| ● | The

exchange has policies to ensure fair and transparent market conditions at all times and

has processes in place to identify and impede illegal, unfair or manipulative trading

practices. |

| ● | The

exchange does not impose undue barriers to entry or restrictions on market participants,

and utilizing the venue does not expose market participants to undue credit risk, operational

risk, legal risk or other risks. |

| ● | The

exchange complies with applicable law and regulation, including, but not limited to capital

markets regulations, money transmission regulations, client money custody regulations,

know-your-client (KYC) regulations and anti-money-laundering (AML) regulations. |

| ● | The

exchange cooperates with inquiries and investigations of regulators and the Administrator

upon request and has to execute data sharing agreements with the CME. |

Should

the average daily contribution of a constituent exchange fall below 3%, then the continued inclusion of the venue as a constituent

exchange is assessed by the CME CF Oversight Committee.

Qualifying

transactions from the constituent exchanges that take place during the one-hour calculation window are added to a list, with the

trade price and size for each transaction recorded. The one-hour calculation is partitioned into twelve intervals of five minutes

each, and for each partition, the volume-weighted median trade price is calculated from the trade prices and sizes of relevant

transactions. (A volume-weighted median differs from a standard median in that a weighting factor, in this case trade size, is

factored into the calculation.) The BRR is the equally-weighted average of the volume-weighted medians of all twelve partitions.

Further

details on the market share and volume information for each constituent platforms used to calculate the CME CF Bitcoin Reference

Rate (BRR) are provided below. The table below lists the seven constituent platforms that contribute transaction data to the BRR.

It includes the aggregate volumes traded on their respective Bitcoin – US Dollar markets over the preceding four calendar

quarters.

| Period |

Aggregate

Trading Volume of BTC-USD Markets of CME CF Constituent Platforms** |

| |

itBit |

LMAX

Digital |

Bitstamp |

Coinbase |

Gemini |

Kraken |

Bullish* |

| 2024

Q1 |

1,300,217,284 |

18,606,590,980 |

12,614,344,809 |

90,691,419,596 |

4,117,487,659 |

17,217,440,706 |

N/A |

| 2024

Q2 |

1,103,291,739 |

11,280,822,955 |

12,745,481,874 |

81,871,129,923 |

4,460,975,011 |

15,942,525,422 |

N/A |

| 2024

Q3 |

742,961,240 |

7,674,154,200 |

11,788,598,149 |

58,463,571,028 |

3,343,922,945 |

10,944,408,968 |

N/A |

| 2024

Q4 |

1,196,003,201 |

15,679,729,421 |

19,041,512,220 |

106,998,253,547 |

7,762,251,106 |

19,039,509,976 |

171,943,974* |

*

Bullish became a CME CF Constituent Platform on December 30th, 2024, and thus its aggregate volume is that observed for 2 days

(December 30th and 31st, 2024).

**

Source: CF Benchmarks

Considering

the 12 highest volume Bitcoin -USD markets operated by spot Bitcoin Trading Platforms, the following table shows the market share

for BTC-USD trading of the seven constituent platforms over the past four calendar quarters:

| Spot

Trading Platforms Market Share of BTC-USD Trading*** |

| Period |

itBit |

LMAX

Digital |

Bitstamp |

Coinbase |

Gemini |

Kraken |

Bullish* |

Others** |

| 2024

Q1 |

0.68% |

9.78% |

6.63% |

47.65% |

2.16% |

9.05% |

N/A |

24.05% |

| 2024

Q2 |

0.69% |

7.05% |

7.97% |

51.17% |

2.79% |

9.96% |

N/A |

20.37% |

| 2024

Q3 |

0.46% |

4.73% |

7.26% |

36.01% |

2.06% |

6.74% |

N/A |

42.75% |

| 2024

Q4 |

0.33% |

4.39% |

5.33% |

29.95% |

2.17% |

5.33% |

0.05%* |

52.44% |

*

Bullish became a CME CF Constituent Platform on December 30th, 2024, and thus its share is that observed for 2 days (December

30th and 31st, 2024) within the quarter.

**

Comprises Bitfinex, Crypto.com

***

Source: CF Benchmarks

The

Fund’s Investment Strategies

The

Fund seeks to achieve its investment objective by primarily investing in bitcoin. The Fund uses Bitcoin Futures Contracts for

the primary purpose of using such Bitcoin Futures Contracts to acquire physical bitcoin through EFP transactions and to offset

cash and receivables for better tracking the Benchmark. Under normal market conditions, the Fund has a policy to maximize its

investments in physical bitcoin such that it is expected that at least 95% of the Fund’s assets will be invested in bitcoin,

and up to 5% may be invested in Bitcoin Futures Contracts and in cash and cash equivalents, such as short-term Treasury bills,

money market funds, and demand deposit accounts. The Sponsor does not have discretion in choosing the Fund’s investments.

See “Use of Proceeds” The term “normal market conditions” includes, but is not limited to, the absence

of: trading halts in the applicable financial markets generally; operational issues (e.g., systems failure) causing dissemination

of inaccurate market information; or force majeure type events such as natural or man-made disaster, act of God, armed conflict,

act of terrorism, riot or labor disruption or any similar intervening circumstance. Similarly, the Fund uses bitcoin to acquire

Bitcoin Futures Contracts through EFP transactions, so the Fund can then sell the Bitcoin Futures Contracts for cash in order

to satisfy redemption orders.

