0001674440

false

Q1

--04-30

MD

P0Y

0001674440

2023-05-01

2023-07-31

0001674440

2023-10-02

0001674440

2023-07-31

0001674440

2023-04-30

0001674440

us-gaap:NonrelatedPartyMember

2023-07-31

0001674440

us-gaap:NonrelatedPartyMember

2023-04-30

0001674440

us-gaap:RelatedPartyMember

2023-07-31

0001674440

us-gaap:RelatedPartyMember

2023-04-30

0001674440

2022-05-01

2022-07-31

0001674440

us-gaap:NonrelatedPartyMember

2023-05-01

2023-07-31

0001674440

us-gaap:NonrelatedPartyMember

2022-05-01

2022-07-31

0001674440

us-gaap:RelatedPartyMember

2023-05-01

2023-07-31

0001674440

us-gaap:RelatedPartyMember

2022-05-01

2022-07-31

0001674440

us-gaap:CommonStockMember

2022-04-30

0001674440

us-gaap:AdditionalPaidInCapitalMember

2022-04-30

0001674440

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2022-04-30

0001674440

us-gaap:RetainedEarningsMember

2022-04-30

0001674440

2022-04-30

0001674440

us-gaap:CommonStockMember

2023-04-30

0001674440

us-gaap:AdditionalPaidInCapitalMember

2023-04-30

0001674440

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2023-04-30

0001674440

us-gaap:RetainedEarningsMember

2023-04-30

0001674440

us-gaap:CommonStockMember

2022-05-01

2022-07-31

0001674440

us-gaap:AdditionalPaidInCapitalMember

2022-05-01

2022-07-31

0001674440

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2022-05-01

2022-07-31

0001674440

us-gaap:RetainedEarningsMember

2022-05-01

2022-07-31

0001674440

us-gaap:CommonStockMember

2023-05-01

2023-07-31

0001674440

us-gaap:AdditionalPaidInCapitalMember

2023-05-01

2023-07-31

0001674440

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2023-05-01

2023-07-31

0001674440

us-gaap:RetainedEarningsMember

2023-05-01

2023-07-31

0001674440

us-gaap:CommonStockMember

2022-07-31

0001674440

us-gaap:AdditionalPaidInCapitalMember

2022-07-31

0001674440

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2022-07-31

0001674440

us-gaap:RetainedEarningsMember

2022-07-31

0001674440

2022-07-31

0001674440

us-gaap:CommonStockMember

2023-07-31

0001674440

us-gaap:AdditionalPaidInCapitalMember

2023-07-31

0001674440

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2023-07-31

0001674440

us-gaap:RetainedEarningsMember

2023-07-31

0001674440

CNXA:SlingerBagAmericasIncMember

2019-08-23

0001674440

CNXA:SlingerBagAmericasIncMember

CNXA:StockPurchaseAgreementMember

2019-08-23

2019-08-23

0001674440

CNXA:StockPurchaseAgreementMember

CNXA:SlingerBagAmericasIncMember

2019-08-23

0001674440

CNXA:SlingerBagAmericasIncMember

2019-09-16

2019-09-16

0001674440

CNXA:SlingerBagAmericasIncMember

2019-09-16

0001674440

CNXA:SoleShareholderofSBLMember

CNXA:StockPurchaseAgreementMember

2019-09-16

2019-09-16

0001674440

CNXA:SoleShareholderofSBLMember

2019-09-16

0001674440

CNXA:SlingerBagAmericasIncMember

2020-02-10

0001674440

CNXA:FoundationSportsSystemsLLCMember

CNXA:CharlesRuddyMember

2021-06-21

0001674440

CNXA:FoundationSportsSystemsLLCMember

2022-12-05

0001674440

2022-06-14

2022-06-14

0001674440

us-gaap:SubsequentEventMember

2023-09-22

2023-09-22

0001674440

srt:MinimumMember

us-gaap:SubsequentEventMember

2023-10-09

0001674440

srt:MinimumMember

2023-07-26

0001674440

CNXA:PlaySightMember

CNXA:FoundationSportsSystemsLLCMember

2022-11-30

0001674440

CNXA:PlaySightMember

CNXA:FoundationSportsSystemsLLCMember

2022-12-31

0001674440

CNXA:FoundationSportsSystemsLLCMember

2023-05-01

2023-07-31

0001674440

CNXA:FoundationSportsSystemsLLCMember

2023-07-31

0001674440

us-gaap:FairValueInputsLevel3Member

2023-05-01

2023-07-31

0001674440

us-gaap:FairValueInputsLevel3Member

2022-05-01

2023-04-30

0001674440

us-gaap:WarrantMember

2023-05-01

2023-07-31

0001674440

CNXA:ProfitGuarantyMember

2023-07-31

0001674440

CNXA:ProfitGuarantyMember

2023-05-01

2023-07-31

0001674440

CNXA:ConvertibleNotesMember

2023-07-31

0001674440

CNXA:ConvertibleNotesMember

2023-05-01

2023-07-31

0001674440

CNXA:UnderwriterWarrantsMember

2023-07-31

0001674440

CNXA:UnderwriterWarrantsMember

2023-05-01

2023-07-31

0001674440

CNXA:WarrantsIssuedWithCommonStockMember

2023-07-31

0001674440

CNXA:WarrantsIssuedWithCommonStockMember

2023-05-01

2023-07-31

0001674440

CNXA:WarrantsIssuedWithNotesPayableMember

2023-07-31

0001674440

CNXA:WarrantsIssuedWithNotesPayableMember

2023-05-01

2023-07-31

0001674440

srt:MinimumMember

us-gaap:MeasurementInputExpectedTermMember

us-gaap:ValuationTechniqueOptionPricingModelMember

2023-05-01

2023-07-31

0001674440

srt:MaximumMember

us-gaap:MeasurementInputExpectedTermMember

us-gaap:ValuationTechniqueOptionPricingModelMember

2023-05-01

2023-07-31

0001674440

srt:MinimumMember

us-gaap:MeasurementInputExpectedTermMember

us-gaap:ValuationTechniqueOptionPricingModelMember

2022-05-01

2022-07-31

0001674440

srt:MaximumMember

us-gaap:MeasurementInputExpectedTermMember

us-gaap:ValuationTechniqueOptionPricingModelMember

2022-05-01

2022-07-31

0001674440

us-gaap:MeasurementInputPriceVolatilityMember

us-gaap:ValuationTechniqueOptionPricingModelMember

2023-07-31

0001674440

us-gaap:MeasurementInputPriceVolatilityMember

us-gaap:ValuationTechniqueOptionPricingModelMember

srt:MinimumMember

2022-07-31

0001674440

us-gaap:MeasurementInputPriceVolatilityMember

us-gaap:ValuationTechniqueOptionPricingModelMember

srt:MaximumMember

2022-07-31

0001674440

srt:MinimumMember

us-gaap:MeasurementInputRiskFreeInterestRateMember

us-gaap:ValuationTechniqueOptionPricingModelMember

2023-07-31

0001674440

srt:MaximumMember

us-gaap:MeasurementInputRiskFreeInterestRateMember

us-gaap:ValuationTechniqueOptionPricingModelMember

2023-07-31

0001674440

srt:MinimumMember

us-gaap:MeasurementInputRiskFreeInterestRateMember

us-gaap:ValuationTechniqueOptionPricingModelMember

2022-07-31

0001674440

srt:MaximumMember

us-gaap:MeasurementInputRiskFreeInterestRateMember

us-gaap:ValuationTechniqueOptionPricingModelMember

2022-07-31

0001674440

us-gaap:MeasurementInputExpectedDividendRateMember

us-gaap:ValuationTechniqueOptionPricingModelMember

2023-07-31

0001674440

us-gaap:MeasurementInputExpectedDividendRateMember

us-gaap:ValuationTechniqueOptionPricingModelMember

2022-07-31

0001674440

us-gaap:WarrantMember

us-gaap:ValuationTechniqueOptionPricingModelMember

us-gaap:MeasurementInputExpectedTermMember

2023-07-31

0001674440

us-gaap:WarrantMember

us-gaap:ValuationTechniqueOptionPricingModelMember

us-gaap:MeasurementInputExpectedTermMember

srt:MinimumMember

2022-07-31

0001674440

us-gaap:WarrantMember

us-gaap:ValuationTechniqueOptionPricingModelMember

us-gaap:MeasurementInputExpectedTermMember

srt:MaximumMember

2022-07-31

0001674440

us-gaap:MeasurementInputPriceVolatilityMember

us-gaap:ValuationTechniqueOptionPricingModelMember

us-gaap:WarrantMember

2023-07-31

0001674440

srt:MinimumMember

us-gaap:MeasurementInputPriceVolatilityMember

us-gaap:ValuationTechniqueOptionPricingModelMember

us-gaap:WarrantMember

2022-07-31

0001674440

srt:MaximumMember

us-gaap:MeasurementInputPriceVolatilityMember

us-gaap:ValuationTechniqueOptionPricingModelMember

us-gaap:WarrantMember

2022-07-31

0001674440

us-gaap:WarrantMember

us-gaap:ValuationTechniqueOptionPricingModelMember

us-gaap:MeasurementInputRiskFreeInterestRateMember

2023-07-31

0001674440

us-gaap:WarrantMember

us-gaap:ValuationTechniqueOptionPricingModelMember

us-gaap:MeasurementInputRiskFreeInterestRateMember

srt:MinimumMember

2022-07-31

0001674440

