UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

SCHEDULE 13E-3

RULE 13e-3 TRANSACTION STATEMENT UNDER SECTION 13(e) OF

THE SECURITIES EXCHANGE ACT OF 1934

SciPlay Corporation

(Name of the Issuer)

SciPlay Corporation

Light & Wonder, Inc.

Bern Merger Sub, Inc.

LNW Social Holding Company I, LLC

LNW Social Holding Company II, LLC

Light and Wonder International, Inc.

(Names of Persons Filing Statement)

Class A Common Stock, par value $0.001

per share

(Title of Class of Securities)

809087109

(CUSIP Number of Class of Securities)

|

Joshua J. Wilson

SciPlay Corporation

6601 Bermuda Road

Las Vegas, Nevada 89119

(702) 897-7150 |

Matthew R. Wilson

Light & Wonder, Inc.

Bern Merger Sub, Inc.

LNW Social Holding Company I, LLC

LNW Social Holding Company II, LLC

Light and Wonder International, Inc.

6601 Bermuda Road

Las

Vegas, Nevada 89119

(702) 897-7150 |

(Name, Address and Telephone Numbers of Person

Authorized to Receive Notices and Communications on Behalf of the Persons Filing Statement)

With copies to

|

Audra D. Cohen

Melissa Sawyer

Sullivan & Cromwell LLP

125 Broad Street

New York, NY 10004 |

Robert I. Townsend, III

Jin-Kyu Baek

Cravath, Swaine & Moore LLP

825 8th Avenue

New York, NY 10019 |

NEITHER THE SECURITIES AND EXCHANGE COMMISSION NOR ANY STATE SECURITIES

COMMISSION HAS APPROVED OR DISAPPROVED THIS TRANSACTION, PASSED ON THE MERITS OR THE FAIRNESS OF THE TRANSACTION OR PASSED UPON THE ADEQUACY

OR ACCURACY OF THE INFORMATION CONTAINED IN THIS DOCUMENT. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

This statement is filed in connection

with (check the appropriate box):

| a. | x The filing of solicitation materials or an information

statement subject to Regulation 14A (§§ 240.14a-1 through 240.14b-2), Regulation

14C (§§ 240.14c-1 through 240.14c-101) or Rule 13e-3(c) (§ 240.13e-3(c))

under the Securities Exchange Act of 1934 (the “Exchange Act”). |

| b. | ¨

The filing of a registration statement under the Securities

Act of 1933. |

Check

the following box if the soliciting materials or information statement referred to in checking box (a) are preliminary copies: x

Check

the following box if the filing is a final amendment reporting the results of the transaction: ¨

INTRODUCTION

This Rule 13e-3

transaction statement on Schedule 13E-3, together with the exhibits hereto (this “Transaction Statement”), is being

filed with the Securities and Exchange Commission (the “SEC”) pursuant to Section 13(e) of the Exchange

Act, by (a) SciPlay Corporation, a Nevada corporation (the “Company”), the issuer of the shares of Class A

common stock, par value $0.001 per share (the “Class A Common Stock”), and Class B common stock, par value

$0.001 per share (the “Class B Common Stock” and, together with the Class A Common Stock, the “Common

Stock”), that are the subject of the Rule 13e-3 transaction; (b) Light & Wonder, Inc., a Nevada

corporation (“Parent”); (c) Bern Merger Sub, Inc., a Nevada corporation (“Merger Sub”);

(d) LNW Social Holding Company I, LLC, a Nevada limited liability company (the “Principal Stockholder”); (e) LNW

Social Holding Company II, LLC, a Nevada limited liability company; and (f) Light and Wonder International, Inc., a Delaware

corporation. Collectively, the persons filing this Transaction Statement are referred to as the “filing persons.”

This Transaction

Statement relates to the Agreement and Plan of Merger, dated as of August 8, 2023 (as amended or otherwise modified in accordance

with its terms, the “Merger Agreement”), by and among Parent, Merger Sub and the Company. Pursuant to the Merger Agreement,

Merger Sub will merge with and into the Company (the “Merger”), with the Company surviving the Merger as the surviving

corporation (the “Surviving Corporation”).

Upon consummation

of the Merger, on the terms and subject to the conditions set forth in the Merger Agreement and in accordance with the laws of the State

of Nevada, each share of Class A Common Stock issued and outstanding immediately prior to the effective time of the Merger (the

“Effective Time”) (other than (i) shares of Class A Common Stock held by the Company as treasury stock immediately

prior to the Effective Time, (ii) shares of Class B Common Stock issued and outstanding immediately prior to the Effective

Time and (iii) Class A Common Stock held by Parent, Merger Sub or any other direct or indirect wholly owned subsidiary of Parent

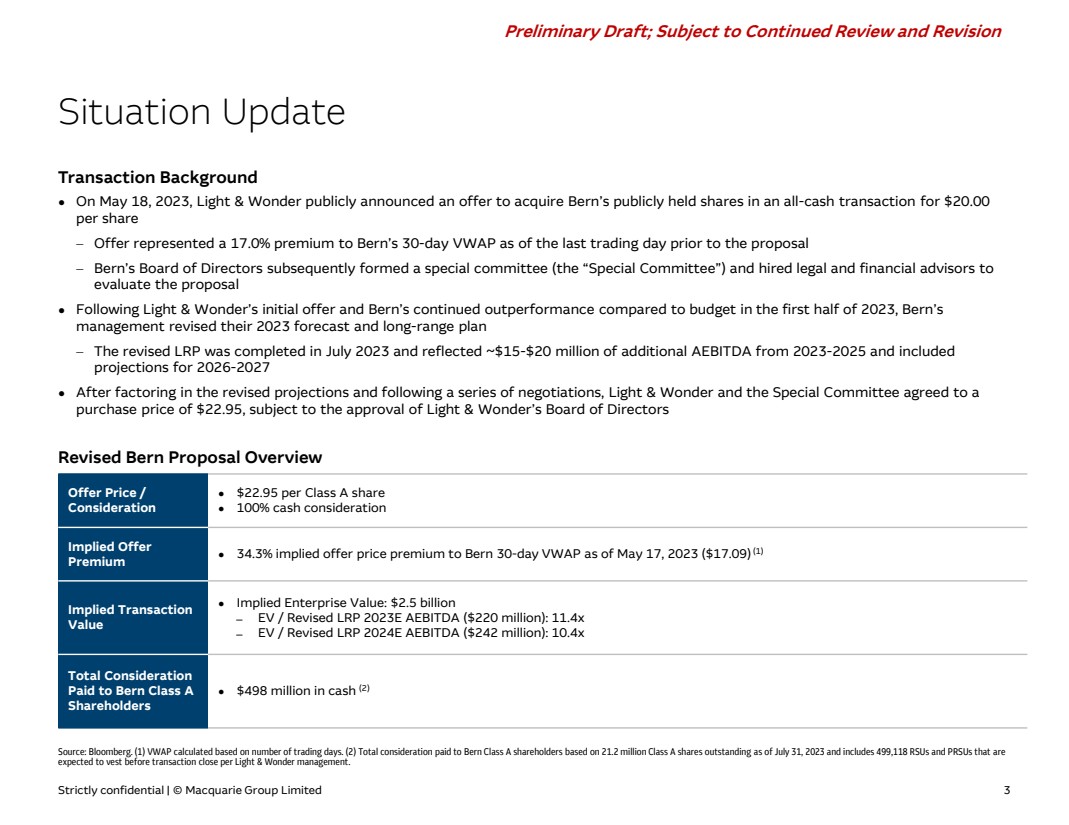

as of immediately prior to the Effective Time not held on behalf of third parties) will be converted into the right to receive $22.95

in cash, without interest (the “Merger Consideration”). Each share of Class B Common Stock issued and outstanding

immediately prior to the Effective Time will remain in existence following the Effective Time as a share of Class B common stock,

par value $0.001 per share, of the Surviving Corporation. In accordance with Section (F) of Article VI of the Amended

and Restated Articles of Incorporation of the Company and Section 11.01 of the Amended and Restated Operating Agreement of SciPlay

Parent Company, LLC, a Nevada limited liability company (“SciPlay Parent LLC”), dated as of May 2, 2019 (as amended,

restated or otherwise modified from time to time, the “SciPlay Parent LLC Agreement”), each holder of a unit of member’s

interest in SciPlay Parent LLC that is authorized and issued under the SciPlay Parent LLC Agreement and that constitutes a “Common

Unit” as defined in the SciPlay Parent LLC Agreement (such unit of member’s interest, a “Common Unit”),

that is issued and outstanding immediately prior to the Effective Time will be entitled, upon the election of such holder exercisable

no later than 10 business days after the Effective Time, to exchange each such Common Unit for the Merger Consideration that is payable

with respect to one share of Class A Common Stock under the Merger Agreement. As part of the Written Consent (as defined below)

executed and delivered by the Principal Stockholder on August 8, 2023, the Principal Stockholder, which on such date beneficially

owned all of the issued and outstanding Common Units not owned by the Company, waived any entitlement it has as a holder of Common Units

to receive the Merger Consideration that is payable under the Merger Agreement with respect to each Common Unit that it holds immediately

prior to the Effective Time. Pursuant to the Merger Agreement, the Company also waived any entitlement it has as a holder of Common Units

to receive the Merger Consideration that is payable under the Merger Agreement with respect to each Common Unit that it holds immediately

prior to the Effective Time. Treatment of outstanding equity plan awards under the Company’s equity incentive plans and award agreements

is described in greater detail in the Information Statement (as defined below) under “The Special Factors—Interests of Our

Directors and Executive Officers in the Merger” and “The Merger Agreement—Consideration to be Received in the Merger.”

Further, following completion of the Merger, the Class A Common Stock will be delisted from the Nasdaq Global Select Market and

deregistered under the Exchange Act.

The board of directors

of the Company (the “Board”) (acting, at least in part, based upon the receipt of the unanimous recommendation of

a special committee of the Board, comprised solely of independent and disinterested directors (the “Special Committee”))

has (i) determined that the Merger Agreement, the Merger and the transactions contemplated by the Merger Agreement (the “Transactions”)

are advisable and fair to, and in the best interests of, the Company and the holders of Common Stock (the “Stockholders”)

(other than Parent and its subsidiaries), (ii) adopted and approved, pursuant to Nevada Revised Statutes (“NRS”)

92A.120, and declared advisable the Merger Agreement, the Merger and the other Transactions, (iii) directed the submission of the

Merger Agreement to the Stockholders for approval and (iv) recommended that the Stockholders vote in favor of the approval of the

Merger Agreement, the Merger and the other Transactions. Ms. Antonia Korsanos, who serves as Chair of the Board and who also serves

as Executive Vice Chair of the board of directors of Parent and Ms. Constance P. James, who at the time served as a member of the

Board and who was also the Executive Vice President, Chief Financial Officer, Treasurer and Corporate Secretary of Parent, recused themselves

from the deliberations and vote of the Board regarding the Merger Agreement, the Merger and the other Transactions.

Concurrently with

the filing of this Transaction Statement, the Company is filing an information statement (the “Information Statement”)

under Section 14(c) of the Exchange Act. A copy of the Information Statement is attached hereto as Exhibit (a)(1) and

a copy of the Merger Agreement is attached as Annex A to the Information Statement. The approval of the Merger Agreement, the Merger

and the other Transactions required the affirmative vote (at a meeting or by written consent) of a majority of the voting power of the

Stockholders, with holders of Class A Common Stock and holders of Class B Common Stock voting together as a single class (the “Required

Stockholder Approval”). Following the execution of the Merger Agreement, Parent caused the Principal Stockholder, which on

such date beneficially owned all of the issued and outstanding shares of Class B Common Stock, representing a majority of the outstanding

voting power of the issued and outstanding shares of Common Stock, to execute and deliver to the Company an irrevocable written consent

approving the Merger Agreement, the Merger and the other Transactions (the “Written Consent”), thereby providing the

Required Stockholder Approval for the Merger.

Pursuant to General

Instruction F to Schedule 13E-3, the information contained in the Information Statement, including all annexes thereto, is expressly

incorporated herein by reference in its entirety, and responses to each item herein are qualified in their entirety by the information

contained in the Information Statement and the annexes thereto. The cross-references below are being supplied pursuant to General Instruction

G to Schedule 13E-3 and show the location in the Information Statement of the information required to be included in response to the

items of Schedule 13E-3. As of the date hereof, the Information Statement is in preliminary form and is subject to completion.

All information

contained in this Transaction Statement concerning any of the filing persons has been provided by such filing person and no filing person

has produced any disclosure with respect to any other filing persons.

ITEM 1. SUMMARY

TERM SHEET

The information

set forth in the Information Statement under the following captions is incorporated herein by reference:

“Summary”

“Questions

and Answers about the Merger”

ITEM 2. SUBJECT

COMPANY INFORMATION

(a) Name

and Address. The information set forth in the Information Statement under the following caption

is incorporated herein by reference:

“The Parties

to the Merger Agreement”

(b) Securities.

The information set forth in the Information Statement under the following captions is incorporated

herein by reference:

“Summary”

“Questions

and Answers about the Merger”

“Market Information,

Dividends and Certain Transactions in the Class A Common Stock”

(c) Trading

Market and Price. The information set forth in the Information Statement under the following

caption is incorporated herein by reference:

“Market Information,

Dividends and Certain Transactions in the Class A Common Stock”

(d) Dividends.

The information set forth in the Information Statement under the following caption is incorporated

herein by reference:

“Market Information,

Dividends and Certain Transactions in the Class A Common Stock”

(e) Prior

Public Offerings. The information set forth in the Information Statement under the following

captions is incorporated herein by reference:

“Summary”

“Market Information,

Dividends and Certain Transactions in the Class A Common Stock”

(f) Prior

Stock Purchases. The information set forth in the Information Statement under the following

caption is incorporated herein by reference:

“Market Information,

Dividends and Certain Transactions in the Class A Common Stock”

ITEM 3. IDENTITY

AND BACKGROUND OF FILING PERSONS

(a)–(c) Name

and Address; Business and Background of Entities; Business and Background of Natural Persons. The

information set forth in the Information Statement under the following captions is incorporated herein by reference:

“Summary”

“The Parties

to the Merger Agreement”

“Directors,

Executive Officers and Controlling Persons of the Company”

“Where You

Can Find More Information”

ITEM 4. TERMS

OF THE TRANSACTION

(a)(1) Material

Terms – Tender Offers. Not applicable.

(a)(2) Material

Terms – Merger or Similar Transactions. The information set forth in the Information Statement

under the following captions is incorporated herein by reference:

“Summary”

“Questions

and Answers about the Merger”

“The Special

Factors – Background of the Merger”

“The Special

Factors – Recommendation of the Special Committee; Reasons for the Merger; Recommendation of the Board”

“The Special

Factors – Required Stockholder Approval for the Merger”

“The Special

Factors – Opinion and Materials of Lazard”

“The Special

Factors – Certain Company Financial Forecasts”

“The Special

Factors – Opinion and Materials of Macquarie Capital”

“The Special

Factors – Position of the Company on the Fairness of the Merger”

“The Special

Factors – Position of the LNW Entities in Connection with the Merger”

“The Special

Factors – Purposes and Reasons of the Company in Connection with the Merger”

“The Special

Factors – Purposes and Reasons of the LNW Entities in Connection with the Merger”

“The Special

Factors – Accounting Treatment”

“The Special

Factors – Interests of Our Directors and Executive Officers in the Merger”

“The Special

Factors – Delisting and Deregistration of Class A Common Stock”

“The Special

Factors – Material United States Federal Income Tax Consequences of the Merger”

“The Merger

Agreement”

“Annex A:

Merger Agreement”

“Annex B:

Lazard Opinion”

“Annex C:

Macquarie Capital Opinion”

“Annex D:

Written Consent”

(c) Different

Terms. The information set forth in the Information Statement under the following captions is

incorporated herein by reference:

“Summary”

“Questions

and Answers about the Merger”

“The Special

Factors – Interests of Our Directors and Executive Officers in the Merger”

“The Merger

Agreement – Consideration to be Received in the Merger”

(d) Appraisal

Rights. The information set forth in the Information Statement under the following captions is

incorporated herein by reference:

“Summary

– No Dissenter’s Rights”

“Questions

and Answers about the Merger”

“No Dissenter’s

Rights”

(e) Provisions

for Unaffiliated Security Holders. The information set forth in the Information Statement under

the following captions is incorporated herein by reference:

“Summary”

“Questions

and Answers about the Merger”

“No Dissenter’s

Rights”

“The Special

Factors – Recommendation of the Special Committee; Reasons for the Merger; Recommendation of the Board”

“Provisions

for Unaffiliated Stockholders”

(f) Eligibility

for Listing or Trading. Not applicable.

ITEM 5. PAST

CONTACTS, TRANSACTIONS, NEGOTIATIONS AND AGREEMENTS

(a) Transactions.

The information set forth in the Information Statement under the following caption is incorporated

herein by reference:

“Market Information,

Dividends and Certain Transactions in the Class A Common Stock”

“Transactions

Between the Company and the LNW Entities”

(b)–(c) Significant

Corporate Events; Negotiations or Contacts. The information set forth in the Information

Statement under the following captions is incorporated herein by reference:

“Summary”

“Questions

and Answers about the Merger”

“The Special

Factors – Background of the Merger”

“The Special

Factors – Recommendation of the Special Committee; Reasons for the Merger; Recommendation of the Board”

“The Special

Factors – Required Stockholder Approval for the Merger”

“The Special

Factors – Financing”

“The Special

Factors – Position of the Company on the Fairness of the Merger”

“The Special

Factors – Position of the LNW Entities in Connection with the Merger”

“The Special

Factors – Purposes and Reasons of the Company in Connection with the Merger”

“The Special

Factors – Purposes and Reasons of the LNW Entities in Connection with the Merger”

“The Special

Factors – Delisting and Deregistration of Class A Common Stock”

“The Special

Factors – Fees and Expenses”

“The Merger

Agreement – Form of Merger”

“The Merger

Agreement – Consummation and Effectiveness of the Merger”

“The Merger

Agreement – Consideration to be Received in the Merger”

“The Merger

Agreement – Written Consent; Merger Sub Shareholder Consent”

“Market Information,

Dividends and Certain Transactions in the Class A Common Stock”

“Annex A:

Merger Agreement”

“Annex D:

Written Consent”

(e) Agreements

Involving the Subject Company’s Securities. The information set forth in the Information

Statement under the following captions is incorporated herein by reference:

“Summary”

“Questions

and Answers about the Merger”

“The Special

Factors – Background of the Merger”

“The Special

Factors – Recommendation of the Special Committee; Reasons for the Merger; Recommendation of the Board”

“The Special

Factors – Required Stockholder Approval for the Merger”

“The Special

Factors – Financing”

“The Special

Factors – Position of the Company on the Fairness of the Merger”

“The Special

Factors – Position of the LNW Entities in Connection with the Merger”

“The Special

Factors – Purposes and Reasons of the Company in Connection with the Merger”

“The Special

Factors – Purposes and Reasons of the LNW Entities in Connection with the Merger”

“The Special

Factors – Interests of Our Directors and Executive Officers in the Merger”

“The Special

Factors – Delisting and Deregistration of Class A Common Stock”

“The Special

Factors – Fees and Expenses”

“The Merger

Agreement – Form of Merger”

“The Merger

Agreement – Consummation and Effectiveness of the Merger”

“The Merger

Agreement – Consideration to be Received in the Merger”

“The Merger

Agreement – Written Consent; Merger Sub Shareholder Consent”

“The Merger

Agreement – Other Covenants and Agreements”

“Market Information,

Dividends and Certain Transactions in the Class A Common Stock”

“Transactions

between the Company and the LNW Entities”

“Annex A:

Merger Agreement”

“Annex D:

Written Consent”

ITEM 6. PURPOSES

OF THE TRANSACTION AND PLANS OR PROPOSALS

(b) Use

of Securities Acquired. The information set forth in the Information Statement under the following

captions is incorporated herein by reference:

“Summary”

“Questions

and Answers about the Merger”

“The Special

Factors – Delisting and Deregistration of Class A Common Stock”

“The Special

Factors – Plans for the Company After the Merger”

“The Merger

Agreement – Form of Merger”

“The Merger

Agreement – Consideration to be Received in the Merger”

(c)(1)–(8) Plans.

The information set forth in the Information Statement under the following captions is incorporated

herein by reference:

“Summary”

“Questions

and Answers about the Merger”

“The Special

Factors – Background of the Merger”

“The Special

Factors – Recommendation of the Special Committee; Reasons for the Merger; Recommendation of the Board”

“The Special

Factors – Position of the Company on the Fairness of the Merger”

“The Special

Factors – Position of the LNW Entities in Connection with the Merger”

“The Special

Factors – Purposes and Reasons of the Company in Connection with the Merger”

“The Special

Factors – Purposes and Reasons of the LNW Entities in Connection with the Merger”

“The Special

Factors – Interests of Our Directors and Executive Officers in the Merger”

“The Special

Factors – Delisting and Deregistration of Class A Common Stock”

“The Special

Factors – Plans for the Company After the Merger”

“The Special

Factors – Fees and Expenses”

“The Merger

Agreement”

“Annex A:

Merger Agreement”

ITEM 7. PURPOSES,

ALTERNATIVES, REASONS AND EFFECTS

(a) Purposes.

The information set forth in the Information Statement under the following captions is incorporated

herein by reference:

“Summary”

“The Special

Factors – Background of the Merger”

“The Special

Factors – Recommendation of the Special Committee; Reasons for the Merger; Recommendation of the Board”

“The Special

Factors – Position of the Company on the Fairness of the Merger”

“The Special

Factors – Purposes and Reasons of the Company in Connection with the Merger”

“The Special

Factors – Purposes and Reasons of the LNW Entities in Connection with the Merger”

“The Special

Factors – Plans for the Company After the Merger”

(b) Alternatives.