The

percentage allocation to Bitcoin Futures Contracts is determined daily such that the Fund may maintain Bitcoin Futures Contracts

positions (with related cash reserves to meet applicable margin requirements) to hedge the cash balance that the Sponsor deems

necessary to meet the Fund’s liquidity needs for the cash payment of Share redemption settlements and of other applicable

expenses borne by the Fund.

When

the Fund needs to increase or decrease its allocation to physical bitcoin it will do so through EFP transactions, by exchanging

a physical bitcoin holding for an equivalent Bitcoin Futures Contracts position.

The

Fund’s futures contract positions will be concentrated on the first to expire contracts and rolled on a monthly basis by

closing out the first to expire contracts prior to their final settlement date and then either entering on and EFP transaction

to exchange that position for physical bitcoin holdings or entering into the second to expire contracts which will become the

new first to expire. A first to expire contract is the contract with the nearest expiration date. A second to expire contract

follows the first - it is the contract that will expire second in line after the first contract has expired. For example, when

a first to expire contract expires, the second to expire contract becomes the first to expire contract.

Futures

contract rolling will take place on the market business day preceding the last trading day of the first to expire contract. The

last trading day of the first to expire contact is currently defined as the last business Friday of each month. By way of example,

as of the date of this prospectus the Fund’s futures contract positions will be entered and exited according to the roll

schedule below.

| Hashdex

Bitcoin ETF (DEFI) – Roll Schedule Jan 2025 – Dec 2025 |

| |

| Roll

Date |

Contract

Expiring |

New

Contract |

First

to Expire Contract |

| |

(Exiting

Position) |

(Entering

Position) |

(Resulting

Position) |

| 1/31/2025 |

January

(BTCF5) |

February

(BTCG5) |

February

(BTCG5) |

| 2/28/2025 |

February

(BTCG5) |

March

(BTCH5) |

March

(BTCH5) |

| 3/28/2025 |

March

(BTCH5) |

April

(BTCJ5) |

April

(BTCJ5) |

| 4/25/2025 |

April

(BTCJ5) |

May

(BTCK5) |

May

(BTCK5) |

| 5/30/2025 |

May

(BTCK5) |

June

(BTCM5) |

June

(BTCM5) |

| 6/27/2025 |

June

(BTCM5) |

July

(BTCN5) |

July

(BTCN5) |

| 7/25/2025 |

July

(BTCN5) |

August

(BTCQ5) |

August

(BTCQ5) |

| 8/29/2025 |

August

(BTCQ5) |

September

(BTCU5) |

September

(BTCU5) |

| 9/26/2025 |

September

(BTCU5) |

October

(BTCV5) |

October

(BTCV5) |

| 10/31/2025 |

October

(BTCV5) |

November

(BTCX5) |

November

(BTCX5) |

| 11/28/2025 |

November

(BTCX5) |

December

(BTCZ5) |

December

(BTCZ5) |

| 12/26/2025 |

December

(BTCZ5) |

January

(BTCF6) |

January

(BTCF6) |

One

factor determining the total return from investing in futures contracts is the price relationship between soon to expire contracts

and later to expire contracts. Sometimes the Fund will have to pay more for longer maturity contracts to replace existing shorter

maturity contracts about to expire. This situation is known as “contango” in the futures markets. In the event of

a prolonged period of contango, and absent the impact of rising or falling bitcoin prices, this could have a negative impact on

the Fund’s NAV and total return, which in turn may have a negative impact on your investment in the Fund. By way of example,

during the period from 6/30/2020 to 6/30/2023, the market for Bitcoin Futures Contracts were in contango approximately 87% of

the time, which resulted in an average annual negative roll yield of approximately 4.5%. If the futures market is in a state of

backwardation (i.e., when the price of bitcoin in the future is to be less than the current price), the Fund will buy later to

expire contracts for a lower price than the soon to expire contracts that it sells.

Consistent

with applicable provisions of the Trust Agreement and Delaware law, the Fund has broad authority to make changes to the Fund’s

operations. The Fund may change its investment objective, benchmark, or investment strategies and Shareholders of the Fund will

not have any rights with respect to these changes. The Fund has no current intention to make any such change, and any change is

subject to applicable regulatory requirements, including, but not limited to, any requirement to amend applicable listing rules

of NYSE Arca.

The

reasons for and circumstances that may trigger any such changes may vary widely and cannot be predicted. However, by way of example,

the Fund may change the term structure or underlying components of the Bitcoin Futures Contracts holdings in furtherance of the

Fund’s investment objective of tracking the price of the Benchmark, due to market conditions, a potential or actual imposition

of position limits by the SEC, the CFTC or futures exchange rules, or the imposition of risk mitigation measures by a futures

commission merchant, restricts the ability of the Fund to invest in bitcoin or in Bitcoin Futures Contracts. The Fund would, among

other things, file a current report on Form 8-K and a prospectus supplement to describe any such change and the effective date

of the change. Shareholders may modify their holdings of the Fund’s Shares in response to any change by purchasing or selling

Fund Shares through their broker-dealer.