us-gaap:WarrantMember

us-gaap:ValuationTechniqueOptionPricingModelMember

us-gaap:MeasurementInputRiskFreeInterestRateMember

srt:MaximumMember

2022-07-31

0001674440

us-gaap:WarrantMember

us-gaap:ValuationTechniqueOptionPricingModelMember

us-gaap:MeasurementInputExpectedDividendRateMember

2023-07-31

0001674440

us-gaap:WarrantMember

us-gaap:ValuationTechniqueOptionPricingModelMember

us-gaap:MeasurementInputExpectedDividendRateMember

2022-07-31

0001674440

us-gaap:AccountsReceivableMember

us-gaap:CreditConcentrationRiskMember

CNXA:CustomerTwoMember

2023-05-01

2023-07-31

0001674440

us-gaap:AccountsReceivableMember

us-gaap:CreditConcentrationRiskMember

CNXA:CustomerTwoMember

2022-05-01

2023-04-30

0001674440

us-gaap:LenderConcentrationRiskMember

CNXA:CustomerFourMember

us-gaap:AccountsPayableMember

2023-05-01

2023-07-31

0001674440

us-gaap:LenderConcentrationRiskMember

CNXA:CustomerFourMember

us-gaap:AccountsPayableMember

2022-05-01

2023-04-30

0001674440

CNXA:TradeNamesAndPatentsMember

2023-07-31

0001674440

CNXA:TradeNamesAndPatentsMember

2023-05-01

2023-07-31

0001674440

us-gaap:CustomerRelationshipsMember

2023-07-31

0001674440

us-gaap:CustomerRelationshipsMember

2023-05-01

2023-07-31

0001674440

us-gaap:ComputerSoftwareIntangibleAssetMember

2023-07-31

0001674440

us-gaap:ComputerSoftwareIntangibleAssetMember

2023-05-01

2023-07-31

0001674440

CNXA:IntangiableAssetMember

2023-07-31

0001674440

CNXA:IntangiableAssetMember

2023-05-01

2023-07-31

0001674440

CNXA:TradeNamesAndPatentsMember

2023-04-30

0001674440

CNXA:TradeNamesAndPatentsMember

2022-05-01

2023-04-30

0001674440

us-gaap:CustomerRelationshipsMember

2023-04-30

0001674440

us-gaap:CustomerRelationshipsMember

2022-05-01

2023-04-30

0001674440

us-gaap:ComputerSoftwareIntangibleAssetMember

2023-04-30

0001674440

us-gaap:ComputerSoftwareIntangibleAssetMember

2022-05-01

2023-04-30

0001674440

CNXA:IntangiableAssetMember

2023-04-30

0001674440

CNXA:IntangiableAssetMember

2022-05-01

2023-04-30

0001674440

CNXA:FoundationSportsSystemsLLCMember

2023-05-01

2023-07-31

0001674440

us-gaap:PatentsMember

2023-07-31

0001674440

CNXA:LoanAgreementsMember

us-gaap:RelatedPartyMember

2022-01-14

0001674440

CNXA:LoanAgreementsMember

us-gaap:RelatedPartyMember

2022-01-13

2022-01-14

0001674440

us-gaap:RelatedPartyMember

2023-01-06

2023-01-06

0001674440

2023-01-06

0001674440

2022-06-17

2022-06-17

0001674440

2022-06-17

0001674440

CNXA:PromissoryNotePayableMember

2021-04-10

2021-04-11

0001674440

CNXA:PromissoryNotePayableMember

2021-04-11

0001674440

2021-04-10

2021-04-11

0001674440

us-gaap:ValuationTechniqueOptionPricingModelMember

2021-04-11

0001674440

CNXA:PromissoryNotePayableMember

2023-04-30

0001674440

CNXA:PromissoryNotePayableMember

2022-04-30

0001674440

2022-02-14

2022-02-15

0001674440

2022-05-01

2023-04-30

0001674440

2021-05-01

2022-07-31

0001674440

CNXA:NotesPayableMember

2022-04-01

0001674440

2022-04-01

2022-04-01

0001674440

2022-08-01

2022-08-01

0001674440

CNXA:UFSAgreementMember

2022-07-29

2022-07-29

0001674440

CNXA:UFSAgreementMember

CNXA:EachWeekForNextThreeWeeksMember

2022-07-29

2022-07-29

0001674440

CNXA:UFSAgreementMember

CNXA:ThereafterPerWeekMember

2022-07-29

2022-07-29

0001674440

CNXA:CedarAgreementMember

2022-07-29

2022-07-29

0001674440

CNXA:CedarAgreementMember

CNXA:EachWeekForNextThreeWeeksMember

2022-07-29

2022-07-29

0001674440

CNXA:CedarAgreementMember

CNXA:ThereafterPerWeekMember

2022-07-29

2022-07-29

0001674440

CNXA:LoanAndSecurityAgreementMember

CNXA:ArmisticeCapitalMasterFundLtdMember

srt:MaximumMember

2023-01-06

0001674440

CNXA:LoanAndSecurityAgreementMember

CNXA:ArmisticeCapitalMasterFundLtdMember

CNXA:NotesMember

2023-01-04

2023-01-06

0001674440

CNXA:LoanAndSecurityAgreementMember

CNXA:ArmisticeCapitalMasterFundLtdMember

2023-01-06

0001674440

CNXA:LoanAndSecurityAgreementMember

CNXA:ArmisticeCapitalMasterFundLtdMember

2023-01-04

2023-01-06

0001674440

us-gaap:WarrantMember

CNXA:LoanAndSecurityAgreementMember

CNXA:ArmisticeCapitalMasterFundLtdMember

2023-01-06

2023-01-06

0001674440

us-gaap:WarrantMember

CNXA:LoanAndSecurityAgreementMember

CNXA:ArmisticeCapitalMasterFundLtdMember

2023-01-06

0001674440

CNXA:LoanAndSecurityAgreementMember

CNXA:ArmisticeCapitalMasterFundLtdMember

2023-07-31

2023-07-31

0001674440

CNXA:LoanAndSecurityAgreementMember

CNXA:ArmisticeCapitalMasterFundLtdMember

2023-07-31

0001674440

CNXA:LoanAndSecurityAgreementMember

CNXA:ArmisticeCapitalMasterFundLtdMember

2023-04-30

0001674440

CNXA:LoanAndSecurityAgreementMember

CNXA:ArmisticeCapitalMasterFundLtdMember

2023-05-01

2023-07-31

0001674440

CNXA:MegedAgreementMember

2023-06-08

2023-06-08

0001674440

us-gaap:RelatedPartyMember

2022-07-31

0001674440

2022-06-15

2022-06-15

0001674440

us-gaap:InvestorMember

2022-06-15

2022-06-15

0001674440

CNXA:GabrielGoldmanMember

2022-06-27

2022-06-27

0001674440

CNXA:GamefaceAIMember

2022-06-27

2022-06-27

0001674440

CNXA:MidcityCapitalLtdMember

2022-08-25

2022-08-25

0001674440

CNXA:SecuritiesPurchaseAgreementMember

us-gaap:InvestorMember

2022-09-28

2022-09-28

0001674440

CNXA:SecuritiesPurchaseAgreementMember

us-gaap:InvestorMember

2022-09-28

0001674440

CNXA:SecuritiesPurchaseAgreementMember

us-gaap:InvestorMember

CNXA:FiveYearWarrantsMember

2022-09-28

0001674440

CNXA:SecuritiesPurchaseAgreementMember

us-gaap:InvestorMember

CNXA:SevenYearWarrantsMember

2022-09-28

2022-09-28

0001674440

CNXA:SecuritiesPurchaseAgreementMember

us-gaap:InvestorMember

CNXA:SevenPointFiveYearWarrantsMember

2022-09-28

0001674440

2022-10-12

2022-10-12

0001674440

2022-11-21

2022-11-21

0001674440

2023-01-26

2023-01-26

0001674440

CNXA:SecuritiesPurchaseAgreementMember

us-gaap:InvestorMember

CNXA:SevenPointFiveYearWarrantsMember

2022-09-28

2022-09-28

0001674440

CNXA:SecuritiesPurchaseAgreementMember

us-gaap:InvestorMember

2023-01-31

0001674440

2023-01-31

0001674440

2022-06-01

2022-06-30

0001674440

2023-03-21

0001674440

srt:MinimumMember

2023-01-31

0001674440

CNXA:SharePurchaseAgreementMember

2022-11-25

2022-11-27

0001674440

CNXA:EmployeeAgreementMember

2022-11-27

0001674440

CNXA:SharePurchaseAgreementMember

2022-11-27

0001674440

CNXA:FoundationSportsToCharlesRuddyMember

2022-12-05

0001674440

2022-12-05

0001674440

us-gaap:CommonStockMember

us-gaap:SubsequentEventMember

2023-08-01

2023-08-01

0001674440

us-gaap:CommonStockMember

us-gaap:SubsequentEventMember

CNXA:RodneyRapsonMember

2023-08-17

2023-08-17

0001674440

us-gaap:CommonStockMember

us-gaap:SubsequentEventMember

2023-08-31

2023-08-31

0001674440

us-gaap:CommonStockMember

us-gaap:SubsequentEventMember

2023-09-18

2023-09-18

0001674440

us-gaap:CommonStockMember

us-gaap:SubsequentEventMember

2023-09-19

2023-09-19

0001674440

us-gaap:SubsequentEventMember

CNXA:UFSAgreementMember

2023-08-07

2023-08-07

0001674440

us-gaap:SubsequentEventMember

CNXA:UFSAgreementMember

CNXA:EachWeekForNextThreeWeeksMember

2023-08-07

2023-08-07

0001674440

CNXA:AmendedUFSAgreementMember

us-gaap:SubsequentEventMember

2023-08-21

2023-08-21

0001674440

us-gaap:SubsequentEventMember

CNXA:SecondMegedAgreementMember

2023-09-19

2023-09-19

0001674440

us-gaap:SubsequentEventMember

CNXA:SecondMegedAgreementMember

CNXA:EachWeekForNextThreeWeeksMember

2023-09-19

2023-09-19

iso4217:USD

xbrli:shares

iso4217:USD

xbrli:shares