The information set forth in the Information Statement under the following captions is incorporated

herein by reference:

“The Special

Factors – Background of the Merger”

“The Special

Factors – Recommendation of the Special Committee; Reasons for the Merger; Recommendation of the Board”

“The Special

Factors – Opinion and Materials of Lazard”

“The Special

Factors – Purposes and Reasons of the Company in Connection with the Merger”

“The Special

Factors – Alternatives to the Merger”

(c) Reasons.

The information set forth in the Information Statement under the following captions is incorporated

herein by reference:

“Summary”

“The Special

Factors – Background of the Merger”

“The Special

Factors – Recommendation of the Special Committee; Reasons for the Merger; Recommendation of the Board”

“The Special

Factors – Position of the Company on the Fairness of the Merger”

“The Special

Factors – Position of the LNW Entities in Connection with the Merger”

“The Special

Factors – Purposes and Reasons of the Company in Connection with the Merger”

“The Special

Factors – Purposes and Reasons of the LNW Entities in Connection with the Merger”

(d) Effects.

The information set forth in the Information Statement under the following captions is incorporated

herein by reference:

“Summary”

“Questions

and Answers about the Merger”

“The Special

Factors – Background of the Merger”

“The Special

Factors – Recommendation of the Special Committee; Reasons for the Merger; Recommendation of the Board”

“The Special

Factors – Financing”

“The Special

Factors – Position of the Company on the Fairness of the Merger”

“The Special

Factors – Position of the LNW Entities in Connection with the Merger”

“The Special

Factors – Purposes and Reasons of the Company in Connection with the Merger”

“The Special

Factors – Purposes and Reasons of the LNW Entities in Connection with the Merger”

“The Special

Factors – Accounting Treatment”

“The Special

Factors – Interests of Our Directors and Executive Officers in the Merger”

“The Special

Factors – Delisting and Deregistration of Class A Common Stock”

“The Special

Factors – Plans for the Company After the Merger”

“The Special

Factors – Fees and Expenses”

“The Special

Factors – Material United States Federal Income Tax Consequences of the Merger”

“The Merger

Agreement – Form of Merger”

“The Merger

Agreement – Consummation and Effectiveness of the Merger”

“The Merger

Agreement – Consideration to be Received in the Merger”

“The

Merger Agreement – Charter; Bylaws”

“The Merger

Agreement – Directors’ and Officers’ Indemnification and Insurance”

“The

Merger Agreement – Continuing Employee Matters”

“No Dissenter’s

Rights”

“Annex A:

Merger Agreement”

ITEM 8. FAIRNESS

OF THE TRANSACTION

(a)–(b) Fairness;

Factors Considered in Determining Fairness. The information set forth in the Information Statement

under the following captions is incorporated herein by reference:

“Summary”

“Questions

and Answers about the Merger”

“The Special

Factors – Background of the Merger”

“The Special

Factors – Recommendation of the Special Committee; Reasons for the Merger; Recommendation of the Board”

“The Special

Factors – Opinion and Materials of Lazard”

“The Special

Factors – Position of the Company on the Fairness of the Merger”

“The Special

Factors – Position of the LNW Entities in Connection with the Merger”

“The Special

Factors – Purposes and Reasons of the Company in Connection with the Merger”

“The Special

Factors – Purposes and Reasons of the LNW Entities in Connection with the Merger”

“The Special

Factors – Interests of Our Directors and Executive Officers in the Merger”

“Annex B:

Lazard Opinion”

The

confidential discussion materials prepared by Lazard Frères & Co. LLC (“Lazard”) and provided to

the Special Committee, dated June 12, 2023, July 12, 2023, July 19, 2023, July 26, 2023 and August 7, 2023,

are attached hereto as Exhibits (c)(3) through and including (c)(7) and, in each case, is incorporated by reference

herein.

(c) Approval

of Security Holders. The information set forth in the Information Statement under the following

captions is incorporated herein by reference:

“Summary”

“Questions

and Answers about the Merger”

“The Special

Factors – Background of the Merger”

“The Special

Factors – Recommendation of the Special Committee; Reasons for the Merger; Recommendation of the Board”

“The Special

Factors – Required Stockholder Approval for the Merger”

“The Merger

Agreement – Written Consent; Merger Sub Shareholder Consent”

“Annex A:

Merger Agreement”

“Annex D:

Written Consent”

(d) Unaffiliated

Representative. The information set forth in the Information Statement under the following captions

is incorporated herein by reference:

“Summary”

“The Special

Factors – Background of the Merger”

“The Special

Factors – Recommendation of the Special Committee; Reasons for the Merger; Recommendation of the Board”

“The Special

Factors – Opinion and Materials of Lazard”

“The Special

Factors – Position of the Company on the Fairness of the Merger”

“The Special

Factors – Position of the LNW Entities in Connection with the Merger”

“The Special

Factors – Interests of Our Directors and Executive Officers in the Merger”

“Annex B:

Lazard Opinion”

(e) Approval

of Directors. The information set forth in the Information Statement under the following captions

is incorporated herein by reference:

“Summary”

“Questions

and Answers about the Merger”

“The Special

Factors – Background of the Merger”

“The Special

Factors – Recommendation of the Special Committee; Reasons for the Merger; Recommendation of the Board”

“The Special

Factors – Position of the Company on the Fairness of the Merger”

“The Special

Factors – Position of the LNW Entities in Connection with the Merger”

(f) Other

Offers. The information set forth in the Information Statement under the following captions

is incorporated herein by reference:

“Summary”

“The Special

Factors – Background of the Merger”

“The Special

Factors – Recommendation of the Special Committee; Reasons for the Merger; Recommendation of the Board”

“The Special

Factors – Position of the Company on the Fairness of the Merger”

“The Special

Factors – Position of the LNW Entities in Connection with the Merger”

“The Merger

Agreement – No Solicitation”

ITEM 9. REPORTS,

OPINIONS, APPRAISALS AND NEGOTIATIONS

(a)–(c) Report,

Opinion or Appraisal; Preparer and Summary of the Report, Opinion or Appraisal; Availability of Documents. The information

set forth in the Information Statement under the following captions is incorporated herein by reference:

“Summary”

“The Special

Factors – Background of the Merger”

“The Special

Factors – Recommendation of the Special Committee; Reasons for the Merger; Recommendation of the Board”

“The Special

Factors – Opinion and Materials of Lazard”

“The Special

Factors – Opinion and Materials of Macquarie Capital”

“The Special

Factors – Certain Company Financial Forecasts”

“The Special

Factors – Position of the Company on the Fairness of the Merger”

“The Special

Factors – Position of the LNW Entities in Connection with the Merger”

“Annex B:

Lazard Opinion”

“Annex C:

Macquarie Capital Opinion”

The

confidential discussion materials prepared by Lazard and provided to the Special Committee, dated June 12, 2023, July 12,

2023, July 19, 2023, July 26, 2023 and August 7, 2023, are attached hereto as Exhibits (c)(3) through and

including (c)(7) and, in each case, is incorporated by reference herein.

The

confidential discussion materials prepared by Macquarie Capital (USA) Inc. and provided to the Board of Directors of Parent, dated

May 17, 2023, August 3, 2023 and August 7, 2023, are attached hereto as Exhibits (c)(8) through and including

(c)(10) and, in each case, is incorporated by reference herein.

The reports, opinions

or appraisals referenced in this Item 9 are filed herewith or incorporated by reference herein and will be made available for inspection

and copying at the principal executive offices of the Company during its regular business hours by any interested holder of Class A

Common Stock or representative who has been designated in writing, and copies may be obtained by requesting them in writing from the

Company at the email address provided under the caption “Where You Can Find More Information” in the Information Statement,

which is incorporated herein by reference.

ITEM 10. SOURCE

AND AMOUNTS OF FUNDS OR OTHER CONSIDERATION

(a)–(b) Source

of Funds; Conditions. The information set forth in the Information Statement under the following

captions is incorporated herein by reference:

“Summary”

“Questions

and Answers about the Merger”

“The Special

Factors – Financing”

“The Special

Factors – Position of the LNW Entities in Connection with the Merger”

“The Merger

Agreement – Consummation and Effectiveness of the Merger”

“Annex A:

Merger Agreement”

(c) Expenses.

The information set forth in the Information Statement under the following caption is incorporated

herein by reference:

“The Special

Factors – Fees and Expenses”

(d) Borrowed

Funds. Not applicable.

ITEM 11. INTEREST

IN SECURITIES OF THE SUBJECT COMPANY

(a) Securities

Ownership. The information set forth in the Information Statement under the following captions

is incorporated herein by reference:

“Directors,

Executive Officers and Controlling Persons of the Company”

“Security

Ownership”

(b) Securities

Transactions. The information set forth in the Information Statement under the following captions

is incorporated herein by reference:

“The Special

Factors – Background of the Merger”

“The Special

Factors – Interests of Our Directors and Executive Officers in the Merger”

“The Merger

Agreement”

“Market Information,

Dividends and Certain Transactions in the Class A Common Stock”

“Annex A:

Merger Agreement”

ITEM 12. THE

SOLICITATION OR RECOMMENDATION

(d) Intent

to Tender or Vote in a Going-Private Transaction. Not applicable.

(e) Recommendations

of Others. Not applicable.

ITEM 13. FINANCIAL

STATEMENTS

(a) Financial

Statements. The audited financial statements set forth in the Company’s Annual Report

on Form 10-K for the fiscal year ended December 31, 2022, originally filed on March 1, 2023 (see pages 58 to 86 therein),

the unaudited consolidated statements of income, consolidated statements of comprehensive income, condensed consolidated balance sheets,

consolidated statements of changes in stockholders’ equity and condensed consolidated statements of cash flows set forth in the

Company’s Quarterly Report on Form 10-Q for the quarter ended March 31, 2023, originally filed on May 9, 2023 (see

pages 6 to 19 therein), and the unaudited consolidated statements of income, consolidated statements of comprehensive income, condensed

consolidated balance sheets, consolidated statements of changes in stockholders’ equity and condensed consolidated statements of

cash flows set forth in the Company’s Quarterly Report on Form 10-Q for the quarter ended June 30, 2023, originally filed

on August 8, 2023 (see pages 6 to 19 therein), are incorporated by reference herein. The information set forth in the Information

Statement under the following captions is incorporated herein by reference:

“Market Information,

Dividends and Certain Transactions in the Class A Common Stock”

“Where You

Can Find More Information”

(b) Pro

Forma Information. Not applicable.

ITEM 14. PERSONS/ASSETS,

RETAINED, EMPLOYED, COMPENSATED OR USED

(a) Solicitations

or Recommendations. Not applicable.

(b) Employees

and Corporate Assets. The information set forth in the Information Statement under the following

captions is incorporated herein by reference:

“Summary”

“Questions

and Answers about the Merger”

“The Special

Factors – Background of the Merger”

“The Special

Factors – Recommendation of the Special Committee; Reasons for the Merger; Recommendation of the Board”

“The Special

Factors – Opinion and Materials of Lazard”

“The Special

Factors – Interests of Our Directors and Executive Officers in the Merger”

“The Special

Factors – Fees and Expenses”

ITEM 15. ADDITIONAL

INFORMATION

(b) Golden

Parachute Compensation. The information set forth in the Information Statement under the following

caption is incorporated herein by reference:

“The Special

Factors – Interests of Our Directors and Executive Officers in the Merger”

“The Merger

Agreement—Consideration to be Received in the Merger”

(c) Other

Material Information. The information set forth in the Information Statement, including all

annexes thereto, is incorporated herein by reference.

ITEM 16. EXHIBITS

| (d)(8) | Services Agreement, dated as of May 7,

2019, by and among Scientific Games Corporation (as predecessor to Light & Wonder, Inc.),

Scientific Games International, Inc. (as predecessor to Light and Wonder International, Inc.),

Bally Gaming, Inc. (as predecessor to LNW Gaming, Inc.) and SciPlay Holding Company, LLC

(as predecessor to SciPlay Games, LLC), incorporated by reference to Exhibit 10.6 to SciPlay Corporation’s

Current Report on Form 8-K filed on May 8, 2019. |

* To be filed herewith

SIGNATURES

After due inquiry

and to the best of each of the undersigned’s knowledge and belief, each of the undersigned certifies that the information set forth

in this statement is true, complete and correct.

Dated as of September 11,

2023.

| |

SCIPLAY CORPORATION |

| |

|

|

| |

By: |

/s/ Daniel O’Quinn |

| |

Name: |

Daniel O’Quinn |

| |

Title: |

Interim Chief Financial Officer and Secretary |

| |

|

|

| |

LIGHT &

WONDER, INC. |

| |

|

|

| |

By: |

/s/

James Sottile |

| |

Name: |

James Sottile |

| |

Title: |

Executive Vice President, Chief

Legal Officer and Corporate Secretary |

| |

|

|

| |

BERN MERGER

SUB, INC. |

| |

|

|

| |

By: |

/s/

James Sottile |

| |

Name: |

James Sottile |

| |

Title: |

President, Treasurer and Secretary |

| |

|

|

| |

LNW SOCIAL

HOLDING COMPANY I, LLC |

| |

|

|

| |

By: |

LNW Social Holding Company II,

LLC, |

| |

|

its sole member |

| |

|

|

| |

By: |

Light and Wonder International,Inc., |

| |

|

its sole member |

| |

|

|

| |

By: |

/s/

James Sottile |

| |

Name: |

James Sottile |

| |

Title: |

Secretary |

| |

|

|

| |

LNW SOCIAL

HOLDING COMPANY II, LLC |

| |

|

|

| |

By: |

Light and Wonder International,Inc., |

| |

|

its sole member |

| |

|

|

| |

By: |

/s/

James Sottile |

| |

Name: |

James Sottile |

| |

Title: |

Treasurer and Secretary |

| |

|

|

| |

LIGHT AND WONDER

INTERNATIONAL, INC. |

| |

|

|

| |

By: |

/s/

James Sottile |

| |

Name: |

James Sottile |

| |

Title: |

Treasurer and Secretary |

Exhibit (c)(3)

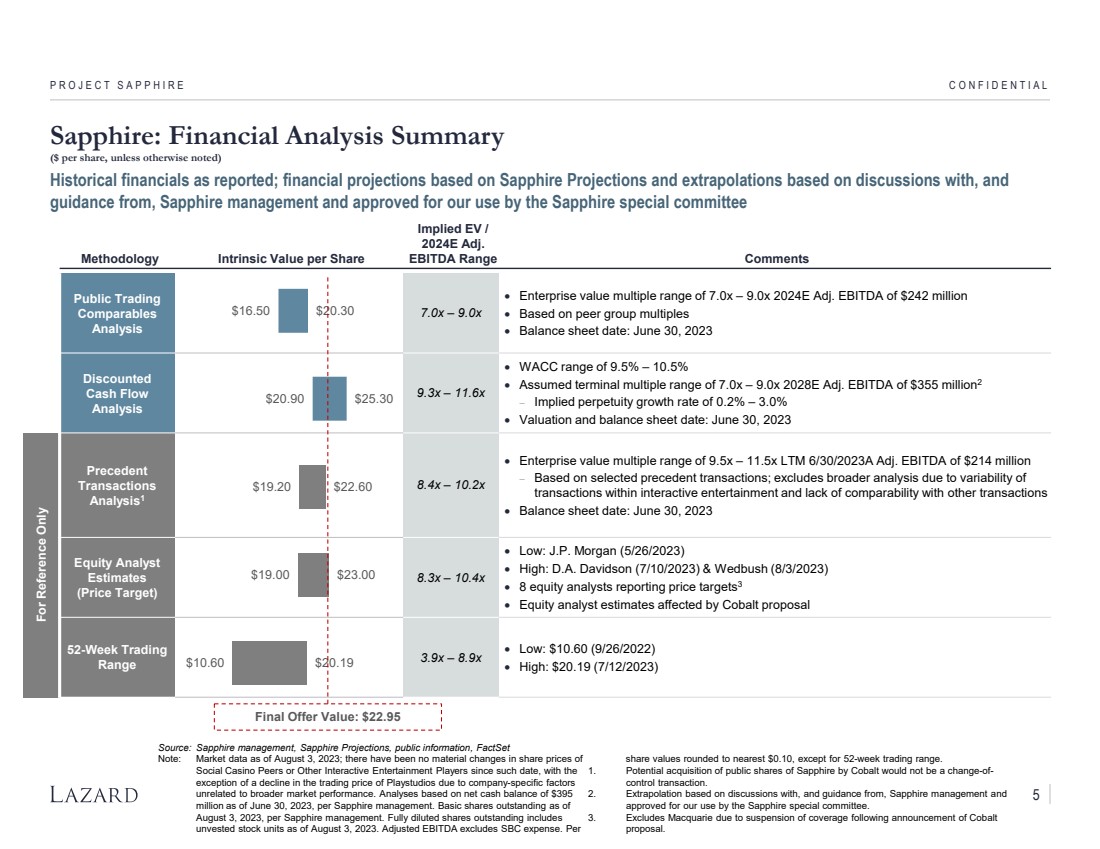

| SPECIAL COMMITTEE DISCUSSION MATERIALS

CONFIDENTIAL 12 JUNE 2023

Project Sapphire |

| PROJECT SAPPHIRE CONFIDENTIAL

The Lazard Team for the Special Committee of Sapphire

Interactive Media & Technologies Team and Special Committee Expertise

David Higley

Managing Director, Global Head of Interactive Media & Technologies

• Based in Los Angeles, with 25+ years of investment banking experience

• Prior to Lazard, founded Bond Lane Partners, a boutique investment bank focused on

interactive media and technologies and served as Managing Director and Global Head of

Digital Media at UBS as well as a member of its Equity Commitment Committee

• Former securities lawyer

• Recent clients include Activision, Bungie, Capcom, Hearst, Lockwood Publishing (Tencent),

Miximo (Adobe), OneTwoSee (Comcast), SciPlay, Sony, Unity Software

Vivienne Zhao

Director

• Based in Los Angeles, with 8+

years of investment banking

experience

• M: +1 847 924 9422

• E: vivienne.zhao@lazard.com

• Based in Los Angeles, with 9+

years of financial advisory

experience

• M: +1 562 447 9460

• E: albert.toscano@lazard.com

Albert Toscano

Senior Associate

Selena Zhu

Associate

• Based in Los Angeles, specializing in

Interactive Media &

Technologies

• T: +1 310 367 5015

• E: selena.zhu@lazard.com

• Based in Los Angeles, specializing in

Interactive Media & Technologies

and Industrials

• T: +1 310 601 3460

• E: chandler.pearce@lazard.com

Chandler Pearce

Analyst

Joe Cassanelli

Managing Director, Co-Head of Financial Institutions Group North America

• Based in New York, with 25+ years of investment banking

and advisory experience

• Member of Lazard's Fairness Opinion Committee and

Lazard's Valuation Subcommittee

• Prior to joining Lazard, worked at Dresdner Kleinwort Wasserstein

and Wasserstein Perella & Co.

• Special Committee expertise

• Recent clients include Allstate, American Express, Ameriprise,

Apollo, Ares, Aviva, Blackstone, First Republic Bank, J.P. Morgan,

KKR, Nestle, Western Union

Capital Markets Advisory

Mary Ann Deignan

Co-Head of Capital Markets

Advisory

New York

John Buchanan

Managing Director

New York

1 |

| CONFIDENTIAL

Situation Update

PROJECT SAPPHIRE |

| Summary of Cobalt’s Proposal to Acquire Public Shares of Sapphire

PROJECT SAPPHIRE SITUATION UPDATE

• On May 18, 2023, Cobalt submitted to the Sapphire Board of Directors a proposal for Cobalt to acquire the 17% equity interest in

Sapphire that it does not currently own for $20.00 per share in cash

− Values Sapphire at $2.1 billion in enterprise value and public shares at $422 million1

• Implied multiple of 10.4x 2023E Adj. EBITDA based on consensus estimates as of May 17, 2023, the last trading day prior to the

proposal (the “unaffected date”)

− Implies a premium of 28.5% based on Sapphire’s closing stock price on the unaffected date

• Implied premium of 17.9% based on Sapphire’s 10-trading day VWAP as of unaffected date and 17.0% based on Sapphire’s 30-trading

day VWAP as of unaffected date

• Cobalt’s stated intent for the proposal based on unifying Cobalt businesses and combining balance sheets to enable greater flexibility

to invest across the enterprise; not driven by cost synergy opportunities

• Proposal conditioned upon approval of special committee of independent directors

• Proposal not conditioned upon approval of independent shareholders

− As holder of ~83% of the economic interest and ~98% of the voting interest of Sapphire, Cobalt intends to vote in favor of the proposal; does

not expect to vote in favor of any alternative sale, merger or other corporate transaction involving Sapphire nor divest or sell any portion of its

ownership interest

Source: Public information, Bloomberg

Note: Unaffected date as of May 17, 2023 (last trading day prior to proposal by Cobalt).