The

Fund invests in bitcoin and Bitcoin Futures Contracts without being leveraged or unable to satisfy its expected current or potential

margin or collateral obligations with respect to its investments. After fulfilling such margin and collateral requirements, the

Fund invests the remainder of its proceeds from the sale of baskets in short term financial instruments of the type commonly known

as “cash and cash equivalents.”

The

Fund’s investment objective is for changes in the Shares’ NAV to reflect the daily changes of the price of the Benchmark,

less expenses from the Fund’s operations. In furtherance of the Fund’s policy to maximize its holdings in bitcoin,

the Sponsor will use cash received through the creation process to purchase Bitcoin Futures Contracts to be exchanged for bitcoin

such that at least 95% of the assets of the Fund will be in bitcoin. In the extraordinary event that Bitcoin Futures Contracts

are unable to be readily exchanged for bitcoin, the Fund will continue to hold Bitcoin Futures Contracts. The Sponsor does not

have discretion in choosing the Fund’s investments. See “Use of Proceeds”. The Fund’s investment strategy

is designed to permit investors generally to purchase and sell the Fund’s Shares for the purpose of investing indirectly

in the bitcoin market in a cost-effective manner. The Sponsor expects that the Fund’s average daily tracking error against

the Benchmark will be less than 10 percent over any period of 30 trading days. However, the Fund incurs certain expenses in connection

with its operations, which cause imperfect correlation between changes in the Fund’s NAV and changes in the Benchmark because

the Benchmark does not reflect expenses or income. As a result, investors may incur a partial or complete loss of their investment

even when the performance of the Benchmark is positive.

Investors

may purchase and sell Shares through their broker-dealers. However, the Fund creates and redeems Shares only in blocks called

Creation Baskets and Redemption Baskets, respectively, and only Authorized Purchasers may purchase or redeem Creation Baskets

or Redemption Baskets. An Authorized Purchaser is under no obligation to create or redeem baskets, and an Authorized Purchaser

is under no obligation to offer to the public Shares of any baskets it does create. Baskets are generally created when there is

a demand for Shares, including, but not limited to, when the market price per Share is at (or perceived to be at) a premium to

the NAV per Share. Similarly, baskets are generally redeemed when the market price per Share is at (or perceived to be at) a discount

to the NAV per Share. Retail investors seeking to purchase or sell Shares on any day are expected to affect such transactions

in the secondary market, on NYSE Arca, at the market price per Share, rather than in connection with the creation or redemption

of baskets.

The

Sponsor believes that by investing in bitcoin and Bitcoin Futures Contracts, the Fund’s NAV closely tracks the Benchmark.

The Sponsor also believes that because of market arbitrage opportunities, the market price at which investors purchase and sell

Shares through their broker-dealer will closely track the Fund’s NAV. The Sponsor believes that the net effect of these

relationships is that the Fund’s market price on NYSE Arca at which investors purchase and sell Shares will closely track

the bitcoin market, as measured by the Benchmark.

The

CFTC and U.S. designated contract markets, such as the CME, have established position limits and accountability levels on the

maximum net long or net short Bitcoin Futures Contracts that the Fund may hold, own or control. The current CME established position

limit level for investments in BTC Contracts for the spot month is 4,000 contracts. A position accountability level of 5,000 contracts

will be applied to positions in single months outside the spot month and in all months combined. The MBT Contracts have a spot

month limit of 200,000 contracts and a position accountability level of 250,000 contracts. Open positions in MBT Contracts will

count as 1/50 of a BTC Contract for the purposes of determining the aggregate position limit. Accountability levels are not fixed

ceilings but rather thresholds above which the exchange may exercise greater scrutiny and control over an investor, including

limiting the Fund to holding no more Bitcoin Futures Contracts than the amount established by the accountability levels. The potential

for the Fund to reach position or accountability limits will depend on if and how quickly the Fund’s net assets increase.

In

addition to position limits and accountability limits, the CME and other exchanges have set dynamic price fluctuation limits on

Bitcoin Futures Contracts. The dynamic price limit functionality under the special price fluctuation limits mechanism assigns

a price limit variant which equals a percentage of the prior trading day’s settlement price, or a price deemed appropriate.

During the trading day, the dynamic variant is utilized in continuous rolling 60-minute look-back periods to establish dynamic

upper and lower price fluctuation limits. Once the dynamic price fluctuation limit has been reached in a particular Bitcoin Futures

Contract, no trades may be made at a price beyond that limit. The CME has adopted daily dynamic price fluctuation limit functionality

effective March 11, 2019, specifically, Rule 589 which is found in the following link: https://www.cmegroup.com/content/dam/cmegroup/notices/ser/2019/03/SER-8351.pdf.

Since dynamic price fluctuation limits were introduced, price limits have been triggered 89 times and there has been one “hard

limit move.” A hard limit move is when the price of Bitcoin Futures Contracts exceeds a price limit that defines the minimum/maximum

price to which such Bitcoin Futures Contracts can move for the given trade date. If the hard limit is reached, trade matching

will not occur at prices above the maximum price or below the minimum price.