CNXA:Integer

xbrli:pure

UNITED

STATES

SECURITIES

AND EXCHANGE COMMISSION

Washington,

D.C. 20549

FORM

10-Q

(Mark

One)

| ☒ |

QUARTERLY

REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For

the quarterly period ended July 31, 2023

| ☐ |

TRANSITION

REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT |

For

the transition period from ________ to ________

Commission

File Number: 01-41423

CONNEXA

SPORTS TECHNOLOGIES INC.

(Exact

name of registrant as specified in its charter)

| Delaware |

|

61-1789640 |

(State

or other jurisdiction of

incorporation

or organization) |

|

(I.R.S.

Employer

Identification

No.) |

2709

NORTH ROLLING ROAD, SUITE 138

WINDSOR

MILL,

MARYLAND

21244

(Address

of principal executive offices, including Zip Code)

(443)

407-7564

(Registrant’s

Telephone Number, including Area Code)

Securities

registered pursuant to Section 12(b) of the Act:

| Title

of each class |

|

Trading

Symbol(s) |

|

Name

of each exchange on which registered |

| Common Stock, $0.001 par

value |

|

CNXA |

|

Nasdaq Capital Market |

Securities

registered pursuant to Section 12(g) of the Securities Exchange Act of 1934: None

Indicate

by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Securities Exchange Act

of 1934. Yes ☐ No ☒

Indicate

by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange

Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2)

has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate

by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule

405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant

was required to submit such files). Yes ☒ No ☐

Indicate

by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting

company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,”

“smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Securities Exchange Act of 1934

Act.

| Large

accelerated filer ☐ |

Accelerated

filer ☐ |

| Non-accelerated

filer ☒ |

Smaller

reporting company ☒ |

| |

Emerging

growth company ☐ |

If

an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying

with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate

by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

If

securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant

included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate

by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation

received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

The

number of shares outstanding of the registrant’s Common Stock, $0.001 par value per share, as of October 2, 2023, was 773,975.

CAUTIONARY

STATEMENT REGARDING FORWARD LOOKING INFORMATION

This

quarterly report contains forward-looking statements within the meaning of Section 27A of the Securities Exchange Act of 1934, as amended

(the “Exchange Act”). The words “believe,” “expect,” “anticipate,” “intend,”

“estimate,” “may,” “should,” “could,” “will,” “plan,” “future,”

“continue,” and other expressions that are predictions of or indicate future events and trends and that do not relate to

historical matters identify forward-looking statements. These forward-looking statements are based largely on our expectations or forecasts

of future events, can be affected by inaccurate assumptions, and are subject to various business risks and known and unknown uncertainties,

a number of which are beyond our control. Therefore, actual results could differ materially from the forward-looking statements contained

in this document, and readers are cautioned not to place undue reliance on such forward-looking statements. We undertake no obligation

to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise. A wide

variety of factors could cause or contribute to such differences and could adversely impact revenues, profitability, cash flows and capital

needs. There can be no assurance that the forward-looking statements contained in this document will, in fact, transpire or prove to

be accurate. These statements are only predictions and involve known and unknown risks, uncertainties and other factors, including the

risks in the section entitled “Risk Factors” in our Form 10-K for the fiscal year ended April 30, 2023, filed on September

14, 2023, that may cause our or our industry’s actual results, levels of activity, performance or achievements to be materially

different from any future results, levels of activity, performance or achievements expressed or implied by any forward-looking statements.

Important

factors that may cause the actual results to differ from the forward-looking statements, projections or other expectations include, but

are not limited to, the following:

| |

● |

risk that we will not be

able to remediate identified material weaknesses in our internal control over financial reporting and disclosure controls and procedures; |

| |

|

|

| |

● |

risk that we fail to meet

the requirements of the agreements under which we acquired our business interests, including any cash payments to the business operations,

which could result in the loss of our right to continue to operate or develop the specific businesses described in the agreements; |

| |

|

|

| |

● |

risk that we will be unable

to secure additional financing in the near future in order to commence and sustain our planned development and growth plans; |

| |

|

|

| |

● |

risk that we cannot attract,

retain and motivate qualified personnel, particularly employees, consultants and contractors for our operations; |

| |

|

|

| |

● |

risks and uncertainties

relating to the various industries and operations we are currently engaged in; |

| |

|

|

| |

● |

results of initial feasibility,

pre-feasibility and feasibility studies, and the possibility that future growth, development or expansion will not be consistent

with our expectations; |

| |

|

|

| |

● |

risks related to the inherent

uncertainty of business operations including profit, cost of goods, production costs and cost estimates and the potential for unexpected

costs and expenses; |

| |

|

|

| |

● |

risks related to commodity

price fluctuations; |

| |

|

|

| |

● |

the uncertainty of profitability

based upon our history of losses; |

| |

|

|

| |

● |

risks related to failure

to obtain adequate financing on a timely basis and on acceptable terms for our planned development projects; |

| |

|

|

| |

● |

risks related to environmental

regulation and liability; |

| |

|

|

| |

● |

risks related to tax assessments;

and |

| |

|

|

| |

● |

other risks and uncertainties

related to our prospects, properties and business strategy. |

Although

we believe that the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee future results, levels

of activity, performance or achievements. You should not place undue reliance on these forward-looking statements, which speak only as

of the date of this report. Except as required by law, we do not undertake to update or revise any of the forward-looking statements

to conform these statements to actual results, whether as a result of new information, future events or otherwise.

As

used in this quarterly report, the “Connexa,” “Company,” “we,” “us,” or “our”

refer to Connexa Sports Technologies Inc. and its subsidiaries, unless otherwise indicated.

CONNEXA

SPORTS TECHNOLOGIES INC.

(FORMERLY

KNOWN AS SLINGER BAG INC. AND LAZEX INC.)

INDEX

PART

I - FINANCIAL INFORMATION

Item

1. Consolidated Financial Statements

CONNEXA

SPORTS TECHNOLOGIES, INC.