1. Per Cobalt press release; $425 million offer value based on publicly disclosed shares of Sapphire Class A Common Stock as of May 4, 2023, per Sapphire Q1 2023 10-Q. 2 |

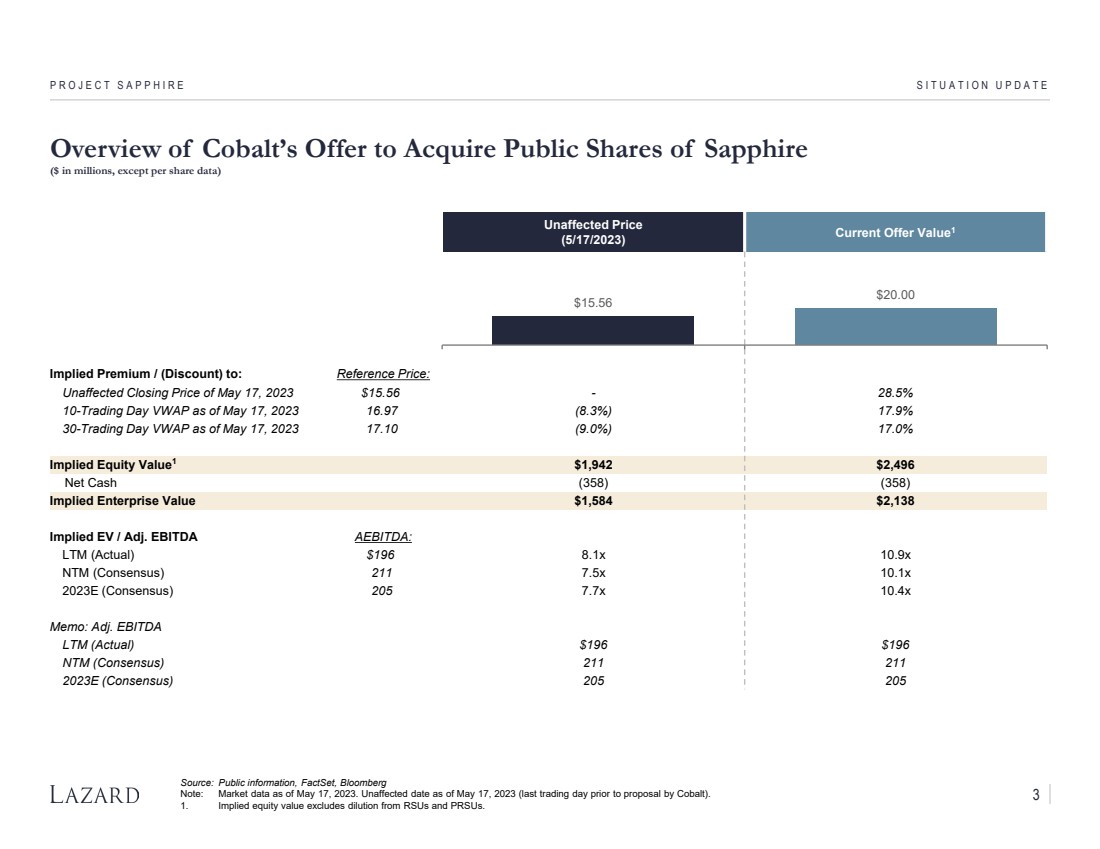

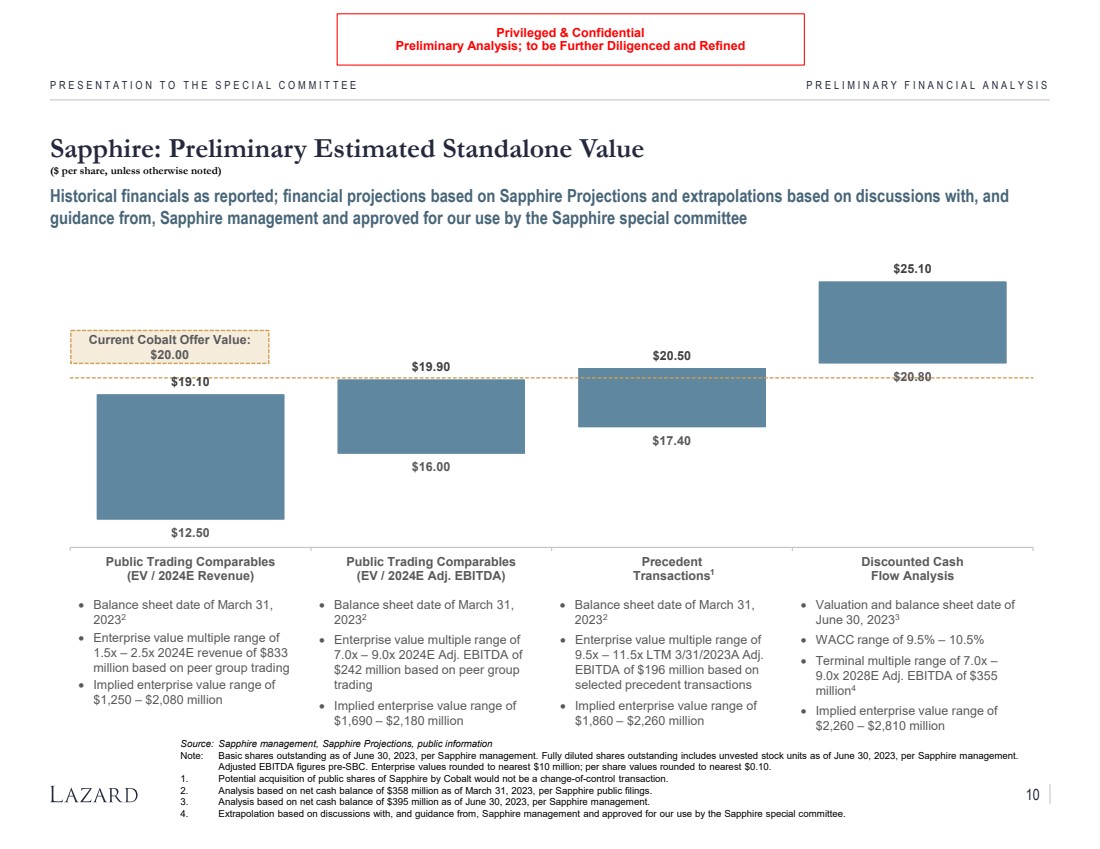

| Overview of Cobalt’s Offer to Acquire Public Shares of Sapphire

($ in millions, except per share data)

PROJECT SAPPHIRE SITUATION UPDATE

Source: Public information, FactSet, Bloomberg

Note: Market data as of May 17, 2023. Unaffected date as of May 17, 2023 (last trading day prior to proposal by Cobalt).

1. Implied equity value excludes dilution from RSUs and PRSUs.

Unaffected Price

(5/17/2023) Current Offer Value1

Implied Premium / (Discount) to: Reference Price:

Unaffected Closing Price of May 17, 2023 $15.56 - 28.5%

10-Trading Day VWAP as of May 17, 2023 16.97 (8.3%) 17.9%

30-Trading Day VWAP as of May 17, 2023 17.10 (9.0%) 17.0%

Implied Equity Value1 $1,942 $2,496

Net Cash (358) (358)

Implied Enterprise Value $1,584 $2,138

Implied EV / Adj. EBITDA AEBITDA:

LTM (Actual) $196 8.1x 10.9x

NTM (Consensus) 211 7.5x 10.1x

2023E (Consensus) 205 7.7x 10.4x

Memo: Adj. EBITDA

LTM (Actual) $196 $196

NTM (Consensus) 211 211

2023E (Consensus) 205 205

$15.56 $20.00

3 |

| 6

8

10

12

14

16

18

20

22

$24

Jan-22 Apr-22 Jul-22 Oct-22 Feb-23 May-23

Sapphire Social Casino Peers

PROJECT SAPPHIRE SITUATION UPDATE

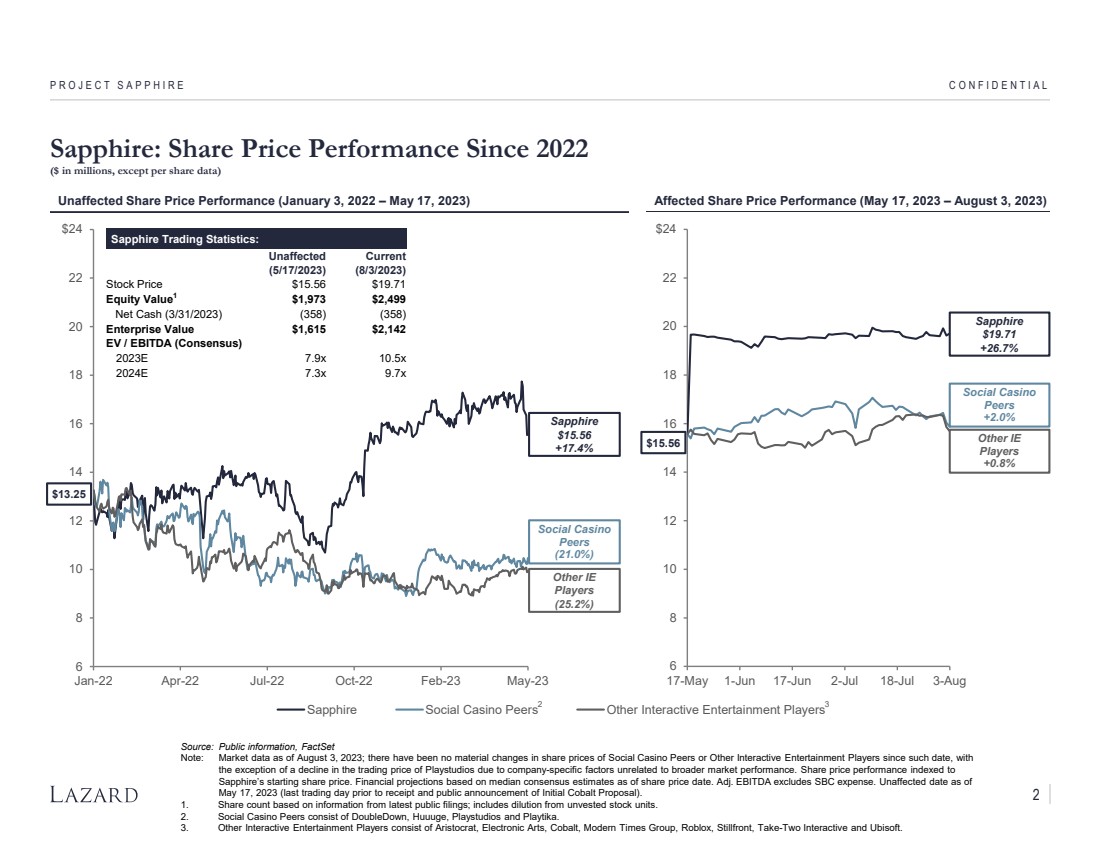

Sapphire Trading Statistics:

Unaffected1

(5/17/2023)

Current2

(6/7/2023)

Stock Price $15.56 $19.17

Equity Value4 $1,973 $2,431

Net Cash (358) (358)

Enterprise Value $1,615 $2,073

EV / 2023E EBITDA 7.9x 10.1x

Unaffected Share Price Performance (January 3, 2022 – May 17, 2023)

3

Sapphire

$15.56

+17.4%

Social Casino

Peers

(21.0%)

Source: Public information, FactSet

Note: Market data as of June 7, 2023. Share price performance indexed to Sapphire’s starting share price. Financial projections based on median consensus estimates; balance sheet

and share count based on latest publicly available data as of share price date. Unaffected date as of May 17, 2023 (last trading day prior to proposal by Cobalt).

1. Financials and market data as of May 17, 2023.

2. Financials and market data as of June 7, 2023.

3. Social Casino peers consist of DoubleDown, Huuuge, Playstudios and Playtika.

4. Equity value on fully diluted basis, including dilution from RSUs and PRSUs.

Sapphire: Share Price Performance Since 2022

($ in millions, except per share data)

6

8

10

12

14

16

18

20

22

$24

17-May 24-May 31-May 7-Jun

Affected Share Price Performance (May 17, 2023 – June 7, 2023)

$15.56

$13.25

Sapphire

$19.17

+23.2%

Social Casino

Peers

3.2%

4 |

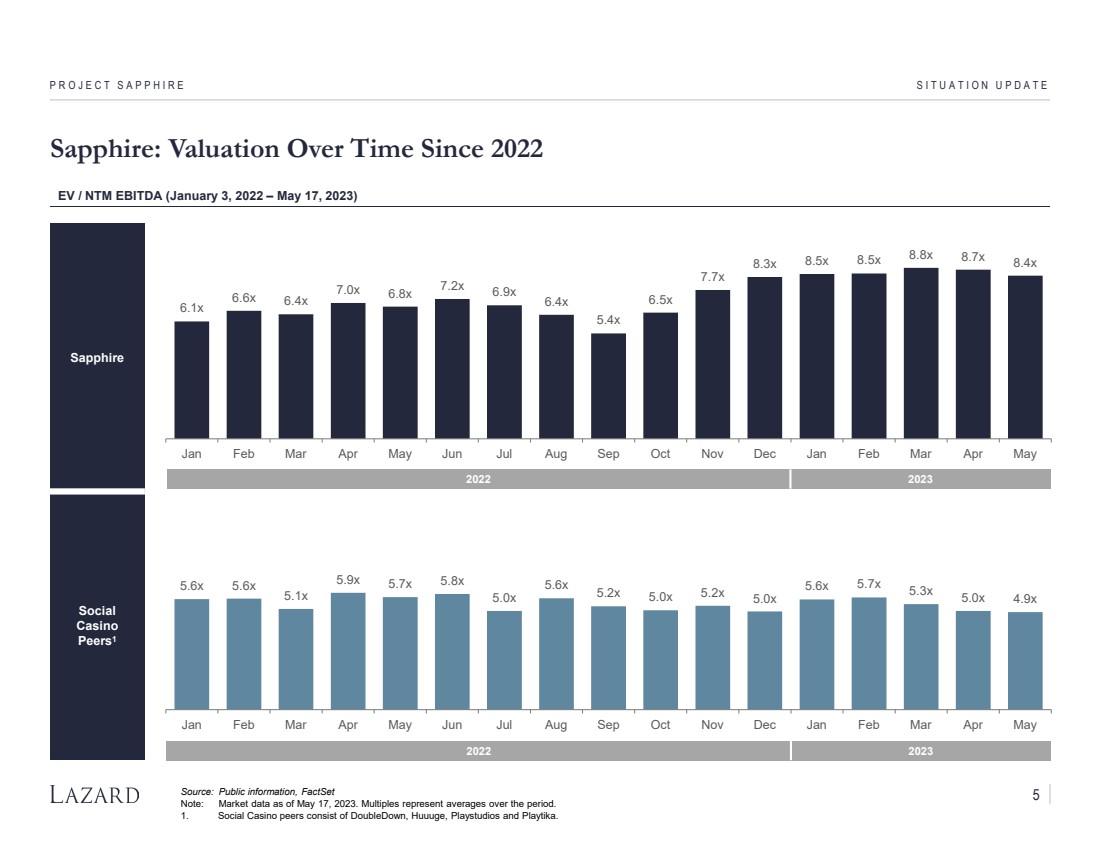

| Sapphire

Social

Casino

Peers1

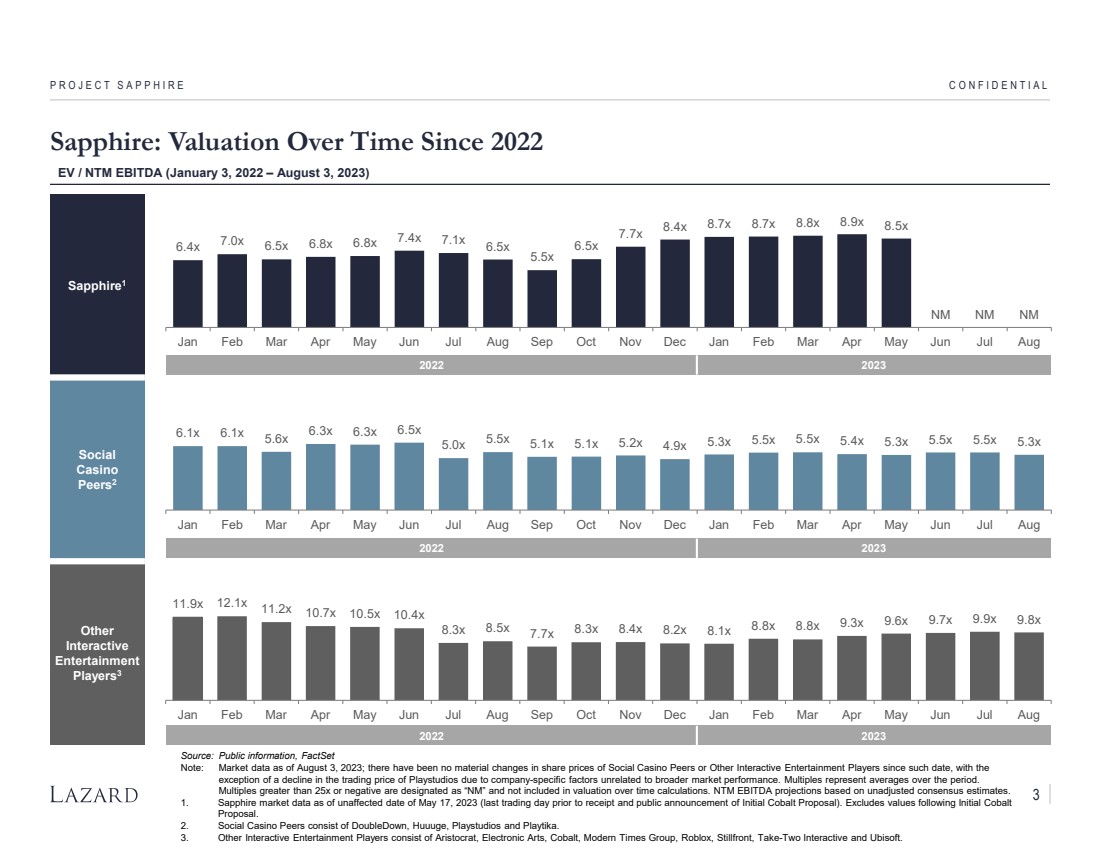

6.1x

6.6x 6.4x

7.0x 6.8x 7.2x 6.9x

6.4x

5.4x

6.5x

7.7x

8.3x 8.5x 8.5x 8.8x 8.7x 8.4x

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May

5.6x 5.6x

5.1x

5.9x 5.7x 5.8x

5.0x

5.6x 5.2x 5.0x 5.2x 5.0x

5.6x 5.7x 5.3x 5.0x 4.9x

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May

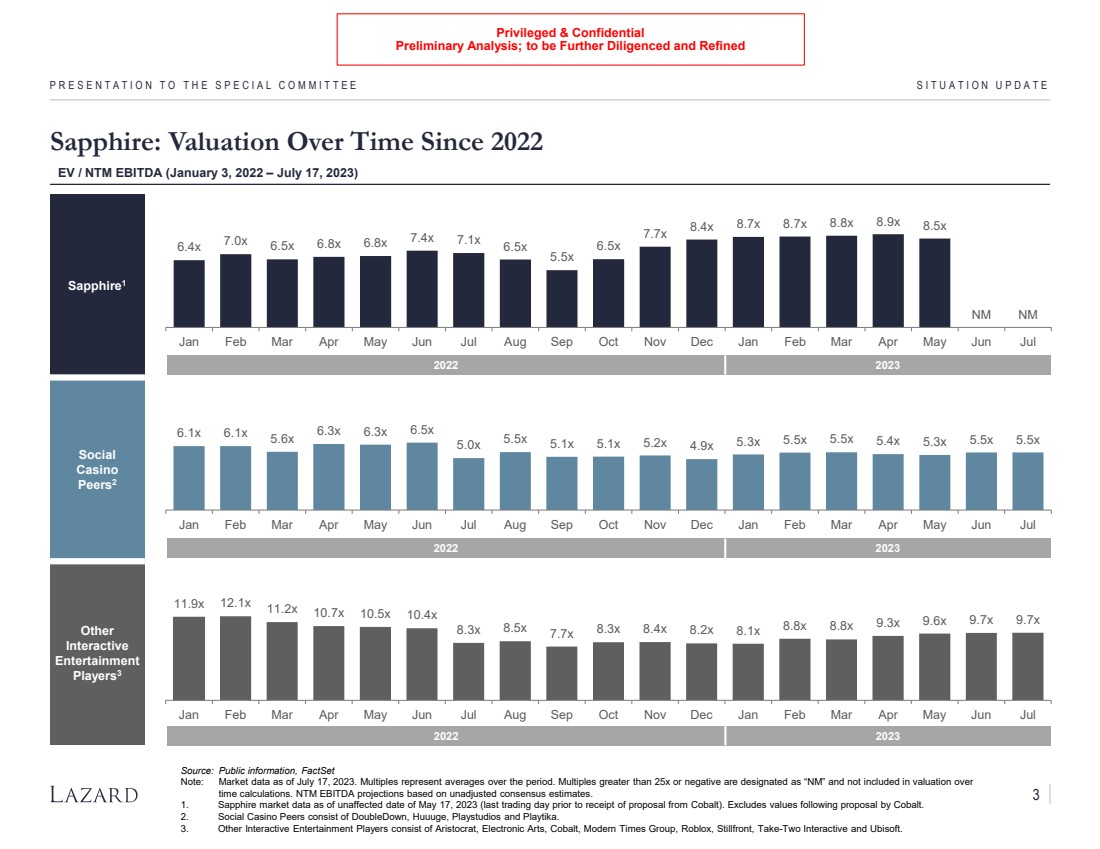

Sapphire: Valuation Over Time Since 2022

PROJECT SAPPHIRE SITUATION UPDATE

EV / NTM EBITDA (January 3, 2022 – May 17, 2023)

Source: Public information, FactSet

Note: Market data as of May 17, 2023. Multiples represent averages over the period.