In

determining the value of Bitcoin Futures Contracts, the Sub-Administrator uses primarily the settlement price for the Bitcoin

Futures Contracts, as reported on the CME. CME Group staff determines the daily settlements for the Bitcoin Futures Contracts

based on trading activity on CME Globex exchange between 14:59:00 and 15:00:00 Central Time (CT), the settlement period. In situations

where a two-sided market is not available during the closing period, the CME will derive a settlement price using the carry calculation

method based on the CME CF Bitcoin Reference Rate (BRR). This method calculates the settlement price as the reference rate plus

an adjustment factoring in the days to expiration and the interest rate. Specifically, the settlement price is determined by the

formula: BRR + [(Days to Expiration / 365) × Interest Rate × BRR]. When a Bitcoin Futures Contracts has closed at

its daily price fluctuation limit, that limit price will be the daily settlement price that the CME publishes.

In

exceptional circumstances when: (i) Bitcoin Futures Contracts settlement prices are not readily available; or (ii) when a trading

halt closes CME or the Bitcoin Futures Market early, including if trading were halted for an entire trading day or several trading

days; or (iii) when a Bitcoin Futures Contracts close at its price fluctuation limit for the day, the fair value of such contracts

are determined by the Sponsor in good faith and in a manner that assesses the Bitcoin Futures Contracts’ value based on

a consideration of all available facts and all available information on the valuation date. The fair value of Bitcoin Futures

Contracts is determined by attempting to estimate the price at which such Bitcoin Futures Contract would be trading in the absence

of the price fluctuation limit (either above such limit when an upward limit has been reached or below such limit when a downward

limit has been reached). Typically, this estimate will be made primarily using a carry calculation described above that uses the

BRR at 4:00 p.m. E.T. on settlement day as a reference price. The fair value of BTC Contracts and MBT Contracts may not reflect

such security’s market value or the amount that the Fund might reasonably expect to receive for the BTC Contracts and MBT

Contracts upon its current sale.

Position

limits, accountability limits and dynamic price fluctuation limits may limit the Fund’s ability to invest the proceeds of

Creation Baskets in bitcoin or Bitcoin Futures Contracts. As a result, when the Fund offers to sell Creation Baskets it may be

limited in its ability to invest in bitcoin or Bitcoin Futures Contracts. The Fund may hold larger amounts of cash and cash equivalents,

which will impair the Fund’s ability to meet its investment objective of tracking the Benchmark.

There

is a minimum number of baskets and associated Shares specified for the Fund. If the Fund experiences redemptions that cause the

number of Shares outstanding to decrease to the minimum level of Shares required to be outstanding, until the minimum number of

Shares is again exceeded through the purchase of a new Creation Basket, there can be no more redemptions by an Authorized Purchaser.

In such cases, market makers may be less willing to purchase Shares from investors in the secondary market, which may in turn

limit the ability of Shareholders of the Fund to sell their Shares in the secondary market. These minimum levels for the Fund

are 50,000 Shares, representing five baskets. The minimum level of Shares specified for the Fund is subject to change.

The

Sponsor maintains a public website on behalf of the Fund, https://hashdex-etfs.com/defi, which contains information about

the Trust, the Fund, and the Shares.

Note

to Secondary Market Investors: Except when aggregated in Redemption Baskets, Shares are not individually redeemable.

Shares can be directly purchased from the Fund only in Creation Baskets, and only by Authorized Purchasers. Each Creation Basket

consists of 10,000 Shares and therefore requires a significant financial commitment to purchase. Shares will be sold at the next

determined NAV per Share. Accordingly, investors who do not have such resources or who are not Authorized Purchasers should be

aware that some of the information contained in this prospectus, including information about purchases and redemptions of Shares

directly with the Fund, is only relevant to Authorized Purchasers. There is no guarantee that Shares will trade at prices that

are at or near the per-Share NAV. When buying or selling Shares on the secondary market through a broker, most investors incur

customary brokerage commissions and charges.

As

noted, the Fund may invest in Bitcoin Futures Contracts traded on the CME. The Fund expressly disclaims any association with the

CME or endorsement of the Fund by such exchange and acknowledges that “CME” is a registered trademark of such exchange.

As

of December 31, 2024, the Fund held 15,785 of BTC Contracts, 0 MBT Contracts, and $29,680 in cash and cash equivalents. As

of December 31, 2024 the Fund held 15,785 bitcoin.

The

Fund’s Investments in Bitcoin

The

Fund’s investment strategy includes direct investments in bitcoin, commonly referred to as “spot bitcoin”. Such

positions are purchased and sold solely through CME’s Exchange for Physical Transactions (“EFP”) and are held

by the Bitcoin Custodian on behalf of the Fund.

EFP

Transactions are privately negotiated trades between two parties that allow for the simultaneous transfer of a futures position

for an equivalent spot market position, or vice versa. The Fund does not intend to trade on unregulated bitcoin spot exchanges.