CONSOLIDATED

BALANCE SHEETS (IN US$)

JULY

31, 2023 (UNAUDITED) AND APRIL 30, 2023

| | |

JULY 31, 2023 | | |

APRIL 30, 2023 | |

| | |

(UNAUDITED) | | |

| |

| | |

| | |

| |

| ASSETS | |

| | | |

| | |

| Current Assets: | |

| | | |

| | |

| Cash and cash equivalents | |

$ | 386,459 | | |

$ | 202,095 | |

| Accounts receivable, net | |

| 444,622 | | |

| 399,680 | |

| Inventories, net | |

| 2,336,918 | | |

| 3,189,766 | |

| Prepaid inventory | |

| 1,134,368 | | |

| 936,939 | |

| Prepaid expenses and other current assets | |

| 280,820 | | |

| 263,020 | |

| | |

| | | |

| | |

| Total Current Assets | |

| 4,583,187 | | |

| 4,991,500 | |

| | |

| | | |

| | |

| Non-Current Assets: | |

| | | |

| | |

| Note receivable - former subsidiary | |

| 2,000,000 | | |

| 2,000,000 | |

| Fixed assets, net of depreciation | |

| - | | |

| 14,791 | |

| Intangible assets, net of amortization | |

| 1,000 | | |

| 101,281 | |

| | |

| | | |

| | |

| Total Non-Current Assets | |

| 2,001,000 | | |

| 2,116,072 | |

| | |

| | | |

| | |

| | |

| | | |

| | |

| TOTAL ASSETS | |

$ | 6,584,187 | | |

$ | 7,107,572 | |

| | |

| | | |

| | |

| LIABILITIES AND SHAREHOLDERS’ EQUITY (DEFICIT) | |

| | | |

| | |

| | |

| | | |

| | |

| LIABILITIES | |

| | | |

| | |

| Current Liabilities: | |

| | | |

| | |

| Accounts payable | |

$ | 6,087,311 | | |

$ | 5,496,629 | |

| Accrued expenses | |

| 5,197,460 | | |

| 4,911,839 | |

| Accrued interest | |

| 41,522 | | |

| 25,387 | |

| Accrued interest - related party | |

| 917,957 | | |

| 917,957 | |

| Accrued interest | |

| 917,957 | | |

| 917,957 | |

| Current portion of notes payable, net of discount | |

| 1,959,671 | | |

| 1,484,647 | |

| Derivative liabilities | |

| 8,345,052 | | |

| 10,489,606 | |

| Contingent consideration | |

| 418,455 | | |

| 418,455 | |

| Other current liabilities | |

| 330,065 | | |

| 22,971 | |

| | |

| | | |

| | |

| Total Current Liabilities | |

| 23,297,493 | | |

| 23,767,491 | |

| | |

| | | |

| | |

| Long-Term Liabilities: | |

| | | |

| | |

| Notes payable related parties, net of current portion | |

| 1,655,966 | | |

| 1,953,842 | |

| | |

| | | |

| | |

| Total Long-Term Liabilities | |

| 1,655,966 | | |

| 1,953,842 | |

| | |

| | | |

| | |

| Total Liabilities | |

| 24,953,459 | | |

| 25,721,333 | |

| | |

| | | |

| | |

| Commitments and contingency | |

| - | | |

| - | |

| | |

| | | |

| | |

| SHAREHOLDERS’ EQUITY (DEFICIT) | |

| | | |

| | |

| | |

| | | |

| | |

| Common stock, par value, $0.001, 300,000,000 shares authorized, 528,297 and 338,579 shares issued and outstanding as of July 31,

2023 and April 30, 2023, respectively | |

| 528 | | |

| 339 | |

| Additional paid in capital | |

| 134,112,083 | | |

| 132,993,998 | |

| Accumulated deficit | |

| (152,597,375 | ) | |

| (151,750,610 | ) |

| Accumulated other comprehensive income (loss) | |

| 115,492 | | |

| 142,512 | |

| | |

| | | |

| | |

| Total Stockholders’ Equity (Deficit) | |

| (18,369,272 | ) | |

| (18,613,761 | ) |

| | |

| | | |

| | |

| TOTAL LIABILITIES AND STOCKHOLDERS’ EQUITY (DEFICIT) | |

$ | 6,584,187 | | |

$ | 7,107,572 | |

The

accompanying notes are an integral part of these unaudited consolidated financial statements.

CONNEXA

SPORTS TECHNOLOGIES, INC

CONSOLIDATED

STATEMENTS OF OPERATIONS (IN US$) (UNAUDITED)

THREE

MONTHS ENDED JULY 31, 2023 AND 2022

| | |

2023 | | |

2022 | |

| | |

| | |

| |

| NET SALES | |

$ | 3,120,231 | | |

$ | 3,583,336 | |

| | |

| | | |

| | |

| COST OF SALES | |

| 2,227,482 | | |

| 2,562,044 | |

| | |

| | | |

| . | |

| GROSS PROFIT | |

| 892,749 | | |

| 1,021,292 | |

| | |

| | | |

| | |

| OPERATING EXPENSES | |

| | | |

| | |

| Selling and marketing expenses | |

| 242,353 | | |

| 756,823 | |

| General and administrative expenses | |

| 2,505,060 | | |

| 3,314,610 | |

| Research and development costs | |

| - | | |

| 19,425 | |

| | |

| | | |

| | |

| Total Operating Expenses | |

| 2,747,413 | | |

| 4,090,858 | |

| | |

| | | |

| | |

| OPERATING LOSS | |

| (1,854,664 | ) | |

| (3,069,566 | ) |

| | |

| | | |

| | |

| NON-OPERATING INCOME (EXPENSE) | |

| | | |

| | |

| Amortization of debt discounts | |

| (777,192 | ) | |

| (2,872,222 | ) |

| Loss on conversion of accounts payable to common stock | |

| (289,980 | ) | |

| - | |

| Change in fair value of derivative liability | |

| 2,144,554 | | |

| 3,687,495 | |

| Interest expense | |

| (69,483 | ) | |

| (191,303 | ) |

| Interest expense - related party | |

| - | | |

| (61,121 | ) |

| Interest expense | |

| - | | |

| (61,121 | ) |

| | |

| | | |

| | |

| Total Non-Operating Income (Expenses) | |

| 1,007,899 | | |

| 562,849 | |

| | |

| | | |

| | |

| | |

| | | |

| | |

| DISCONTINUED OPERATIONS | |

| | | |

| | |

| Loss from discontinued operations | |

| - | | |

| (1,759,714 | ) |

| Loss on disposal of subsidiaries | |

| - | | |

| | |

| LOSS FROM DISCONTINUED OPERATIONS | |

| - | | |

| (1,759,714 | ) |

| | |

| | | |

| | |

| | |

| | | |

| | |

| Provision for income taxes | |

| - | | |

| - | |

| | |

| | | |

| | |

| NET LOSS | |

$ | (846,765 | ) | |

$ | (4,266,431 | ) |

| | |

| | | |

| | |

| Other comprehensive income (loss) | |

| | | |

| | |

| Foreign currency translations adjustment | |

| (27,020 | ) | |

| 58,139 | |

| Comprehensive income (loss) | |

$ | (873,785 | ) | |

$ | (4,208,292 | ) |

| | |

| | | |

| | |

| Net income (loss) per share - basic and diluted | |

| | | |

| | |

| Continuing operations | |

$ | (1.93 | ) | |

$ | (14.27 | ) |

| Discontinued operations | |

$ | - | | |

$ | (10.02 | ) |

| | |

| | | |

| | |

| Net loss per share - basic and diluted | |

$ | (1.93 | ) | |

$ | (24.29 | ) |

| | |

| | | |

| | |

| Weighted average common shares outstanding - basic and diluted | |

| 438,354 | | |

| 175,653 | |

The

accompanying notes are an integral part of these unaudited consolidated financial statements.

CONNEXA

SPORTS TECHNOLOGIES, INC

CONSOLIDATED

STATEMENT OF CHANGES IN SHAREHOLDERS’ EQUITY (DEFICIT) (IN US$) (UNAUDITED)

FOR

THE THREE MONTHS ENDED JULY 31, 2023 AND 2022

| | |

| | |

| | |

| | |

Accumulated | | |

| | |

| |

| | |

| | |

Additional | | |

Other | | |

| | |

| |

| | |

Common Stock | | |

Paid-In | | |

Comprehensive | | |

Accumulated | | |

| |

| | |

Shares | | |

Amount | | |

Capital | | |

Income (Loss) | | |

Deficit | | |

Total | |

| | |

| | |

| | |

| | |

| | |

| | |

| |

| Balance - May 1, 2022 | |

| 104,871 | | |

$ | 105 | | |

$ | 113,053,790 | | |

$ | 54,962 | | |

$ | (80,596,925 | ) | |

$ | 32,511,932 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Stock issued for: | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Conversion of notes payable | |

| 109,737 | | |

| 110 | | |

| 14,046,190 | | |

| - | | |

| - | | |

| 14,046,300 | |

| Acquisition | |

| 14,960 | | |

| 15 | | |

| 915,530 | | |

| - | | |

| - | | |

| 915,545 | |

| Services | |

| 625 | | |

| 1 | | |

| 35,249 | | |

| - | | |

| - | | |

| 35,250 | |

| Cash | |

| 26,219 | | |

| 26 | | |

| 4,194,974 | | |

| - | | |

| - | | |

| 4,195,000 | |

| Fractional share issuance | |

| 38 | | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | |

| Share-based compensation | |

| - | | |

| - | | |

| 277,625 | | |

| - | | |

| - | | |

| 277,625 | |

| Change in comprehensive income | |

| - | | |

| - | | |

| - | | |

| 58,139 | | |

| - | | |

| 58,139 | |

| Change in comprehensive income (loss) | |

| - | | |

| - | | |

| - | | |

| 58,139 | | |

| - | | |

| 58,139 | |

| Net loss for the period | |

| - | | |

| - | | |

| - | | |

| - | | |

| (4,266,431 | ) | |

| (4,266,431 | ) |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Balance - July 31, 2022 | |