1. Social Casino peers consist of DoubleDown, Huuuge, Playstudios and Playtika.

2022 2023

2022 2023

5 |

| CONFIDENTIAL

Preliminary Financial Analysis

PROJECT SAPPHIRE |

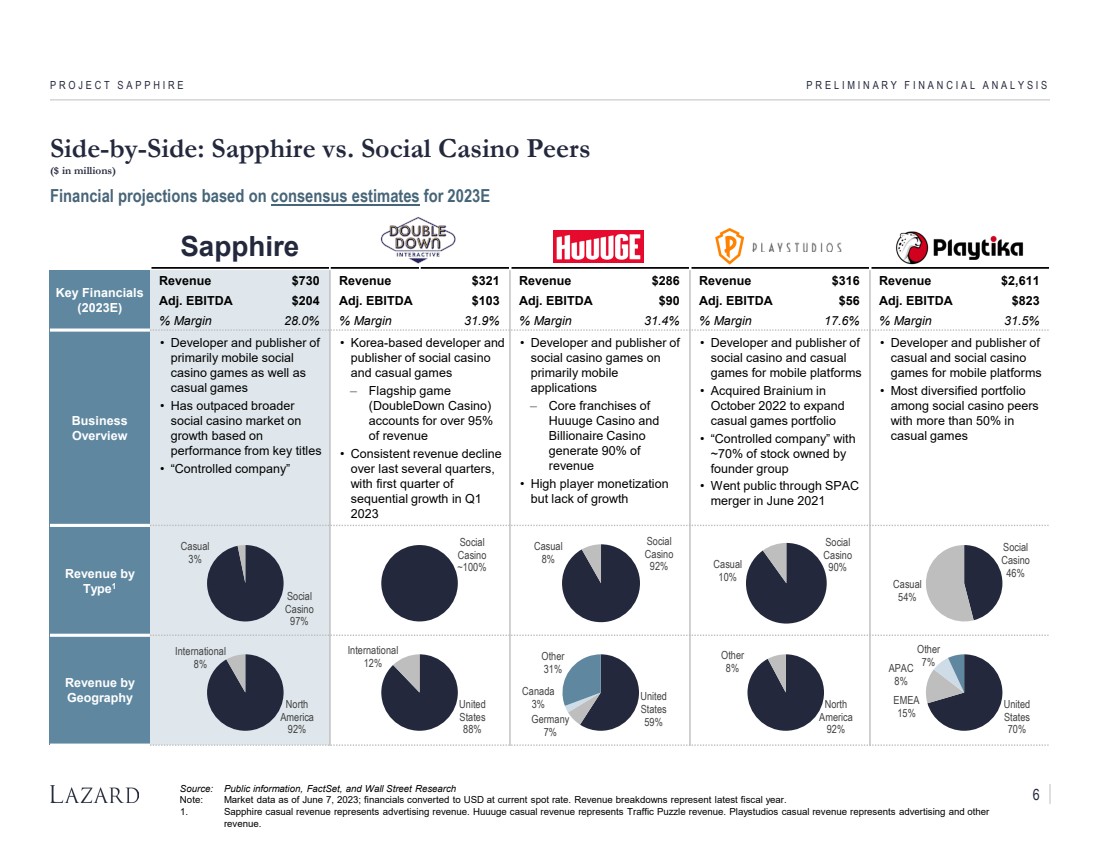

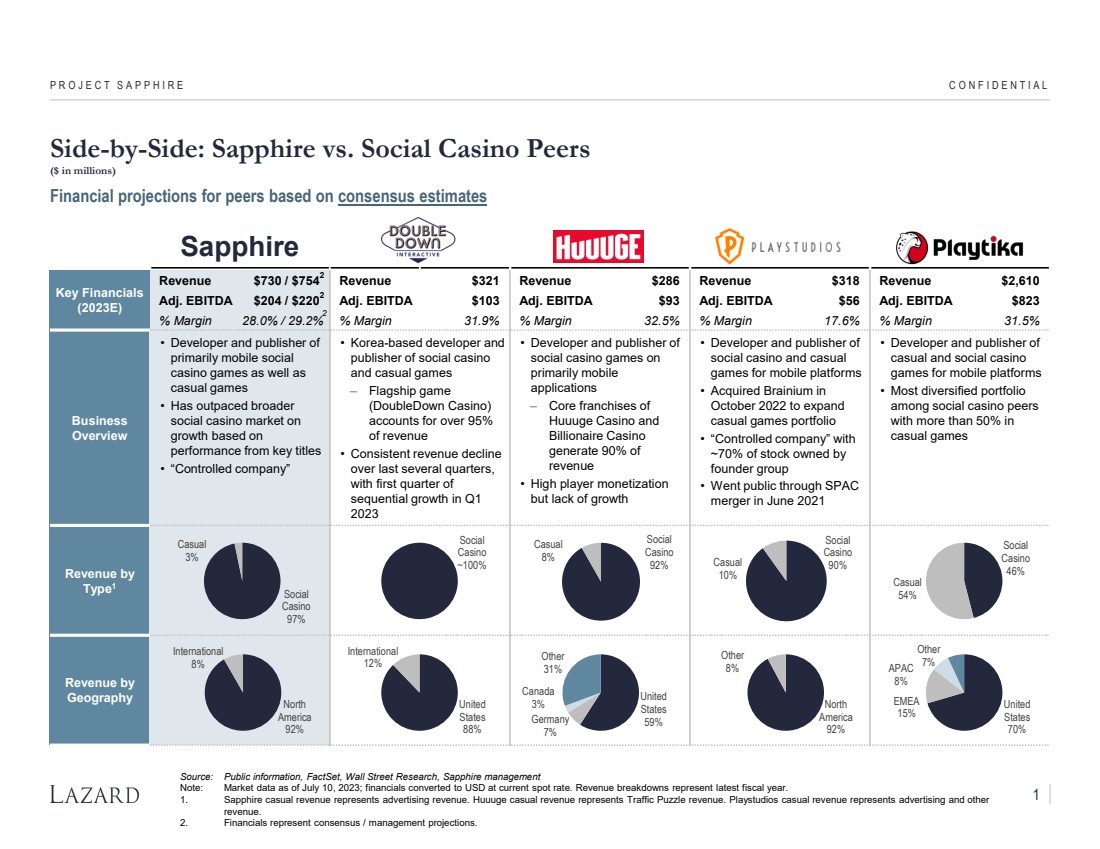

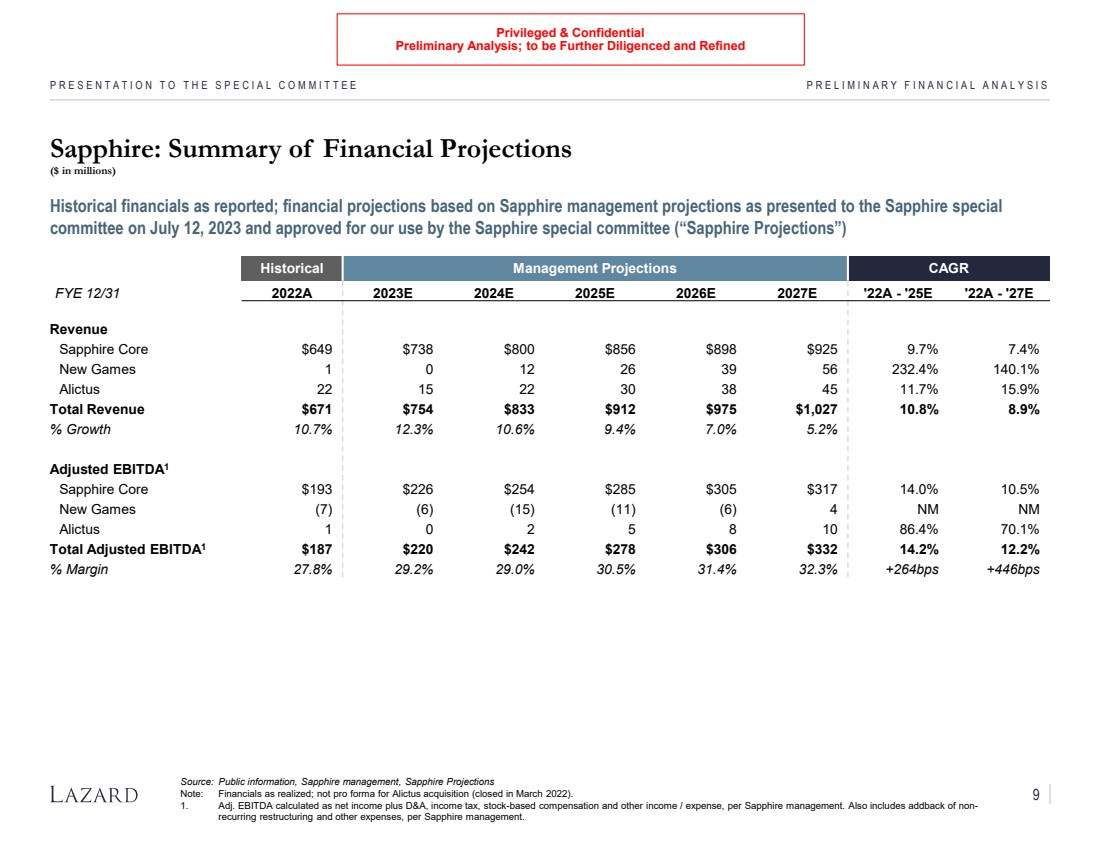

| Sapphire

Key Financials

(2023E)

Revenue $730 Revenue $321 Revenue $286 Revenue $316 Revenue $2,611

Adj. EBITDA $204 Adj. EBITDA $103 Adj. EBITDA $90 Adj. EBITDA $56 Adj. EBITDA $823

% Margin 28.0% % Margin 31.9% % Margin 31.4% % Margin 17.6% % Margin 31.5%

Business

Overview

• Developer and publisher of

primarily mobile social

casino games as well as

casual games

• Has outpaced broader

social casino market on

growth based on

performance from key titles

• “Controlled company”

• Korea-based developer and

publisher of social casino

and casual games

‒ Flagship game

(DoubleDown Casino)

accounts for over 95%

of revenue

• Consistent revenue decline

over last several quarters,

with first quarter of

sequential growth in Q1

2023

• Developer and publisher of

social casino games on

primarily mobile

applications

‒ Core franchises of

Huuuge Casino and

Billionaire Casino

generate 90% of

revenue

• High player monetization

but lack of growth

• Developer and publisher of

social casino and casual

games for mobile platforms

• Acquired Brainium in

October 2022 to expand

casual games portfolio

• “Controlled company” with

~70% of stock owned by

founder group

• Went public through SPAC

merger in June 2021

• Developer and publisher of

casual and social casino

games for mobile platforms

• Most diversified portfolio

among social casino peers

with more than 50% in

casual games

Revenue by

Type1

Revenue by

Geography

Side-by-Side: Sapphire vs. Social Casino Peers

($ in millions)

PROJECT SAPPHIRE PRELIMINARY FINANCIAL ANALYSIS

Source: Public information, FactSet, and Wall Street Research

Note: Market data as of June 7, 2023; financials converted to USD at current spot rate. Revenue breakdowns represent latest fiscal year.

1. Sapphire casual revenue represents advertising revenue. Huuuge casual revenue represents Traffic Puzzle revenue. Playstudios casual revenue represents advertising and other

revenue.

Financial projections based on consensus estimates for 2023E

North

America

92%

International

8%

Social

Casino

97%

Casual

3%

United

States

Germany 59%

7%

Canada

3%

Other

31%

Social

Casino

92%

Casual

8%

North

America

92%

Other

8%

Social

Casino

Casual 90%

10%

United

States

70%

EMEA

15%

APAC

8%

Other

7%

Social

Casino

46%

Casual

54%

United

States

88%

International

12%

Social

Casino

~100%

6 |

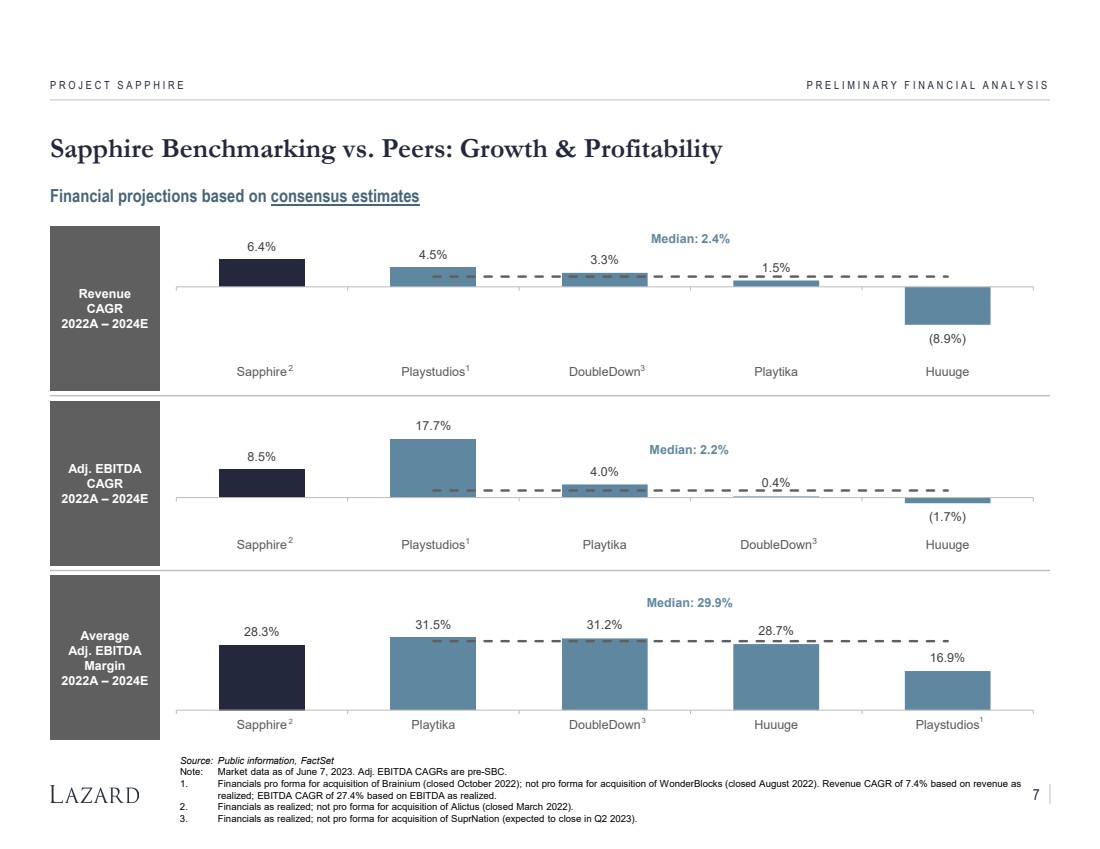

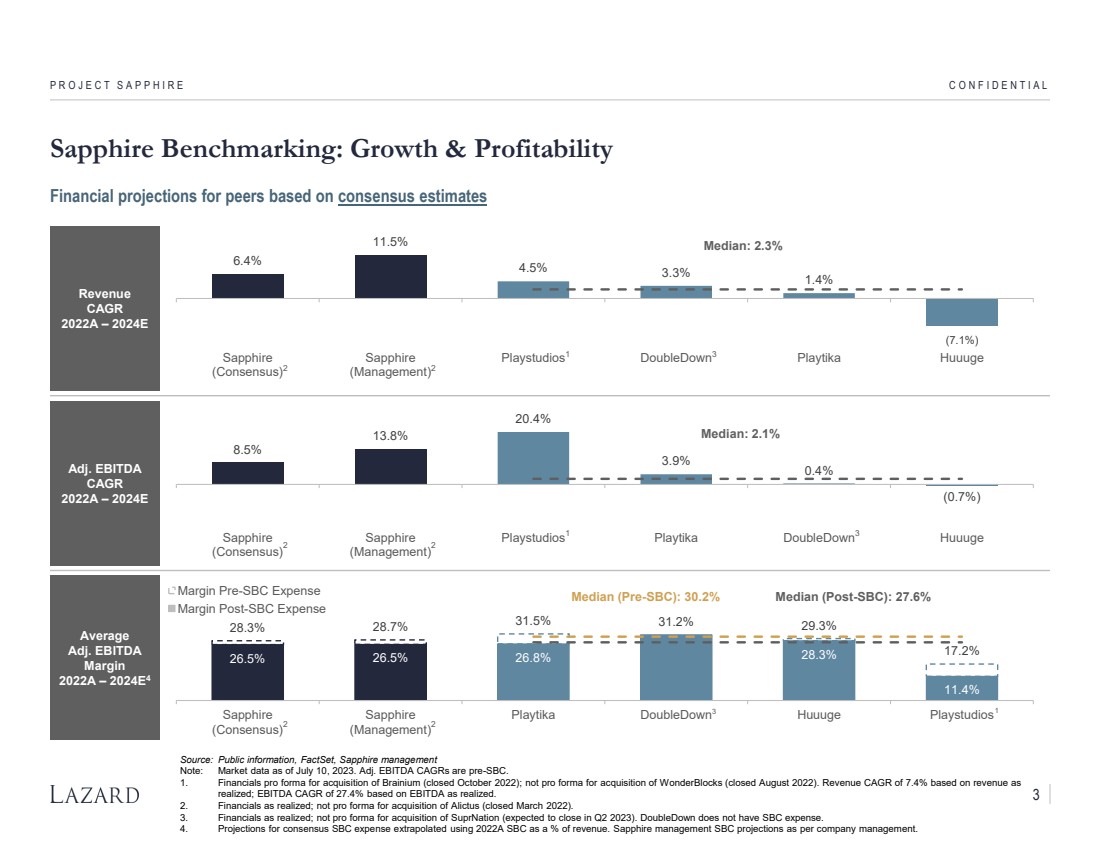

| Revenue

CAGR

2022A – 2024E

Adj. EBITDA

CAGR

2022A – 2024E

Average

Adj. EBITDA

Margin

2022A – 2024E

6.4% 4.5% 3.3% 1.5%

(8.9%)

Median: 2.4%

Sapphire Playstudios DoubleDown Playtika Huuuge

Sapphire Benchmarking vs. Peers: Growth & Profitability

PROJECT SAPPHIRE PRELIMINARY FINANCIAL ANALYSIS

Source: Public information, FactSet

Note: Market data as of June 7, 2023. Adj. EBITDA CAGRs are pre-SBC.

1. Financials pro forma for acquisition of Brainium (closed October 2022); not pro forma for acquisition of WonderBlocks (closed August 2022). Revenue CAGR of 7.4% based on revenue as

realized; EBITDA CAGR of 27.4% based on EBITDA as realized.