All transfers relating to purchases or sales of bitcoin are settled via “on-chain” transactions represented on the

bitcoin blockchain. The EFP transactions, although facilitated by the infrastructure and under the regulatory oversight of the

CME, a CFTC-regulated market, are executed off-exchange and may not carry the same regulatory requirements and level of oversight

as on-exchange transactions.

Governed

by CME Exchange Rule 538, EFP transactions must be executed at commercially reasonable prices mutually agreed upon by the parties

involved. All parties to an EFP are required to prepare and maintain all documents related to both the futures and the corresponding

physical bitcoin position, in accordance with CFTC Regulation 1.35. CME has the authority to obtain records related to EFP transactions

and has a surveillance program in place to appropriately monitor and enforce compliance with its Market Regulation to prevent

fraud and manipulation.

Given

that both sides of the trade track the same benchmark (Bitcoin), an EFP is a market-neutral transaction. Therefore, the pricing

of the EFP is quoted in terms of the basis between the price of the futures contract and the level of the underlying bitcoin.

When

the Sponsor decides to increase or decrease its holdings of physical bitcoin, it will cause the Fund to execute an EFP trade with

a liquidity provider (an “LP”). The selection of those LPs is based on the objective of achieving the best execution

for each transaction, in line with the Fund’s investment strategy. As of the date of this prospectus, Cumberland DRW LLC,

Flow Traders B.V., JSCT, LLC, XBTO International Ltd., DV Chain, LLC, GSR Markets Ltd. B2C2 USA, Inc. and Nonco LLC have been

approved as LPs. Jane Street Capital, LLC, one of the Authorized Purchasers, is an affiliate of JSCT, LLC, one of the LPs. Current

or future LPs may be affiliates or, or have material relationships with, the Fund’s current or future Authorized Purchasers.

The

Fund and the LP will simultaneously exchange a futures position for a corresponding, economically offsetting position in physical

bitcoin. Specifically, when the Sponsor intends to increase the Fund’s bitcoin holdings, the Fund will participate in an

EFP transaction to sell futures contracts and buy physical bitcoin, while the LP participating in such transaction will buy futures

contracts and sell physical bitcoin. Similarly, when the Sponsor seeks to decrease the Fund’s bitcoin holdings, the Fund

will participate in an EFP transaction to buy futures contracts and sell physical bitcoin, while the LP on the other side of the

transaction will sell futures contracts and buy physical bitcoin.

In

order to ensure best execution and ensure that transactions are executed at commercially reasonable prices when the Fund needs

to purchase or sell spot bitcoin, the Sponsor will conduct a Request-for-Quote (“RFQ”) auction with multiple LPs using

the current day settlement price as the reference for the Futures Contracts. The Sponsor may use electronic means such as the

Directed Request for Quote (DRFQ) available in the CME Direct, chat services or any other communication mechanism that is compatible

with CME’s and CFTC guidance around recordkeeping of EFP transactions. The LPs will present their quotes in terms of basis

points (1 bps = 0.01%) difference between the current day’s settlement price of the futures contract and bitcoin. The Fund

will then confirm the trade with the LP that offered the best quote. After the CME publishes the daily settlement price of the

relevant Bitcoin Futures Contract, the Sponsor and the selected LP calculate and confirm the price of the futures leg of the transaction

as being the published settlement price and the price of physical bitcoin leg of the transaction by applying the agreed upon basis

spread and submit the transaction to one of its FCMs that subsequently reports the transaction to the CME.

After

the EFP Transaction is confirmed by the CME, the futures leg of the transaction is cleared by CME Clearing, while the physical

leg is settled bilaterally with the LP depositing in the Fund’s Wallet with the Bitcoin Custodian the agreed upon amount

of bitcoin until the end of day New York time of the business day following the transaction date prior to any movement of cash

from the Cash Custodian. Upon receipt of the required amount of bitcoin, the Bitcoin Custodian will notify the Sponsor that the

bitcoin has been received. The Sponsor will then notify the Cash Custodian to write the corresponding cash to the LPF to complete

the settlement of the physical leg of the EFP Transaction. All purchases or sales of bitcoin related to EFP Transactions executed

by the Fund are settled on-chain.

Share

Price Premium and Discount

The

amount that the Fund’s market price is above the reported NAV is called the premium. The amount that the Fund’s market

price is below the reported NAV is called the discount. The market price is determined using the midpoint between the highest

bid and the lowest offer on the listing exchange, as of the time that the Fund’s NAV is calculated (usually 4:00 p.m., (ET)).

Since the Fund’s inception on September 16, 2022 - December 31, 2024, the highest premium was $2.89 (4.28%) and the highest

discount was $0.75 (-2.38%). For further information about premium discount information see “THE OFFERING - Prior Performance

of the Fund”.

Voting

Rights

As

interests in separate series of a Delaware statutory trust, the Shares do not involve the rights normally associated with the

ownership of shares of a corporation (including, for example, the right to bring shareholder oppression and derivative actions).

In addition, the Shares have limited voting and distribution rights (for example, shareholders do not have the right to elect

directors, as the Trust does not have a board of directors, and generally will not receive regular distributions of the net income

and capital gains earned by the Fund).