| 256,450 | | |

$ | 257 | | |

$ | 132,523,358 | | |

$ | 113,101 | | |

$ | (84,863,356 | ) | |

$ | 47,773,360 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Balance - May 1, 2023 | |

| 338,579 | | |

$ | 339 | | |

$ | 132,993,998 | | |

$ | 142,512 | | |

$ | (151,750,610 | ) | |

$ | (18,613,761 | ) |

| Balance | |

| 338,579 | | |

$ | 339 | | |

$ | 132,993,998 | | |

$ | 142,512 | | |

$ | (151,750,610 | ) | |

$ | (18,613,761 | ) |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Stock issued for: | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Services | |

| 188 | | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | |

| Accounts payable | |

| 67,500 | | |

| 67 | | |

| 559,913 | | |

| - | | |

| - | | |

| 559,980 | |

| Acquisition | |

| 1,350 | | |

| 1 | | |

| (1 | ) | |

| - | | |

| - | | |

| - | |

| Cashless exercise of warrants | |

| 27,000 | | |

| 27 | | |

| (27 | ) | |

| - | | |

| - | | |

| - | |

| Satisfaction of profit guarantee on note payable | |

| 93,680 | | |

| 94 | | |

| 558,200 | | |

| - | | |

| - | | |

| 558,294 | |

| Share-based compensation | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | |

| Change in comprehensive income | |

| - | | |

| - | | |

| - | | |

| (27,020 | ) | |

| - | | |

| (27,020 | ) |

| Change in comprehensive income (loss) | |

| - | | |

| - | | |

| - | | |

| (27,020 | ) | |

| - | | |

| (27,020 | ) |

| Net loss for the period | |

| - | | |

| - | | |

| - | | |

| - | | |

| (846,765 | ) | |

| (846,765 | ) |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Balance - July 31, 2023 | |

| 528,297 | | |

$ | 528 | | |

$ | 134,112,083 | | |

$ | 115,492 | | |

$ | (152,597,375 | ) | |

$ | (18,369,272 | ) |

| Balance | |

| 528,297 | | |

$ | 528 | | |

$ | 134,112,083 | | |

$ | 115,492 | | |

$ | (152,597,375 | ) | |

$ | (18,369,272 | ) |

The

accompanying notes are an integral part of these unaudited consolidated financial statements.

CONNEXA SPORTS TECHNOLOGIES, INC

CONSOLIDATED STATEMENTS OF CASH FLOWS (IN US$) (UNAUDITED)

THREE MONTHS ENDED JULY 31, 2023 AND 2022

| | |

2023 | | |

2022 | |

| CASH FLOW FROM OPERATING ACTIVITIES | |

| | | |

| | |

| Net loss | |

$ | (846,765 | ) | |

$ | (4,266,431 | ) |

| Adjustments to reconcile net loss to net cash used in operating activities | |

| | | |

| | |

| Depreciation, amortization and impairment expense | |

| 115,072 | | |

| - | |

| Change in fair value of derivative liability | |

| (2,144,554 | ) | |

| (3,687,495 | ) |

| Shares and warrants issued for services | |

| - | | |

| 35,250 | |

| Share-based compensation | |

| - | | |

| 277,625 | |

| Amortization of debt discounts | |

| 777,192 | | |

| 2,872,222 | |

| Settlement expense | |

| 558,294 | | |

| - | |

| Loss on settlement of accounts payable | |

| 289,980 | | |

| - | |

| Loss on conversion of convertible notes | |

| - | | |

| - | |

| | |

| | | |

| | |

| Changes in assets and liabilities, net of acquired amounts | |

| | | |

| | |

| Accounts receivable | |

| 265,992 | | |

| - | |

| Inventories | |

| 852,848 | | |

| - | |

| Prepaid inventory | |

| (197,429 | ) | |

| - | |

| Prepaid expenses and other current assets | |

| (1,316 | ) | |

| - | |

| Accounts payable and accrued expenses | |

| 255,199 | | |

| - | |

| Other current liabilities | |

| 326,550 | | |

| - | |

| Accrued interest | |

| 16,135 | | |

| - | |

| Accrued interest - related parties | |

| - | | |

| - | |

| Total adjustments | |

| 1,113,963 | | |

| (502,398 | ) |

| | |

| | | |

| | |

| Net cash used in operating activities of continuing operations | |

| 267,198 | | |

| (4,768,829 | ) |

| Net cash provided by operating activities of discontinued operations | |

| - | | |

| - | |

| Net cash used in operating activities | |

| 267,198 | | |

| (4,768,829 | ) |

| | |

| | | |

| | |

| CASH FLOWS FROM FINANCING ACTIVITIES | |

| | | |

| | |

| Proceeds from issuance of common stock for cash | |

| - | | |

| 4,195,000 | |

| Proceeds from notes payable | |

| - | | |

| 925,000 | |

| Payments of notes payable - related parties | |

| (298,834 | ) | |

| (15,386 | ) |

| Payments of notes payable | |

| (302,168 | ) | |

| (1,698,485 | ) |

| Net cash provided by financing activities | |

| (601,002 | ) | |

| 3,406,129 | |

| | |

| | | |

| | |

| Effect of exchange rate fluctuations on cash and cash equivalents | |

| (17,996 | ) | |

| 67,357 | |

| | |

| | | |

| | |

| NET DECREASE IN CASH AND RESTRICTED CASH | |

| (351,800 | ) | |

| (1,295,343 | ) |

| | |

| | | |

| | |

| CASH AND RESTRICTED CASH - BEGINNING OF PERIOD | |

| 202,095 | | |

| 665,002 | |

| | |

| | | |

| | |

| CASH AND RESTRICTED CASH - END OF PERIOD | |

$ | (149,705 | ) | |

$ | (630,341 | ) |

| | |

| | | |

| | |

| CASH PAID DURING THE PERIOD FOR: | |

| | | |

| | |

| Interest expense | |

$ | - | | |

$ | - | |

| | |

| | | |

| | |

| Income taxes | |

$ | - | | |

$ | - | |

| | |

| | | |

| | |

| SUPPLEMENTAL INFORMATION - NON-CASH INVESTING AND FINANCING ACTIVITIES: | |

| | | |

| | |

| | |

| | | |

| | |

| Conversion of convertible notes payable and accrued interest to common stock | |

$ | - | | |

$ | 14,046,300 | |

| Shares issued for contingent consideration | |

$ | - | | |

$ | 915,545 | |

| Shares issued for settlement of accounts payable | |

$ | 270,000 | | |

$ | - | |

The

accompanying notes are an integral part of these unaudited consolidated financial statements.

CONNEXA

SPORTS TECHNOLOGIES INC.

NOTES

TO CONSOLIDATED FINANCIAL STATEMENTS

Note

1: ORGANIZATION AND NATURE OF BUSINESS

Organization

Lazex

Inc. (“Lazex”) was incorporated under the laws of the State of Nevada on July 12, 2015. On August 23, 2019, the majority

owner of Lazex entered into a Stock Purchase Agreement with Slinger Bag Americas Inc., a Delaware corporation (“Slinger Bag Americas”),

which was 100% owned by Slinger Bag Ltd. (“SBL”), an Israeli company. In connection with the Stock Purchase Agreement, Slinger

Bag Americas acquired 50,000 shares of common stock of Lazex for $332,239. On September 16, 2019, SBL transferred its ownership of Slinger

Bag Americas to Lazex in exchange for the 50,000 shares of Lazex acquired on August 23, 2019. As a result of these transactions, Lazex

owned 100% of Slinger Bag Americas and the sole shareholder of SBL owned 50,000 shares of common stock (approximately 82%) of Lazex.

Effective September 13, 2019, Lazex changed its name to Slinger Bag Inc.

On

October 31, 2019, Slinger Bag Americas acquired control of Slinger Bag Canada, Inc., (“Slinger Bag Canada”) a Canadian company

incorporated on November 3, 2017. There were no assets, liabilities or historical operational activity of Slinger Bag Canada.

On

February 10, 2020, Slinger Bag Americas became the 100% owner of SBL, along with SBL’s wholly owned subsidiary Slinger Bag International

(UK) Limited (“Slinger Bag UK”), which was formed on April 3, 2019. On February 10, 2020, the owner of SBL, contributed Slinger

Bag UK to Slinger Bag Americas for no consideration.

On

June 21, 2021, Slinger Bag Americas entered into a membership interest purchase agreement with Charles Ruddy to acquire a 100% ownership

stake in Foundation Sports Systems, LLC (“Foundation Sports”). On December 5, 2022, the Company sold 75% of Foundation Sports

back to the original sellers. As a result, at that time, the Company recorded a loss on the sale and deconsolidated Foundation Sports.

On

February 2, 2022, the Company entered into a share purchase agreement with Flixsense Pty, Ltd. (“Gameface”). As a result

of the share purchase agreement, Gameface would become a wholly owned subsidiary of the Company.