2. Financials as realized; not pro forma for acquisition of Alictus (closed March 2022).

3. Financials as realized; not pro forma for acquisition of SuprNation (expected to close in Q2 2023).

Financial projections based on consensus estimates

2 1 3

7

8.5%

17.7%

4.0%

0.4%

(1.7%)

Median: 2.2%

Sapphire Playstudios Playtika DoubleDown Huuuge 2 1 3

28.3% 31.5% 31.2% 28.7%

16.9%

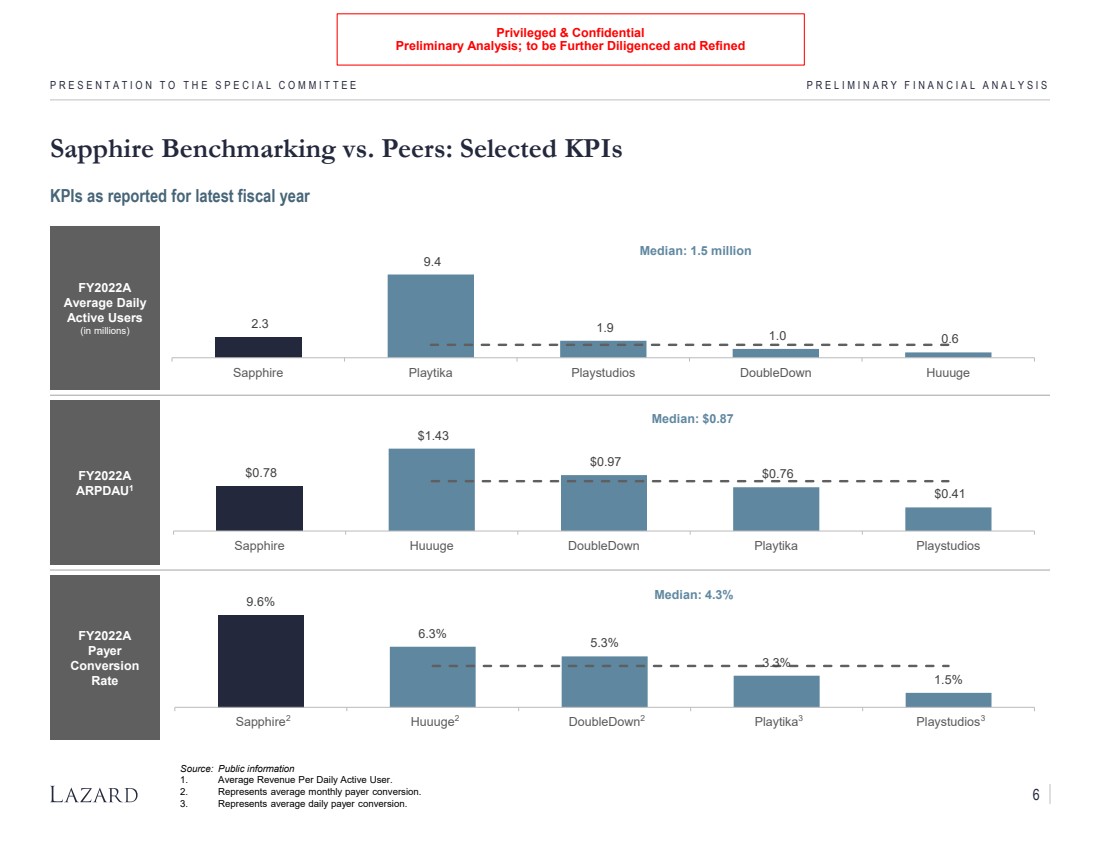

Median: 29.9%

Sapphire Playtika DoubleDown Huuuge Playstudios 2 3 1 |

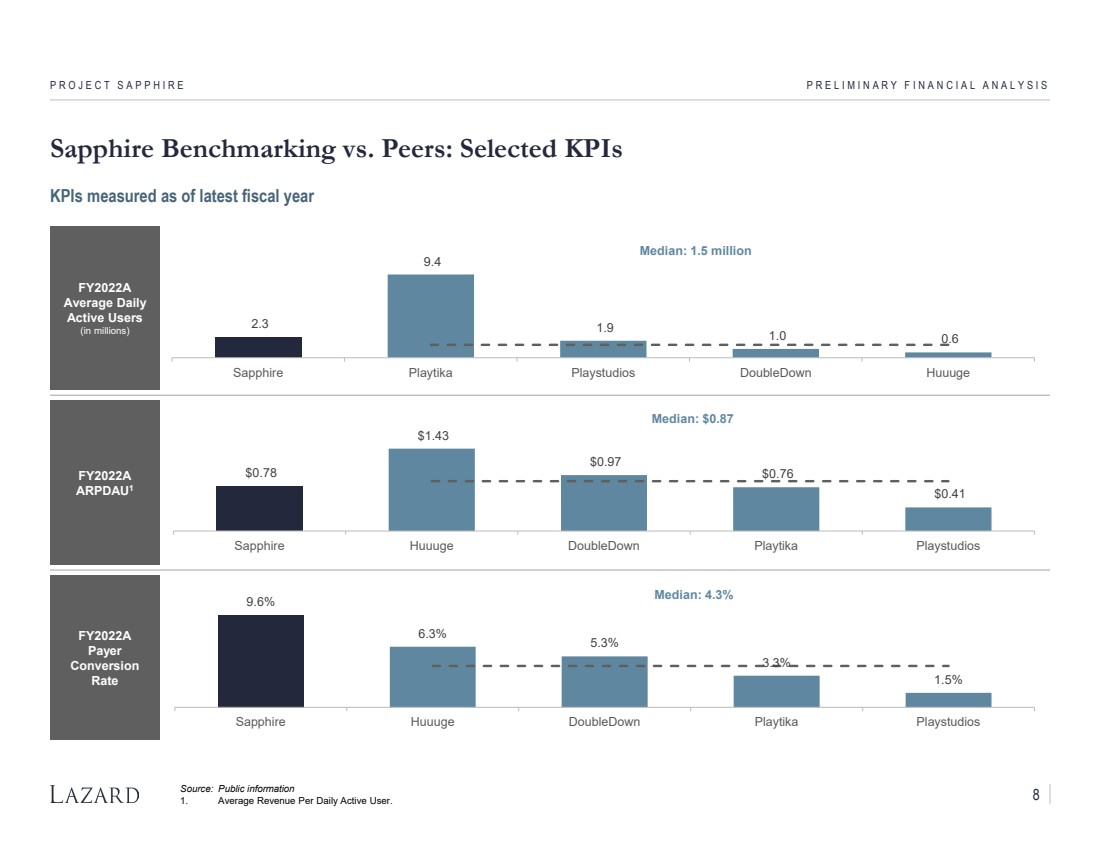

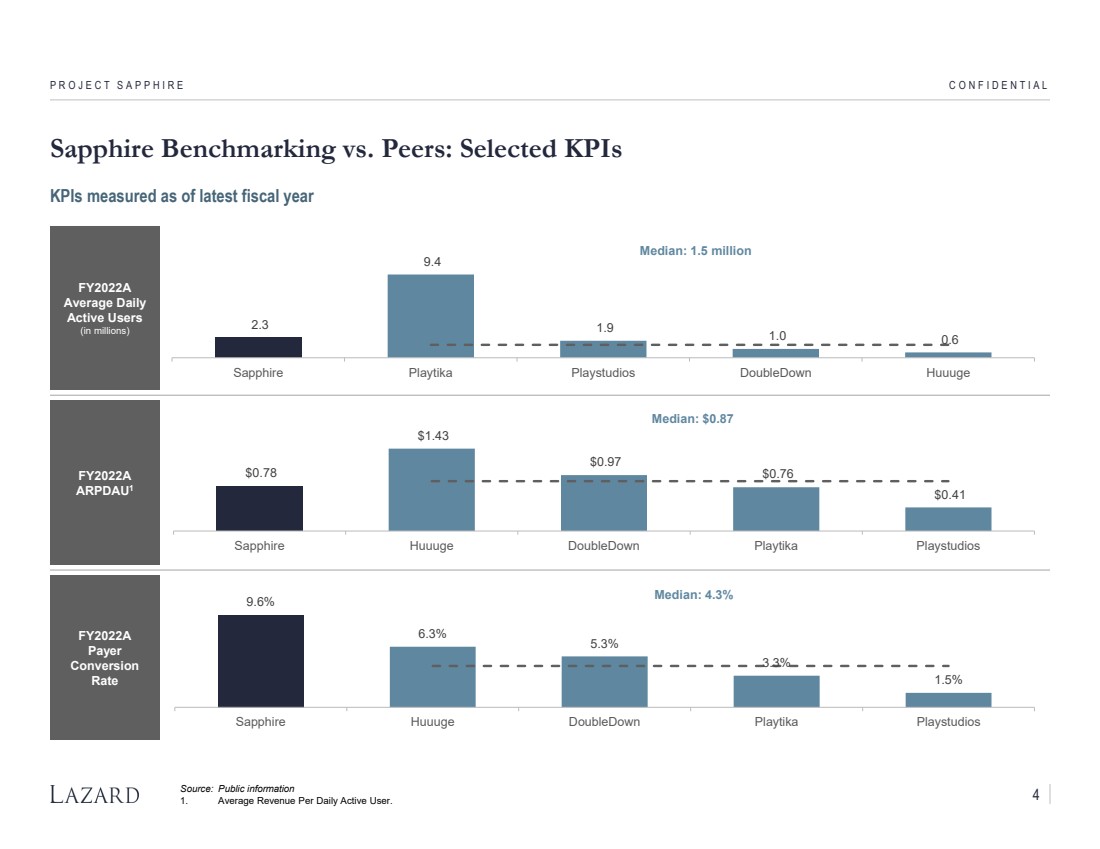

| Social Casino Peers

FY2022A

Average Daily

Active Users

(in millions)

FY2022A

ARPDAU1

FY2022A

Payer

Conversion

Rate

9.6%

6.3%

5.3%

3.3%

1.5%

Median: 4.3%

Sapphire Huuuge DoubleDown Playtika Playstudios

$0.78

$1.43

$0.97

$0.76

$0.41

Median: $0.87

Sapphire Huuuge DoubleDown Playtika Playstudios

Sapphire Benchmarking vs. Peers: Selected KPIs

PROJECT SAPPHIRE PRELIMINARY FINANCIAL ANALYSIS

Source: Public information

1. Average Revenue Per Daily Active User.

2.3

9.4

1.9 1.0 0.6

Median: 1.5 million

Sapphire Playtika Playstudios DoubleDown Huuuge

KPIs measured as of latest fiscal year

8 |

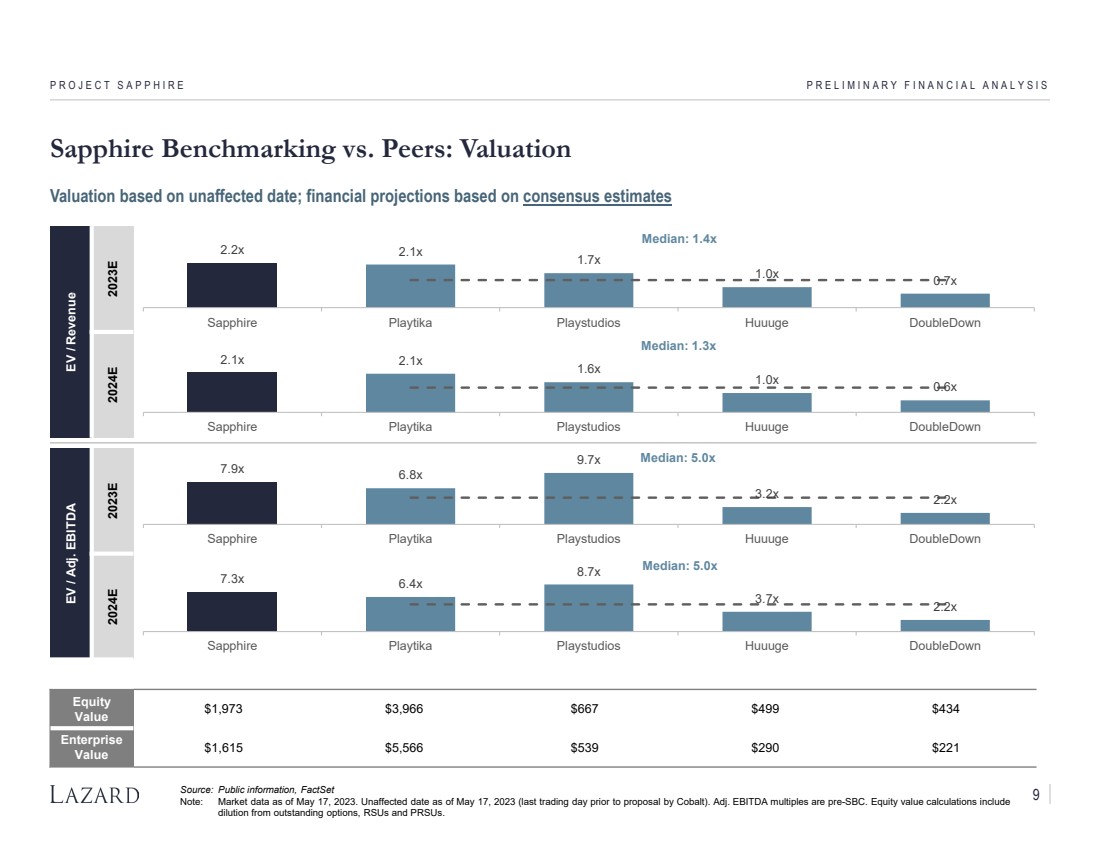

| Social Casino Peers

EV / Revenue

2023E 2024E

EV / Adj. EBITDA

2023E 2024E

Equity

Value $1,973 $3,966 $667 $499 $434

Enterprise

Value $1,615 $5,566 $539 $290 $221

2.1x 2.1x 1.6x

1.0x 0.6x

Median: 1.3x

Sapphire Playtika Playstudios Huuuge DoubleDown

7.3x 6.4x

8.7x

3.7x 2.2x

Median: 5.0x

Sapphire Playtika Playstudios Huuuge DoubleDown

7.9x 6.8x

9.7x

3.2x 2.2x

Median: 5.0x

Sapphire Playtika Playstudios Huuuge DoubleDown

Sapphire Benchmarking vs. Peers: Valuation

PROJECT SAPPHIRE PRELIMINARY FINANCIAL ANALYSIS

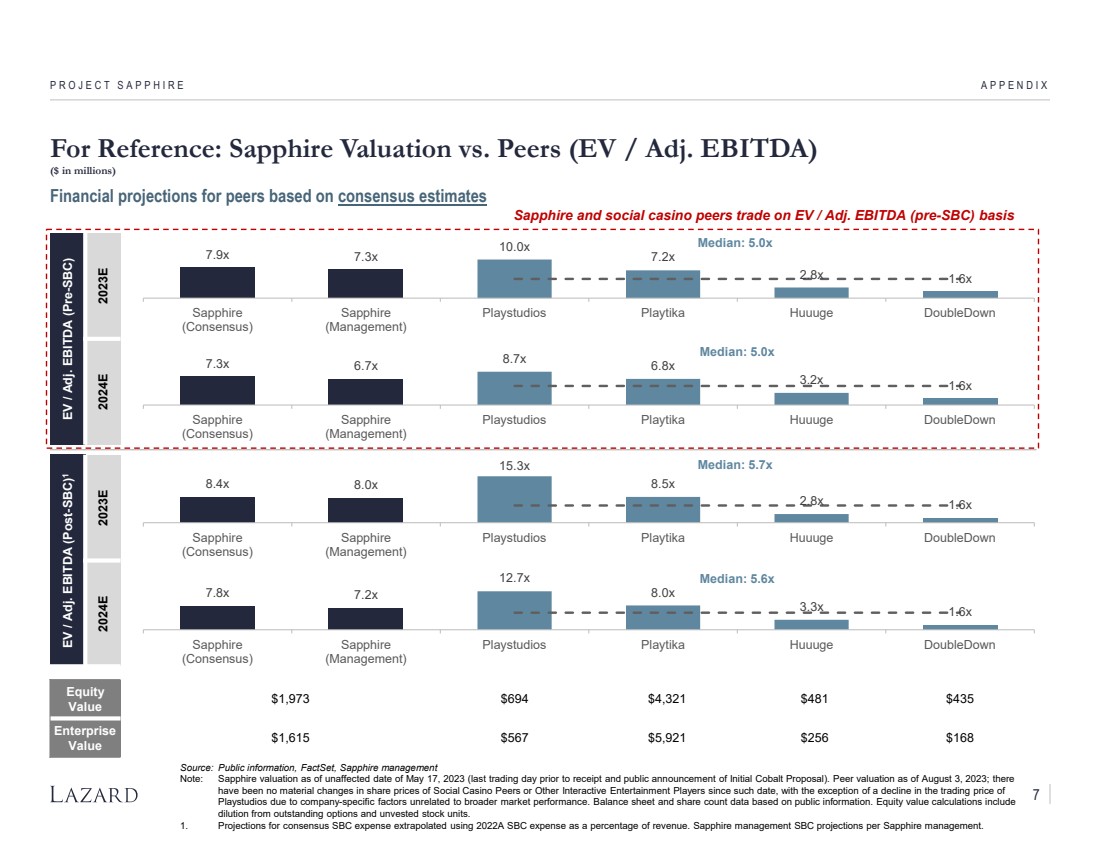

Source: Public information, FactSet

Note: Market data as of May 17, 2023. Unaffected date as of May 17, 2023 (last trading day prior to proposal by Cobalt). Adj. EBITDA multiples are pre-SBC. Equity value calculations include

dilution from outstanding options, RSUs and PRSUs.

2.2x 2.1x 1.7x

1.0x 0.7x

Median: 1.4x

Sapphire Playtika Playstudios Huuuge DoubleDown

Valuation based on unaffected date; financial projections based on consensus estimates

9 |

| CONFIDENTIAL

Key Process Workstreams

PROJECT SAPPHIRE |

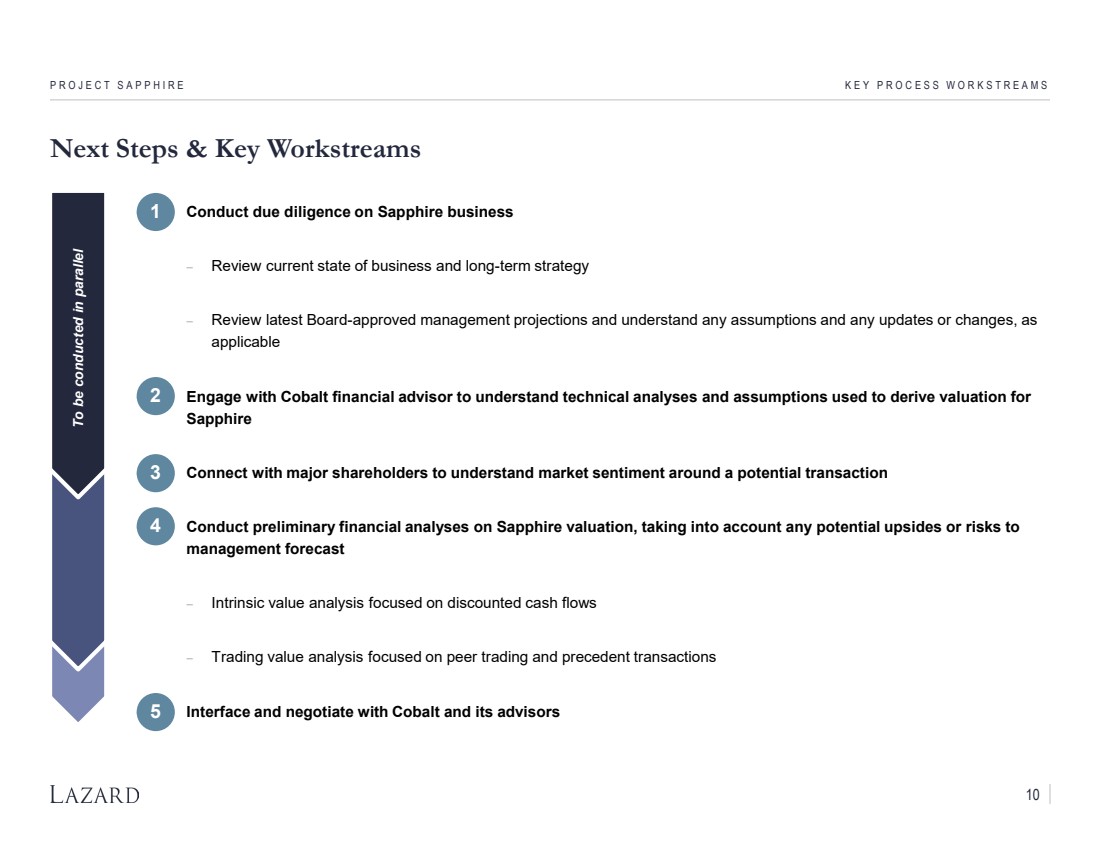

| Next Steps & Key Workstreams

• Conduct due diligence on Sapphire business

− Review current state of business and long-term strategy

− Review latest Board-approved management projections and understand any assumptions and any updates or changes, as

applicable

• Engage with Cobalt financial advisor to understand technical analyses and assumptions used to derive valuation for

Sapphire

• Connect with major shareholders to understand market sentiment around a potential transaction

• Conduct preliminary financial analyses on Sapphire valuation, taking into account any potential upsides or risks to