Shareholders

have no voting rights with respect to the Trust or the Fund except as expressly provided in the Trust Agreement. The Trust Agreement

provides that Shareholders representing at least a majority (over 50%) of the outstanding Shares of the Trust, voting together

as a single class (excluding Shares acquired by the Sponsor in connection with its initial capital contribution to any Trust series),

may vote to (i) continue the Trust by electing a successor Sponsor as described above, and (ii) approve amendments to the Trust

Agreement that impair the right to surrender Redemption Baskets for redemption. In addition, Fund shareholders holding Shares

representing seventy-five percent (75%) of the outstanding Shares of the Trust, voting together as a single class (excluding Shares

acquired by the Sponsor in connection with its initial capital contribution to any Trust series) may vote to dissolve the Trust

upon not less than ninety (90) days’ notice to the Sponsor.

Principal

Investment Risks of an Investment in the Fund

An

investment in the Fund involves a degree of risk and you could incur a partial or total loss of your investment in the Fund. Some

of the risks you may face are summarized below. A more extensive discussion of these risks appears in the “What Are the

Risk Factors Involved with an Investment in the Fund?” section, beginning on page 19.

| ● | The

Fund was formed as the survivor to the Merger with the Predecessor Fund, which commenced

operations on September 15, 2022. The Fund has the limited performance history of the

Predecessor Fund to serve as a basis for you to evaluate an investment in the Fund. In

addition, the Fund may not be successful in implementing its investment objective or

may fail to attract sufficient assets. |

| ● | Bitcoin

and Bitcoin Futures Contracts are a relatively new asset class and bitcoin is subject

to rapid changes, uncertainty and regulation that may adversely affect the value of bitcoin

and bitcoin futures, and therefore the nature of an investment in the Fund and may adversely

affect the ability of the Fund to buy and sell bitcoin and Bitcoin Futures Contracts,

and therefore the ability to achieve its investment objective. |

| ● | Historically,

bitcoin and Bitcoin Futures Contracts have been subject to significant price volatility.

The price of Bitcoin Futures Contracts may differ significantly from the spot price of

bitcoin. According to Bloomberg from 6/30/2022 to 12/31/2024 front month Bitcoin Futures

Contracts exhibited an average implied 30-Day volatility of 56.39. The highest volatility

during that period was 92.86 on 7/12/22 and the lowest was 27.58 on 10/24/2022. Bitcoin

can be highly volatile, for example, after a 774% price increase from 1/1/2020 prices

peaked in May 2021 and front month Bitcoin Futures Contracts began to decline with a

peak to trough retracement of 47.06% by 7/20/2021. Prices then rose from that low until

11/9/2021, a new all time high, resulting in a price increase of 127.58%. Front month

Bitcoin Futures Contracts prices peaked on 11/9/2021, began to decline with a peak to

trough retracement of 76.91% by 11/09/2022 and rose from that level by 503% as of 12/31/2024. |

| ● | The

market for Bitcoin Futures Contracts is less developed than older, more established futures

markets (such as corn or wheat futures) and may be more volatile and less liquid. |

| ● | The

Fund will compete with direct investments in bitcoin, other cryptocurrencies and other

potential financial vehicles and other investment vehicles that focus on other digital

assets. Market and financial conditions, and other conditions beyond the Fund’s

control, such as the timing of reaching the market and the Fund’s fee structure

relative to other bitcoin exchange-trade products, may make it more attractive to invest

in other vehicles. The competition from other investment vehicles focused on bitcoin

or other cryptocurrencies could have a detrimental effect on the scale and sustainability

of the Fund. |

| ● | Unlike

mutual funds, commodity pools and other investment pools that manage their investments

so as to realize income and gains for distribution to their investors, the Fund generally

does not distribute dividends to Shareholders. You should not invest in the Fund if you

will need cash distributions from the Fund to pay taxes on your share of income and gains

of the Fund, if any, or for other purposes. |

| ● | Only

an Authorized Purchaser may engage in creation or redemption transactions with the Fund.

The Fund has a limited number of institutions that act as Authorized Purchasers. To the

extent these institutions exit the business or are unable or unwilling to proceed with

creation and/or redemption orders with respect to the Fund, Fund Shares may, particularly

in times of market stress, trade at a discount to the NAV per Share and possibly face

trading halts and/or delisting. |

| ● | In

some cases, the near month Bitcoin Futures Contract’s price will be lower than

the next month’s contract prices (a situation known as “contango” in

the futures markets). In the event of a prolonged period of contango, and absent the

impact of rising or falling bitcoin prices, this could have a significant negative impact

on the Fund’s NAV and total return, and you could incur a partial or total loss

of your investment in the Fund. By way of example, during the period from 6/30/2020 to

6/30/2023, the market for Bitcoin Futures Contracts were in contango approximately 87%

of the time, which resulted in an average annual negative roll yield of approximately

4.5%. |

| ● | You

will have no rights to participate in the management of the Fund and will have to rely

on the duties and judgment of the Sponsor to manage the Fund. |

| ● | The

Fund seeks to have changes in its Shares’ NAV track changes in the Benchmark, rather

than profit from speculative trading of bitcoin and Bitcoin Futures Contracts or from

the use of leverage (i.e., the Sponsor manages the Fund so that the aggregate value of

the Fund’s exposure to losses from its investments in bitcoin and Bitcoin Futures