On

February 22, 2022, the Company entered into a merger agreement with PlaySight Interactive Ltd. (“PlaySight”) and Rohit Krishnan

(the “Shareholders’ Representative”). As a result of the merger agreement, PlaySight would become a wholly owned subsidiary

of the Company. In November 2022, the Company sold PlaySight and recorded a loss on the sale.

On

May 16, 2022, the Company changed its domicile from Nevada to Delaware. On April 7, 2022, the Company effected a name change to Connexa

Sports Technologies Inc. We also changed our ticker symbol, “CNXA”.

On

June 14, 2022, the Company effected a 1-for-10 reverse stock split, where the Company’s common stock began to trade on a reverse

split adjusted basis. No fractional shares were issued in connection with the reverse stock split and all such fractional interests were

rounded up to the nearest whole number of shares of common stock. All references to the outstanding stock have been retrospectively adjusted

to reflect this reverse split. The Company also consummated a public offering of shares of its common stock and the listing of its common

stock on the Nasdaq Capital Market.

On

October 10, 2022, the Company received a letter from the Listing Qualifications Department of the Nasdaq indicating that the Company’s

common stock is subject to potential delisting from Nasdaq because, for a period of 30 consecutive business days, the bid price of the

Company’s common stock has closed below the minimum $1.00 per share requirement for continued listing under Nasdaq Listing Rule

5450(a)(1) (the “Bid Price Rule”). The Nasdaq notice indicated that, in accordance with Nasdaq Listing Rule 5810(c)(3)(A),

the Company would be provided 180 calendar days, or until April 10, 2023, to regain compliance. If the Company were to fail to regain

compliance with the Bid Price Rule before April 10, 2023, the Company may be eligible for an additional

180-calendar day compliance period. The Company failed to regain compliance with the Bid Price Rule by April 10, 2023 and requested and

received an additional period of 180 days until October 9, 2023 to regain compliance with the Minimum Bid Price Requirement. On

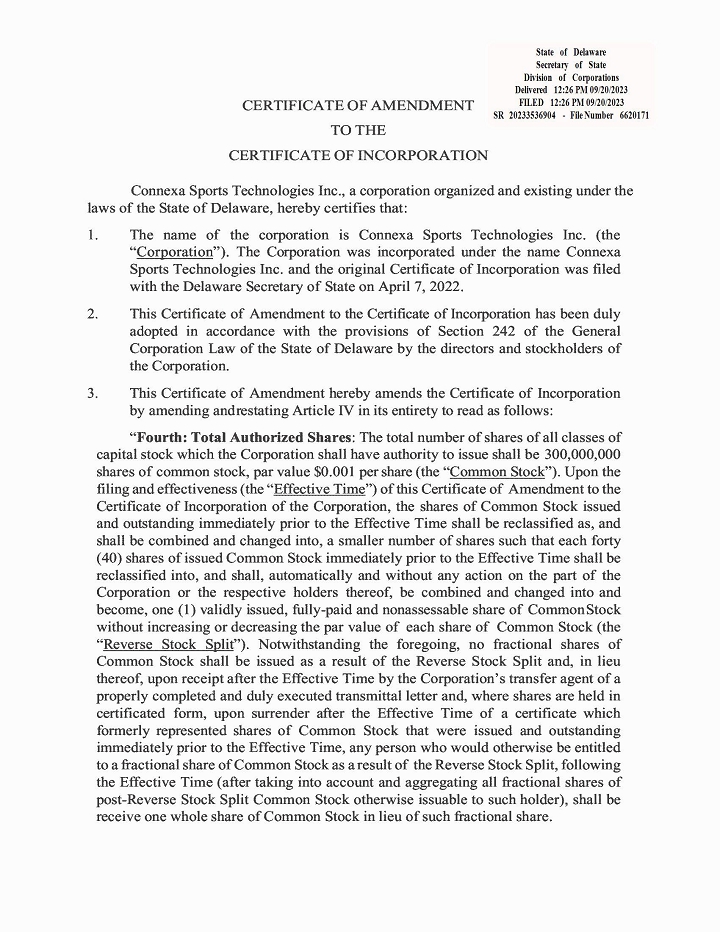

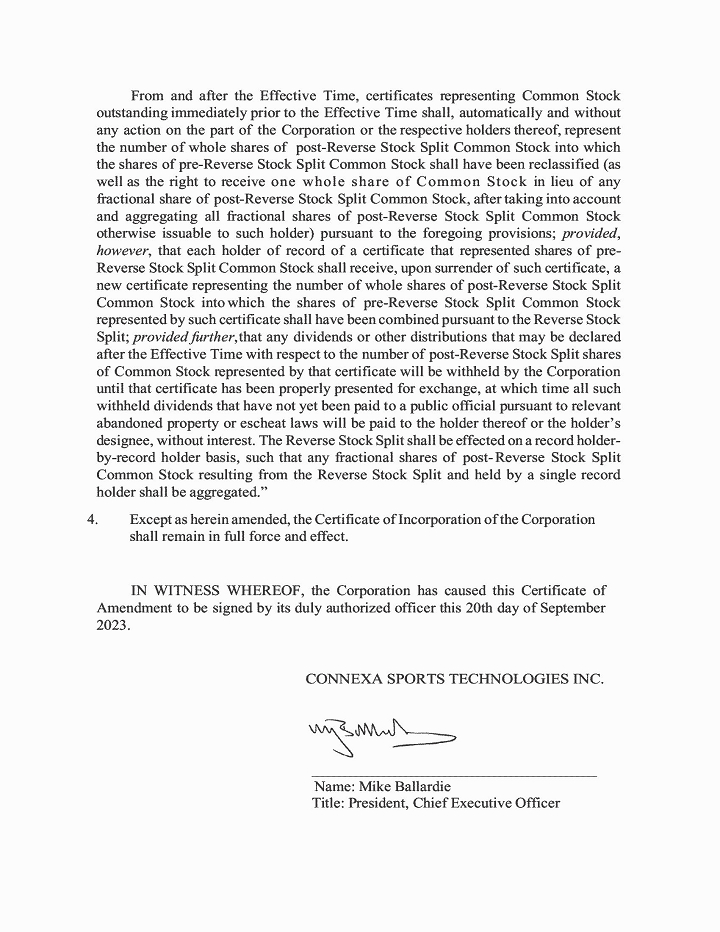

September 13, 2023, the Company obtained shareholder consent to effect a reverse split of its shares of common stock. On September 22,

2023, the Company effected a 1-for-40 reverse stock split, where the Company’s common stock began to trade on a reverse split adjusted

basis commencing with trading on September 25, 2023. No fractional shares were issued in connection with the reverse stock split and

all such fractional interests were rounded up to the nearest whole number of shares of common stock. All references herein to the outstanding

stock have been retrospectively adjusted to reflect this reverse split. In order to regain compliance with the Bid Price Rule by October

9, 2023, the Company’s shares of common stock must trade above $1.00 for 10 consecutive trading days, which means that the Company’s

shares must remain above $1.00 through the close of the Nasdaq on Friday, October 9, 2023 in order to regain compliance with the Bid

Price Rule.

On

July 26, 2023, the Company received a letter from the Listing Qualifications Department of Nasdaq indicating that the Company’s

stockholders’ equity as reported in its Quarterly Report on Form 10-Q for the quarterly period ended January 31, 2023 did not satisfy

the continued listing requirement under Nasdaq Listing Rule 5550(b)(1), which requires that a listed company’s stockholders’

equity be at least $2.5 million (the “Minimum Stockholders’ Equity Requirement”). In addition, the Company did not

meet the alternatives of listed securities or net income from continuing operations as of the date of the letter. The Company timely

submitted a compliance plan to the Panel and on August 23, 2023 received notice from Nasdaq that it has until January 22, 2024 to demonstrate

compliance with the Minimum Stockholders’ Equity Requirement.

There

can be no assurance that the Company will be able to satisfy the Nasdaq’s continued listing requirements, regain compliance with

the Rule, the Minimum Stockholders’ Equity Requirement, and the Minimum Bid Price Requirement, and maintain compliance with other

Nasdaq listing requirements.

For

further details on PlaySight and Foundation Sports we refer you to our Annual Report on Form 10-K for the year ended April 30, 2023,

filed with the Securities and Exchange Commission on September 14, 2023. This Form 10-K and the consolidated financial statements will

concentrate on our existing business as reflected in the following paragraph.

The

Company operates in the sport equipment and technology business. The Company is the owner of the Slinger Launcher, which is a portable

tennis ball launcher as well as other associated tennis accessories and Gameface AI an Australian artificial intelligence sports software

company.

The

operations of Slinger Bag Inc., Slinger Bag Americas, Slinger Bag Canada, Slinger Bag UK, SBL, and Gameface are collectively referred

to as the “Company.”