management forecast

− Intrinsic value analysis focused on discounted cash flows

− Trading value analysis focused on peer trading and precedent transactions

• Interface and negotiate with Cobalt and its advisors

PROJECT SAPPHIRE KEY PROCESS WORKSTREAMS

1

2

3

4

5

To be conducted in parallel

10 |

| CONFIDENTIAL

Appendix

PROJECT SAPPHIRE |

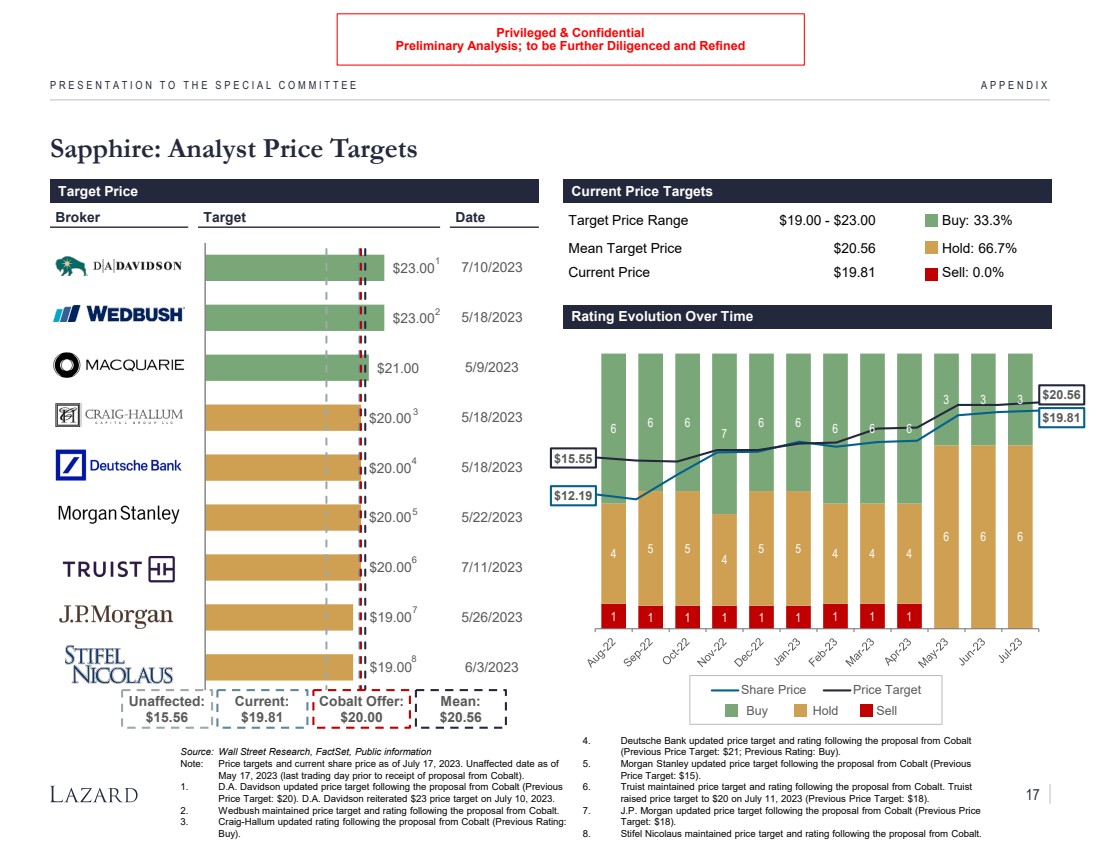

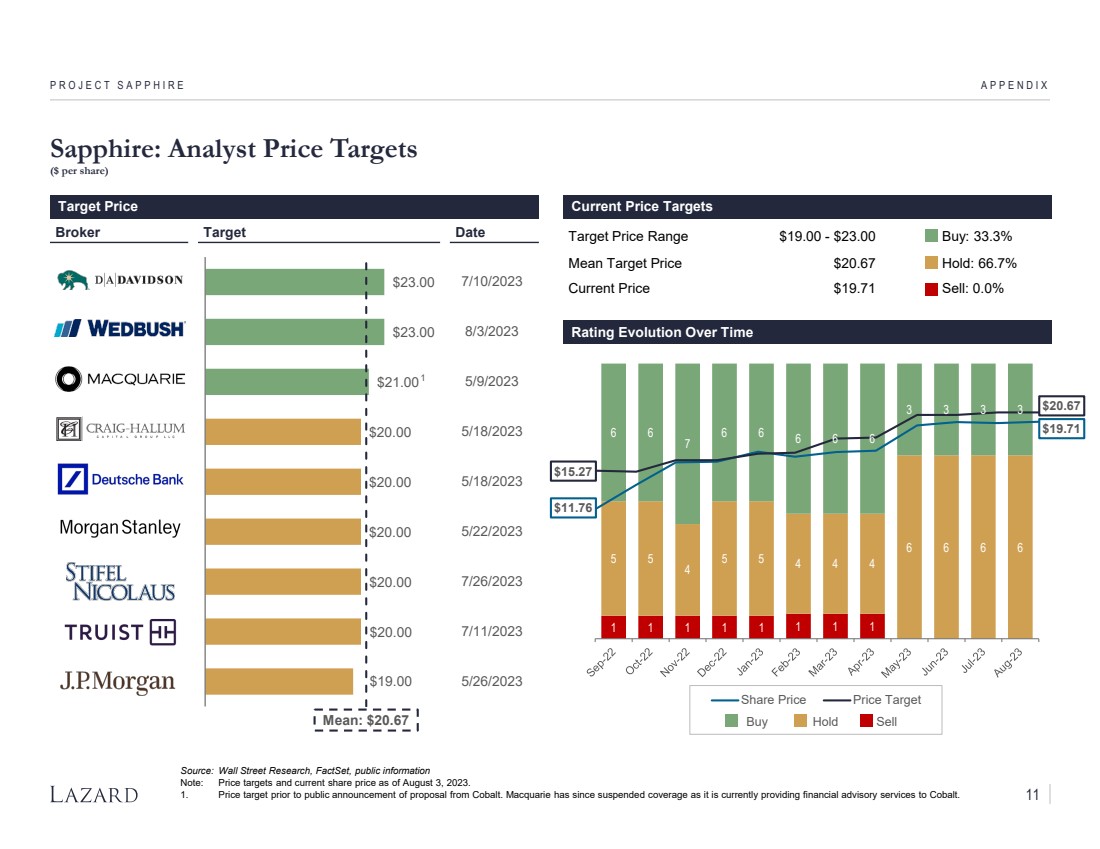

| $23.00

$23.00

$21.00

$20.00

$20.00

$20.00

$19.00

$19.00

$18.00

Sapphire: Analyst Price Targets

PROJECT SAPPHIRE APPENDIX

Target Price Range $18.00 - $23.00 Buy: 33.3%

Mean Target Price $20.33 Hold: 66.7%

Current Price $19.17 Sell: 0.0%

Broker Target Date

Target Price Current Price Targets

Rating Evolution Over Time

Current:

$19.17

Mean:

$20.33

1 1 1 1 1 1 1 1 1

5

4 5 5

4

5 5 4 4 4

6 6

6 6 6 6

7

6 6 6 6 6

3 3

Jul-22 Aug-22Sep-22 Oct-22 Nov-22Dec-22 Jan-23 Feb-23 Mar-23 Apr-23 May-23 Jun-23

Share Price Price Target

Buy Hold Sell

$16.30

$13.64

$20.33

$19.17

5/18/2023

5/18/2023

5/10/2023

5/18/2023

5/18/2023

5/22/2023

5/26/2023

6/3/2023

5/15/2023

Source: Wall Street Research, FactSet, Public information

Note: Price targets and share price as of June 7, 2023.

1. D.A. Davidson updated price target following the proposal from Cobalt (Previous

Price Target: $20).

2. Wedbush maintained price target and rating following the proposal from Cobalt.

3. Craig-Hallum updated rating following the proposal from Cobalt (Previous Rating:

Buy).

4. Deutsche Bank updated price target and rating following the proposal from Cobalt

(Previous Price Target: $21; Previous Rating: Buy).

5. Morgan Stanley updated price target following the proposal from Cobalt (Previous

Price Target: $15).

6. J.P.Morgan updated price target following the proposal from Cobalt (Previous Price

Target: $18).

7. Stifel Nicolaus maintained price target and rating following the proposal from Cobalt.

Cobalt Offer:

$20.00

1

3

4

5

2

6

7

11 |

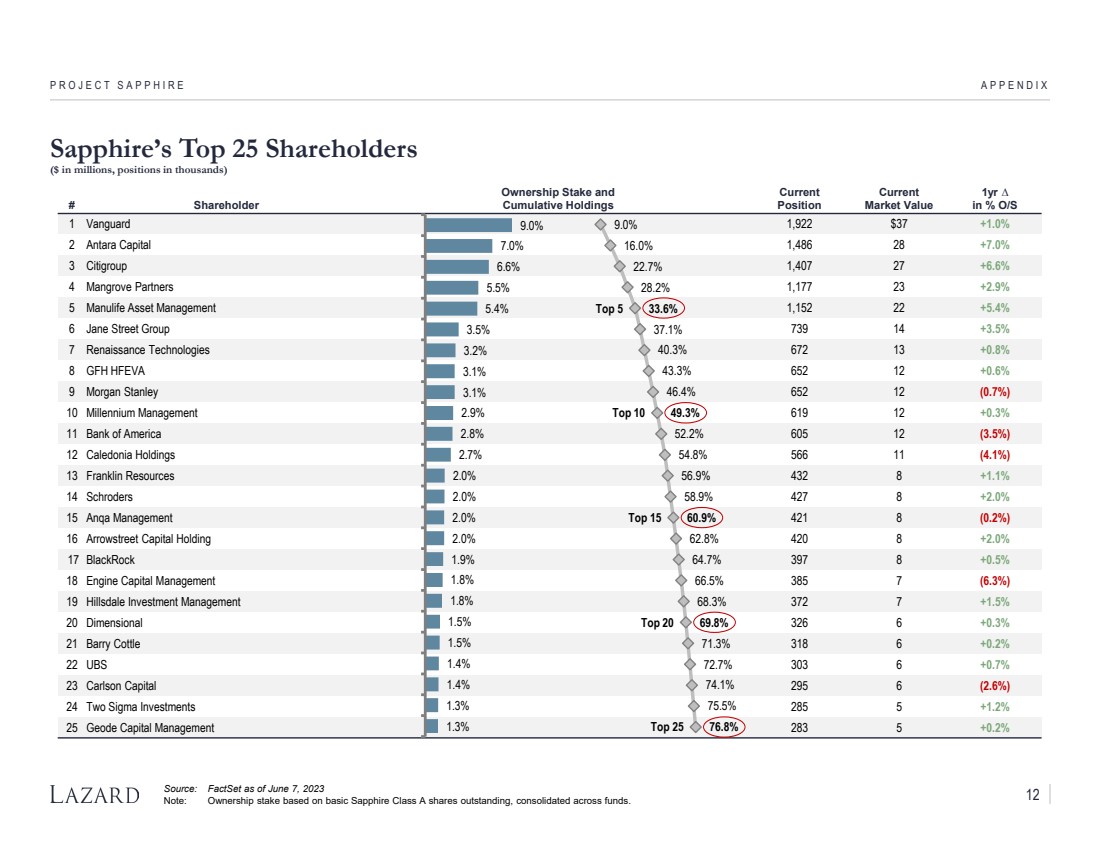

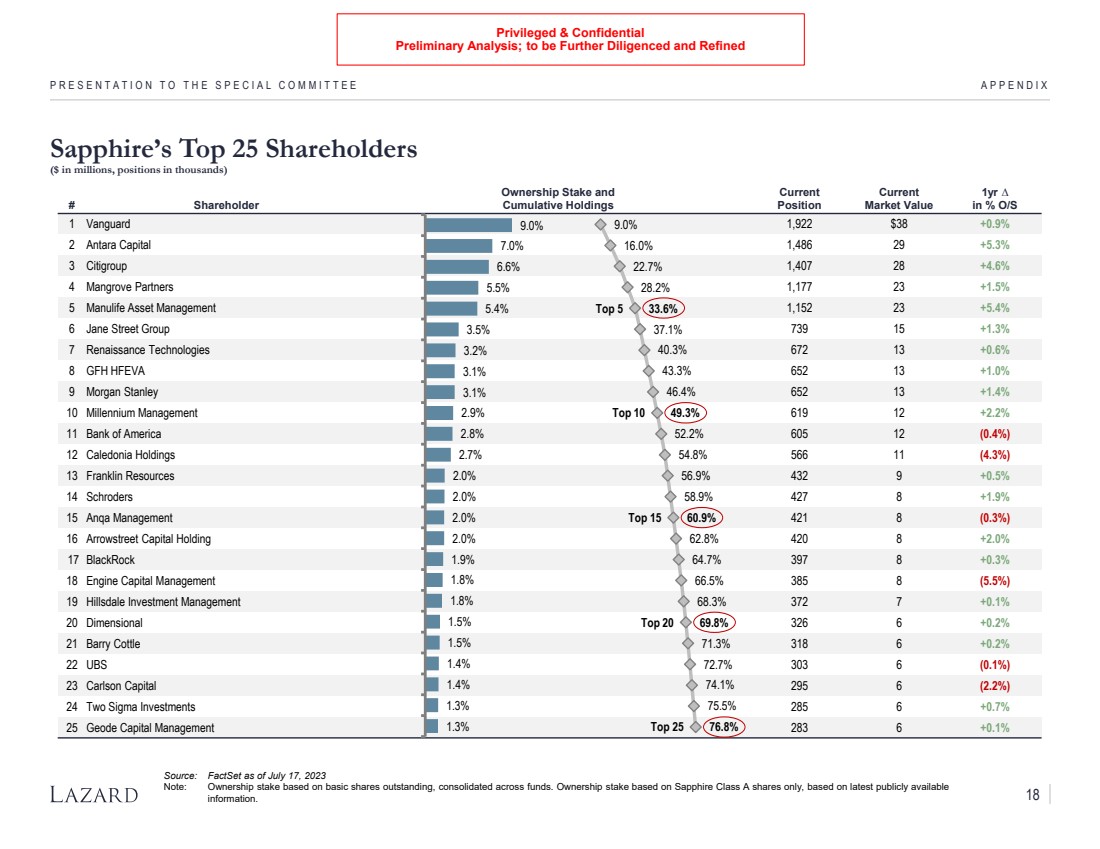

| APPENDIX

Sapphire’s Top 25 Shareholders

($ in millions, positions in thousands)

Source: FactSet as of June 7, 2023

Note: Ownership stake based on basic Sapphire Class A shares outstanding, consolidated across funds.

PROJECT SAPPHIRE

# Shareholder

Ownership Stake and

Cumulative Holdings

Current

Position

Current

Market Value

1yr ∆

in % O/S

1 Vanguard 1,922 $37 +1.0%

2 Antara Capital 1,486 28 +7.0%

3 Citigroup 1,407 27 +6.6%

4 Mangrove Partners 1,177 23 +2.9%

5 Manulife Asset Management 1,152 22 +5.4%

6 Jane Street Group 739 14 +3.5%

7 Renaissance Technologies 672 13 +0.8%

8 GFH HFEVA 652 12 +0.6%

9 Morgan Stanley 652 12 (0.7%)

10 Millennium Management 619 12 +0.3%

11 Bank of America 605 12 (3.5%)

12 Caledonia Holdings 566 11 (4.1%)

13 Franklin Resources 432 8 +1.1%

14 Schroders 427 8 +2.0%

15 Anqa Management 421 8 (0.2%)

16 Arrowstreet Capital Holding 420 8 +2.0%

17 BlackRock 397 8 +0.5%

18 Engine Capital Management 385 7 (6.3%)

19 Hillsdale Investment Management 372 7 +1.5%

20 Dimensional 326 6 +0.3%

21 Barry Cottle 318 6 +0.2%

22 UBS 303 6 +0.7%

23 Carlson Capital 295 6 (2.6%)

24 Two Sigma Investments 285 5 +1.2%

25 Geode Capital Management 283 5 +0.2%

9.0%

7.0%

6.6%

5.5%

5.4%

3.5%

3.2%

3.1%

3.1%

2.9%

2.8%

2.7%

2.0%

2.0%

2.0%

2.0%

1.9%

1.8%

1.8%

1.5%

1.5%

1.4%

1.4%

1.3%

1.3%

9.0%

16.0%

22.7%

28.2%

33.6%

37.1%

40.3%

43.3%

46.4%

49.3%

52.2%

54.8%

56.9%

58.9%

60.9%

62.8%

64.7%

66.5%

68.3%

69.8%

71.3%

72.7%

74.1%

75.5%

76.8%

Top 5

Top 10

Top 15

Top 20

Top 25

12 |

Exhibit (c)(4)

| P R E L I M I N A R Y B E N C H M A R K I N G A N A LY S I S

C O N F I D E N T I A L J U L Y 2 0 2 3

Project Sapphire |

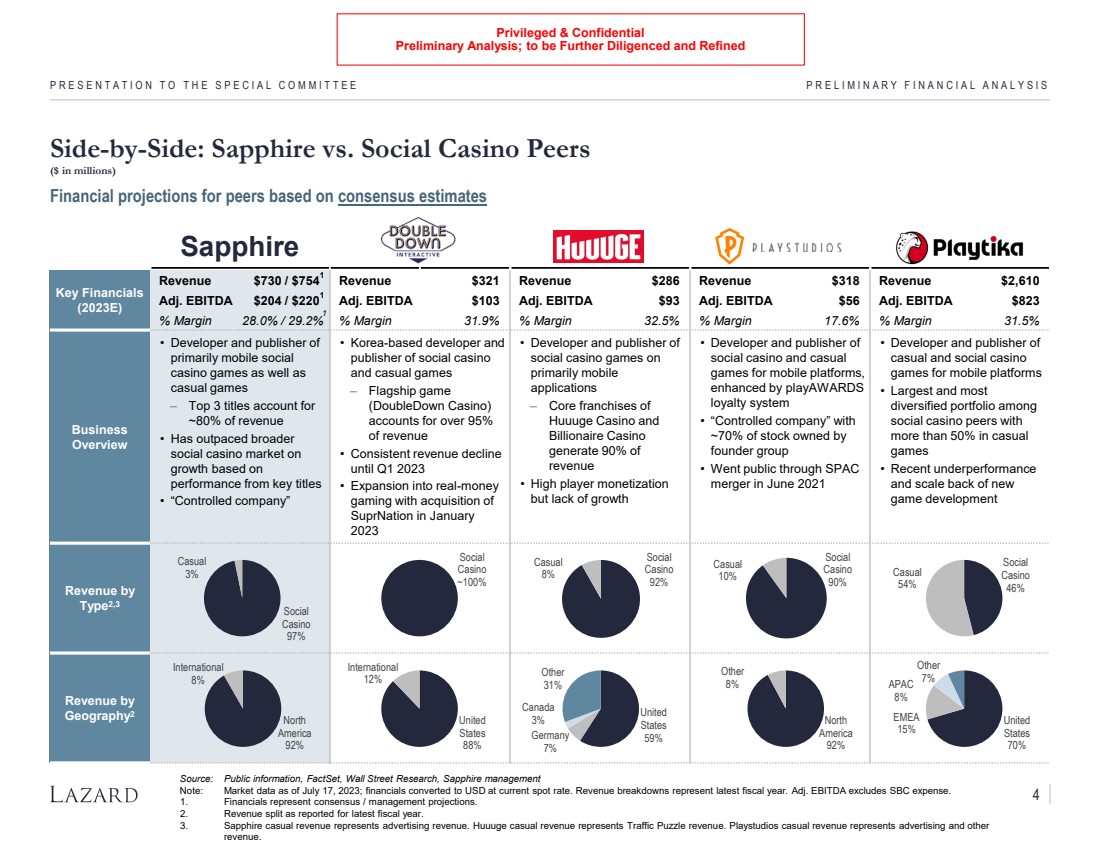

| Sapphire

Key Financials

(2023E)

Revenue $730 / $754 Revenue $321 Revenue $286 Revenue $318 Revenue $2,610

Adj. EBITDA $204 / $220 Adj. EBITDA $103 Adj. EBITDA $93 Adj. EBITDA $56 Adj. EBITDA $823

% Margin 28.0% / 29.2% % Margin 31.9% % Margin 32.5% % Margin 17.6% % Margin 31.5%

Business

Overview

• Developer and publisher of

primarily mobile social

casino games as well as

casual games

• Has outpaced broader

social casino market on

growth based on

performance from key titles

• “Controlled company”

• Korea-based developer and

publisher of social casino

and casual games

‒ Flagship game

(DoubleDown Casino)

accounts for over 95%

of revenue

• Consistent revenue decline

over last several quarters,

with first quarter of

sequential growth in Q1

2023

• Developer and publisher of

social casino games on

primarily mobile

applications

‒ Core franchises of

Huuuge Casino and

Billionaire Casino

generate 90% of

revenue

• High player monetization

but lack of growth

• Developer and publisher of

social casino and casual

games for mobile platforms

• Acquired Brainium in

October 2022 to expand

casual games portfolio

• “Controlled company” with

~70% of stock owned by

founder group

• Went public through SPAC

merger in June 2021

• Developer and publisher of

casual and social casino

games for mobile platforms

• Most diversified portfolio

among social casino peers

with more than 50% in

casual games

Revenue by

Type1

Revenue by

Geography

Side-by-Side: Sapphire vs. Social Casino Peers

($ in millions)

P R O J E C T S A P P H I R E C O N F I D E N T I A L

Source: Public information, FactSet, Wall Street Research, Sapphire management

Note: Market data as of July 10, 2023; financials converted to USD at current spot rate. Revenue breakdowns represent latest fiscal year.

1. Sapphire casual revenue represents advertising revenue. Huuuge casual revenue represents Traffic Puzzle revenue. Playstudios casual revenue represents advertising and other

revenue.

2. Financials represent consensus / management projections.

Financial projections for peers based on consensus estimates

North

America

92%

International

8%

Social

Casino

97%

Casual

3%

United

States

Germany 59%

7%

Canada

3%

Other

31%

Social

Casino

92%

Casual

8%

North

America

92%

Other

8%

Social

Casino

Casual 90%

10%

United

States

70%

EMEA

15%

APAC

8%

Other

7%

Social

Casino

46%

Casual

54%

United

States

88%

International

12%

Social

Casino

~100%

2

2

2

1 |

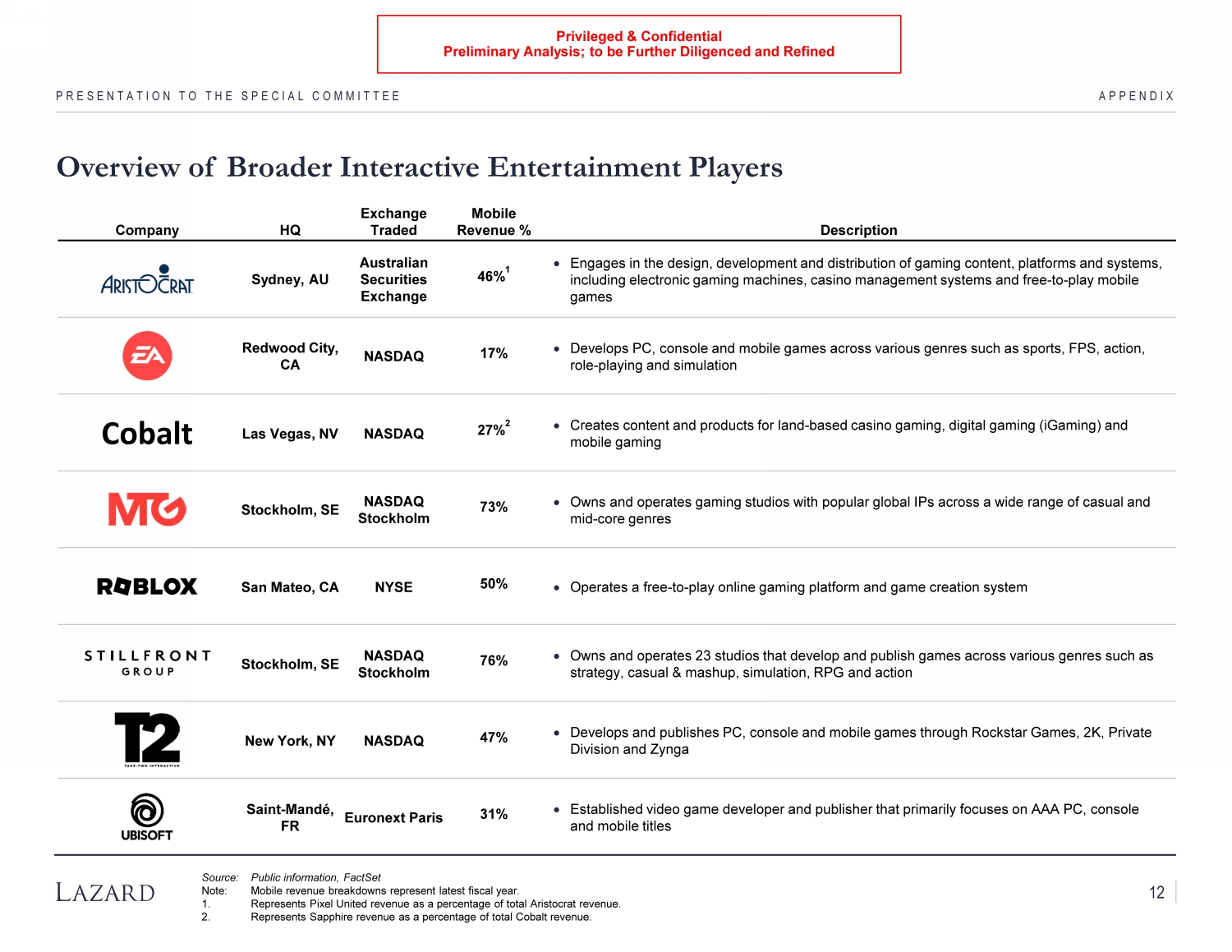

| Company HQ

Exchange

Traded

Mobile

Revenue % Description

Sydney, AU

Australian

Securities

Exchange

46%1

• Engages in the design, development and distribution of gaming content, platforms and systems,

including electronic gaming machines, casino management systems and free-to-play mobile

games

Redwood City,

CA NASDAQ 17% • Develops PC, console and mobile games across various genres such as sports, FPS, action,

role-playing and simulation

Cobalt Las Vegas, NV NASDAQ 27%2 • Creates content and products for land-based casino gaming, digital gaming (iGaming) and

mobile gaming

Stockholm, SE NASDAQ

Stockholm

73% • Owns and operates gaming studios with popular global IPs across a wide range of casual and

mid-core genres

San Mateo, CA NYSE 50% • Operates a free-to-play online gaming platform and game creation system

Stockholm, SE NASDAQ

Stockholm

76% • Owns and operates 23 studios that develop and publish games across various genres such as

strategy, casual & mashup, simulation, RPG and action

New York, NY NASDAQ 47% • Develops and publishes PC, console and mobile games through Rockstar Games, 2K, Private

Division and Zynga

Saint-Mandé,

FR Euronext Paris 31% • Established video game developer and publisher that primarily focuses on AAA PC, console

and mobile titles

P R O J E C T S A P P H I R E C O N F I D E N T I A L

Overview of Broader Interactive Entertainment Players

Source: Public information, FactSet

Note: Mobile revenue breakdowns represent latest fiscal year.