Contracts at any time will not exceed the value of the Fund’s assets). |

| ● | Bitcoin

and other cryptocurrencies are a new and developing asset class subject to both developmental

and regulatory uncertainty. Future U.S. or foreign regulatory changes may alter the nature

of an investment in the Fund, or the ability of the Fund to continue to implement its

investment strategy. |

| ● | Failures

or breaches of the electronic systems of the Fund, the Sponsor, or third parties or other

events such as the recent COVID-19 pandemic have the ability to cause disruptions and

negatively impact the Fund’s business operations, potentially resulting in financial

losses to the Fund and its Shareholders. |

| ● | The

Fund is subject to position limits, accountability limits and dynamic price fluctuation

limits that could limit the Fund’s ability to invest the proceeds of Creation Baskets

in bitcoin and Bitcoin Futures Contracts. Position limits, accountability limits and

dynamic price fluctuation limits may cause tracking error or may impair the Fund’s

ability to meet its investment objective of tracking the Benchmark. |

| ● | War

and other geopolitical events may cause volatility in bitcoin prices. These events are

unpredictable and may lead to extended periods of price volatility. |

| ● | The

Fund currently has two futures commission merchants (“FCMs”) through which

it buys and sells futures contracts. Volatility in the bitcoin futures market may lead

one or both of the Fund’s FCMs to impose risk mitigation procedures that could

limit the Fund’s investment in Bitcoin Futures Contracts beyond the accountability

and position limits imposed by the CME futures contract exchange as discussed herein.

An FCM could impose a financial ceiling on initial margin that could change and become

more or less restrictive on the Fund’s activities depending upon a variety of conditions

beyond the Sponsor’s control. If the Fund’s other current FCM were to impose

position limits, or if any other FCM with which the Fund establishes a relationship in

the future were to impose position limits, the Fund’s ability to meet its investment

objective could be negatively impacted. The Fund continues to monitor and manage its

existing relationships with its FCMs and will continue to seek additional relationships

with FCMs as needed. |

| ● | The

occurrence of a severe weather event, natural disaster, terrorist attack, geopolitical

event, outbreak or public health emergency as declared by the World Health Organization,

the continuation or expansion of war or other hostilities, or a prolonged government

shutdown may have significant adverse effects on the Fund and its investments and alter

current assumptions and expectations. For example, in late February 2022, Russia invaded

Ukraine, significantly amplifying already existing geopolitical tensions among Russia

and other countries in the region and in the West. The responses of countries and political

bodies to Russia’s actions, the larger overarching tensions, and Ukraine’s

military response and the potential for wider conflict may increase financial market

volatility generally, have severe adverse effects on regional and global economic markets,

and cause volatility in the price of bitcoin, bitcoin futures and the Share price of

the Fund. |

| ● | The

ability of Authorized Purchasers to create or redeem Shares may be suspended for several

reasons, including but not limited to the Fund voluntarily imposing such restrictions.

A suspension in the ability of Authorized Purchasers to create or redeem Shares would

have no impact on the Fund’s investment objective – the Fund would continue

to seek to track its Benchmark. However, with respect to the impact of a suspension on

the price of Fund Shares in the secondary market, investors may have to pay a higher

price to buy Shares and receive a lower price when they sell their Shares. This “spread”

may continue to widen the longer the suspension lasts. |

| ● | Market

fraud and/or manipulation and other fraudulent trading practices such as the intentional

dissemination of false or misleading information (e.g., false rumors) can, among other

things, lead to a disruption of the orderly functioning of bitcoin and Bitcoin Futures

Contract markets, significant market volatility, and cause the value of bitcoin and Bitcoin

Futures Contracts to fluctuate quickly and without warning. Depending on the timing of

an investor’s purchases and sales of the Fund’s Shares, these pricing anomalies

could cause the investor to incur losses. |

| ● | There

can be no assurance that the Fund will achieve its investment objective due to position

limits, accountability levels, dynamic price fluctuation limits and other limitations

on the Fund’s investing in bitcoin and Bitcoin Futures Contracts that may be imposed

following the Merger. |

For

additional risks, see “What Are the Risk Factors Involved with an Investment in the Fund?”

Determination

of NAV

The

Fund’s NAV is determined as of the earlier of the close of trading on NYSE Arca or 4:00 p.m. (ET) on each day that NYSE

Arca is open for trading.

Defined

Terms

For

a glossary of defined terms, see Appendix A.