Basis

of Presentation

The

accompanying condensed consolidated financial statements of the Company are presented in accordance with accounting principles generally

accepted in the United States of America (“GAAP”). As a result of the transactions described above, the accompanying consolidated

financial statements include the combined results of Slinger Bag Inc., Slinger Bag Americas, Slinger Bag Canada, Slinger Bag UK, SBL,

and Gameface for the periods ended July 31, 2023 and 2022. The operations of Foundation Sports and PlaySight are included as discontinued

operations in our statements of operations as these entities were sold in November 2022 and December 2022 for the period ended July 31,

2022.

Impact

of COVID-19 Pandemic

The

Company continues to carefully monitor the global COVID-19 pandemic status and its impact on its business. In that regard, while the

Company has continued to sell its products it has previously experienced certain minor disruptions in its supply chains. The Company

expects the significance of the COVID-19 pandemic, including the extent of its effect on the Company’s financial and operational

results, to be dictated by, among other things, the on-going global efforts to contain it. While the Company has not experienced any

material disruptions to its business and operations as a result of the COVID-19 pandemic, it is possible such disruptions may occur in

the future which may impact its financial and operational results, and which could be material.

Impact

of Russian and Ukrainian Conflict

In

February 2022, the Russian Federation and Belarus commenced a military action with the country of Ukraine. We are closely monitoring

the unfolding events due to the Russia-Ukraine conflict and its regional and global ramifications. We have one distributor in Russia,

which is not material to our overall financial results. We do not currently have operations in Ukraine or Belarus. We are monitoring

any broader economic impact from the current crisis. The specific impact on the Company’s financial condition, results of operations,

and cash flows is also not determinable as of the date of these financial statements. However, to the extent that such military action

spreads to other countries, intensifies, or otherwise remains active, such action could have a material adverse effect on our financial

condition, results of operations, and cash flows.

Note

2: GOING CONCERN

The

financial statements have been prepared on a going concern basis, which assumes the Company will be able to realize its assets and discharge

its liabilities in the normal course of business for the foreseeable future. The Company has an accumulated deficit of $152,597,375 as

of July 31, 2023, and more losses are anticipated in the development of the business. Accordingly, there is substantial doubt about the

Company’s ability to continue as a going concern. These financial statements do not include any adjustments related to the recoverability

and classification of assets or the amounts and classification of liabilities that might be necessary should the Company be unable to

continue as a going concern.

The

ability to continue as a going concern is dependent upon the Company generating profitable operations in the future and/or being able

to obtain the necessary financing to meet its obligations and repay its liabilities arising from normal business operations when they

become due. Management intends to finance operating costs over the next twelve months with existing cash on hand, loans from related

parties, and/or private placement of debt and/or common stock. In the event that the Company is unable to successfully raise capital

and/or generate revenues, the Company will likely reduce general and administrative expenses, and cease or delay its development plan

until it is able to obtain sufficient financing. The Company has begun reducing operating expenses and cash outflows by selling PlaySight,

as well as selling 75% of Foundation Sports in November and December 2022, respectively to the former shareholders of those companies.

There can be no assurance that additional funds will be available on terms acceptable to the Company, or at all. We have recorded the

25% investment in Foundation Sprots at $0.

Note

3: SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Interim

Financial Statements

The

accompanying condensed financial statements of the Company have been prepared without audit, pursuant to the rules and regulations of

the Securities and Exchange Commission. Certain information and disclosures required by accounting principles generally accepted in the

United States have been condensed or omitted pursuant to such rules and regulations. These condensed financial statements reflect all

adjustments that, in the opinion of management, are necessary to present fairly the results of operations of the Company for the period

presented. The results of operations for the three months ended July 31, 2023, are not necessarily indicative of the results that may

be expected for any future period or the fiscal year ending April 30, 2024 and should be read in conjunction with the Company’s

Annual Report on Form 10-K for the year ended April 30, 2023, filed with the Securities and Exchange Commission on September 14, 2023.

Use

of Estimates

The

preparation of consolidated financial statements in conformity with GAAP requires management to make estimates and assumptions that affect

the amounts reported in the financial statements and accompanying notes. Accordingly, actual results could differ from those estimates.

Financial

Statement Reclassification

Certain

prior year amounts within accounts payable, accrued expenses, and certain operating expenses have been reclassified for consistency with

the current year presentation and had no effect on the Company’s balance sheet, net loss, shareholders’ deficit or cash flows.

Cash

and Cash Equivalents

The

Company considers all highly liquid investments with an original maturity of three months or less when purchased to be cash equivalents.

The majority of payments due from banks for credit card transactions process within 24 to 48 hours and are accordingly classified as

cash and cash equivalents.

Accounts

Receivable

The

Company’s accounts receivable are non-interest bearing trade receivables resulting from the sale of products and payable over terms

ranging from 15 to 60 days. The Company provides an allowance for doubtful accounts at the point when collection is considered doubtful.

Once all collection efforts have been exhausted, the Company charges-off the receivable with the allowance for doubtful accounts. The

Company recorded $200,000 and $209,690 in allowance for doubtful accounts as of July 31, 2023 and April 30, 2023, respectively.

Inventory

Inventory

is valued at the lower of the cost (determined principally on a first-in, first-out basis) or net realizable value. The Company’s

valuation of inventory includes inventory reserves for inventory that will be sold below cost and the impact of inventory shrink. Inventory

reserves are based on historical information and assumptions about future demand and inventory shrink trends. The Company’s inventory

as of July 31, 2023 and April 30, 2023 consisted of the following:

SCHEDULE OF INVENTORY

| | |

July 31, 2023 | | |

April 30, 2023 | |

| Finished Goods | |

$ | 400,598 | | |

$ | 1,509,985 | |

| Component/Replacement Parts | |

| 2,064,041 | | |

| 1,712,553 | |

| Capitalized Duty/Freight | |

| 47,279 | | |

| 517,228 | |

| Inventory Reserve | |

| (175,000 | ) | |

| (550,000 | ) |

| Total | |

$ | 2,336,918 | | |

$ | 3,189,766 | |

Prepaid

Inventory

Prepaid

inventory represents inventory that is in-transit that has been paid for but not received from the Company’s third-party vendors.

The Company typically prepays for the purchase of materials and receives the products within three months after making payments. The

Company continuously monitors delivery from, and payments to, the vendors. If the Company has difficulty receiving products from a vendor,

the Company would cease purchasing products from such vendors in future periods. The Company has not had difficulty receiving products

during the reporting periods.

Property

and equipment

Property

and equipment acquired through business combinations are stated at the estimated fair value at the date of the acquisition. Purchases

of property and equipment are stated at cost, net of accumulated depreciation and impairment losses. Expenditures that materially increase

the useful life of the assets are capitalized. Ordinary repairs and maintenance are expensed as incurred. Depreciation and amortization

are computed using the straight-line method over the estimated useful lives of the related assets, which is an average of 5 years.

Concentration

of Credit Risk

The

Company maintains its cash in bank deposit accounts, the balances of which at times may exceed insured limits. The Company continually

monitors its banking relationships and consequently has not experienced any losses in such accounts. While we may be exposed to credit

risk, we consider the risk remote and do not expect that any such risk would result in a significant effect on our results of operations

or financial condition. See Note 4 for further details on the Company’s concentration of credit risk as well as other risks and

uncertainties.

Revenue

Recognition

The

Company recognizes revenue for their continuing operations in accordance with Accounting Standards Codification (“ASC”) 606,

the core principle of which is that an entity should recognize revenue to depict the transfer of promised goods or services to customers

in an amount that reflects the consideration to which the entity expects to be entitled to receive in exchange for those goods or services.

The Company recognizes revenue for its performance obligation associated with its contracts with customers at a point in time once products

are shipped. Amounts collected from customers in advance of shipping products ordered are reflected as contract liabilities on the accompanying

consolidated balance sheets. The Company’s standard terms are non-cancelable and do not provide for the right-of-return, other

than for defective merchandise covered under the Company’s standard warranty. The Company has not historically experienced any

significant returns or warranty issues.

The

Company recognizes revenue under ASC 606, “Revenue from Contracts with Customers”. The core principle of this revenue standard

is that a company should recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects

the consideration to which the company expects to be entitled in exchange for those goods or services. The following five steps are applied

to achieve that core principle:

Step

1: Identify the contract with the customer

The

Company determines that it has a contract with a customer when each party’s rights regarding the products or services to be transferred

can be identified, the payment terms for the services can be identified, the Company has determined the customer has the ability and

intent to pay, and the contract has commercial substance. At contract inception, the Company evaluates whether two or more contracts

should be combined and accounted for as a single contract and whether the combined or single contract includes more than one performance

obligation.

Step

2: Identify the performance obligations in the contract

The

Company’s customers are buying an integrated system. In evaluating whether the equipment is a separate performance obligation,

the Company’s management considered the customer’s ability to benefit from the equipment on its own or together with other

readily available resources and if so, whether the service and equipment are separately identifiable (i.e., is the service highly dependent

on, or highly interrelated with the equipment). Because the Products and Services included in the customer’s contract are integrated

and highly interdependent, and because they must work together to deliver the Solution, the Company has concluded that Products installed

on customer’s premise and Services contracted for by the customer are generally not distinct within the context of the contract

and, therefore, constitute a single, combined performance obligation.