1. Represents Pixel United revenue as a % of total Aristocrat revenue.

2. Represents Sapphire revenue as a % of total Cobalt revenue.

2 |

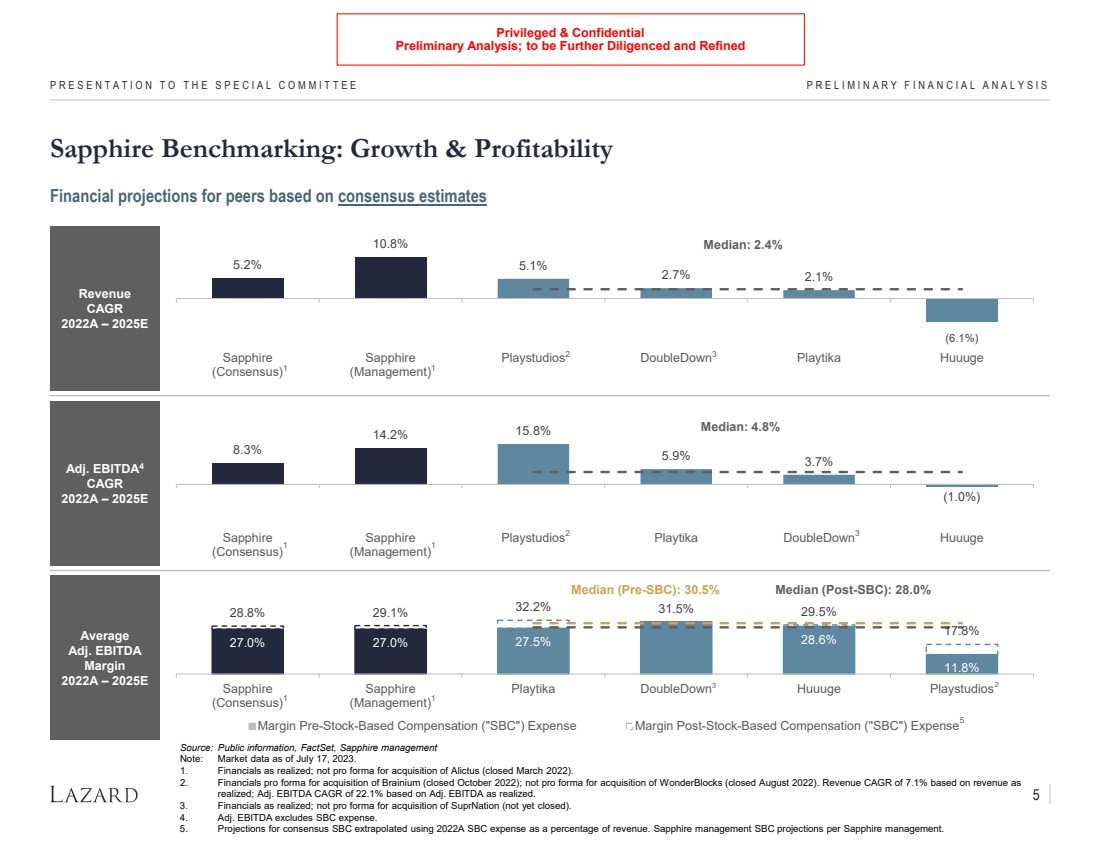

| Revenue

CAGR

2022A – 2024E

Adj. EBITDA

CAGR

2022A – 2024E

Average

Adj. EBITDA

Margin

2022A – 2024E4

(7.1%)

6.4%

11.5%

4.5% 3.3% 1.4%

Median: 2.3%

Sapphire

(Consensus)

Sapphire

(Management)

Playstudios DoubleDown Playtika Huuuge

Sapphire Benchmarking: Growth & Profitability

P R O J E C T S A P P H I R E C O N F I D E N T I A L

Source: Public information, FactSet, Sapphire management

Note: Market data as of July 10, 2023. Adj. EBITDA CAGRs are pre-SBC.

1. Financials pro forma for acquisition of Brainium (closed October 2022); not pro forma for acquisition of WonderBlocks (closed August 2022). Revenue CAGR of 7.4% based on revenue as

realized; EBITDA CAGR of 27.4% based on EBITDA as realized.

2. Financials as realized; not pro forma for acquisition of Alictus (closed March 2022).

3. Financials as realized; not pro forma for acquisition of SuprNation (expected to close in Q2 2023). DoubleDown does not have SBC expense.

4. Projections for consensus SBC expense extrapolated using 2022A SBC as a % of revenue. Sapphire management SBC projections as per company management.

Financial projections for peers based on consensus estimates

1

2

3

(0.7%)

8.5%

13.8%

20.4%

3.9%

0.4%

Median: 2.1%

Sapphire

(Consensus)

Sapphire

(Management)

Playstudios Playtika DoubleDown Huuuge 1 3

26.5% 26.5% 26.8% 28.3%

11.4%

28.3% 28.7% 31.5% 31.2% 29.3%

17.2%

Median (Pre-SBC): 30.2% Median (Post-SBC): 27.6%

Sapphire

(Consensus)

Sapphire

(Management)

Playtika DoubleDown Huuuge Playstudios

Margin Pre-SBC Expense

Margin Post-SBC Expense

3 1

2

2 2

2 2

3 |

| Social Casino Peers

FY2022A

Average Daily

Active Users

(in millions)

FY2022A

ARPDAU1

FY2022A

Payer

Conversion

Rate

9.6%

6.3%

5.3%

3.3%

1.5%

Median: 4.3%

Sapphire Huuuge DoubleDown Playtika Playstudios

$0.78

$1.43

$0.97

$0.76

$0.41

Median: $0.87

Sapphire Huuuge DoubleDown Playtika Playstudios

Sapphire Benchmarking vs. Peers: Selected KPIs

P R O J E C T S A P P H I R E C O N F I D E N T I A L

Source: Public information

1. Average Revenue Per Daily Active User.

2.3

9.4

1.9 1.0 0.6

Median: 1.5 million

Sapphire Playtika Playstudios DoubleDown Huuuge

KPIs measured as of latest fiscal year

4 |

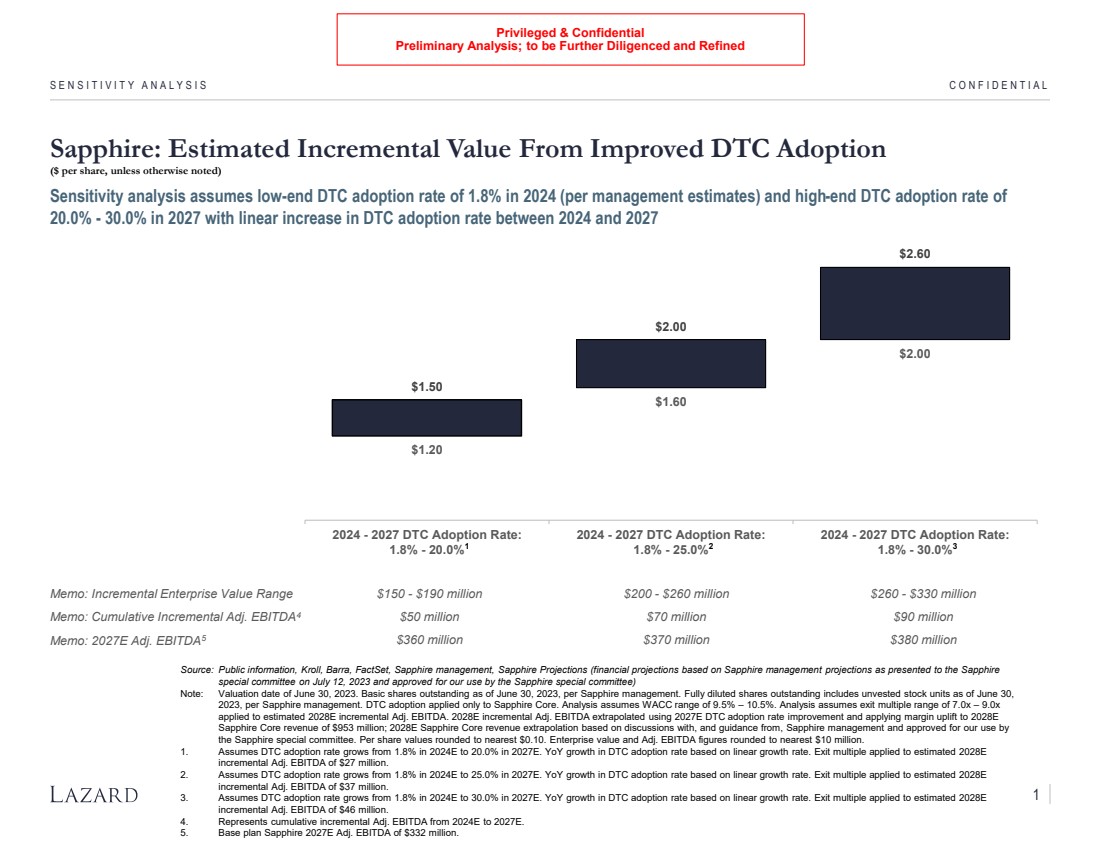

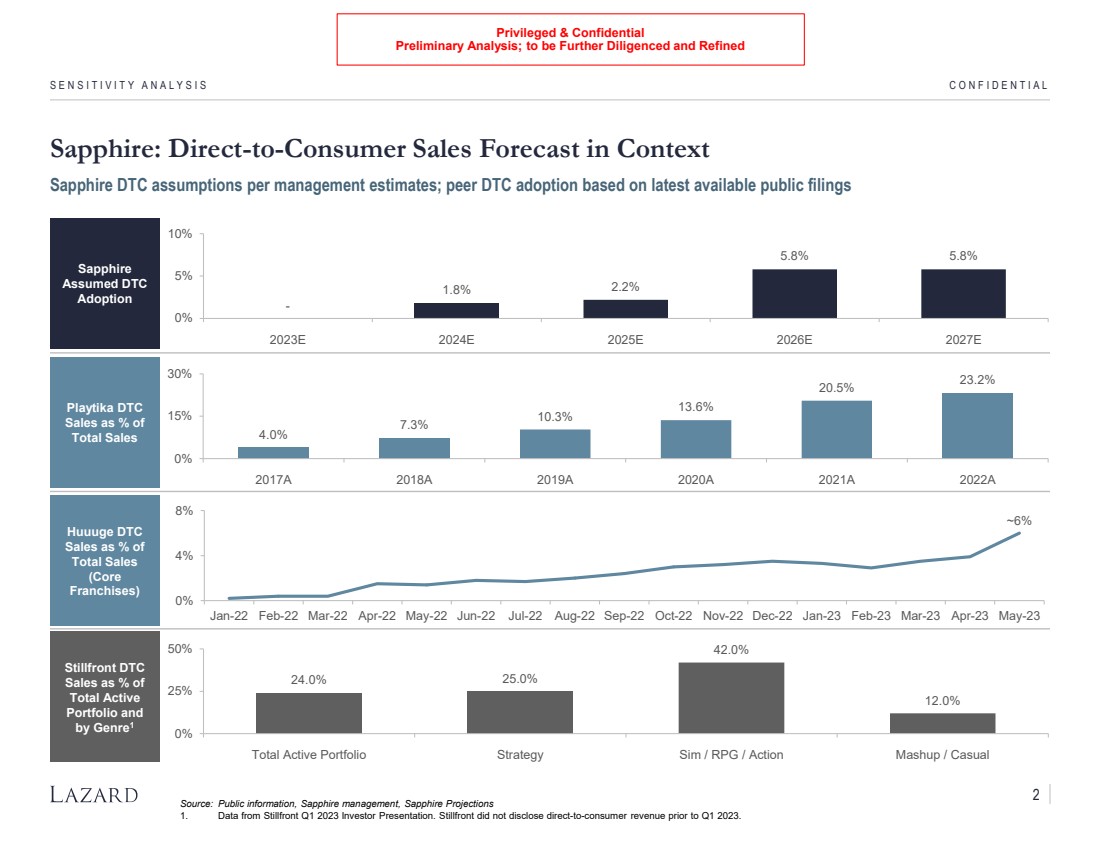

| P R O J E C T S A P P H I R E

Sapphire: Direct-to-Consumer Benchmarking

C O N F I D E N T I A L

Sapphire

Assumed DTC

Adoption

Playtika DTC

Sales as % of

Total Sales

Huuuge DTC

Sales as % of

Total Sales

(Core

Franchises)

Stillfront DTC

Sales as % of

Total Active

Portfolio and

by Genre2

-

1.5% 2.2%

5.8% 5.8%

0%

5%

10%

2023E 2024E 2025E 2026E 2027E

4.0%

7.3% 10.3%

13.6%

20.5% 23.2%

0%

15%

30%

2017A 2018A 2019A 2020A 2021A 2022A

0%

4%

8%

Jan-22 Feb-22 Mar-22 Apr-22 May-22 Jun-22 Jul-22 Aug-22 Sep-22 Oct-22 Nov-22 Dec-22 Jan-23 Feb-23 Mar-23 Apr-23 May-23

Sapphire DTC assumptions per management estimates; social casino peers and other interactive entertainment players DTC adoption based

on public information

Source: Public information, Sapphire management

1. Estimate per discussion with management.

2. Data from Stillfront Q1 2023 Investor Presentation. Stillfront did not disclose direct-to-consumer revenue prior to Q1 2023.