Breakeven

Analysis

The

breakeven analysis set forth below is a hypothetical illustration of the approximate dollar returns and percentage returns for

the redemption value of a single Share to equal the amount invested twelve months after the investment is made. For purposes of

this breakeven analysis, an initial selling price of $106.00per Share, is assumed. The breakeven analysis is an approximation

only and assumes a constant month-end Net Asset Value. In order for a hypothetical investment in Shares to breakeven over the

next 12 months, assuming a selling price of 106.00per Share, the investment would have to generate a 0.00% or $0.00 return. The

numbers in the chart below have been rounded to the nearest 0.01.

| | |

Per Share | |

| | |

| |

| Assumed initial selling price per Share (1) | |

$ | 106.00 | |

| Management Fee (0.25%) (2) | |

$ | 0.27 | |

| Estimated Brokerage Commissions and Fees (3) | |

$ | 0.00 | |

| Other Fund Fees and Expenses (4) | |

$ | 0.00 | |

| Interest and Other Income (5.00%) (5) | |

$ | (2.65 | ) |

| Amount of trading income (loss) required for the redemption value at the end of one year to equal the selling price of the Share | |

$ | 0.00 | |

| Percentage of initial selling price per Share (6) | |

| 0.00 | % |

| (1) |

In order to show how a hypothetical investment

in Shares would break even over the next 12 months, this breakeven analysis uses an assumed initial selling price of $106.00per

Share, which is based on the Fund NAV per share as of December 31, 2025. Investors should note that, because the Fund’s

NAV will change on a daily basis, the breakeven amount on any given day could be higher or lower than the amount reflected

here. |

| |

|

| (2) |

From the Management Fee, the Sponsor pays all

of the routine operational, administrative and other ordinary expenses of the Fund, generally as determined by the Sponsor,

including but not limited to, fees and expenses of the Administrator, Sub-Administrator, Custodians, Marketing Agent, Transfer

Agent, licensors, accounting and audit fees and expenses, tax preparation expenses, legal fees, ongoing SEC registration fees,

individual Schedule K-1 preparation and mailing fees, and report preparation and mailing expenses. These fees and expenses

are not included in the breakeven table because they are paid for by the Sponsor through the proceeds from the Management

Fee. |

| |

|

| (3) |

Reflects estimated brokerage commissions and

fees for Bitcoin Futures Contract purchase or sale and acquiring and selling physical bitcoin, reflected on a per trade basis.

The estimated fee is based on the actual fees for the acquisition and sale of physical bitcoin in the Fund for the period

from March 27, 2024 to December 31, 2024. The actual amount of brokerage commissions and trading fees to be incurred will

vary based upon the trading frequency of the Fund. The Sponsor may elect to pay or waive a portion of these fees. The Fund

may elect to waive fees in order to reduce the Fund’s expenses. |

| |

|

(4)

|

The Fund pays all of its non-recurring and unusual

fees and expenses, if any, as determined by the Sponsor. Non-recurring and unusual fees and expenses are unexpected or unusual

in nature, such as legal claims and liabilities and litigation costs or indemnification or other unanticipated expenses. Extraordinary

fees and expenses also include material expenses which are not currently anticipated obligations of the Fund. Routine operational,

administrative and other ordinary expenses are not deemed extraordinary expenses. |

| |

|

| (5) |

The Fund seeks to earn interest and other income

in high credit quality, short-duration instruments or deposits associated with the pool’s cash management strategy that

may be used to offset expenses. These investments may include, but are not limited to, short-term Treasury Securities, demand

deposits, and money market funds. Considering various uncertain factors in the US and commodity markets, management has estimated

a blended interest rate of 5.00%. This estimate assumes that 95% of the Fund will be invested in spot bitcoin and the remaining

5% has the potential to earn interest. It’s important to note that the actual rate may vary and not all assets within

the Fund will necessarily earn interest. The actual rate may vary and not all assets of the Fund will earn interest. |

| |

|

| (6) |

This represents the estimated approximate percentage

for the redemption value of a hypothetical initial investment in a single Share to equal the amount invested twelve months after

the investment was made. The estimated approximate percentage of selling price is 0.00% or $0.00 per Share. |

THE

OFFERING

| Offering |

The Fund’s

Shares are listed on NYSE Arca and investors may purchase and sell Shares through their broker-dealer. The Fund only offers

Creation Baskets consisting of 10,000 Shares through the Marketing Agent to Authorized Purchasers. Authorized Purchasers may

purchase Creation Baskets consisting of 10,000 Shares at the Fund’s NAV. |

| |

|

| Merger |

The Fund is the

successor and surviving entity from the merger (the “Merger”) into the Fund of Hashdex Bitcoin Futures ETF (the

“Predecessor Fund”) that was a series of the Teucrium Commodity Trust (the “Predecessor Trust”) sponsored

by Teucrium Trading, LLC (“Prior Sponsor”). The Merger closed on January 3, 2024. |

| |

|

| Use of Proceeds |

The Sponsor applies

substantially all of the Fund’s assets toward investing in bitcoin, Bitcoin Futures Contracts, cash, and cash equivalents.

The Fund will aim to maximize its investment in bitcoin and may also use Bitcoin Futures Contracts for the primary purpose

of using such Bitcoin Futures Contracts to acquire physical bitcoin through EFP transactions and to offset cash and receivables

for better tracking the benchmark index. The Sponsor deposits a portion of the Fund’s net assets with its FCM or other

financial institutions to be used to meet its current or potential margin or collateral requirements in connection with its

investment in Bitcoin Futures Contracts. The Fund uses only cash and cash equivalents to satisfy these requirements. The Sponsor