Step

3: Determine the transaction price

The

transaction price is the amount of consideration to which an entity expects to be entitled in exchange for transferring promised goods

or services to a customer. The consideration promised in a contract with a customer includes predetermined fixed amounts, variable amounts,

or both. The Company’s contracts do not include any rights of returns or refunds.

The

Company collects each year’s service fees in advance and should therefore consider the existence of a significant financing component.

However, due to the fact that the payments are provided for the service of a one-year term, the Company elected to apply the practical

expedient under ASC 606 which exempts the adjustment of the consideration for the existence of a significant financing component when

the period between the transfer of the services and the payment for such services is one year or less.

Step

4: Allocate the transaction price to the performance obligations in the contract

Contracts

that contain multiple performance obligations require an allocation of the transaction price to each performance obligation based on

each performance obligation’s relative standalone selling price (“SSP”). The Company has identified a single performance

obligation in the contract, and therefore, the allocation provisions under ASC 606 do not apply to the Company’s contracts.

Step

5: Recognize revenue when the Company satisfies a performance obligation

Revenues

for the Company’s single, combined performance obligation are recognized on a straight-line basis over the customer’s contract

term, which is the period in which the parties to the contract have enforceable rights and obligations (Typically 3-4 years).

Business

Combinations

Upon

acquisition of a company, we determine if the transaction is a business combination, which is accounted for using the acquisition method

of accounting. Under the acquisition method, once control is obtained of a business, the assets acquired, and liabilities assumed, are

recorded at fair value. We use our best estimates and assumptions to assign fair value to the tangible and intangible assets acquired

and liabilities assumed at the acquisition date. One of the most significant estimates relates to the determination of the fair value

of these assets and liabilities. The determination of the fair values is based on estimates and judgments made by management. Our estimates

of fair value are based upon assumptions we believe to be reasonable, but which are inherently uncertain and unpredictable. Measurement

period adjustments are reflected at the time identified, up through the conclusion of the measurement period, which is the time at which

all information for determination of the values of assets acquired and liabilities assumed is received and is not to exceed one year

from the acquisition date. We may record adjustments to the fair value of these tangible and intangible assets acquired and liabilities

assumed, with the corresponding offset to goodwill. The Company elected to apply pushdown accounting to all entities acquired.

Additionally,

uncertain tax positions and tax-related valuation allowances are initially recorded in connection with a business combination as of the

acquisition date. We continue to collect information and reevaluate these estimates and assumptions periodically and record any adjustments

to preliminary estimates to goodwill, provided we are within the measurement period. If outside of the measurement period, any subsequent

adjustments are recorded to the consolidated statement of operations.

Fair

Value of Financial Instruments

Fair

value of financial and non-financial assets and liabilities is defined as an exit price, representing the amount that would be received

to sell an asset or paid to transfer a liability in an orderly transaction between market participants. The three-tier hierarchy for

inputs used in measuring fair value, which prioritizes the inputs used in the methodologies of measuring fair value for assets and liabilities,

is as follows:

Level

1 — Quoted prices in active markets for identical assets or liabilities

Level

2 — Observable inputs other than quoted prices in active markets for identical assets and liabilities

Level

3 — Unobservable pricing inputs in the market

Financial

assets and financial liabilities are classified in their entirety based on the lowest level of input that is significant to the fair

value measurements. Our assessment of the significance of a particular input to the fair value measurements requires judgment and may

affect the valuation of the assets and liabilities being measured and their categorization within the fair value hierarchy.

The

Company’s financial instruments consist of cash and cash equivalents, accounts receivable, and accounts payable. The carrying amount

of these financial instruments approximates fair value due to their short-term maturity.

The

Company’s contingent consideration in connection with the acquisition of Gameface was calculated using Level 3 inputs. The fair

value of contingent consideration as of July 31, 2023 and April 30, 2023 was $418,455 and $418,455, respectively.

The

Company estimates the fair value of its intangible assets using Level 3 assumptions, primarily based on the income approach utilizing

the discounted cash flow method.

The

Company’s derivative liabilities were calculated using Level 2 assumptions on the issuance and balance sheet dates via a Black-Scholes

option pricing model and consisted of the following ending balances and gain amounts as of and for the three months ended July 31, 2023:

SCHEDULE OF DERIVATIVE LIABILITIES

| Note derivative is related to | |

July 31, 2023

ending balance | | |

(Gain) loss for the

three months ended

July 31, 2023 | |

| 4/11/21 profit guaranty | |

$ | 1,456,854 | | |

$ | - | |

| 8/6/21 convertible notes | |

| 74,958 | | |

| (26,966 | ) |

| 6/17/22 underwriter warrants | |

| 4,966 | | |

| (1,565 | ) |

| 9/30/22 warrants issued with common stock | |

| 4,668,608 | | |

| (1,440,951 | ) |

| 1/6/2023 warrants issued with note payable | |

| 2,139,666 | | |

| (675,072 | ) |

| Total | |

$ | 8,345,052 | | |

$ | (2,144,554 | ) |

The

Black-Scholes option pricing model assumptions for the derivative liabilities during the periods ended July 31, 2023 and 2022 consisted

of the following:

SCHEDULE

OF DERIVATIVE AND WARRANTS GRANTED VALUATION USING BLACK-SCHOLES PRICING METHOD

| | |

Period Ended

July 31, 2023 | |

|

Period Ended

July 31, 2022 | |

| Expected life in years | |

| 0.7-10 years | |

|

| 4-4.3 years | |

| Stock price volatility | |

| 150 | % |

|

| 50-148 | % |

| Risk free interest rate | |

| 4.08%-5.37 | % |

|

| 2.90%-3.27 | % |

| Expected dividends | |

| 0 | % |

|

| 0 | % |

Income

Taxes

Income

taxes are accounted for in accordance with the provisions of ASC 740, Accounting for Income Taxes. Deferred tax assets and liabilities

are recognized for the future tax consequences attributable to differences between the financial statement carrying amounts of existing

assets and liabilities and their respective tax bases. Deferred tax assets and liabilities are measured using enacted tax rates expected

to apply to taxable income in the years in which those temporary differences are expected to be recovered or settled. The effect on deferred

tax assets and liabilities of a change in tax rates is recognized in income in the period that includes the enactment date. Valuation

allowances are established, when necessary, to reduce deferred tax assets to the amounts that are more likely than not to be realized.

Intangible

Assets

Intangible

assets relate to the “Slinger” technology trademark, which the Company purchased on November 10, 2020. The Company also acquired

intangible assets as a part of the Gameface acquisition. These intangible assets include tradenames, internally developed software, and

customer relationships. The acquired intangible assets are amortized based on the estimated present value of cash flows of each class

of intangible assets in order to determine their economic useful life. During the three months ended July 31, 2023, the Company impaired

their intangible assets down to a nominal value of $1,000 as the technology has changed and Management determined the value to be greater

than the fair value of those assets. Refer to Note 5 for more information.

Impairment

of Long-Lived Assets

In

accordance with ASC 360-10, the Company evaluates long-lived assets for impairment whenever events or changes in circumstances indicate

that their net book value may not be recoverable. Factors which could trigger impairment review include significant underperformance

relative to historical or projected future operating results, significant changes in the manner of use of the assets or the strategy

for the overall business, a significant decrease in the market value of the assets or significant negative industry or economic trends.

When such factors and circumstances exist, the Company compares the projected undiscounted future cash flows associated with the related

asset or group of assets over their estimated useful lives against their respective carrying amount. If those net undiscounted cash flows

do not exceed the carrying amount, impairment, if any, is based on the excess of the carrying amount over the fair value based on the

market value or discounted expected cash flows of those assets and is recorded in the period in which the determination is made. The

Company impaired $100,281 in intangible assets and $14,791 in fixed assets during the three months ended July 31, 2023. Refer to Note

5 for more information.

Goodwill

The

Company accounts for goodwill in accordance with ASC 350, Intangibles - Goodwill and Other (“ASC 350”). ASC 350 requires

that goodwill not be amortized, but reviewed for impairment if impairment indicators arise and, at a minimum, annually. The Company records

goodwill as the excess purchase price over assets acquired and includes any work force acquired as goodwill. Goodwill is evaluated for

impairment on an annual basis.

With

the adoption of the ASU 2017-04, which eliminates the second step of the goodwill impairment test, the Company tests impairment of goodwill

in one step. In this step, the Company compares the fair value of each reporting unit with goodwill to its carrying value. The Company

determines the fair value of its reporting units with goodwill using a combination of a discounted cash flow and a market value approach.

If the carrying value of the net assets assigned to the reporting unit exceeds the fair value of the reporting unit, the Company will

record an impairment charge based on the excess of a reporting unit’s carrying amount over its fair value. If the fair value of