1

24.0% 25.0%

42.0%

12.0%

0%

25%

50%

Total Active Portfolio Strategy Sim / RPG / Action Mashup / Casual

5 |

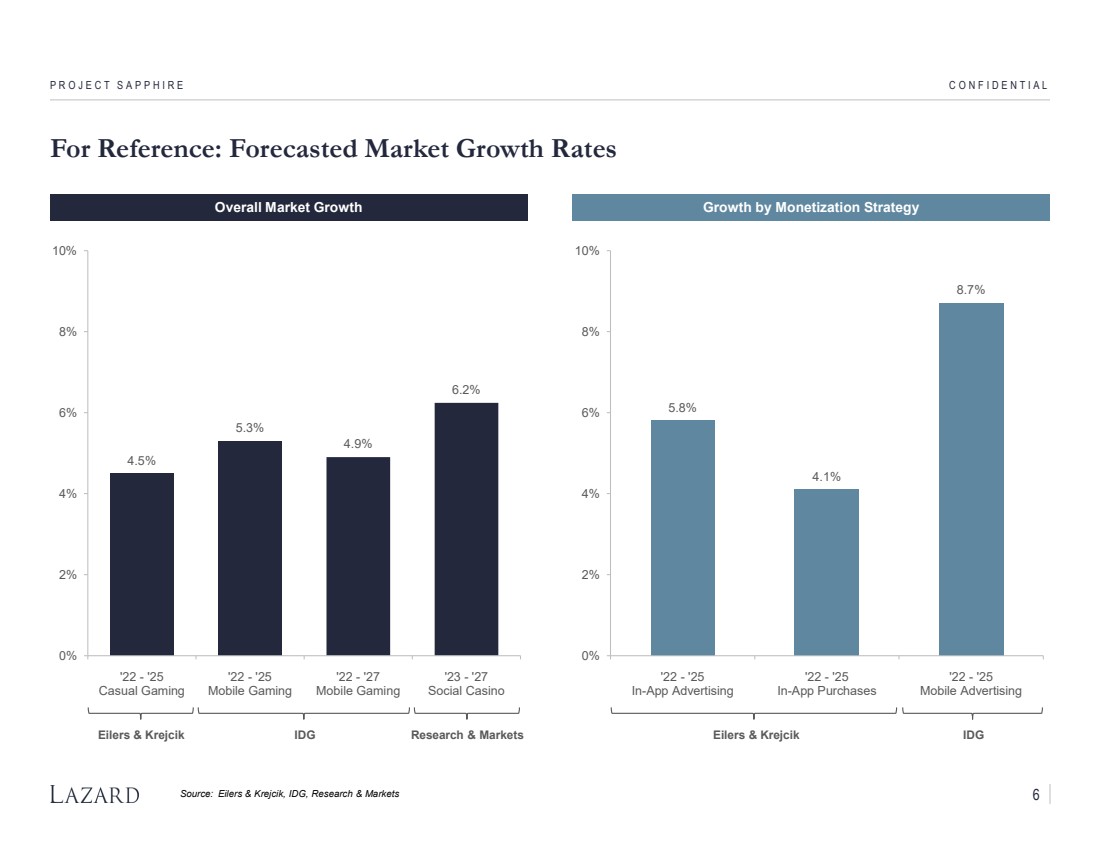

| P R O J E C T S A P P H I R E

For Reference: Forecasted Market Growth Rates

C O N F I D E N T I A L

4.5%

5.3%

4.9%

6.2%

0%

2%

4%

6%

8%

10%

'22 - '25

Casual Gaming

'22 - '25

Mobile Gaming

'22 - '27

Mobile Gaming

'23 - '27

Social Casino

Source: Eilers & Krejcik, IDG, Research & Markets

Overall Market Growth Growth by Monetization Strategy

Eilers & Krejcik IDG Research & Markets

5.8%

4.1%

8.7%

0%

2%

4%

6%

8%

10%

'22 - '25

In-App Advertising

'22 - '25

In-App Purchases

'22 - '25

Mobile Advertising

Eilers & Krejcik IDG

6 |

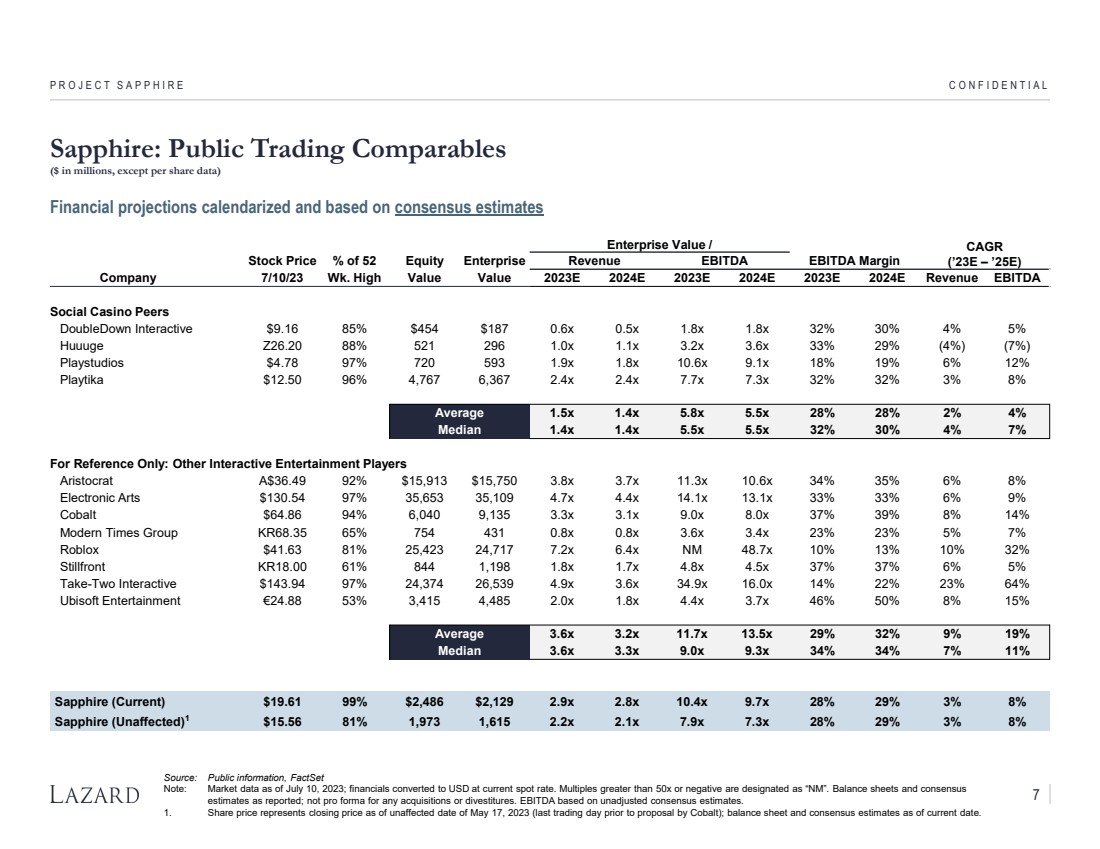

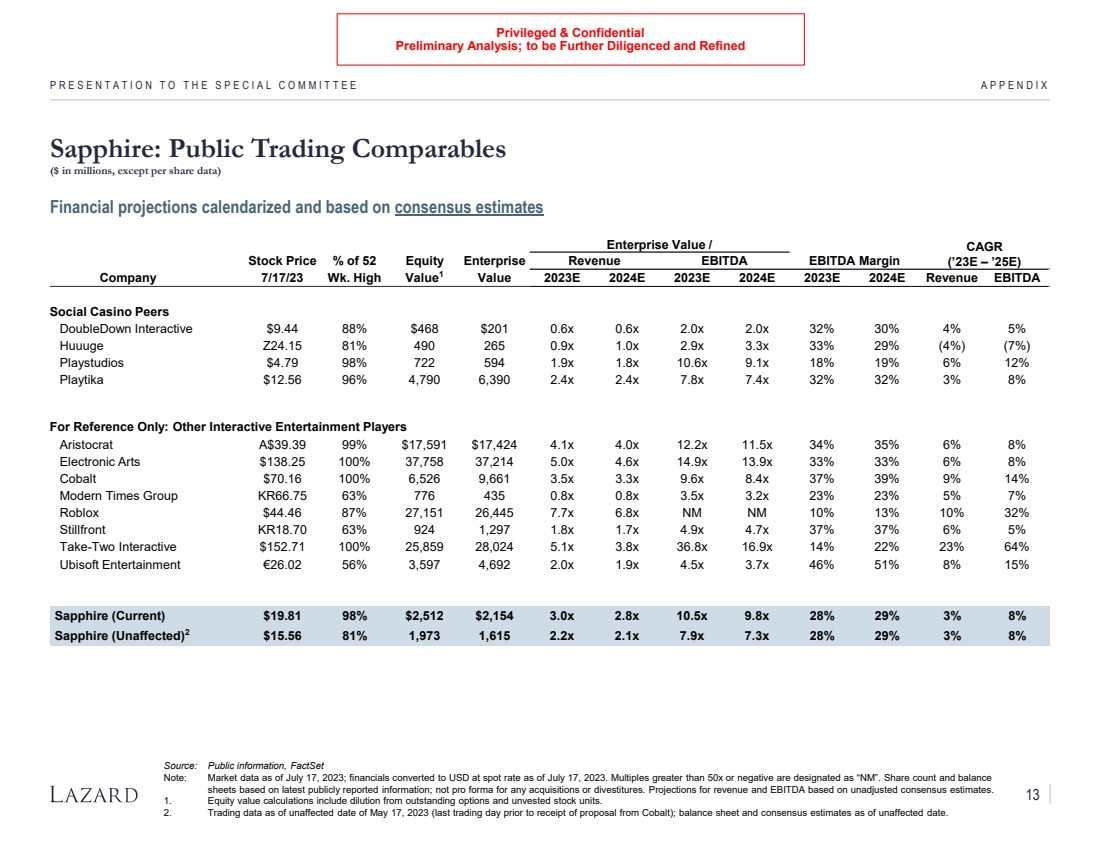

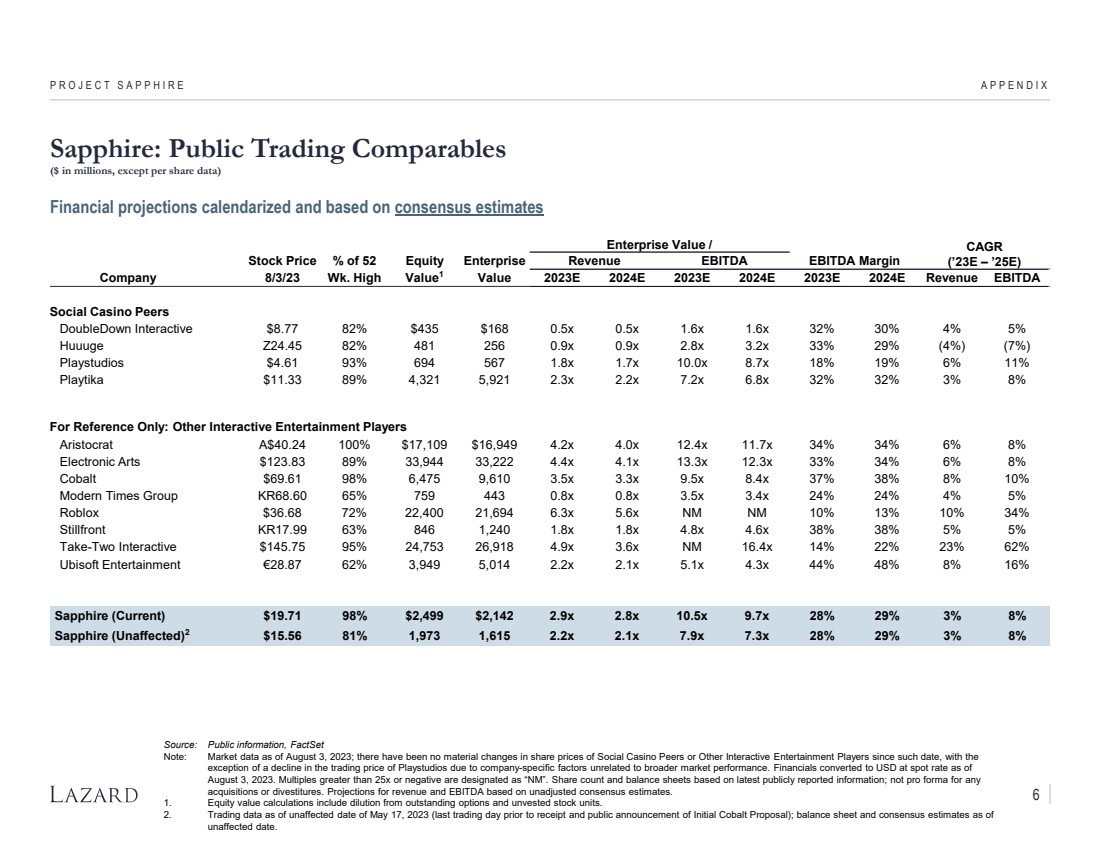

| Enterprise Value / CAGR

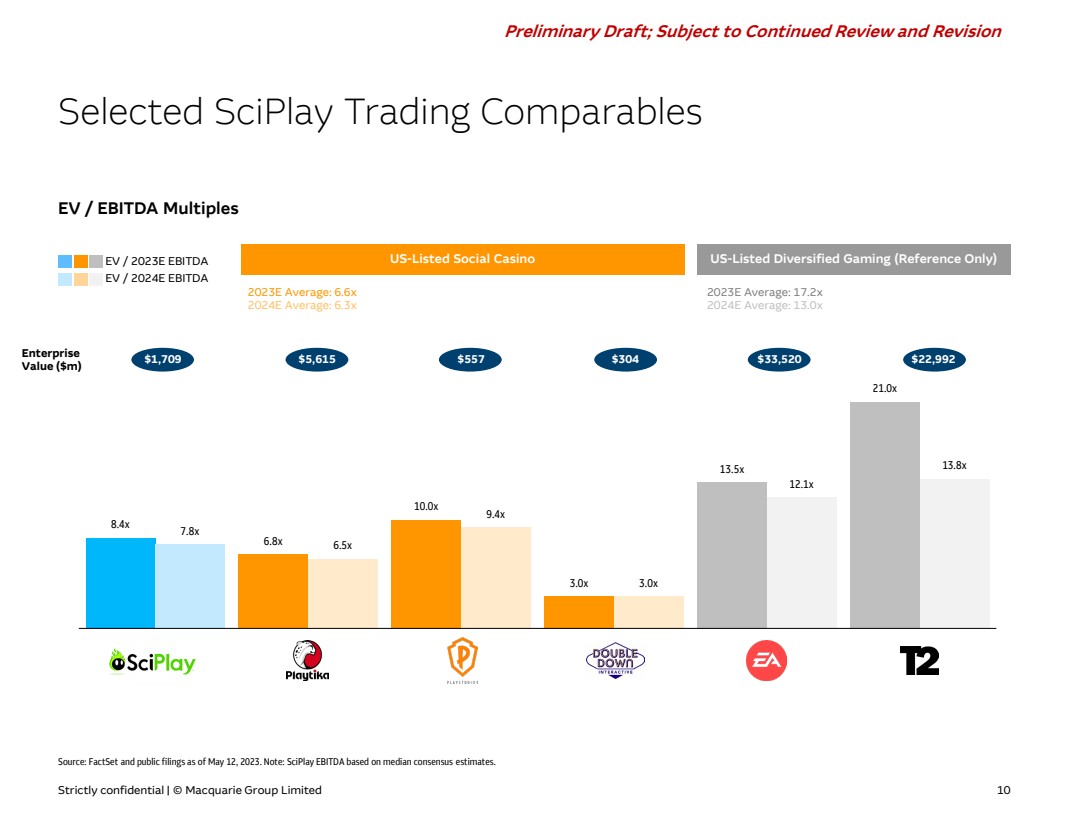

Stock Price % of 52 Equity Enterprise Revenue EBITDA EBITDA Margin (’23E – ’25E)

Company 7/10/23 Wk. High Value Value 2023E 2024E 2023E 2024E 2023E 2024E Revenue EBITDA

Social Casino Peers

DoubleDown Interactive $9.16 85% $454 $187 0.6x 0.5x 1.8x 1.8x 32% 30% 4% 5%

Huuuge Z26.20 88% 521 296 1.0x 1.1x 3.2x 3.6x 33% 29% (4%) (7%)

Playstudios $4.78 97% 720 593 1.9x 1.8x 10.6x 9.1x 18% 19% 6% 12%

Playtika $12.50 96% 4,767 6,367 2.4x 2.4x 7.7x 7.3x 32% 32% 3% 8%

Average 1.5x 1.4x 5.8x 5.5x 28% 28% 2% 4%

Median 1.4x 1.4x 5.5x 5.5x 32% 30% 4% 7%

For Reference Only: Other Interactive Entertainment Players

Aristocrat A$36.49 92% $15,913 $15,750 3.8x 3.7x 11.3x 10.6x 34% 35% 6% 8%

Electronic Arts $130.54 97% 35,653 35,109 4.7x 4.4x 14.1x 13.1x 33% 33% 6% 9%

Cobalt $64.86 94% 6,040 9,135 3.3x 3.1x 9.0x 8.0x 37% 39% 8% 14%

Modern Times Group KR68.35 65% 754 431 0.8x 0.8x 3.6x 3.4x 23% 23% 5% 7%

Roblox $41.63 81% 25,423 24,717 7.2x 6.4x NM 48.7x 10% 13% 10% 32%

Stillfront KR18.00 61% 844 1,198 1.8x 1.7x 4.8x 4.5x 37% 37% 6% 5%

Take-Two Interactive $143.94 97% 24,374 26,539 4.9x 3.6x 34.9x 16.0x 14% 22% 23% 64%

Ubisoft Entertainment €24.88 53% 3,415 4,485 2.0x 1.8x 4.4x 3.7x 46% 50% 8% 15%

Average 3.6x 3.2x 11.7x 13.5x 29% 32% 9% 19%

Median 3.6x 3.3x 9.0x 9.3x 34% 34% 7% 11%

Sapphire (Current) $19.61 99% $2,486 $2,129 2.9x 2.8x 10.4x 9.7x 28% 29% 3% 8%

Sapphire (Unaffected)1

$15.56 81% 1,973 1,615 2.2x 2.1x 7.9x 7.3x 28% 29% 3% 8%

Sapphire: Public Trading Comparables

($ in millions, except per share data)

P R O J E C T S A P P H I R E C O N F I D E N T I A L

Source: Public information, FactSet

Note: Market data as of July 10, 2023; financials converted to USD at current spot rate. Multiples greater than 50x or negative are designated as “NM”. Balance sheets and consensus

estimates as reported; not pro forma for any acquisitions or divestitures. EBITDA based on unadjusted consensus estimates.

1. Share price represents closing price as of unaffected date of May 17, 2023 (last trading day prior to proposal by Cobalt); balance sheet and consensus estimates as of current date.

Financial projections calendarized and based on consensus estimates

7 |

Exhibit (c)(5)

| Privileged & Confidential

Preliminary Analysis; to be Further Diligenced and Refined

Presentation to the Special Committee

PROJECT SAPPHIRE

CONFIDENTIAL 19 JULY 2023 |

| Privileged & Confidential

Preliminary Analysis; to be Further Diligenced and Refined

The information herein has been prepared by Lazard Frères & Co. LLC (“Lazard”) based upon information supplied by you (the “Company”) or

publicly available information, and portions of the information herein may be based upon certain statements, estimates and forecasts provided by

the Company with respect to the anticipated future performance of the Company. Lazard has relied upon the accuracy and completeness of the

foregoing information, and has not assumed any responsibility for any independent verification of such information or any independent valuation or

appraisal of any of the assets or liabilities of the Company, or any other entity, or concerning solvency or fair value of the Company or any other

entity. With respect to financial forecasts, Lazard has assumed that they have been reasonably prepared on bases reflecting the best currently

available estimates and judgments as to the future financial performance of the Company. Lazard assumes no responsibility for and expresses no

view as to such forecasts or the assumptions on which they are based. The information set forth herein is based upon economic, monetary, market

and other conditions as in effect on, and the information made available to us as of, the date hereof, unless indicated otherwise. Lazard is not

making any assessment regarding the impact or economic effects of the COVID-19 virus, including with respect to the potential impact or effects on

the future financial performance of the Company. Subsequent developments, including, without limitation, in relation to COVID-19, may affect the

forecasts and other information set out in this document and Lazard assumes no responsibility for updating or revising this document based on

circumstances or events after the date hereof. These materials and the information contained herein are confidential and may not be disclosed

publicly or made available to third parties without the prior written consent of Lazard; provided, however, that you may disclose to any and all

persons the U.S. federal income tax treatment and tax structure of the transaction described herein and the portions of these materials that relate to

such tax treatment or structure. Lazard is acting as financial advisor to the special committee of the board of directors of the Company, and will not

be responsible for and will not provide any tax, accounting, actuarial, legal or other specialist advice.

Disclaimer

CONFIDENTIAL PRESENTATION TO THE SPECIAL COMMITTEE |

| Privileged & Confidential

Preliminary Analysis; to be Further Diligenced and Refined

CONFIDENTIAL

Situation Update

PRESENTATION TO THE SPECIAL COMMITTEE |

| Privileged & Confidential

Preliminary Analysis; to be Further Diligenced and Refined

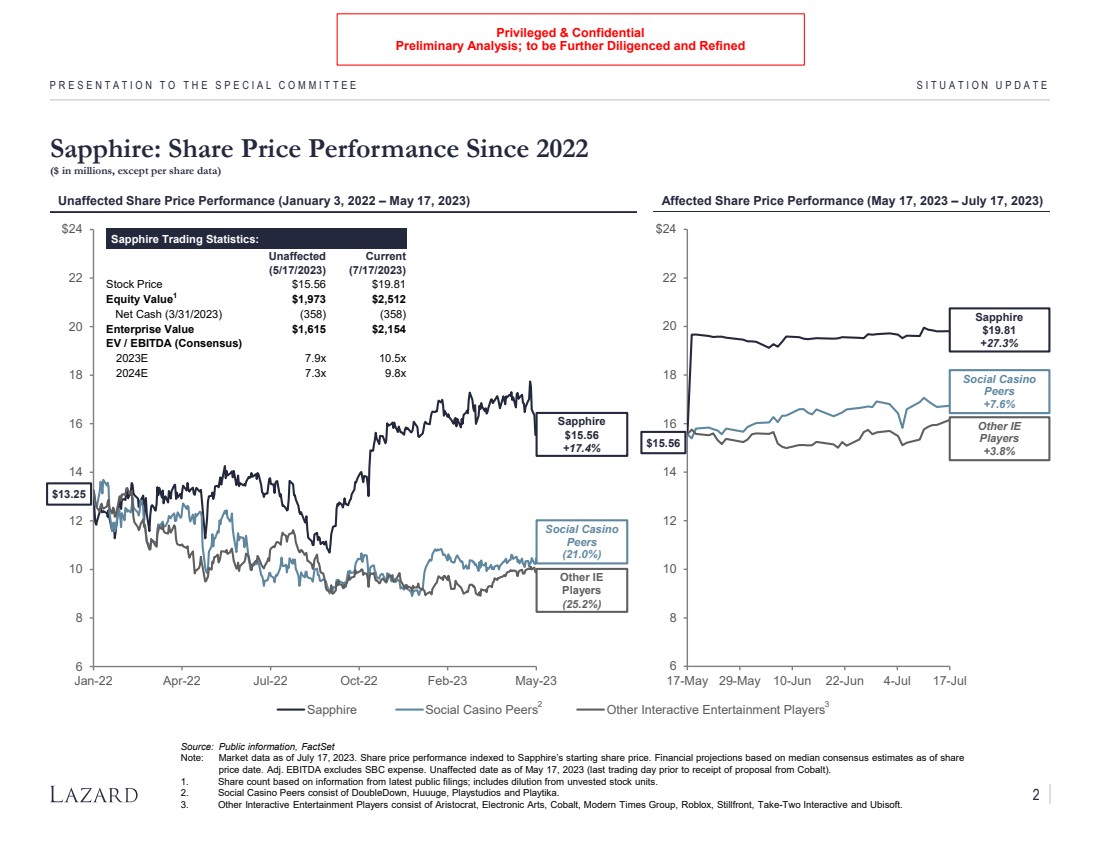

Overview of Cobalt’s Offer to Acquire Public Shares of Sapphire

($ in millions, except per share data)

PRESENTATION TO THE SPECIAL COMMITTEE SITUATION UPDATE

Source: Public information, FactSet, Bloomberg

Note: Unaffected date as of May 17, 2023 (last trading day prior to receipt of proposal from Cobalt); current date as of July 17, 2023. Adj. EBITDA excludes stock-based compensation (“SBC”)

expense.

1. Share count based on information from latest public filings; includes dilution from unvested stock units.

2. Projections represent consensus Adj. EBITDA estimates as of July 17, 2023.

Unaffected Price

(5/17/2023)

Current Price

(7/17/2023)

Current

Offer Value

Implied Premium / (Discount) to: Reference Price:

Unaffected Closing Price $15.56 - 27.3% 28.5%

Unaffected 10-Trading Day VWAP 16.97 (8.3%) 16.8% 17.9%

Unaffected 30-Trading Day VWAP 17.10 (9.0%) 15.9% 17.0%

Unaffected 60-Trading Day VWAP 16.96 (8.3%) 16.8% 17.9%

Implied Equity Value1 $1,973 $2,512 $2,536

Net Cash (3/31/2023) (358) (358) (358)

Implied Enterprise Value $1,615 $2,154 $2,178

Implied EV / Adj. EBITDA (Consensus) Adj. EBITDA:2

2023E $204 7.9x 10.5x 10.7x

2024E 220 7.3x 9.8x 9.9x

Implied EV / Adj. EBITDA (Management) Adj. EBITDA:

2023E $220 7.3x 9.8x 9.9x

2024E 242 6.7x 8.9x 9.0x

$15.56

$19.81 $20.00

On May 18, 2023, Cobalt submitted to the Sapphire Board of Directors and concurrently publicly announced a new proposal for Cobalt to

acquire the 17% equity interest in Sapphire that it does not currently own for $20.00 per share in cash

• Proposal conditioned upon approval of special committee of independent directors; not conditioned upon approval of independent

shareholders

1 |

| Privileged & Confidential

Preliminary Analysis; to be Further Diligenced and Refined

6

8

10

12

14

16

18

20

22

$24

Jan-22 Apr-22 Jul-22 Oct-22 Feb-23 May-23

Sapphire Social Casino Peers Other Interactive Entertainment Players

6

8

10

12

14

16

18

20

22

$24

17-May 29-May 10-Jun 22-Jun 4-Jul 17-Jul

PRESENTATION TO THE SPECIAL COMMITTEE SITUATION UPDATE

Sapphire Trading Statistics:

Unaffected

(5/17/2023)

Current

(7/17/2023)

Stock Price $15.56 $19.81

Equity Value1 $1,973 $2,512

Net Cash (3/31/2023) (358) (358)

Enterprise Value $1,615 $2,154

EV / EBITDA (Consensus)

2023E 7.9x 10.5x

2024E 7.3x 9.8x

Unaffected Share Price Performance (January 3, 2022 – May 17, 2023)

2

Sapphire

$15.56

+17.4%

Social Casino

Peers

(21.0%)

Source: Public information, FactSet